8vFanI

Looking for a high yield investment that profits from rising interest rates?

Take a look at Owl Rock Capital (NYSE:ORCC), the 3rd largest company in the Business Development Company, BDC, industry.

A key positive for ORCC in the current rising rate environment is that 99% of its assets are floating rate, while 47% of outstanding debt is fixed rate. Subsequently, a 100-bps increase in rates would add approximately $0.04/share per quarter to Net Investment Income, NII, when accounting for the impact of income-based fees.

LIBOR is currently at 2.36%, up from 1.79% a month ago, and way up from just 0.09% a year ago. The majority of ORCC’s borrowers have 100 basis point floors – management expects rising rate benefits to begin in the 2nd half of 2022, and we can see that this already began to happen in Q2 2022.

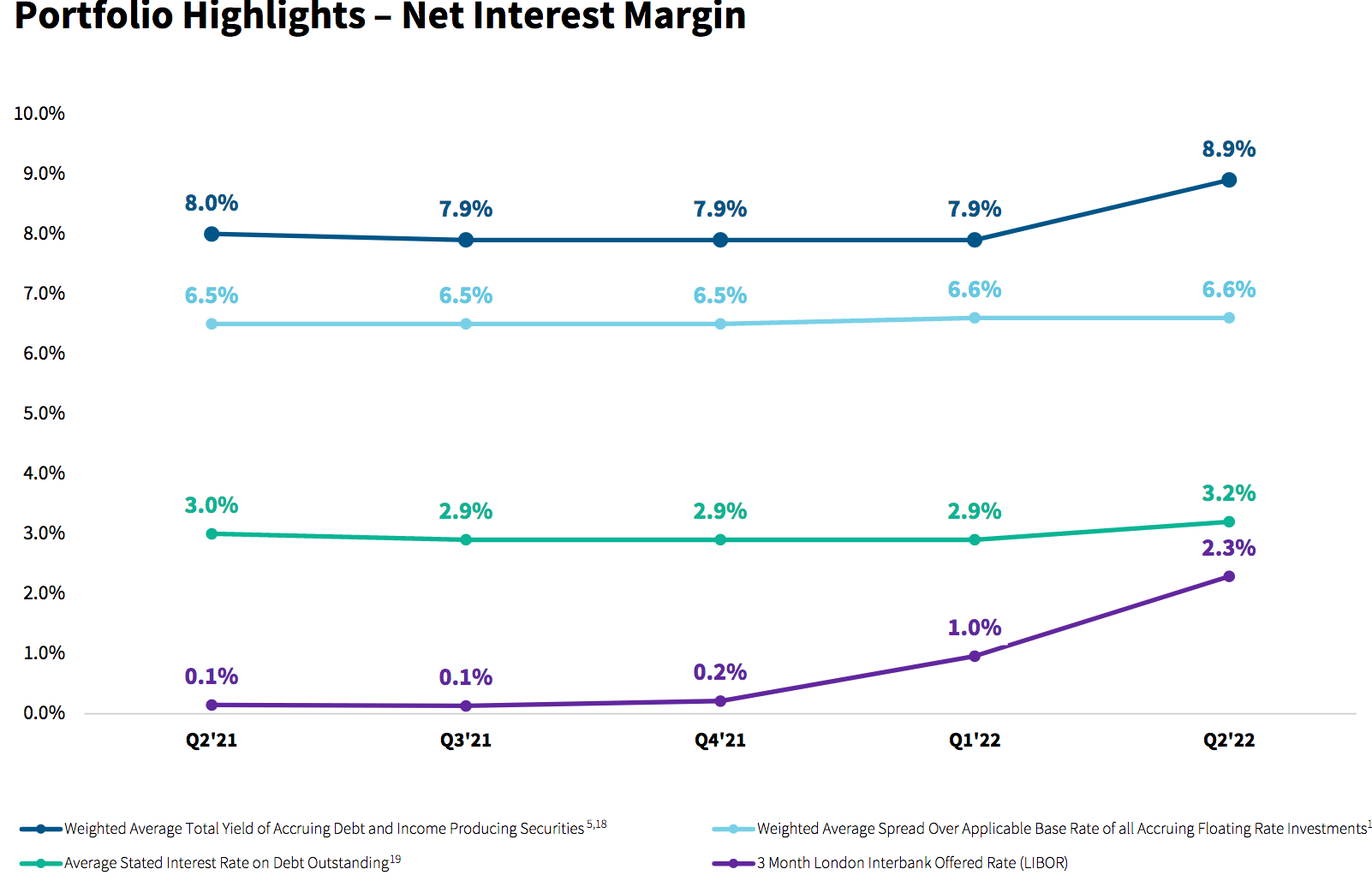

ORCC’s average debt and income yield jumped 100 basis points in Q2 ’22, to 8.9%, vs. 7.9% in Q1 ’22, while its interest rate on outstanding debt only rose 30 basis points, to 3.2%:

ORCC site

Profile:

ORCC benefits from its size – it’s the 3rd largest BDC by market cap, with access to its parent’s, Blue Owl (OWL) huge $44.8B platform, which includes several other companies, and 4 types of direct lending segments – Diversified, Technology, 1st Lien, and Opportunistic, in addition to its $6.8B in assets under management in its Wellfleet CLO’s.

Holdings:

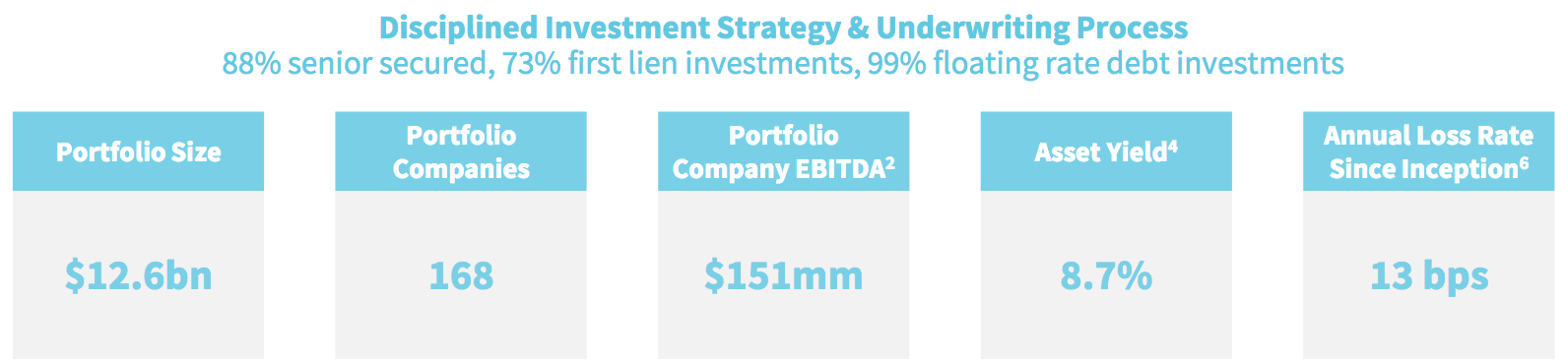

ORCC’s $12.6B portfolio is comprised of 88% Senior Secured, and 73% 1st Lien investments in 168 companies, with an average company annual EBITDA of $151M. Management has done a good job of screening these investments – there’s only a 13 basis point loss since inception.

ORCC site

Portfolio Company Ratings:

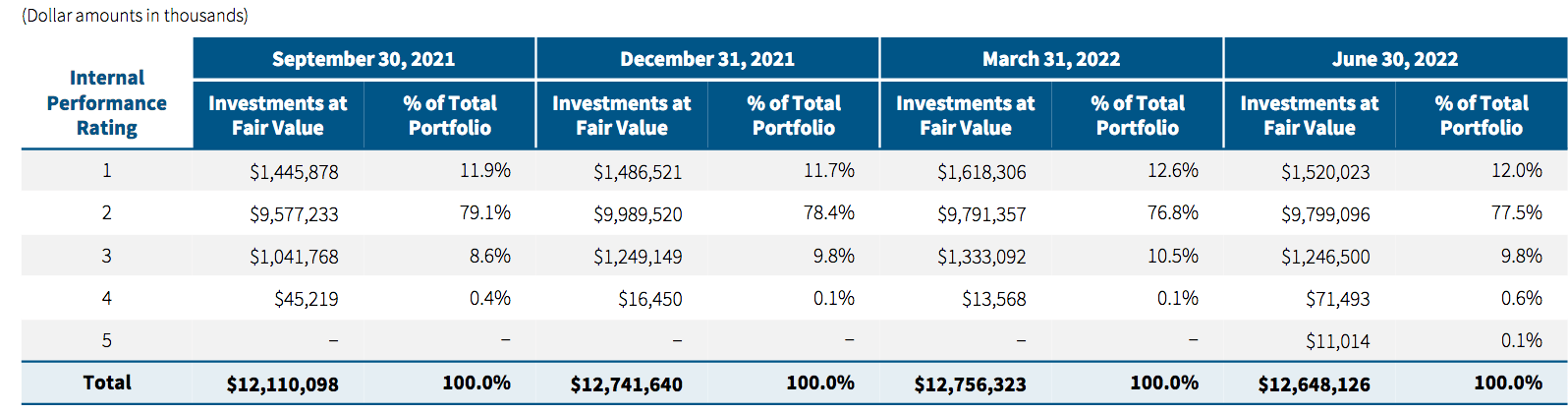

Management reviews and rates ORCC’s holdings quarterly, on a 1 – 5 tier system, with 1 being the best financial performance and 5 being the lowest.

As of 6/30/22, there was 1 company on non-accrual status, which equaled just 0.1% of ORCC’s portfolio, (based on fair value), one of the lowest levels in the BDC industry. The top 1-2 tiers represented 89.5% of the portfolio, similar to Q1 ’22:

ORCC site

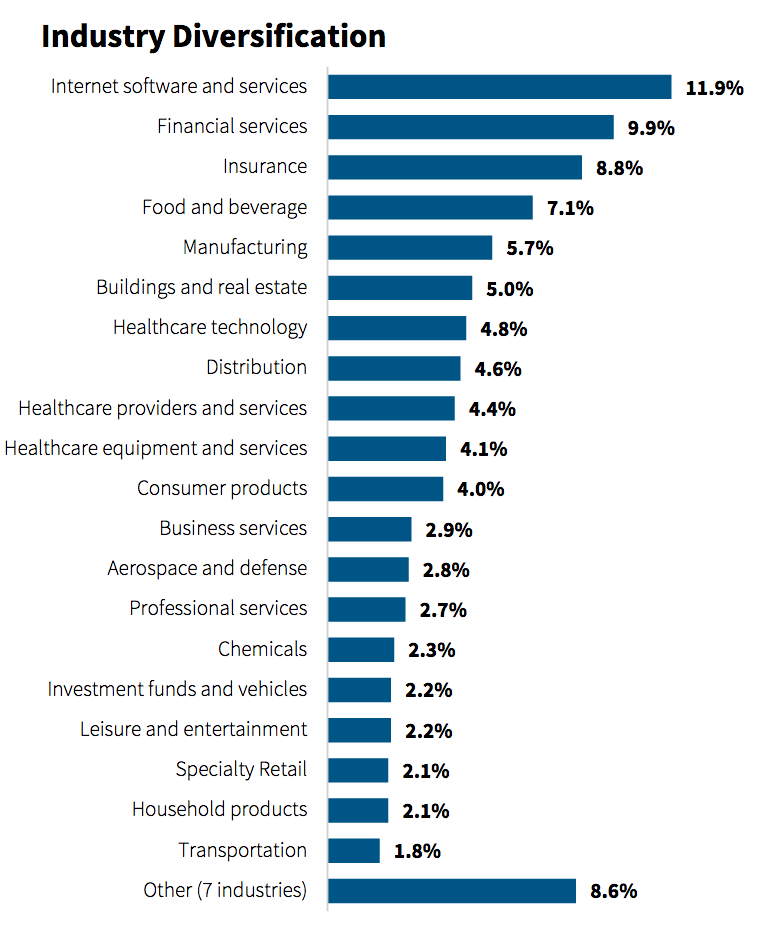

ORCC’s top 4 industries comprise ~38% of its holdings, with Internet Software & Services in the top slot, at ~12%, followed by Financial Services, at ~10%, up from 9% in Q1 ’22. Insurance has an 8.8% weighting, with Food & Beverage at 7%, similar to Q1 ’22. The majority of the portfolio is comprised of non-cyclical companies in service-oriented sectors, such as software, insurance and healthcare.

ORCC site

Earnings:

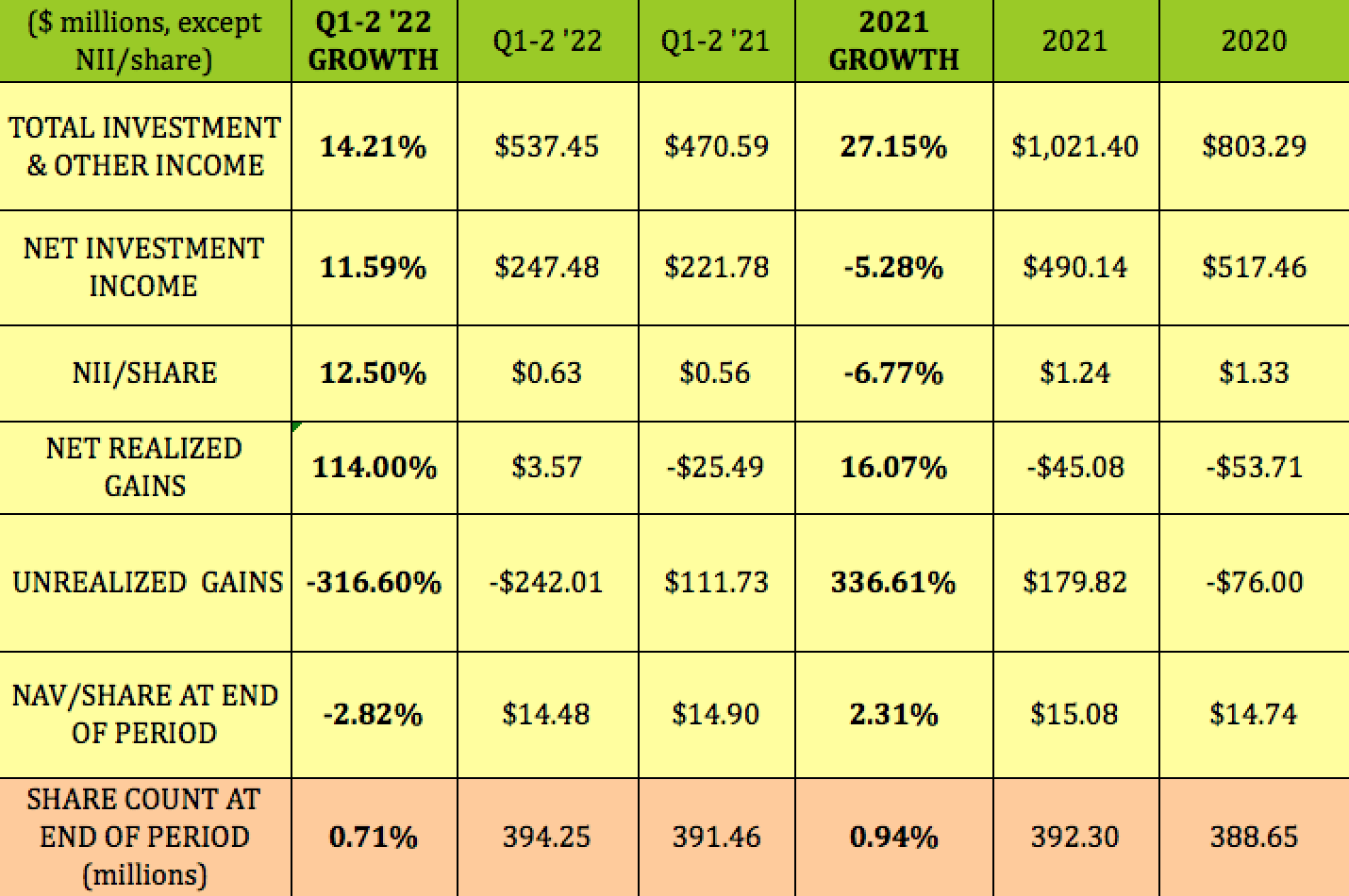

Q2 ’22 Investment income rose 9.75% to $273.3M, vs. $249M in Q1 ’21. Net investment income was $125.1M, up 5%, vs. $119M a year ago.

NAV/Share fell $.40, from Q1’s $14.88 figure, to $14.48 as of 6/30/22, mainly due to net changes in Unrealized Gains of ~$159M. There was a markdown in portfolio share value from market adjustments due to the impact of wider credit spreads.

ORCC site

ORCC has had good growth in the 1st half of 2022, with total Investment Income rising 14%, NII up 11.6%, and NII/share up 12.5%. The share count was roughly flat.

Hidden Dividend Stocks Plus

New Business:

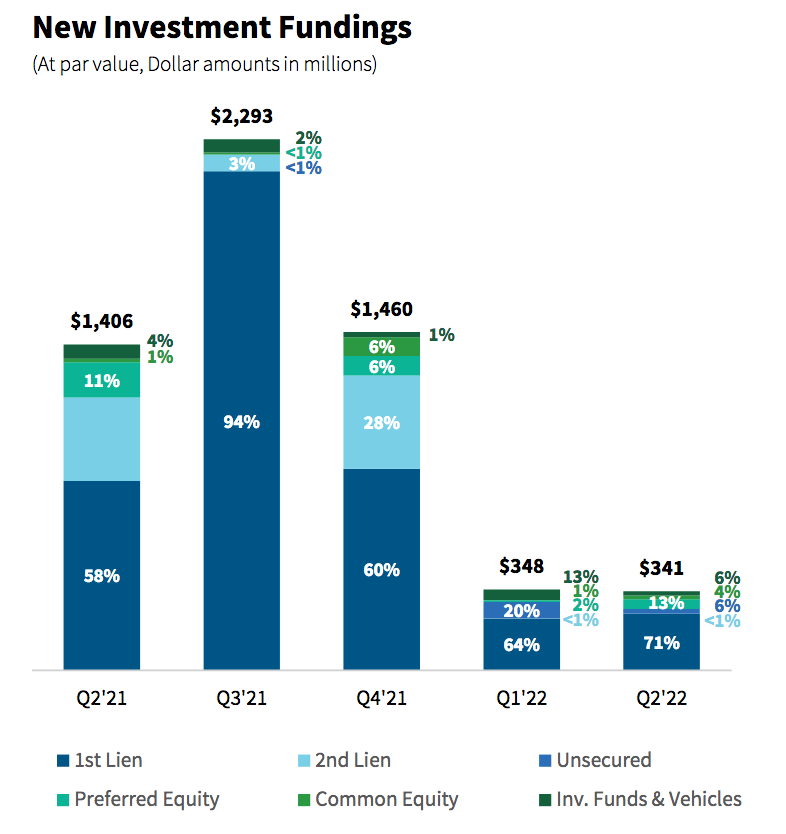

In Q2 ’22, new investment commitments totaled $603.4M across 16 new portfolio companies and 10 existing portfolio companies. This was up ~14%, vs. $530.4M in Q1 ’22, across 17 new portfolio companies and 4 existing portfolio companies.

The principal amount of new investments funded was $341.3M, with $488.3M aggregate principal amount in sales and repayments.

One benefit from ORCC’s size is that, unlike many smaller BDC’s, it’s able to do large deals. For example, in Q2 ’22, management evaluated over 20 opportunities for $1B deals.

Fundings have been much lower in the 1st half of 2022, vs. 2021, with higher rates reducing refinancings, and market uncertainty leading to a decline in M&A activity.

ORCC recently announced an equity commitment in Emergent Asset Management. Emergent is a newly formed portfolio company created to invest in a leasing platform focused on rail car and aviation assets.

ORCC site

Leverage & Profitability:

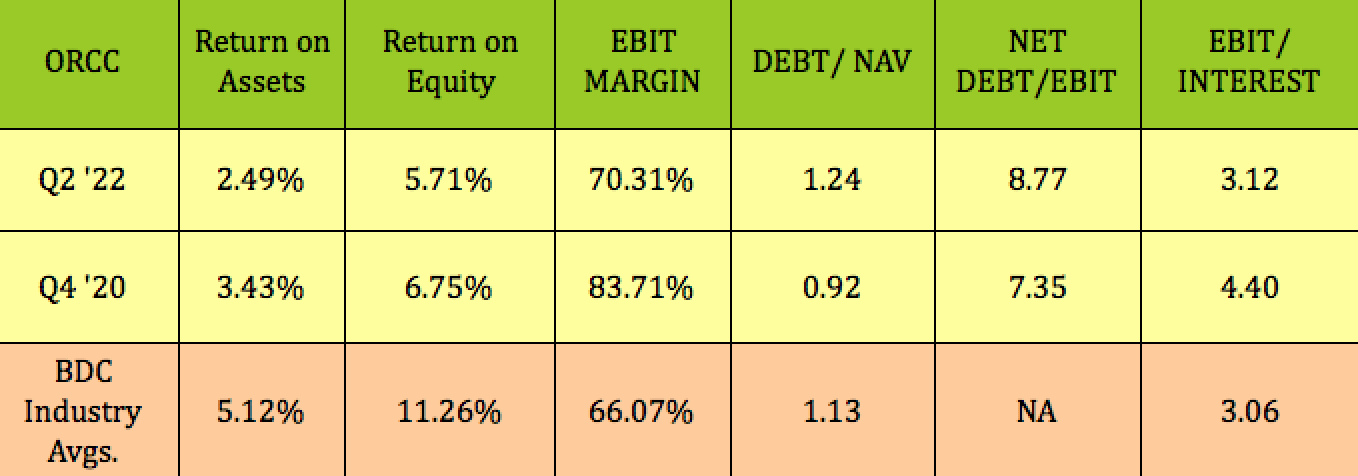

Management has increased debt leverage to 1.24X, within its target range, vs. 0.92X in pre-pandemic Q4 ’20, in order to ramp up earnings. Increasing debt isn’t seen as a bad feature in BDC’s, which pay out 90% of their taxable income to shareholders. The key here is for management to be able to not get over-leveraged. ORCC’s Debt/NAV is roughly in line with the BDC industry’s 1.13X average, as is its EBIT/Interest coverage.

ROA and ROE are down a bit vs. Q4 ’20, as are EBIT Margin and EBIT/Interest coverage.

Hidden Dividend Stocks Plus

Debt & Liquidity:

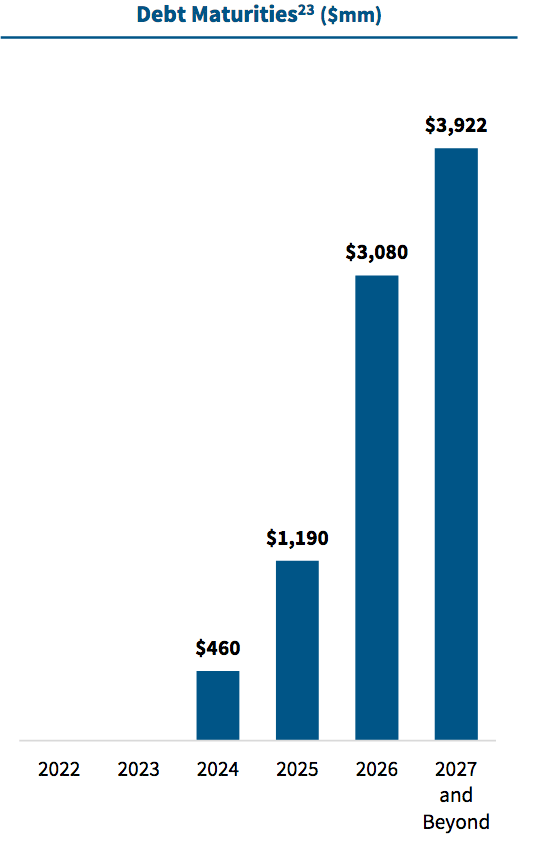

ORCC has no debt coming due until April 2024, when $460M matures. It finished Q2 ’22 with $1.7B in liquidity, comprised of $1.4 billion of undrawn capacity on its credit facility and $0.3B in cash.

ORCC Site

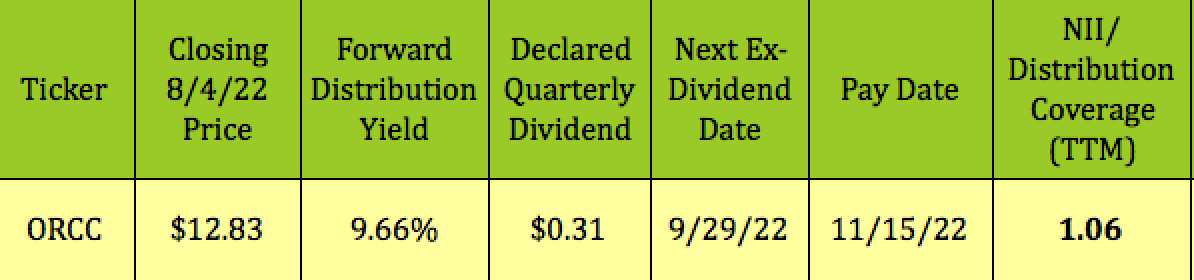

Dividends:

At its 8/4/22 closing price of $12.83, ORCC yields 9.66%. It goes ex-dividend next on 9/29/22, with an 11/15/22 pay date.

Hidden Dividend Stocks Plus

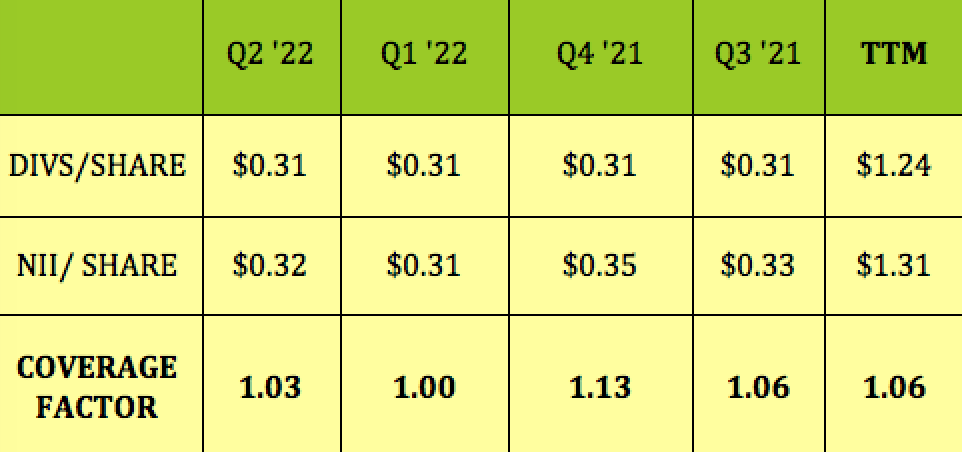

A big challenge for ORCC over the past 2 years was to be able to cover its quarterly dividends when incentive fee waivers expired. Management has delivered on that challenge, beginning in Q3 ’21 with 1.06X coverage. NII/Dividend coverage was 1.03X in Q2 ’22, with trailing coverage of 1.06X:

Hidden Dividend Stocks Plus

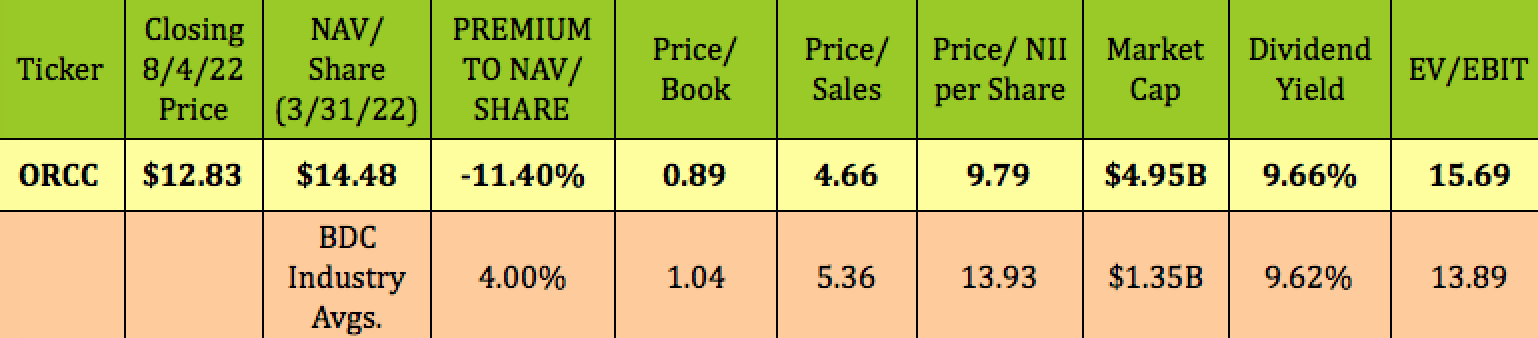

Valuations:

At its 8/4/22 closing price of $12.83, ORCC is selling at an 11.4% discount to NAV, much lower than the BDC industry’s average premium of 4%.

ORCC is also selling at a much cheaper earnings multiple, of 9.79X, vs. the 13.93X industry average.

Hidden Dividend Stocks Plus

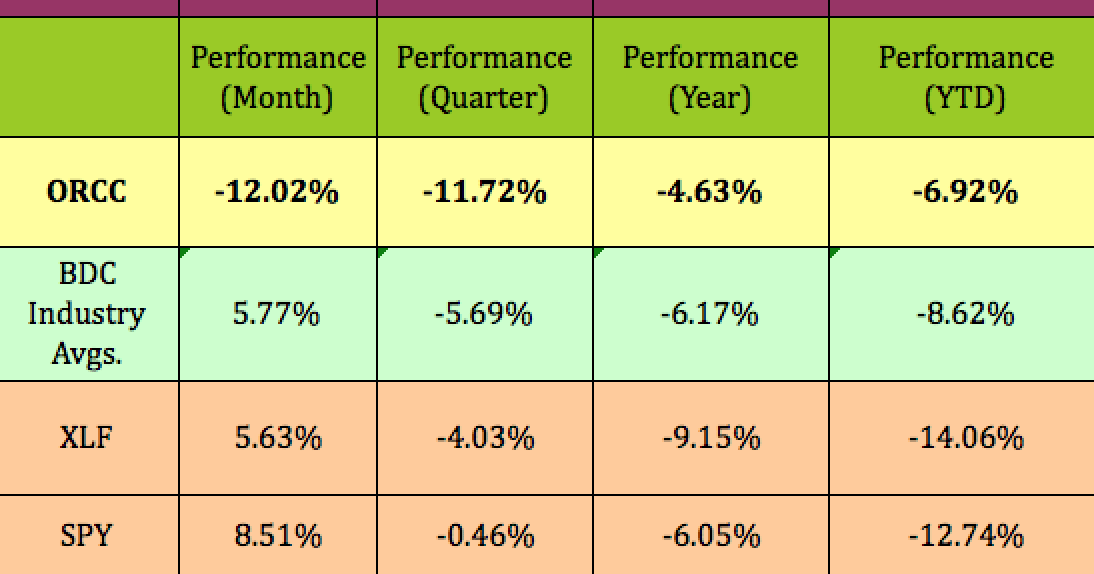

Performance:

While it has underperformed the BDC industry, the broad Financials sector and the S&P 500 over the past month and quarter, ORCC has outperformed them over the past year, and so far in 2022:

Hidden Dividend Stocks Plus

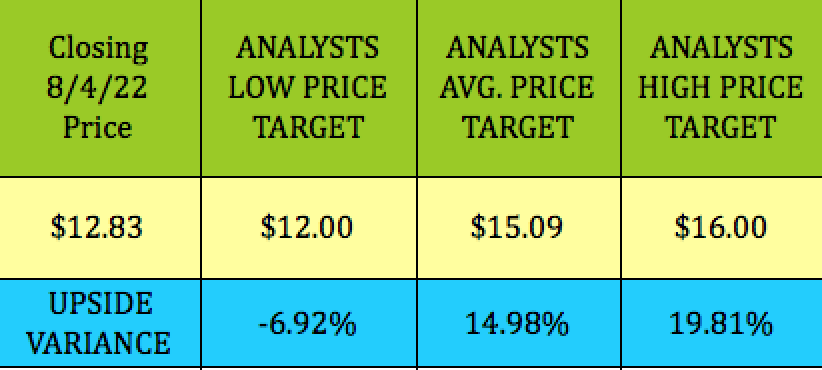

Analysts’ Price Targets:

At $12.83, ORCC is 15% below analysts’ $15.09 average price target, and nearly 20% below the $16.00 highest target.

Hidden Dividend Stocks Plus

Parting Thoughts:

We rate ORCC a BUY, based upon its attractive dividend yield, its earnings prospects in a rising rate environment, its low valuations, and its sound management.

If you’re interested in other high yield vehicles, we cover them every Friday and Sunday in our articles.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

Be the first to comment