andreswd

The Company

Founded in 2006 and headquartered in São Paulo, Brazil, PagSeguro Digital Ltd. (NYSE:PAGS) is a $3.9-billion market cap Brazilian fintech company providing a digital ecosystem for financial solutions. Their offerings include the PagSeguro Ecosystem, PagBank digital account, and PlugPag for merchants. They offer cash-in solutions, payment tools, online gaming, and cross-border services. The company issues prepaid, credit & cash cards, along with various features like purchase protection and antifraud platforms. Additionally, they provide back-office solutions and gateway services for credit card processing.

PagSeguro’s IR materials

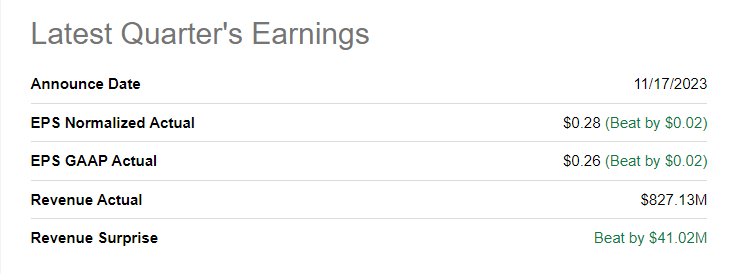

In Q3 2023, PagSeguro reported its highest-ever net income, both GAAP and Non-GAAP. Non-GAAP net income reached 440 million BRL, growing by 7% YoY. Despite an expanding footprint in larger merchants, which contributed to higher gross profit but with lower take rates, the company’s margins improved, resulting in an EBITDA of 894 million BRL, the highest margin since Q3 FY2021. Total revenue was stable YoY and grew by 5% QoQ, reaching 4.0 billion BRL. So in terms of both top line and bottom line – when converted to US dollars – the firm beat the consensus in Q3, according to Seeking Alpha:

Seeking Alpha data

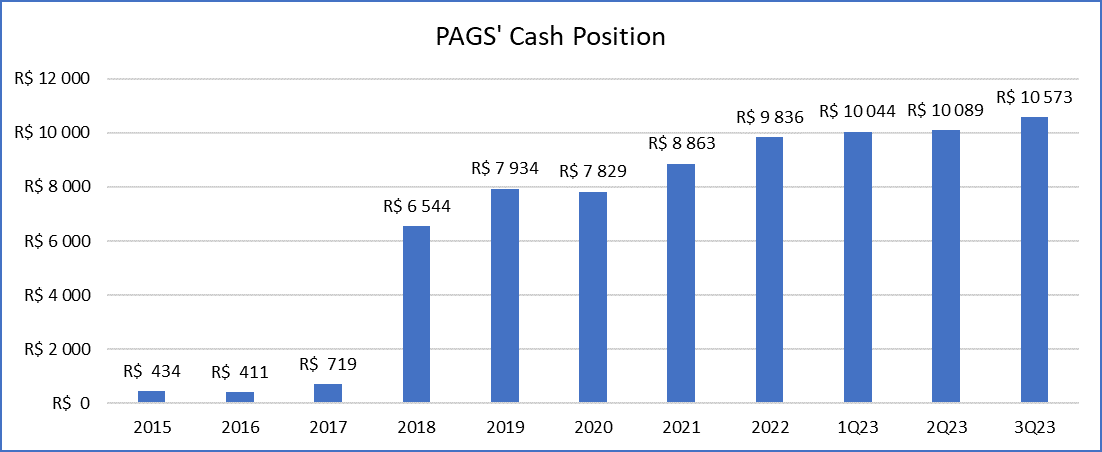

The company highlighted disciplined CapEx deployment, leading to a net cash balance of 10.6 billion BRL at the end of the quarter, a 17% increase from the previous year. The financial services segment showed positive results, with continued credit underwriting efforts, collateralized product offerings, and growth in revenues despite the impact of an interchange cap.

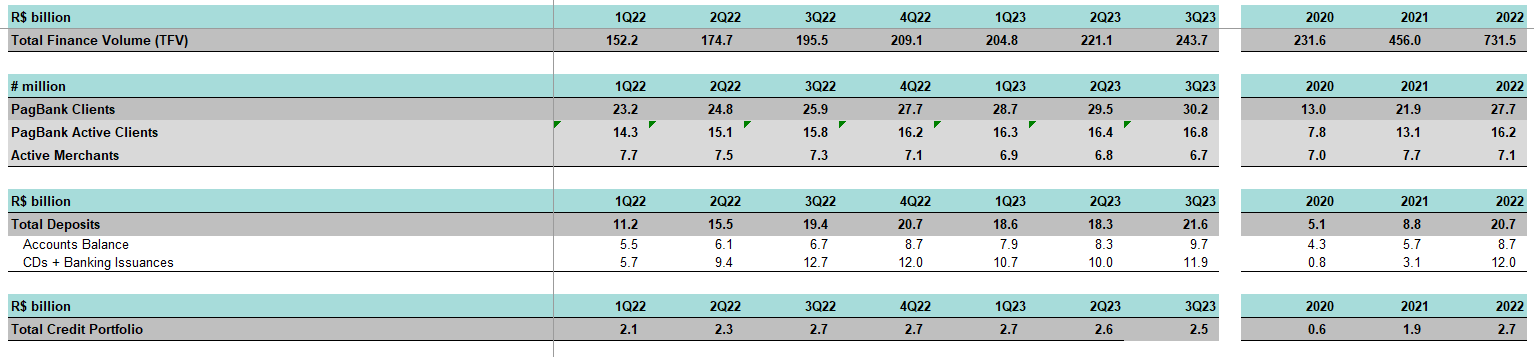

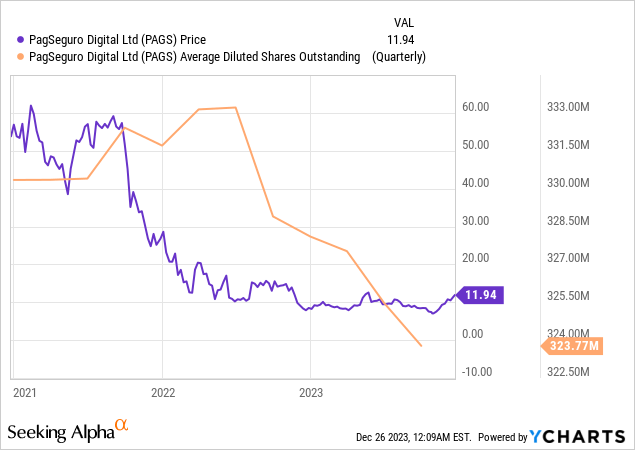

PagSeguro’s data bank, author’s notes

The active PagBank client base surpassed 30 million, with clients growing by 16% YoY. PagBank Cash-in reached 56 billion BRL, driving deposits to an all-time high of 21.6 billion BRL. In terms of credit, the portfolio reached 2.5 billion BRL, with a focus on secured products, resulting in a downtrend in NPL90+ to 10.7%, which is good.

PagSeguro’s data bank

The company continued to grow in payments, with a nearly 100 billion BRL TPV, representing an 11% YoY growth. The focus on new technologies included the execution of the first transaction using the Brazilian digital currency through the blockchain platform (DREX) and the introduction of facial authentication for the payment link option.

PagSeguro’s financial services unit experienced a quarterly increase in total revenues to 260 million BRL, up 8% from Q2, although gross profit decreased due to higher provisions for losses. Financial expenses decreased YoY, and total losses decreased by 39% YoY. Operating expenses were down 5% YoY and 1% QoQ, representing 14.5% of total revenue and income.

Cash earnings gained momentum, reaching a positive amount of 365 million BRL, up 36% vs. the same period last year. The net cash balance at the end of Q3 was 10.6 billion BRL, and the company continued its commitment to shareholders through share buybacks and an increasing equity position.

PagSeguro’s data book, author’s notes

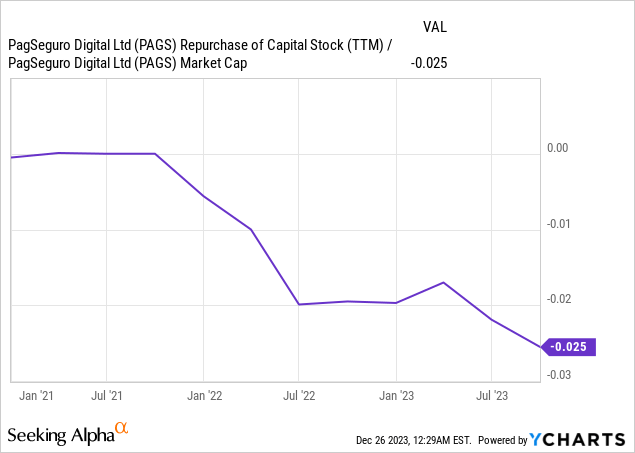

According to YCharts, on a TTM basis, PAGS spends ~2.5% of its market capitalization on share buybacks, which is a lot for a company in its current development phase:

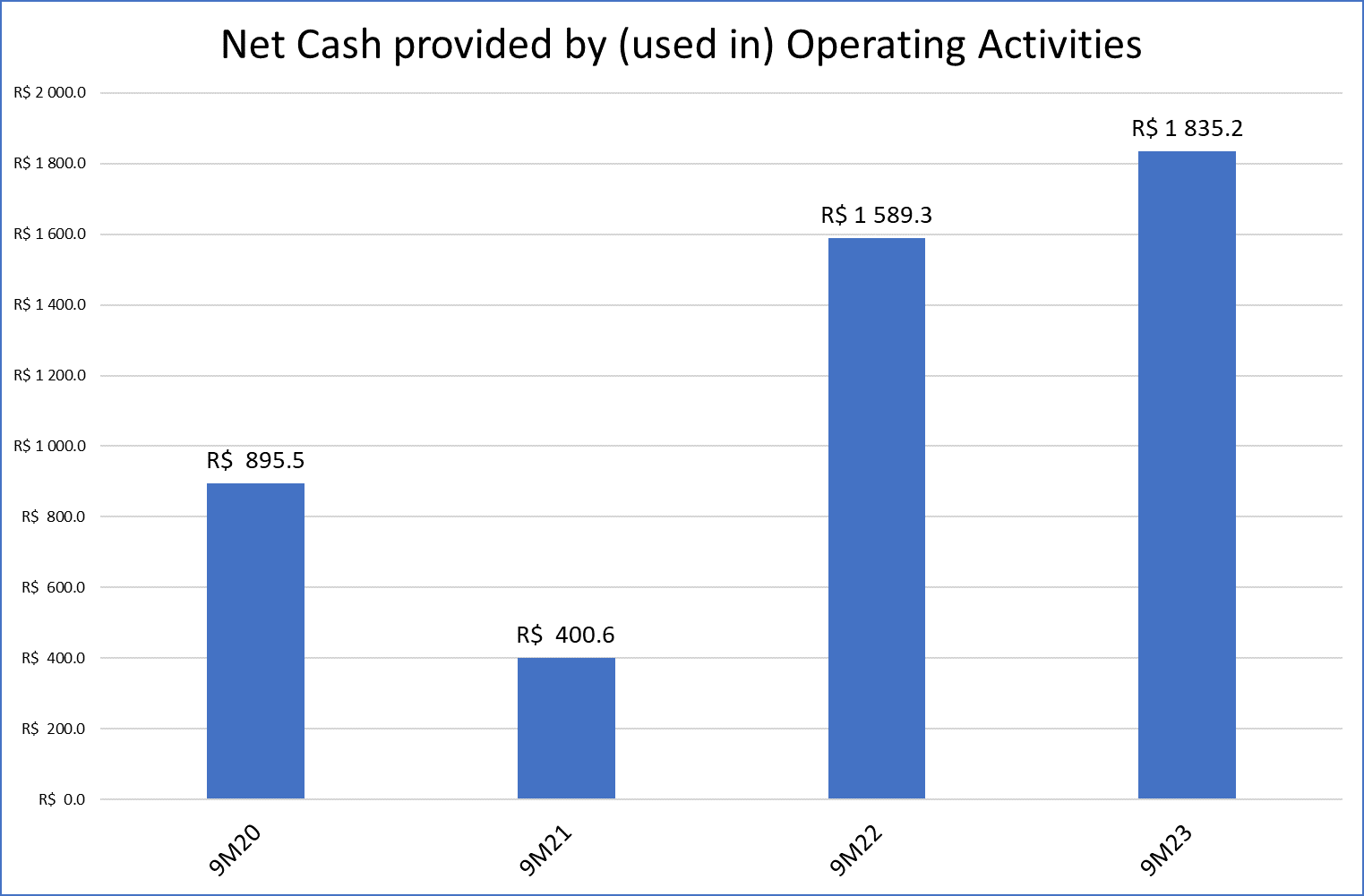

There’s a strong indication that PAGS won’t be slowing down anytime soon. This is not just based on the adjusted EBITDA, which might be subject to different interpretations, but also on the robust and rapidly growing operating cash flow.

PagSeguro’s data book, author’s notes

Based on what I found in the last earnings release, PagSeguro plans to expand in different regions of Brazil using HUBs and improve online payment usage for a smoother shopping experience; they are working on balancing spending and depreciation/amortization levels in the latter part of 2024, focusing on growing their sales team to promote the use of various financial services and building a complete financial system. The company is also adopting new technologies, like executing transactions with DREX and adding facial authentication features.

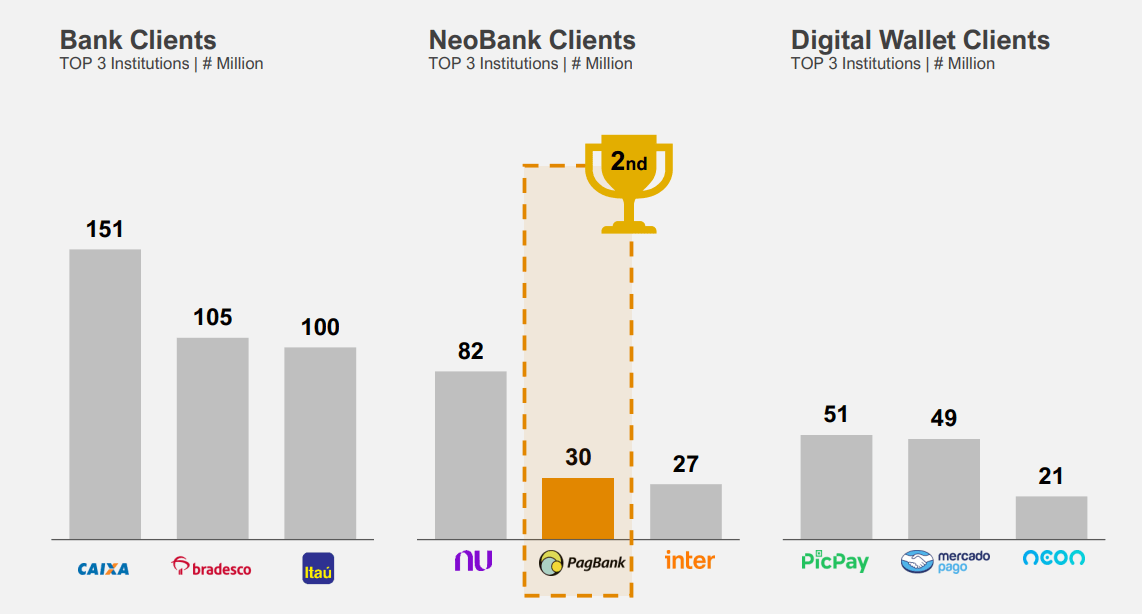

At the same time, the company already occupies a leading position in its niche.

PagSeguro’s IR materials

The company’s expansion within end markets and sustained growth rates can be achieved through the further development of the projects amid solid financials. Additionally, ongoing share buybacks on the existing high-yield base should contribute to stock growth in this favorable context, in my view.

But what about the company’s valuation?

The Valuation

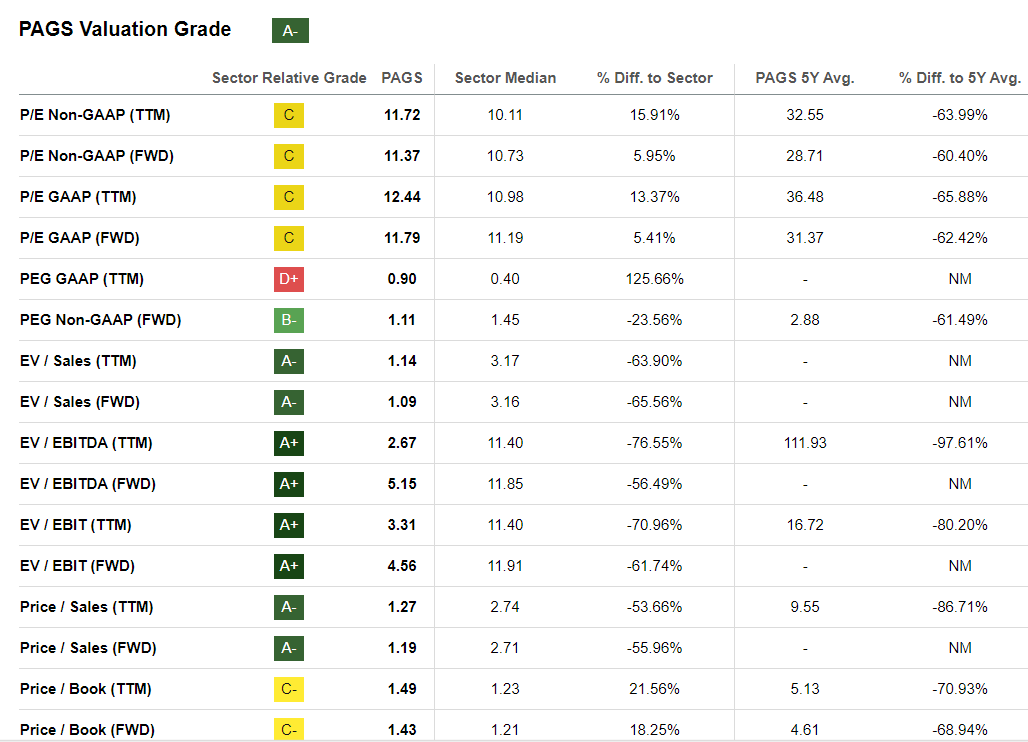

According to Seeking Alpha’s Quant System, PAGS stock’s Valuation grade is ‘A-” based on the comparison to the whole Financials sector. That looks absolutely solid because we’re dealing with a fast-growing fintech company whose multiples compare well even with commercial banks.

Seeking Alpha, PAGS’s Valuation

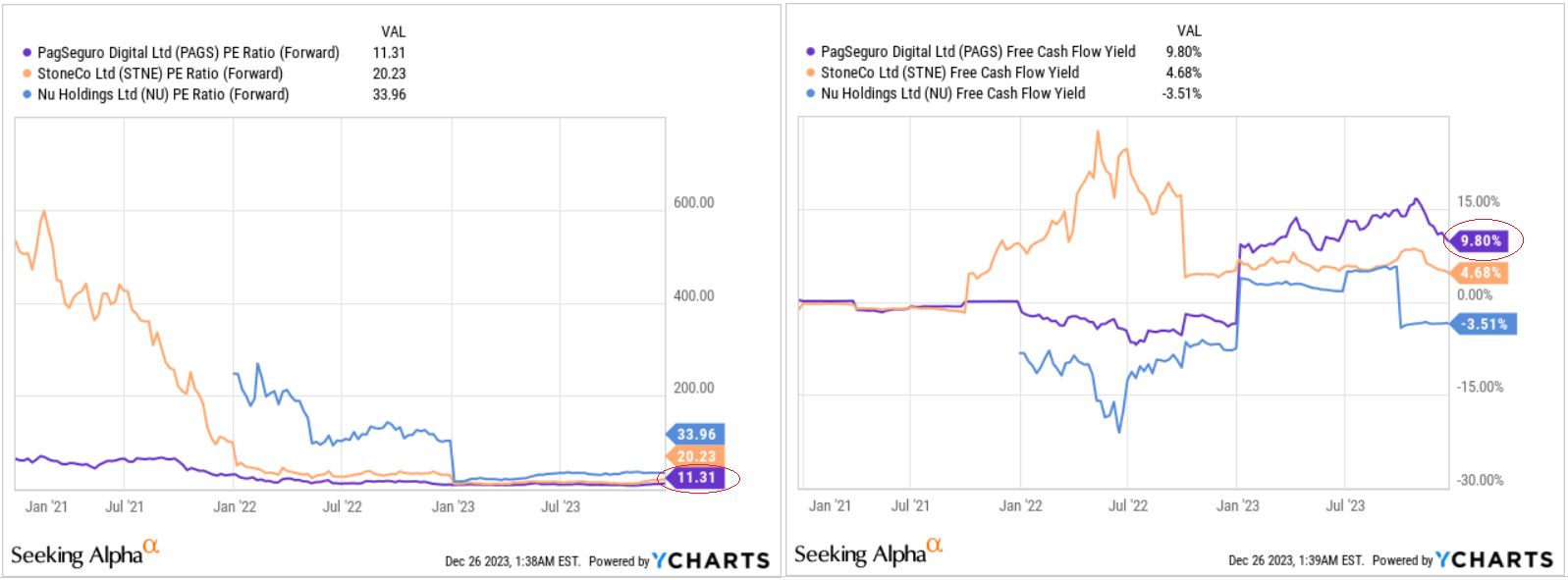

But you have to admit that it makes little sense for investors to make comparisons with the sector as a whole. It would make much more sense to focus our attention on the comparison with direct peers, and here PAGS definitely has something to brag about. The company’s P/E ratio for next year is almost twice lower than StoneCo’s (STNE) and about 3x lower than Nu Holdings’ (NU). At the same time, PagSeguro’s FCF yield is significantly higher:

YCharts, author’s notes

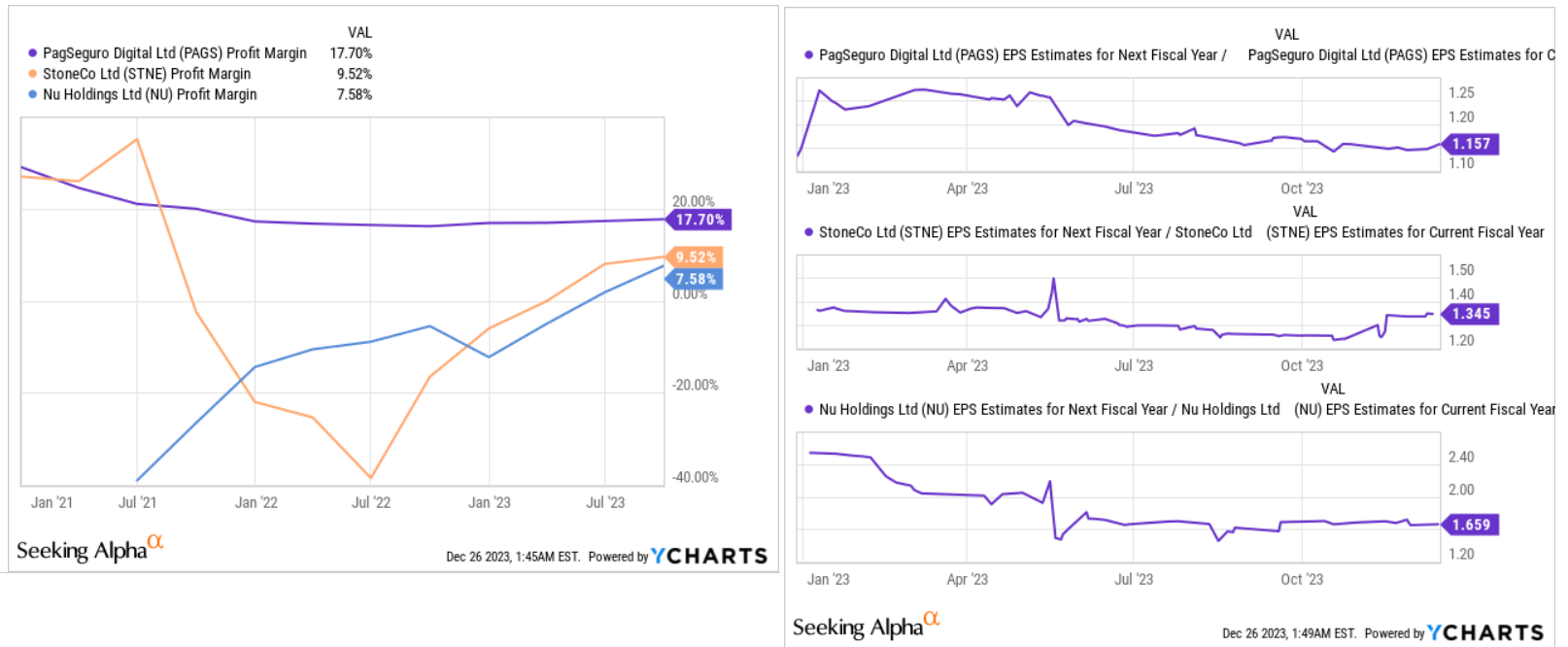

But if there is such a large discount, it must be due to either lower margins or significantly lower business growth. In the case of PAGS, we face the second option, as the company’s NI margin is still much higher than its peer group, but the projected EPS growth is many times lower.

YCharts, author’s notes

In my opinion, the market has already abandoned PAGS to outsiders by lowering multiples and partially “writing off” its growth prospects. However, if we take a closer look, we will realize that PAGS is not growing that slow compared to its peers; it’s just that the company is 1-2 steps higher in its business cycle. While NU or STNE are trying to maintain their newly emerged profitability, PAGS continues to grow its earnings per share, which seems to be growing much slower due to the growing base effect:

Author’s work, Seeking Alpha data

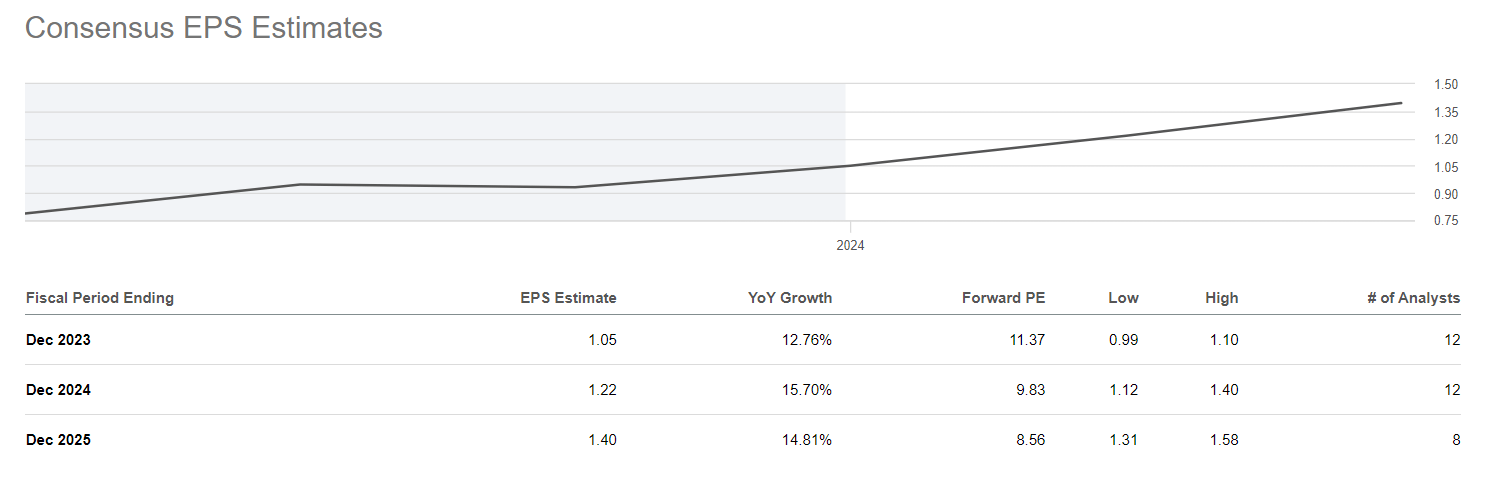

Assuming that the consensus data is right (which the company has often beaten in the recent past), PAGS should continue to actively increase its EPS. At the same time, the implied P/E ratio in FY2025 looks ridiculously cheap at just 8.56x:

Seeking Alpha

So PagSeguro stock looks too cheap to ignore, in my view, even considering its YTD rise of 44.9%.

The Bottom Line

Of course, PAGS has plenty of risk factors that every investor should take into account. For example, a couple of months ago, Viceroy announced their short position on Brazilian payment processors PagSeguro and StoneCo due to concerns about the operational integrity of both companies. The FBI’s raid on PAX Global Technology Ltd’s Florida offices, a Chinese company crucial to PagSeguro and StoneCo for their POS terminals, raised serious red flags. The investigation involved allegations of these machines being used for malware and command-and-control activities. Viceroy anticipated potential regulatory and legal actions against PagSeguro, emphasizing the significant risk to its PagBank license. However, it should be noted here that this particular report by the Viceroy was less detailed than previous research work by the short-seller. Furthermore, both stocks have gained significantly in value since then. But all this does not eliminate the threat of risk in the future.

Nevertheless, I am quite positive about the growth prospects of PAGS. Given the outlook for the end markets and the improving macroeconomic situation in Brazil, the company seems undervalued to me today. I think PAGS is well positioned to leverage its strong financials to increase its market share. In parallel to this process, nothing prevents PAGS from continuing to buy back shares from the market. For all these reasons, I rate the stock a ‘Buy’ this time.

Thanks for reading!

Be the first to comment