Andreas Rentz

Investment Thesis

Palantir (NYSE:PLTR) is a leading software company helping organizations to make sense of the massive amounts of data they ingest on a daily basis – transforming this from billions of data points into actionable information. It started off predominantly by serving governments, but in recent years Palantir has been expanding rapidly into the commercial market, opening up a much larger opportunity.

Palantir Q2’22 Business Update

My investment thesis for Palantir is the following: the amount of data that businesses have to work with is only going to increase exponentially, and they need a way of coping with this data and making use of it – this is where Palantir comes in. I want to see continued expansion within commercial customers, a strong dollar-based retention rate implying high switching costs, and continued execution of Palantir’s ‘land and expand’ strategy, as well as margins improving over the long term.

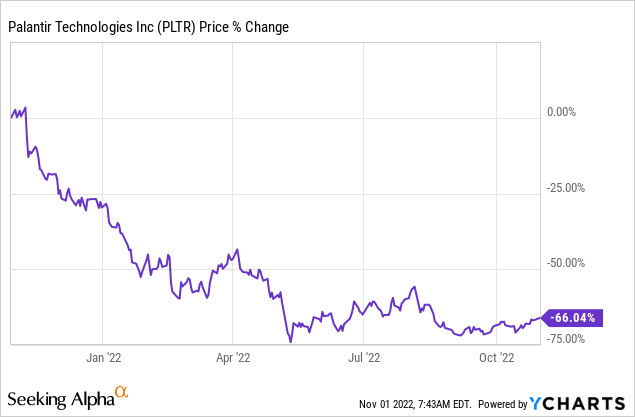

Unfortunately for Palantir shareholders, 2022 has been a pretty painful year so far. The company underwhelmed investors with its Q2 earnings report, offering up extremely soft Q3 guidance and reducing its full year revenue outlook. Shares reacted by falling 15%, compounding on the misery that shareholders have been feeling all year after seeing the stock tumble 65% in the last twelve months.

Yet the long-term thesis for Palantir remains very much intact. It’s also worth remembering that the contracts Palantir signs with its customers are pretty huge, so the timing of these contracts can cause revenue to be quite lumpy on a quarter-to-quarter basis, which goes some way to explaining the slowdown in management’s Q3 guidance.

A few months have passed and Palantir’s Q3 results are just around the corner. The question is whether or not investors will be in for more pain, or if expectations have got so low for Palantir’s results that the slightest bit of good news will be met with positivity from Wall Street? Let’s see at what investors should look out for when Palantir reports next week.

Latest Expectations

Palantir is set to report its Q3 earnings on Monday, November 7, before the market opens, and there are several key items that investors should keep their eyes on.

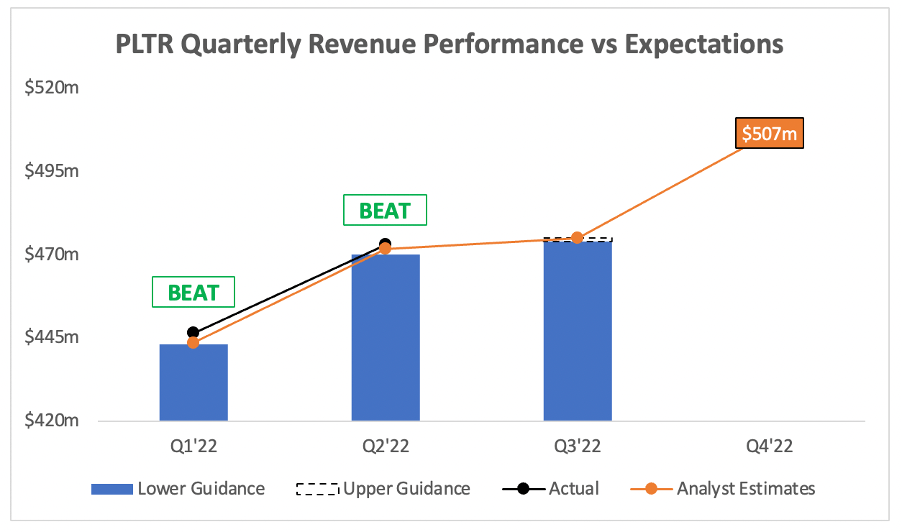

Starting with the headline numbers, analysts are expecting Q3 revenue of ~$475m, representing YoY growth of 21.1%. This expectation is at the top end of management’s guidance of $474-$475m. As the graph below shows, Q3 revenue of $475m would represent virtually zero sequential growth from Q2 to Q3, with revenue increasing by only 0.4% – this is certainly not what investors would expect from a ‘growth’ company such as Palantir, and it’s part of the reason why shares cratered after its Q2 earnings report.

Seeking Alpha / Palantir / Author’s Work

As mentioned, Palantir’s revenue from quarter-to-quarter can be quite lumpy due to the nature of its large, government contracts, and this is part of the reason why the Q3 revenue guidance was so poor, as Chief Legal and Business Affairs Officer Ryan Taylor outlined on the earnings call:

Across government and commercial, the opportunity in front of us is enormous, which makes the revised near-term outlook, all the more disappointing. It doesn’t come close to representing our ambition and the opportunity before us.

While the timing of large contracts in government can be frustrating, the underlying requirements and needs are enduring. It’s worth noting that our revised guidance excludes any new major U.S. government awards.

This volatile revenue growth is something Palantir investors have to accept (even if the market doesn’t), with the understanding that as long as the business is succeeding, these fluctuations will balance out in the long-term. The problem is that it can be difficult to know whether or not the slowdown is in fact caused by contract timing, or if there are underlying problems with the business – and, frankly, only time will tell.

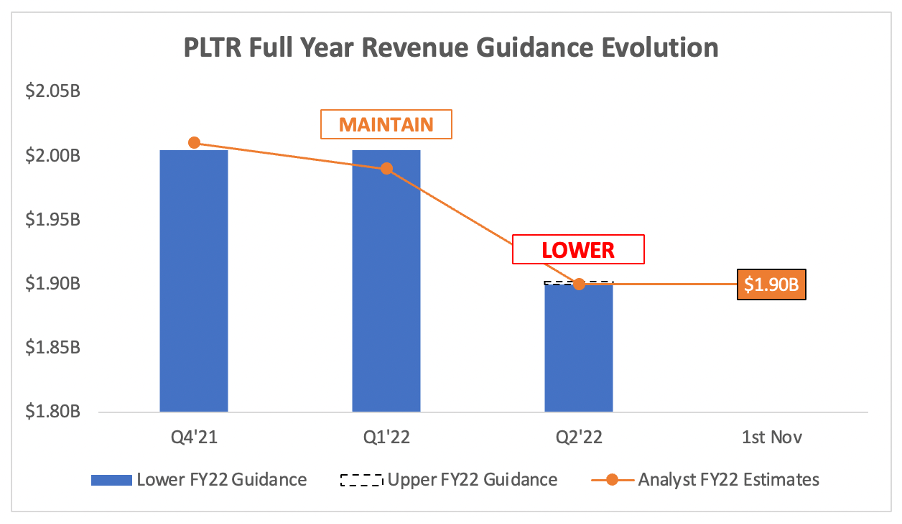

This uncertainty surrounding government contracts caused Palantir to lower its full year revenue guidance as well, moving from $2.004B in Q1’22 to $1,900-$1,902B in Q2’22. Wall Street has listened to these expectations, and expects exactly $1.9B in full year revenue for Palantir.

Seeking Alpha / Palantir / Author’s Work

It’s worth noting that Palantir’s Q3 and full year revenue guidance excludes ‘any new major U.S. government awards’, so there is ample opportunity for Palantir to exceed analysts’ expectations when it reports. For example, Palantir announced at the end of September that the U.S. Army Research Lab extended its contract, with the new contract being worth up to $229m over one year – this won’t materially impact Q3 results, but may well boost Palantir’s outlook for Q4.

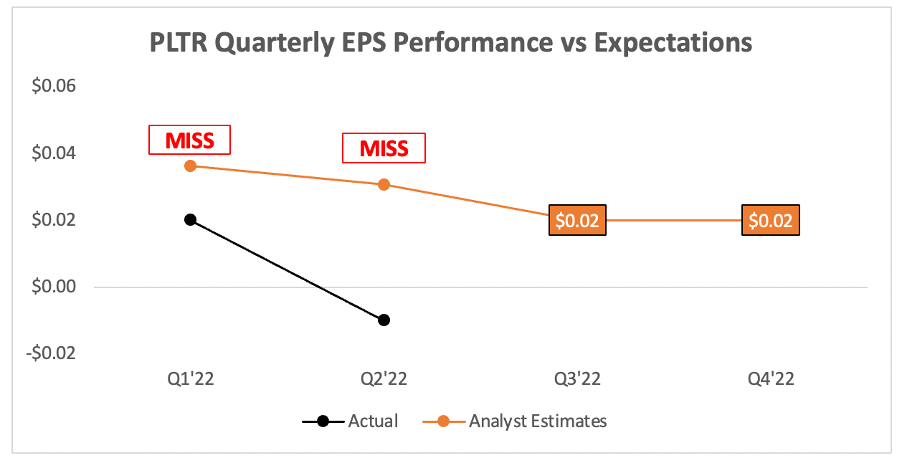

Taking a quick look at the bottom line, analysts are expecting Palantir to deliver EPS of $0.02.

Seeking Alpha / Author’s Work

The company missed analysts’ expectations on earnings in Q1 and Q2 this year, but I’m not too concerned; it continues to churn out free cash flow, and it doesn’t give EPS guidance anyway. It is, however, still worth watching for investors in order to gauge Palantir’s cost-control ability, but there isn’t anything here to worry me.

Besides the headline figures, what else should investors look at when Palantir reports?

Key Metrics To Watch In Palantir’s Q3 Earnings

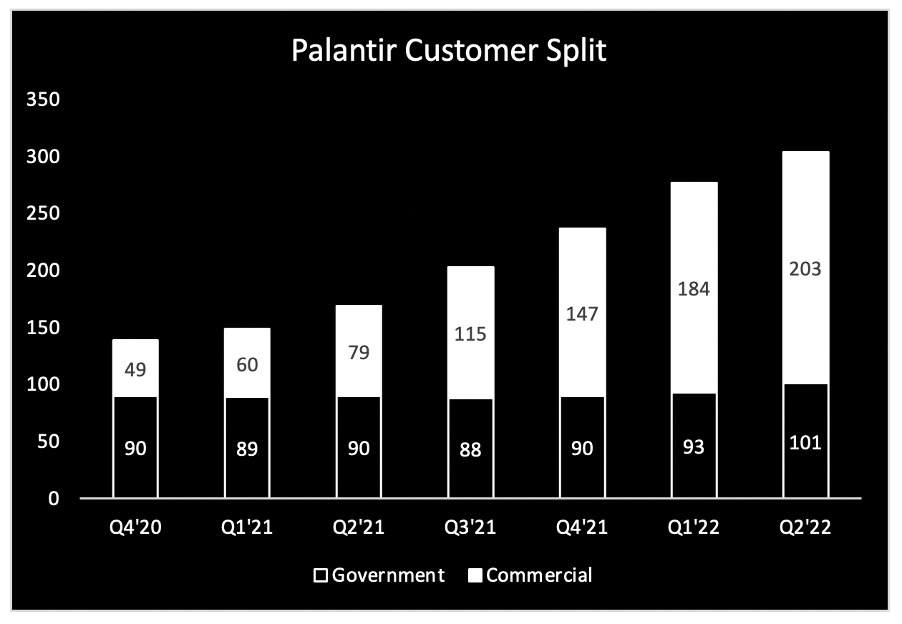

A cornerstone of my investment thesis in Palantir is the company’s ability to expand beyond its government customers and into the commercial market, since I believe there is a substantially larger opportunity if it can gain commercial traction. As per the below chart, Palantir has been doing just that over the past year or two, however the sequential growth rate in Q2 of just ~10% for commercial customers indicated a sharp slowdown.

Palantir / Author’s Work

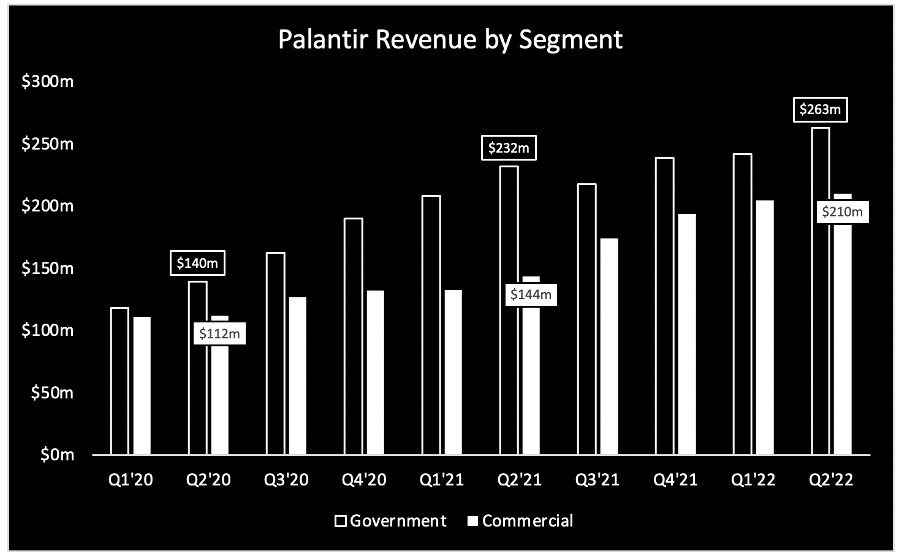

On the plus side, Palantir has seen incredible momentum in the U.S. commercial market, with revenues growing 120% YoY in Q2 from $39m to $86m. This commercial momentum is what drove Palantir forward over the past year, with Q2 commercial revenues growing 46% YoY compared to just 13% growth from government revenues.

Palantir / Author’s Work

It’ll be interesting to see exactly how this trend plays out in Q3, but I personally will be disappointed to see a substantial slowdown in commercial momentum. I understand that we’re in a difficult macroeconomic environment, so I am prepared for a slight slowdown, but the above graph shows that the rapid growth in commercial revenues have been driving Palantir forwards – if this starts to falter, Q3 may not paint a pretty picture.

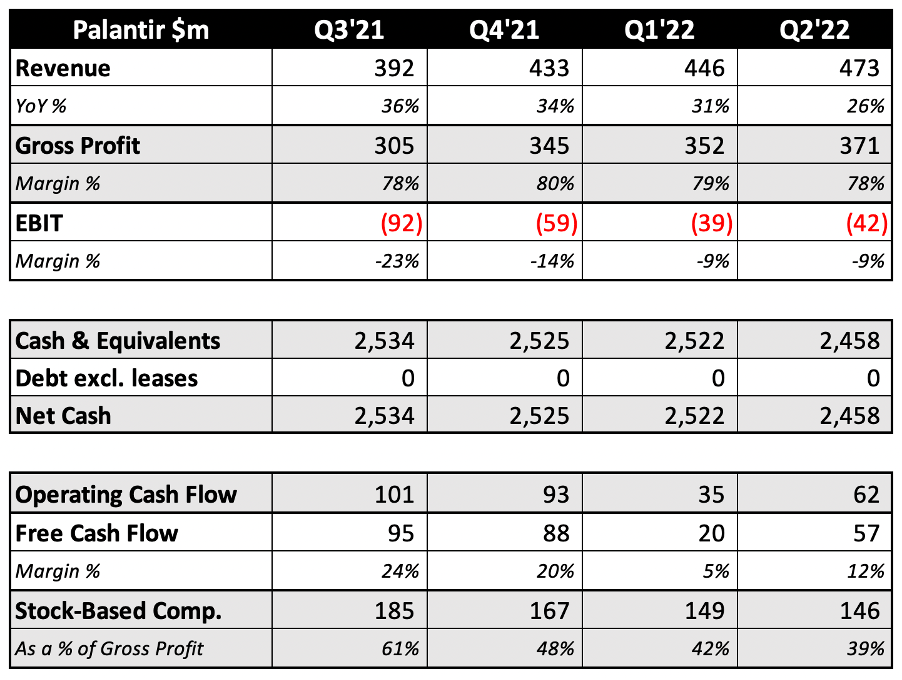

Quick Take: Palantir’s Core Financial Metrics

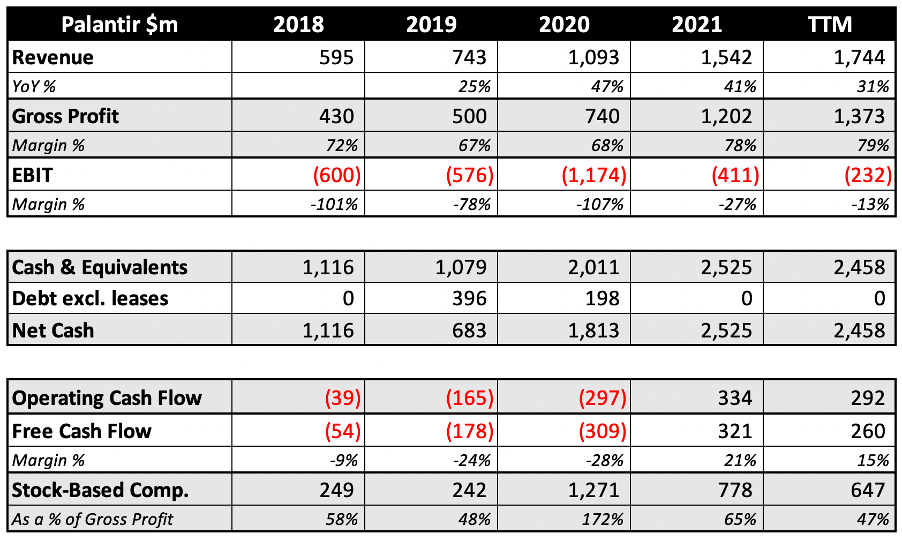

The deceleration of Palantir’s revenues is extremely apparent in the below table, with revenue over the past 12 months only growing 31% YoY compared to 41% in 2021. On the plus side, Palantir’s insane EBIT margins in 2020 of -107% have improved greatly, and are now just -13% over the past 12 months; which remains a substantial improvement from the -27% in 2021.

Author’s Work

The company continues to have an extremely strong balance sheet, with net cash of almost $2.5 billion, and remains free cash flow positive – so, no risk of Palantir running into financial difficulties any time soon. Stock-based compensation as a percentage of the total gross profit has also declined rapidly (phew!), although it still accounts for a whopping 47% of gross profits over the past 12 months.

Taking a look at the quarterly metrics below should give investors more of an indication of Palantir’s current direction, but I’ll do a very quick summary.

Author’s Work

The good: consistently strong gross profit margins, negative EBIT margins down into the single digits, balance sheet remains extremely strong, and stock-based compensation is consistently falling.

The bad: revenue growth is declining rapidly (and Q3 guidance implies that this decline will continue), and free cash flow margins are worsening, at least in part due to the declining revenue growth.

If you take out the sharp revenue decline, then I would say that Palantir’s financials are heading in the right direction fast. The main issue is that Palantir is a growth story, and so investors cannot ignore the slowing revenue growth; so, investors will be hoping that Q3 shows signs of continuing commercial momentum, and perhaps more optimism on the government side than management alluded to in Q2.

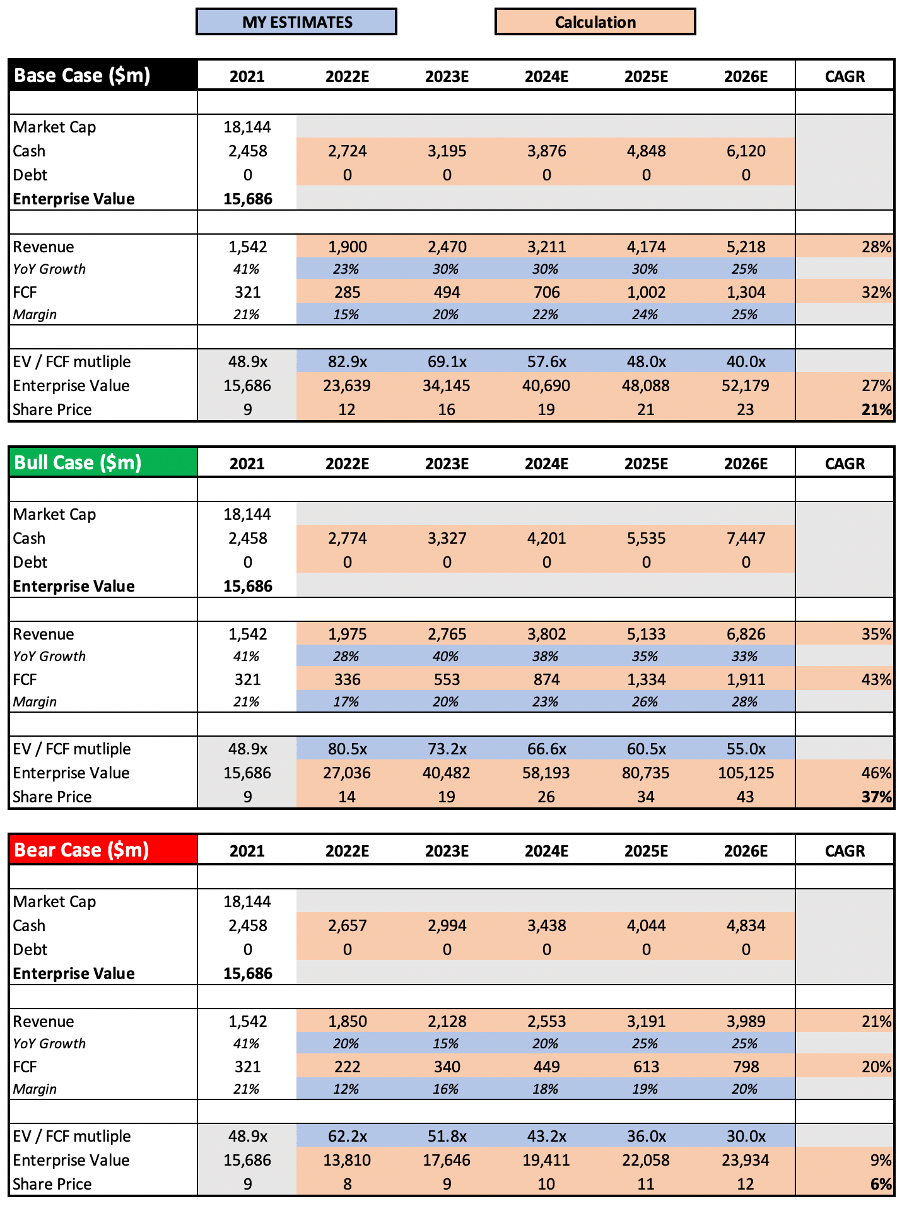

PLTR Stock Valuation

As with all high growth, disruptive companies, valuation is tough. I believe that my approach will give me an idea about whether Palantir is insanely overvalued or undervalued, but valuation is the final thing I look at – the quality of the business itself is far more important in the long run.

Author’s Work

I have kept my model virtually the same as in my previous article, with a few slight tweaks to the 2026 FCF / EV multiple in order to be a bit more conservative in my base and bear case scenarios.

Put that all together, and I can see Palantir shares achieving a CAGR of 6%, 21%, and 37% in my respective bear, base, and bull case scenarios. Whilst it has been a tough year for the business, if it achieves its frequently stated aim of ‘at least 30% annual revenue growth through to 2025’, then the current share price appears to be very attractive.

Bottom Line

Q3 earnings will be crucial for Palantir, because there are plenty of yellow flags that could turn into red flags, such as slowing commercial customer acquisition and the sharp decline in revenue growth. I will cut the company some slack due to the difficult macroeconomic environment, since cost-cutting companies may not be willing to undertake large transformational projects until there is more certainty in the economy.

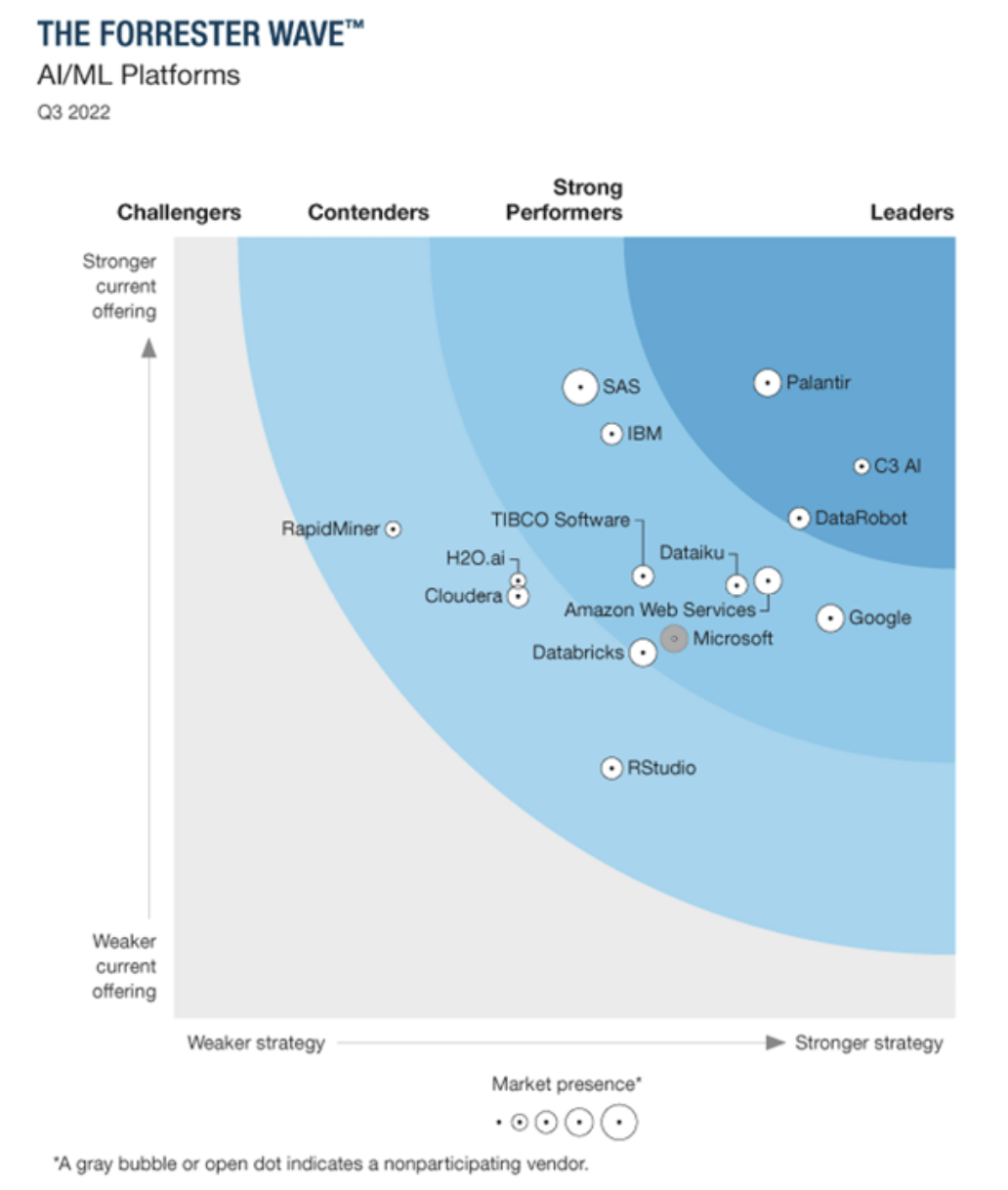

Yet investors can also find plenty of reasons to be optimistic, not least because Palantir was recently named as a leader in the Forrester Wave Report for AI / ML Platforms – ahead of the likes of IBM (IBM), Google (GOOGL) (GOOG), Amazon’s AWS (AMZN), and Microsoft (MSFT). This should give investors some comfort in the quality of Palantir’s platform, and I believe that when organizations are looking to undergo this level of transformation, they would prefer to go with the best offering out there.

Forrester Wave

Personally, I remain cautiously optimistic about Palantir. The company is very well set up for a decade of success, even if it is currently hitting some bumps in the road (that are at least partially macro-induced). It has a stellar balance sheet, is free cash flow positive, has an industry leading product in a growing market with tons of optionality, and the current share price is very attractive.

Given all this, I will reiterate my previous ‘Buy’ rating on Palantir shares, and look forward to hearing management’s latest update on the business when Q3 earnings come round next week.

Be the first to comment