guvendemir/E+ via Getty Images

After the fall of the Soviet Union, the world entered an era of relative peace and prosperity. For nearly 30 years, we’ve experienced the rise of living standards across the globe, as cross-border trade and trading agreements were shown to be more effective than war in achieving national interests at that time. However, that era is coming to an end. The start of a major pandemic, Russia’s invasion of Ukraine, and China’s more aggressive posturing in the Indo-Pacific region in recent years highlighted the vulnerabilities of our current supply chains, which we built in recent decades as a result of globalization.

The current relatively high prices for commodities along with the ongoing supply disruptions show the need for the development of more protectionist trade policies that encourage the shortening of supply chains in order to decrease the exposure to non-allied third parties, which don’t share the same values, view the world differently, and could pose a major threat in the foreseeable future. As we enter this new reality, which is in the midst of a bifurcation of the global system, we as investors should start preparing our portfolios to meet the new challenges that arise from the changing geopolitical landscape.

That’s where Palantir (NYSE:PLTR) comes into play. For nearly two decades, the company has been actively strengthening its ties with American federal agencies by providing its custom software solutions for various needs ranging from border protection to geospatial intelligence. At the same time, Palantir has been actively expanding to different markets such as the UK, France, and Germany, all of which are allies of the United States and are part of a single NATO military bloc. As the U.S. plans to mitigate the Chinese threats in the Indo-Pacific region, while Europe starts to decouple from Russia, Palantir has the opportunity to strengthen its ties with the western governments and military-industrial complexes, which would result in the creation of an additional shareholder value in years to come.

A Storm Is Brewing

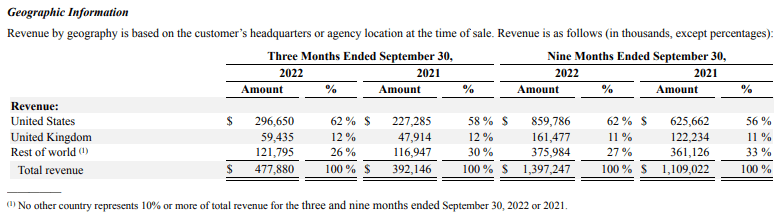

Recently, I wrote an earnings preview article on Palantir, in which I outlined what investors should expect from the Q3 results that came out a week ago. What we saw from a report is that despite all the macroeconomic troubles, which forced companies to scale down their operations, Palantir nevertheless managed to aggressively grow its business, as its revenues of $477.88 million in Q3 were up 21.9% Y/Y. What’s also important to note is that the company’s governmental business also showed an outstanding performance in comparison to relatively weaker performances in Q1 and Q2, and was able to grow its revenues by 26% Y/Y in Q3 to $274 million, while also passing the $1 billion revenue threshold in the last twelve months.

Considering those numbers, it’s safe to say that the demand for Palantir’s governmental solutions is significant, and is more than likely to increase as we enter a new geopolitical reality. In my previous article on the company, I’ve already stated how the U.S. defense spending for 2023 is about to be the biggest in its history and is forecasted to increase even more in the years ahead. In the last couple of months alone, Palantir managed to receive record contract awards from various federal and defense agencies to help them enhance their software capabilities. Those contracts, such as the $95.9 million contract with Homeland Security, the $229 million one-year contract extension with the U.S. Army Research Lab, the $59.1 million Army contract, and the $85.1 million contract with the U.S. Army Materiel Command, reveal the increased influence that Palantir has within the U.S. military-industrial complex. As such big contracts continue to be awarded, it’s more than likely that the company’s business would continue to generate aggressive returns and would also be able to increase the annual revenue per governmental customer, which stood at $9 million at the end of September.

At the same time, as the U.S.-China systemic rivalry intensifies, Palantir is well-positioned to capitalize on the increase in tensions. The company has no exposure to China or any other U.S. adversaries and it also has the ability to help the military to actively monitor the movement of Chinese vessels and planes in the Indo-Pacific region, and in the South China Sea in particular. Thanks to this, Palantir is likely going to become a crucial element in helping the U.S. to contain the Chinese threats in the region and at the same time help the Department of Defense to achieve its own goals there, which were outlined in the latest 2022 National Defense Strategy report. It also seems that Palantir’s CEO Alex Karp himself supports this thinking considering that in his latest shareholder letter where he discussed the strength of the company’s defense business he stated the following:

We furthermore do not view the increase in contract value this quarter as an aberration but rather as a sign of a more fundamental shift in our business, from insurgent outsider to incumbent, particularly in the U.S. market.

On top of that, Palantir has also been actively increasing its presence in other allied markets such as the UK, France, and Germany. The United Kingdom in recent years has become its second-biggest market after the United States, and the company has all the chances to expand its presence there if it manages to secure a £360 million contract from the NHS in the following months. In addition, earlier this year the company managed to secure a $26.2 five-year contract with the German police, which marked one of its first major expansions in the country, while its cooperation with the French military-industrial complex in the last year has accounted for 6% of its total revenues.

Palantir’s Sales By Region (Palantir)

Considering all of this, it’s safe to say that Palantir is well-positioned to tackle all the challenges and seize all the opportunities that come with this changing geopolitical landscape, which should lead to the creation of shareholder value in years to come. That’s why I continue to believe that the company’s stock offers a decent upside for investors at the current levels, especially since it has no debt on its balance sheet, $2.4 billion in liquidity, and $4.1 billion in remaining deal value at the end of Q3. At the same time, the continued growth of its commercial offerings, which I plan to outline in my other article on the company, only strengthens the bullish thesis.

As for the value itself, Palantir’s management didn’t make any major changes to the top-line projections from the last quarter and it still expects to generate ~$1.9 billion in revenues in FY22. As such, my DCF models from the past don’t require any serious revisions for now, and in the base case and an optimistic case continue to show Palantir’s fair value to be $10.03 per share and $12.08 per share, respectively, which implicates a decent upside in both scenarios.

Risks

There are two major risks concerning the bullish thesis and Palantir’s governmental business in particular. First of all, during the Obama administration, U.S. defense spending was below the average, which prevented the aggressive growth of companies within the military-industrial complex. While that’s not the case right now, there’s always a possibility that in a few years things will dramatically change and Russia along with China would no longer pose a threat to the U.S. interests due to their own internal issues. Even though it’s hard to see this happening right now, the decline of the Soviet Union in the past wasn’t expected as well, but it nevertheless started gradually and then happened suddenly.

With Russia’s failure to achieve any strategic objectives in Ukraine and losing 50% of the territory that it occupied before, Ukraine could become Russia’s second Afghanistan, which kicked off the dissolution of the Soviet Union in the past. In case that happens, there’s always a possibility that the U.S. would pivot to dealing with its internal issues and stops spending so much in the military as was the case a decade ago.

Secondly, since it appears that the global recession is around the corner, there’s always a possibility that Palantir’s stock would continue to trade at a distressed territory for a while until the Federal Reserve changes its course and stops raising rates and engaging in a quantitative tightening. As a result, the fundamentals and any aggressive growth of its businesses won’t matter until things normalize on a macroeconomic level.

The Bottom Line

As the world is changing, Palantir has a unique opportunity to help western governments and their defense industries to better prepare for the new reality. The latest earnings results proved that despite all the risks the company’s governmental business is still able to generate aggressive Y/Y returns and the latest contract awards along with the increase in defense spending make me believe that Palantir’s software would continue to be in high demand for years to come. This in the end could potentially lead to the creation of additional shareholder value and an appreciation of the company’s stock in years to come.

Be the first to comment