Victoria Kotlyarchuk /iStock via Getty Images

Shares of Owens & Minor (NYSE:OMI) have rallied about 8% over the past year, but this masks how volatile they have been, with shares rising about 50% from their lows just a couple of months ago. On Wednesday, the company presented its five-year plans at its investor day. These plans are ambitious, and given recent performance, I am not certain investors should assume they are attained. Shares appear to be fully reflecting them given the rally, creating more downside, and I would be a seller as a result.

Seeking Alpha

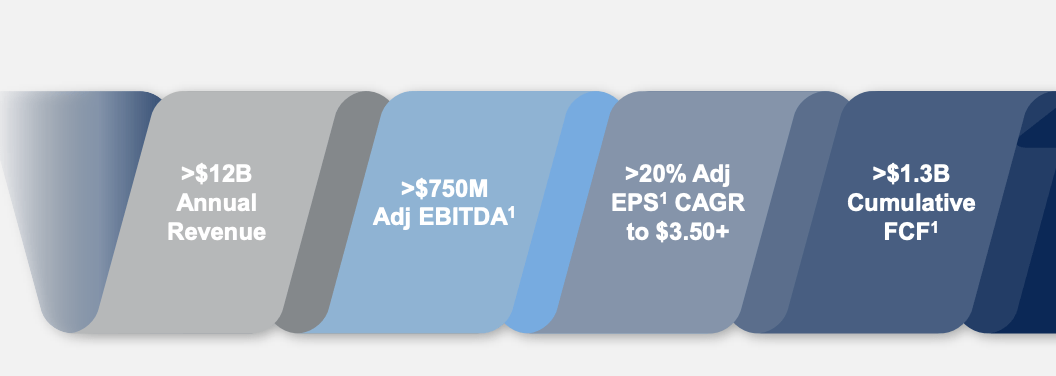

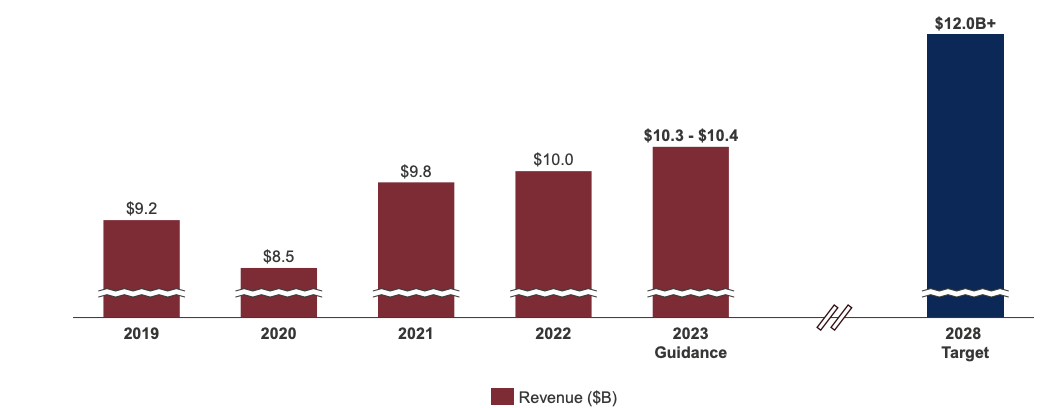

At the company’s investor day, management made clear that Owens & Minor is focused on growing in home-based care, where it increased its exposure via the acquisition of Apria last year, while also reducing costs in its legacy distribution business. Based on this, it aims to grow revenue to $12 billion, from $10.3 billion today, on which it believes can deliver 20% annual EPS growth and $1.3 billion in free cash flow from 2024-2028.

Owens & Minor

In patient direct (its home care unit), OMI is focused on organic growth while also looking at acquisitions to enhance growth and scale. Home-based care is a $70 billion market with 6% growth. Medicare beneficiaries are growing at an even faster 8% pace, given the aging of the US population. Moreover, as Medicare looks to save money, there has been increased focus on providing more care at home vs in hospitals and nursing homes; with estimates of $200+ billion in home-care opportunities. As a result, I believe this is a good business to be in.

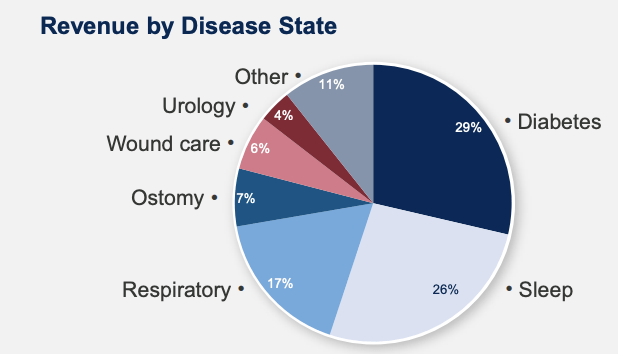

OMI’s product portfolio here is focused on chronic conditions, like diabetes, respiratory illness, and sleep apnea. This is a positive because these create long-term customers with ongoing product needs; as a result, 80% of its revenue in this unit is recurring, a clear positive. OMI also has an excellent payer mix of 80% commercial, 18% Medicare, 2% Medicaid, which has contributed to solid margins. With CMS looking to increase at-home care, I would expect its Medicare mix to increase over time.

Owens & Minor

In this unit, OMI has been able to deliver growth. Since 2019, revenue has grown on a pro forma basis by 8% annually to $2.5 billion (over the trailing twelve months). At the same time, operating income has grown by 18% to $235 million, solid margin expansion as it has built scale with 3 million active patients today.

Owens & Minor’s five year-plan assumes it can double revenue to $5 billion in 2028. I would note about half of this growth comes organically and half from unannounced M&A. To power additional organic growth, it seeks to move into adjacent product lines, lie prosthetics and rehab therapy. This assumes about 8% organic annual growth, which assumes it can grow as fast the next five years as the last five.

Given we are likely to see a somewhat worse payer-mix, that means it will need to grow its patient population even more quickly. On the one hand, there is a clear push towards more at-home care, which can be cheaper for payers. On the other, as the business has grown market share, the law of large numbers is likely to make it harder to keep growing as quickly. We also have the unknown of what GLP-1 drugs aimed at obesity and diabetes will do to trends in that disease, which accounts for 29% of this unit. I suspect their impact will be to reduce the growth in the diabetes population in the long-run, but this may not be evident over the next five years. I view 8% growth as a potentially attainable, but aggressive, target.

It is notable that management seeks $1.1 billion in organic revenue growth here; however, its total revenue growth is just $1.7+ billion to $12+ billion. This is because it assumes just 1% growth in legacy products & healthcare services (P&HS), where it seeks to reduce to costs while expanding its product offerings.

Owens & Minor

Despite the lack of top-line growth, Owens & Minor aims to double profits here based on scale and increasing its own branded products. It currently focuses on PPE, sterilization, hygiene products, and surgical accessories. Given weakness in PPE (which has begun to stabilize), management aims to move deeper into critical care work, surgical instruments, and more specialized practices. In fact, it will be quadrupling its new product additions in 2024.

If the company is significantly increasing the number of products it sells, but revenue is barely rising (and likely falling on an inflation-adjusted basis), that likely means volumes per product are declining. I do fear that will be a difficult environment in which to maintain margins, let alone expand them. Adding more products will also increase complexity and inventory needs, which may add costs, making this margin expansion more difficult. This is where I have concern over the company’s ability to meet targets. Frankly, this is just a very difficult business.

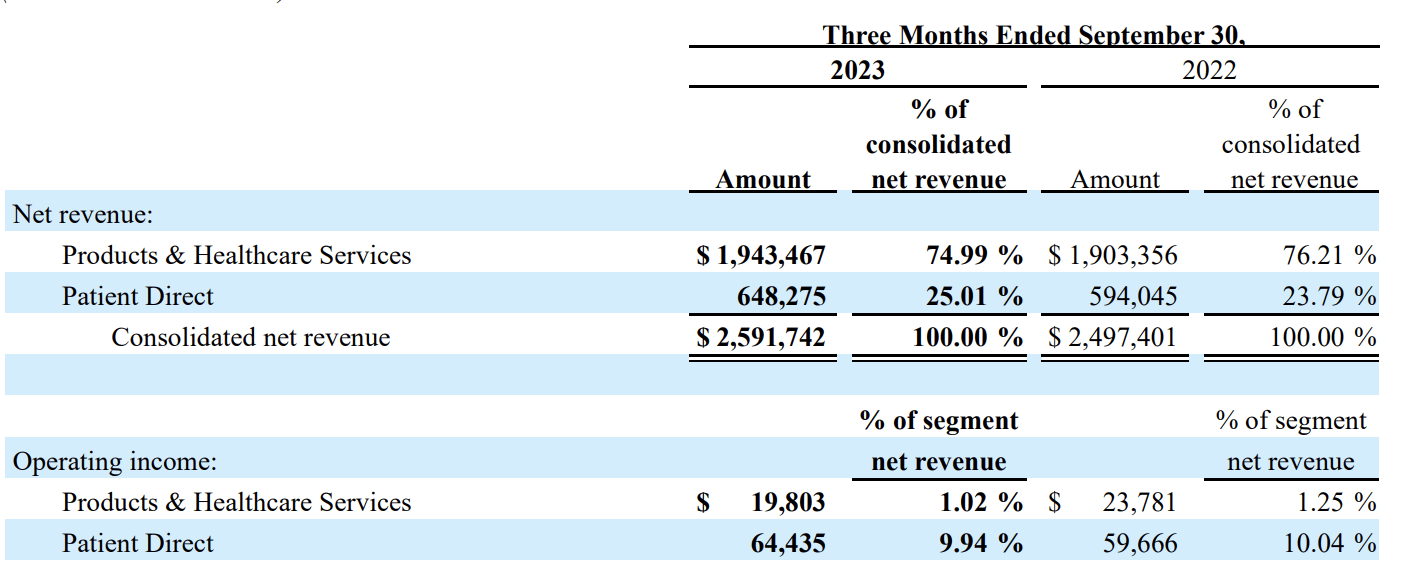

One way to judge the plausibility of future results is to see how the company is performing today. If we look at the company’s third quarter, revenue rose by 4% to $2.6 billion, while adjusted income rose 9% to $34 million. Adjusted EBITDA rose about 5.5% to $135 million. This does point to some margin expansion; however, this expansion is coming from mix shift, not accretion within each unit.

As you can see below, patient direct revenue rose by 9% while legacy P&HS rose by 2%. This is consistent with aims to grow at-home care more quickly. Because of this, P&HS now accounts for just 75% of revenue, from 76.2% last. Its margins are 8-10x lower than patient direct, so as it becomes a smaller piece of the pie, consolidated margins rise.

Owens & Minor

As you can see, though, P&HS margins fell by 23bp while patient direct fell by 10bp. Neither performance is particularly compelling. It is also clear why OMI is focused on patient direct as its growth engine. Revenue grows more quickly, and margins are dramatically better here. The medical distribution business is just a really difficult one with extremely narrow margins. With management planning to add more products and complexity, I fear margins are likely to remain extremely weak. This is why consolidated EBITDA margins are so low at 5.3%.

While management is focused on costs, I would note that distribution, selling, and administrative expenses rose by 5% to $452.6 million, which actually outpaces revenue growth slightly. While it is engaged in a $30 million cost reduction program, we are not seeing this pay off yet. On the positive side, interest expense has fallen to $38.1 million from $39.9 million. Over the past five years, it has succeeded at paying down net debt by $500 million, bringing net leverage from a dangerously-high 7x to below 4x. Over time, it targets 2-3x.

Much of this debt reduction has come from working capital optimization rather than underlying profitability. Inventories are down 18.7% to $1.084 billion this year. OMI generated $110 million of free cash flow in Q3; it was just $7 million excluding working capital, though. For the year so far, there has been $489 million of free cash flow. All of this is due to changes in working capital, including a $247 million drop in inventories. $364 million of debt reduction this year.

To be clear, reducing excess inventory to pay down debt is a significant positive. There is less capital trapped in slow-moving products, while interest expense is lower. This is a more optimal balance sheet structure. However, with inventories having fallen so much, this story is likely largely played out. Particularly as it expands product offerings, inventories may even need to rise somewhat. In the longer-term, underlying free cash flow is what can drive shareholder returns.

On its balance sheet, I would also note that in addition to reducing debt to $2.1 billion from $2.5 billion at the start of the year, it has minimal near-term maturities. Its $172 million maturity in December 2024 at 4.375% can be covered by its $216 million in cash. As such, OMI will not need to roll over debt at higher rates. This is a positive.

Owens & Minor

As the company has faced pressures in its legacy business, this year EPS will fall from $2.42 to $1.30-$1.40. It will also generate less than $75 million of underlying free cash flow. That leaves me questioning its aim for $400 million free cash flow in 2028, as risks are skewed to somewhat slower organic revenue growth in patient direct while margins may struggle to expand in its distribution business.

At its $750 million EBITDA target, debt would fall inside its leverage target of 2-3x by 2028. With cash flow, management is focused on organic investment and M&A and then buybacks. We know the company seeks a $1.3 billion revenue boost via M&A. OMI paid $1.6 billion for Apria, which had $1.15 billion in sales. At that multiple, it will have to pay $1.8 billion for M&A to reach its revenue target. At a 12-15% EBITDA margin, that would enable $540 million of incremental debt capacity. With $1.3 billion in targeted free cash flow, all cash flow would have to go into M&A, likely leaving nothing for share repurchases.

I also view risks as skewed to generating less retained free cash flow, given its poor underlying cash generation this year. With an EV/EBITDA multiple of 7x, limited cash flow generation, a reliance on M&A to achieve growth ambitions, and a large legacy business running dangerously close to breakeven, there is limited scope for capital returns, and now plenty of room to undershoot raised expectations. I would take advantage of the rally to sell shares.

Be the first to comment