naphtalina/iStock via Getty Images

What insiders bought in Q4?

We have once again analyzed thousands of S-4 fillings in the fourth quarter in order to find companies that have experienced periods of unusually concentrated purchasing activity by their corporate insiders. An emphasis was placed on firms that enjoyed buying across the board from multiple insiders in previously unrecorded quantities, often following a period of selloff. Our original thesis can be accessed through this link, and the last quarter update on the article can be read here.

Today’s article will focus its discussion exclusively on large-cap stocks, but the series will be followed up with a fourth-quarter installment covering popular small-caps and mid-caps as well. For the purposes of this analysis, we stand behind the definition of large-cap companies as publicly listed companies carrying a market capitalization larger than $10 billion. Below is our list of research-worthy large-caps that in our view enjoyed a period of unusual and atypical interest from corporate insiders. They are worthy of a further dive:

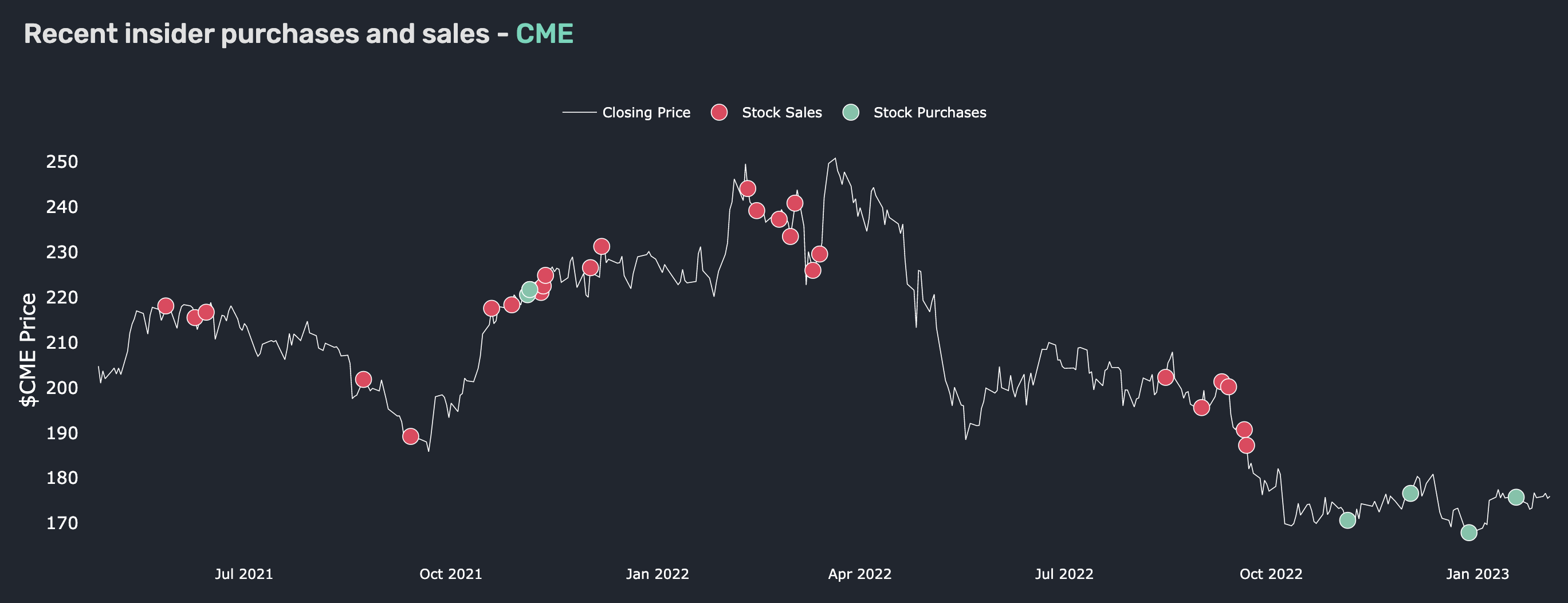

CME Group Inc. (CME)

-

Active Corporate Insiders: 2

-

One-Year Performance: -24.5%

- Total Bought Back: $8.3 million

CME is a global financial markets company. It operates one of the world’s leading derivatives exchanges, offering futures and options trading in a wide range of products, including interest rates, equity indexes, foreign exchange, energy, agricultural commodities, and metals. The firm is headquartered in Chicago, Illinois, and represents a dominant player in the derivatives market, with a long history of steady growth and profitability. CME traded for as high as $240 per share at the beginning of the last year and had a bumpy ride for the better part of the year, losing 23.73% on a one-year basis. The group is currently selling for an NTM P/E of 22.37x and an NTM EV/EBITDA of 19.73x. The firm is also offering a 2.35% dividend yield in hopes of sweetening the deal. Seeking Alpha Authors and Wall Street Analysts have a split view as far as the company is concerned. The first group of analysts has a much more negative outlook, assigning the company a “Hold” rating with an average score of 2.80/5.00. The street side analysts hold the company in much higher regard, assigning it a “Buy” rating with an average score of 3.88/5.00, just shy of a “Strong Buy” rating. Directors William Sheppard and Robert Tierney jumped on the opportunity to acquire cheaper CME shares, buying $8.3 million in the fourth quarter. The company currently trades at $184.10 per share.

CME Insider Activity (Quiver Quantitative)

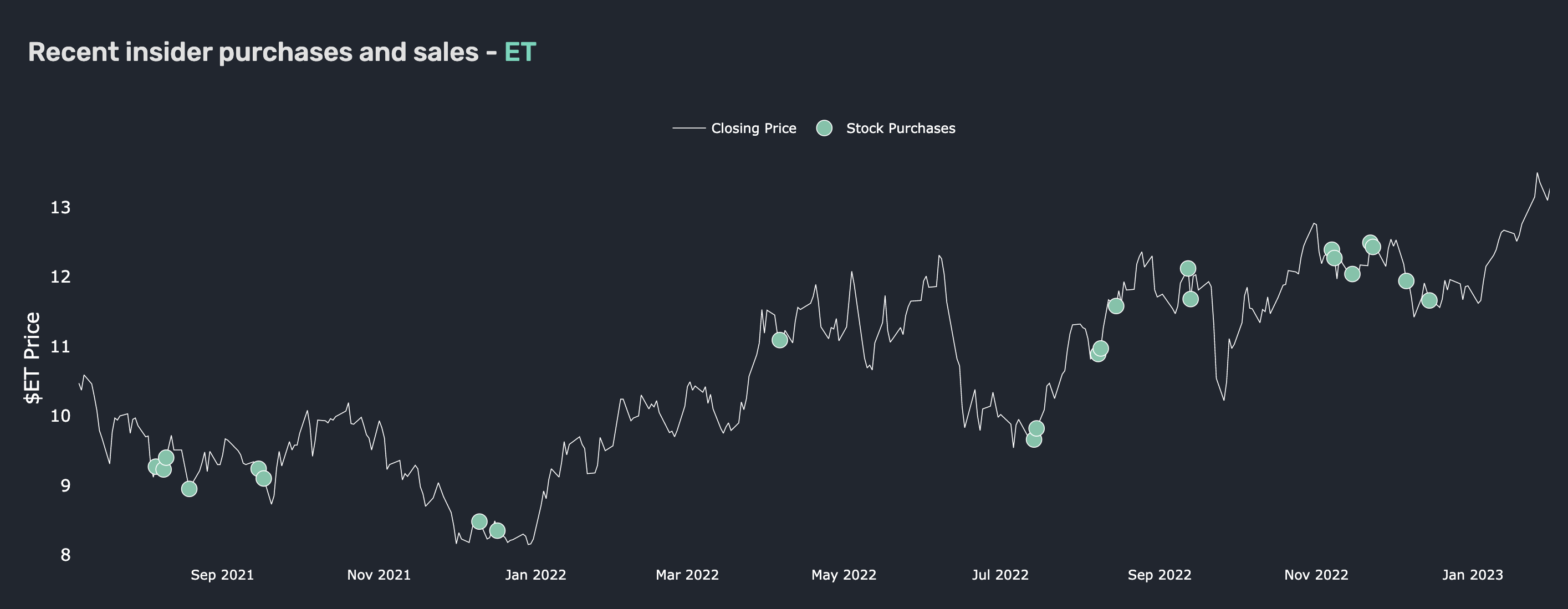

Energy Transfer LP (ET)

-

Active Corporate Insiders: 3

-

One-Year Performance: 28.4%

- Total Bought Back: $38.2 million

ET is the only candidate from last quarter’s list that made its way to our fourth-quarter article. Energy Transfer is a leading energy infrastructure company in the United States, operating approximately 120 thousand miles of pipelines and associated energy infrastructure in 41 different states. It operates a vast network of pipelines, storage facilities, and terminals that transport and store natural gas, crude oil, and refined petroleum products. Energy Transfer has a diverse portfolio of assets and is involved in various aspects of the energy industry, including production, processing, storage, and transportation. As mentioned before, ET has enjoyed years of confidence from its insiders, who have managed to build up close to a 25% ownership stake in the company. Insiders that bought shares in the third quarter are already up some 11% on their investment. After outperforming the market by a significant margin last year, ET is off to a strong start once more, delivering a 7.5% year-to-date return. Strong operational results brought the company to a very attractive valuation, as it currently trades at an NTM EV/EBITDA of 7.77x, an NTM P/E of 9.49x, and an NTM MC/FCF of 7.02x. On top of that, the company offers a 9.55% dividend yield. Both Seeking Alpha Authors and Wall Street Analysts upheld their bullish views on the stock, rating it “Buy” and “Strong Buy”, respectively. For the fourth quarter, EVP and former CFO Bradford Whitehurst, Executive Chairman Kelcy Warren, and Director Richard Brannon purchased $38.2 million worth of ET stock. The estimated average purchase price was $11.50 per share. This is on top of the $54.8 million they bought last quarter. ET is currently selling at $12.84.

Energy Transfer Insider Activity (Quiver Quantitative)

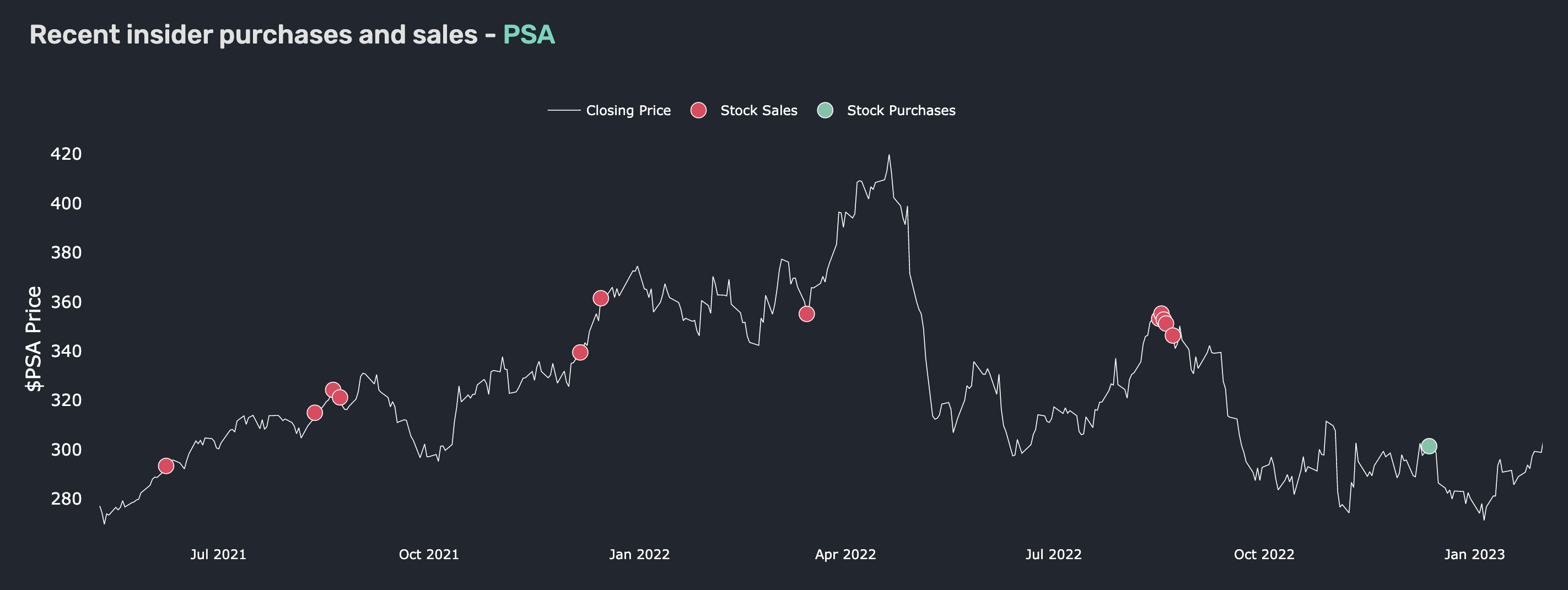

Public Storage (PSA)

-

Active Corporate Insiders: 1

-

One-Year Performance: -16.48%

- Total Bought Back: $748,550

Public Storage is the only REIT on our list today. It represents the largest self-storage company in the world, with over 2,780 locations in the United States and Europe. PSA was founded in 1972 and is headquartered in Glendale, California. Public Storage offers self-storage units for personal and business use, as well as vehicle storage options. The company operates on an interesting rental model, where tenants pay monthly fees for the use of their storage units. Public Storage is known for its extensive real estate portfolio, customer-focused approach, and commitment to providing high-quality storage solutions. As a result, it was well positioned to withstand the 2022 pressures and remains one of the few REITs to outperform the S&P 500 (SPY). Current year-to-date performance is also exemplary, as the REIT is already up 7.0% at the time of writing this article. However, the valuation was, and still is, somewhat steep. The California-based REIT is currently being sold for an FWD P/FFO of 19.21x, which constitutes a premium in the sector. It does however offer a very attractive dividend yield of 3.97%. The overall consensus as far as Seeking Alpha Authors are concerned puts the company amongst the “Hold” recommendations. Wall Street Analysts do not necessarily share this opinion, assigning the company a “Buy” rating with an average score of 4.00/5.00. In the fourth quarter, CEO Joseph Russell bought 2500 shares, or about $750 thousand worth of PSA shares at an estimated average price of $308.00 per share. The REIT is currently selling at $299.91 per share.

PSA Insider Activity (Quiver Quantitative)

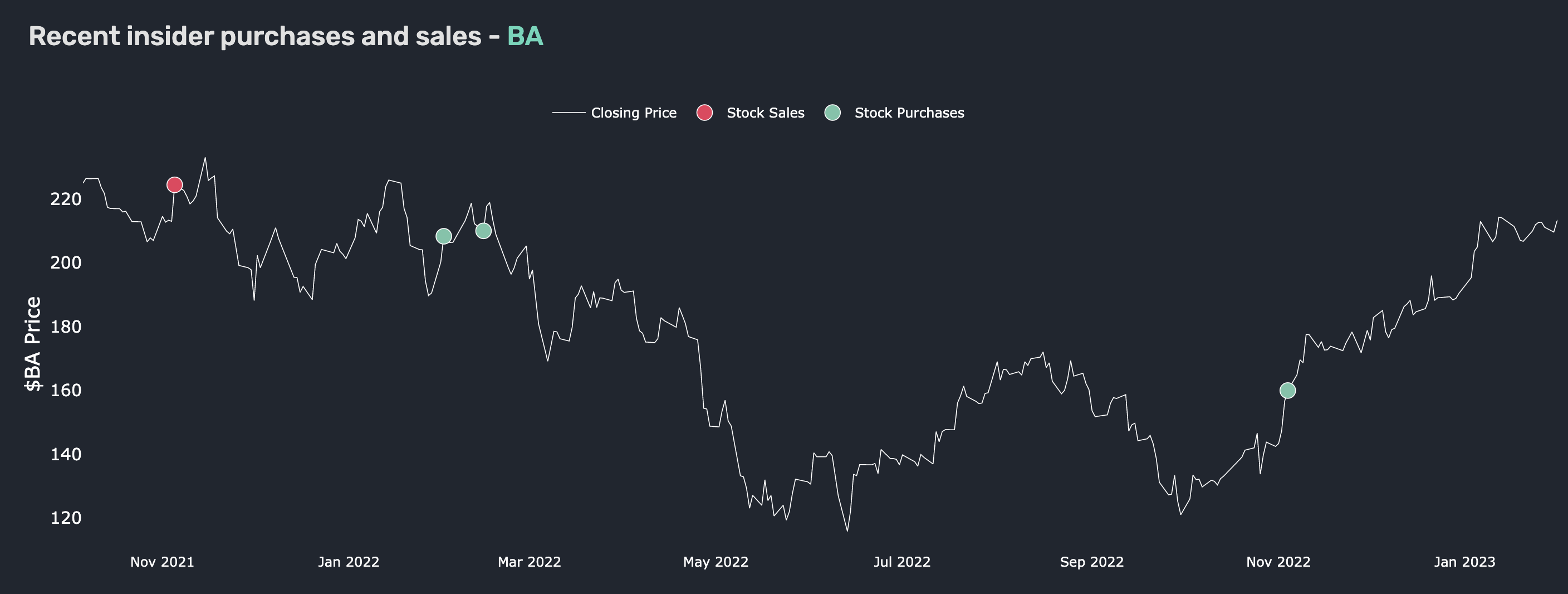

The Boeing Company (BA)

-

Active Corporate Insiders: 2

-

One-Year Performance: -2.68%

- Total Bought Back: $4.2 million

Boeing Company is the leading aerospace and defense company in the world and was founded all the way back in 1916. Since then, the Illinois-based company has become one of the largest manufacturers of commercial jetliners and military aircraft. Boeing is also a major player in the space industry, providing a range of products and services for satellite and space exploration. The company operates through two main divisions: Commercial Airplanes and Defense, Space & Security. Despite facing some challenges in recent years, including the grounding of its 737 MAX aircraft following two fatal crashes, BA continues to be a major player in the aerospace industry, with a strong portfolio of products, a long history of innovation, and a commitment to advancing the field of aviation. Boeing has largely traded flat for the better part of the year. It has returned a respectable 7.70% year-to-date. BA trades at a noticeable premium with an NTM EV/EBITDA of 31.50x and an NTM P/E of 29.85x. Overall, the analyst consensus for SA authors sees the company as a “Hold”. Wall Street is much more bullish and rates the stock as a “Buy” with an average score of 4.26/5.00. Active corporate insiders in the fourth quarter were CEO David Calhoun and Director Steven Mollenkopf. They bought back 26,285 or $4.2 million worth of BA shares for an average estimated price of $157.5. The company is currently trading at $212.89 per share.

BA Insider Activity (Quiver Quantitative)

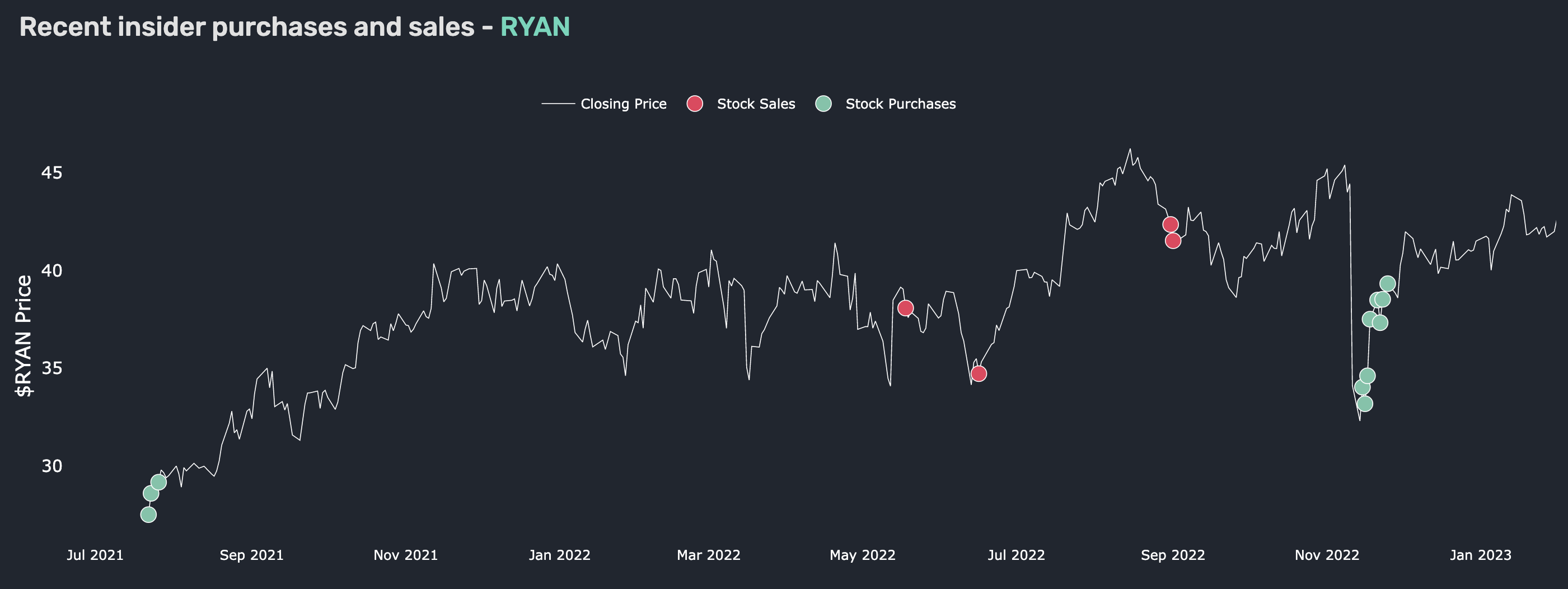

Ryan Specialty Holdings (RYAN)

-

Active Corporate Insiders: 2

-

One-Year Performance: 6.75%

- Total Bought Back: $55 million

RYAN is yet another Chicago, Illinois-based company on today’s list. It is a specialty insurance and services company founded in 2010. It is in the business of providing a range of insurance and risk management products and services to clients in the specialty insurance industry, including distribution, underwriting, product development, administration, and risk management services. They have been acting both as wholesale brokers and managing underwriters. Ryan Specialty Holdings held its initial public offering in late 2021 and achieved respectable results, almost doubling its IPO price in the few years since. Insiders used a temporary selloff to start accumulating a large position in the company. RYAN is currently being valued by the market at an NTM EV/EBITDA of 11.17x and an NTM MC/FCF of 14.44x. Seeking Alpha Authors rate the company as a “Buy”, with an average score of 4.00/5.00. Wall Street Analysts on the other end share a similar sentiment, assigning RYAN a “Buy” rating with an average score of 3.90/5.00. In the fourth quarter, shares of Ryan Specialty Holdings were bought by the CEO Patrick Ryan and Director Michael O’Halleran. Together, they bought more than $55 million of RYAN stock at an estimated average price of $36.0. The firm is currently selling for $42.71 per share.

RYAN Insider Activity (Quiver Quantitative)

Final Arguments

As the last market bell for 2022 was heard and all the tallies had been accounted for, it became clear that the market just returned a mind-boggling -19.95% YTD in what ended up being the worst investing year since the 2008 financial crisis. It is quite likely that the average retail investor returned far less than that. The year has been marked by what seemed to be an ever-deteriorating macroeconomic situation, with the economy being ravaged by surging inflation, rising interest rates, an energy crisis, as well as the largest European conflict in modern history. The insider purchases on this list have been made exactly at the culmination of that situation, just as the sentiment began to swing. As such, the highlighted purchases should be considered that much more important as candidates possibly worthy of further research.

Be the first to comment