Michael Vi

Palantir Technologies Inc. (NYSE:PLTR) is scheduled to report fourth-quarter earnings at the beginning of next week, and given the company’s history of significant profit misses in 2022, I believe Palantir’s stock is extremely vulnerable to another disappointment.

Palantir’s stock recently soared to more than $9, but this optimism, in my opinion, is misplaced given that Palantir’s fundamentals are deteriorating across the board.

Palantir’s stock is approaching the danger zone, with the stock experiencing renewed weakness in February and earnings expected to disappoint.

A History Of Profit Misses

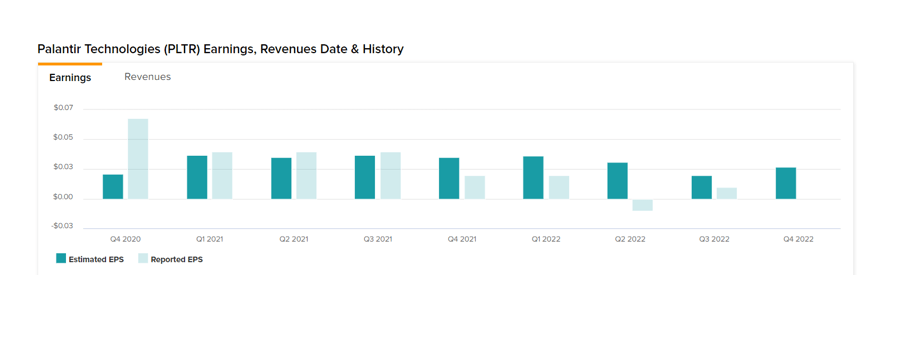

Palantir will release its 4Q-22 earnings report on Monday, February 13, 2023. Palantir has missed profit estimates four times in a row, including in the fourth quarter of last year.

The market expects $0.03 in 4Q-22, but given that Palantir has failed to meet expectations so frequently in 2022, indicating that investors tend to overestimate Palantir’s profit potential, I believe the odds are stacked against another profit miss next Monday.

Earnings (Palantir Technologies Inc)

Palantir’s Business Is Deteriorating

Palantir’s business was not on a good trajectory in 2022, and I doubt the company turned things around in the fourth quarter.

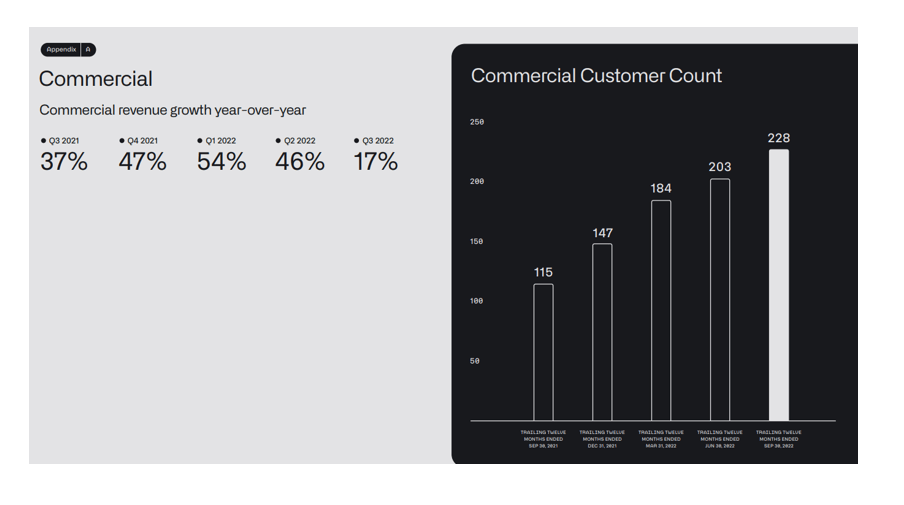

Palantir’s main problem in 2022 was that its heightened expectations for its commercial business could not be met. The commercial segment, which generated $204 million in sales (44% of total sales) in 3Q-22, experienced a significant slowdown, with segment sales falling from 47% in 4Q-21 to 17% in 3Q-22. Commercial sales are likely to have remained in the double digits in the fourth quarter, but investors should not expect a significant improvement.

Commercial Revenue Growth (Palantir Technologies Inc)

Palantir had to revise its sales growth guidance for 2023 because the commercial segment did not meet the company’s high expectations.

The Most Important Metric For Palantir: Sales Growth

Palantir’s stock suffered a setback when the company warned investors in the second quarter that sales growth would slow to 23% in 2022. Unfortunately, this meant that Palantir fell short of its much-touted 30% annual sales growth target, which was primarily what kept investors interested in the stock.

Given that consumer prices are still rising at significantly higher rates than in the past, and that tech companies are cutting jobs, I believe Palantir will fail to meet its 30% sales growth target in 2023. If Palantir forecasts less than 30% annual sales growth on Monday, I believe investors should brace themselves for the stock to retest its recent lows.

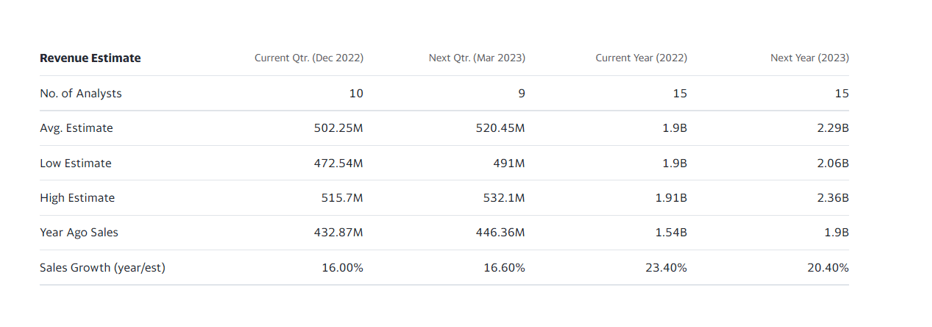

The market appears to have lost faith in Palantir’s ability to turn things around by 2023. Based on Yahoo Finance consensus estimates, the assumption is for only 20.6% sales growth this year, implying another 3 percentage point slowdown from Palantir’s guidance for 2022 sales.

Palantir has a sales multiple of 7.2x based on $2.29 billion in projected sales for 2023, and investors appear to be willing to pay this kind of sales multiple for a company that is incapable of producing profits.

Revenue Estimate (Yahoo Finance)

Palantir, in my opinion, will not report positive net income in the fourth quarter, as the company continues to struggle with high costs and inflated SBC expenses that benefit Alexander Karp and other senior executives more than shareholders.

Palantir Is Nearing A Danger Zone

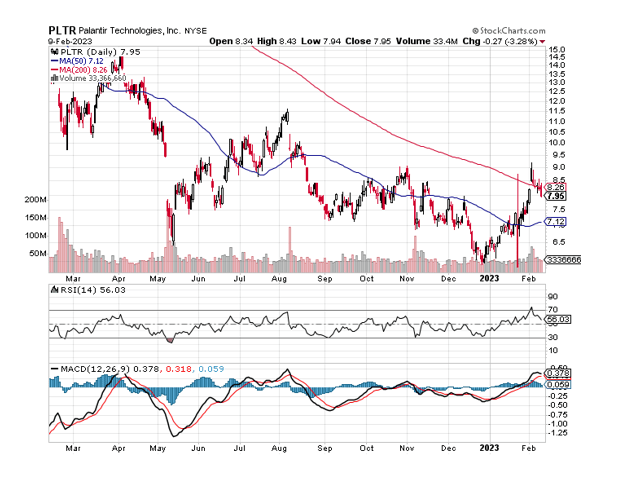

Palantir’s stock is approaching a catalyst event on Monday, and I believe it is at a risk. Palantir recently fell below the 200-day moving average line, signaling a short-term sell signal.

The next key level to watch is the 50-day moving average line, which is currently at $7.12. I believe this level will be broken on Monday if Palantir confirms my suspicion that sales growth will slow further in 2023.

The 50-day moving average line is currently 10% below Palantir’s stock price, so a retest is entirely possible in the next two to three trading days. If this 50-day moving average line is broken, the stock is in jeopardy, with an immediate drop to $5.84, Palantir’s most recent low.

Moving Averages (Stockcharts.com)

Why Palantir Could See A Higher Valuation

Palantir could theoretically report better-than-expected 4Q-22 earnings, reversing the company’s negative earnings surprise trend that it established throughout 2022.

A better-than-expected earnings report could boost Palantir’s price, but even in that case, I would remain skeptical given that Palantir is unlikely to be profitable on a net income basis in the fourth quarter.

If I had to guess about Palantir’s sales growth guidance, I’d say the company guided for less than 23% growth this year, despite the economy’s overall expected slowdown.

My Conclusion

Palantir’s stock price is falling ahead of its 4Q-22 earnings, and PLTR is approaching the danger zone.

If Palantir’s stock price falls below $7.12 in the short term, possibly as a result of Monday’s earnings release, the path is clear for a retest of Palantir’s low of $5.84.

Given Palantir’s track record of missed profit targets in 2022 and slowing sales growth throughout the year, I believe the odds are stacked against another disappointment on Monday.

With the stock already trading weakly ahead of earnings, it won’t take much to push Palantir’s stock price back into the danger zone.

Be the first to comment