agnormark

While it’s been a volatile year for the gold producers and precious royalty/streaming companies, the real volatility has been among the explorers and developers that have suffered a 70%+ decline from their highs. One name that’s been punished over the past year after already being stuck in a secular bear market since 2017 is Osisko Mining (OTCPK:OBNNF), a high-grade gold developer that’s looking like it could ultimately uncover an 11.0+ million-ounce resource base in James Bay, Quebec. Unfortunately, the release of its recent Feasibility Study led to a sharp reversal in the stock, with Osisko Mining (“Osisko”) underperforming its peers thus far in December.

Although the recent underperformance is disappointing, I don’t see any reason to be miffed with the recent Feasibility Study [FS] results which showcase an underground mine with dual ramp-access that is projected to produce ~294,000 ounces of gold per year at $760/oz all-in sustaining cost [AISC]. This is because these projections could end up being on the low end with a mine plan that looks quite conservative combined with a resource that’s already very conservative. So, with Osisko owning one of the best gold projects globally in a Tier-1 jurisdiction, I see considerable re-rating potential, and I would expect any sharp pullbacks to provide buying opportunities.

All figures are in United States Dollars unless otherwise noted.

Windfall Mineralization (Company Presentation)

Windfall Feasibility Study

Osisko Mining released an FS for its Windfall Project in Quebec last month, showcasing a project capable of producing ~294,000 ounces per annum with a peak output of 374,000 ounces of gold in Year 2. This makes Windfall one of the largest undeveloped gold projects from an average production standpoint globally, and certainly one of the highest margins with AISC that are expected to come in at $758/oz despite incorporating inflationary pressures and the study being done in a period of what looks to be peak inflation. In terms of design, Windfall is expected to be a dual ramp-access mine employing a long-hole open-stoping mining method with planned daily mine production of 3,400 tonnes, an increase from 3,100 tonnes per day contemplated in its PEA.

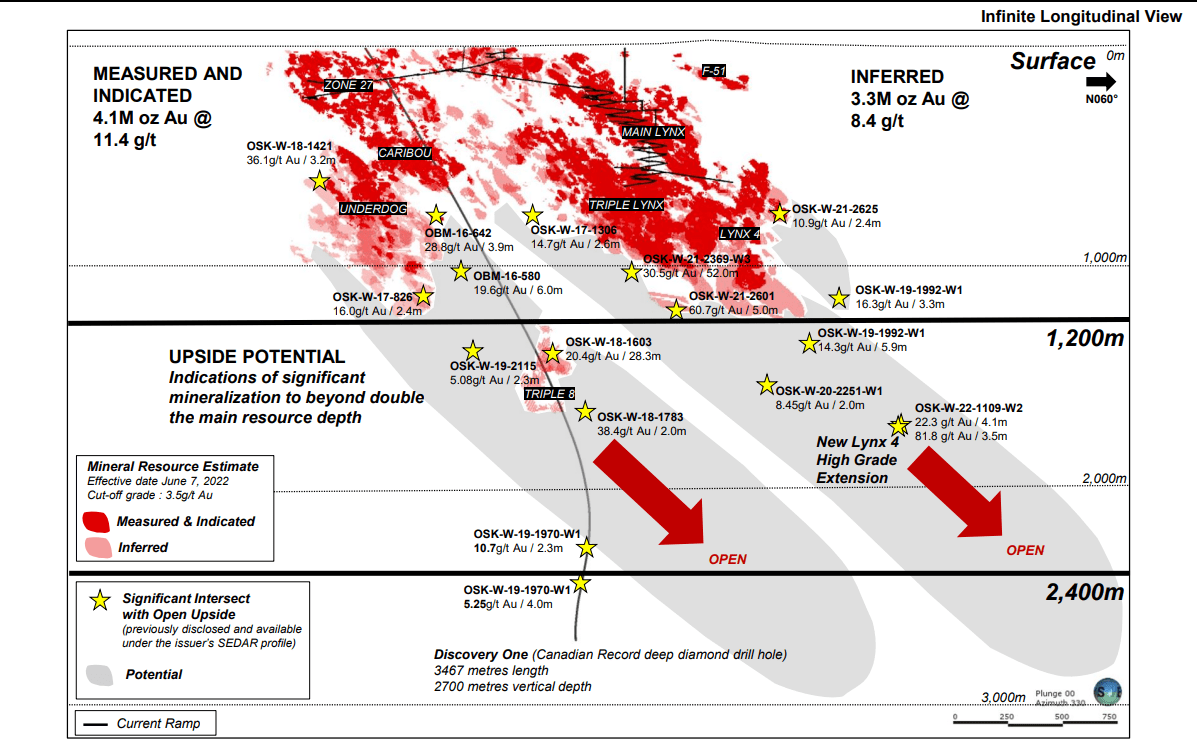

Windfall Mine Design (Company Presentation) Windfall Resources (Company Presentation)

As shown in the above image, the mine will focus on ore within the first 1,200 meters from the surface, but this is a deposit where we’ve seen an abundance of economic mineralization near the 1,400-meter level (Triple 8), at much further depths in the deep discovery hole, and more recently in what’s believed to be a high-grade extension of Lynx 4, where Osisko intersected 3.5 meters of 81.8 grams per tonne gold, as well as 4.1 meters at 22.3 grams per tonne gold. This phenomenal intercept is well above the average grade of the current reserves (8.1 grams per tonne of gold). Osisko also noted that the mineralization is typical of Lynx 4 wireframe 3449 with disseminated pyrite associated with strong pervasive silica alteration hosted in a seriticized gabbro.

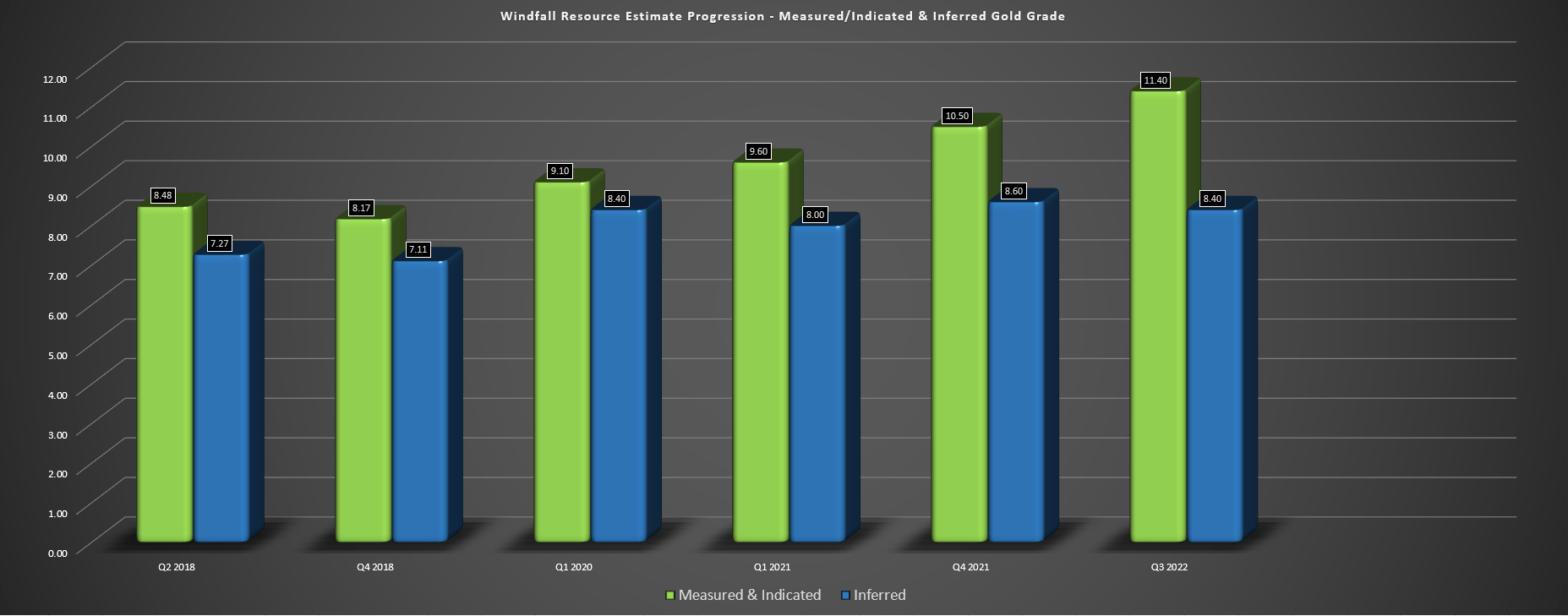

Windfall Resource Estimate Progression (Company Filings, Author’s Chart)

While the production profile is impressive at ~300,000 ounces per annum, the average head grade of 8.1 grams per tonne of gold may have disappointed the market a little, especially with the steady increase in measured & indicated resource grades we’ve seen over the years. As shown above, the most recent resource estimate highlighted an average grade of 11.4 grams per tonne of gold, which led me to assume that head grades would come in closer to 9.0 grams per tonne of gold after adjustments for mining dilution. However, external dilution came in at 20%, with assumed mining recoveries of 91% for production, resulting in ~29% dilution and a much lower feed grade. The result is that despite a 10% increase in the throughput rate (PEA –> FS), projected output came in at similar levels.

When it comes to the inflationary pressures that we’ve seen, plus limited improvement in grades (elevated assumed dilution and its triple-capping method that results in hits like ~13,600 grams over 2.0 meters being capped at 200 grams per tonne gold), Windfall’s projected life of mine AISC increased substantially from $610/oz to $758/oz. Meanwhile, upfront capex also soared due to the inflation we’ve seen over the past 18 months, with upfront capital expenditures estimated at $607 million (0.77 CAD/USD exchange rate) vs. ~$419 million previously. This conservative mine plan and cost creep resulted in a shorter mine life and a much lower After-Tax NPV (5%) figure of ~$1.09 billion at $1,750/oz gold.

Windfall Bulk Samples (Company Presentation)

While this is a slight downgrade from the economics highlighted in the 2021 PEA completed by Osisko, it’s important to make two points. For starters, despite these slightly weaker economics, this is still one of the most attractive undeveloped gold projects globally. Second, and most importantly, is the fact that these assumptions appear to be very conservative for several reasons. The most salient of these is that this mine plan is based on very high capping of grades, and bulk samples are showing very different results. In fact, of the 16,000 tonnes mined to date at Windfall (three different bulk samples), recovery rates were above the recovery assumptions used in the FS, and we saw an average of ~60% positive grade reconciliation.

Obviously, 16,000 tonnes of material is more or less a rounding error when combining this with over 12.0 million tonnes of material in the mine plan. Still, these bulk sample results are very encouraging and considerably better than the bulk sample results that sent Pretium soaring in 2013 with just 5% positive grade reconciliation. It’s important to note that this does not mean that the average 8.0 gram per tonne stope will deliver 12.8+ gram per tonne material at Windfall, given that this is a small representation of the whole deposit. Still, even if we were to see an 8% positive grade reconciliation (1/7th of what’s been realized in bulk samples to date), this mine would produce an extra 24,000 ounces per annum, resulting in a positive impact on cash costs and AISC. Let’s see how it stacks up vs. peers:

How It Stacks Up Vs. Peers

As noted in the updated Feasibility Study, mining dilution was 29% which is quite conservative, reducing the most recent resource’s M&I grade of 11.4 grams per tonne of gold to 8.1 grams per tonne of gold in the Feasibility Study. This severely impacted the average annual production and unit costs. However, if we assume that dilution is a little too conservative and that we see some positive grade reconciliation (resulting in at least a 9.0 grams per tonne head grade), this would result in a production profile closer to ~335,000 ounces and all-in-sustaining costs below $700/oz. In fact, every extra gram effectively adds ~37,000 ounces of extra gold outside the mine plan per annum.

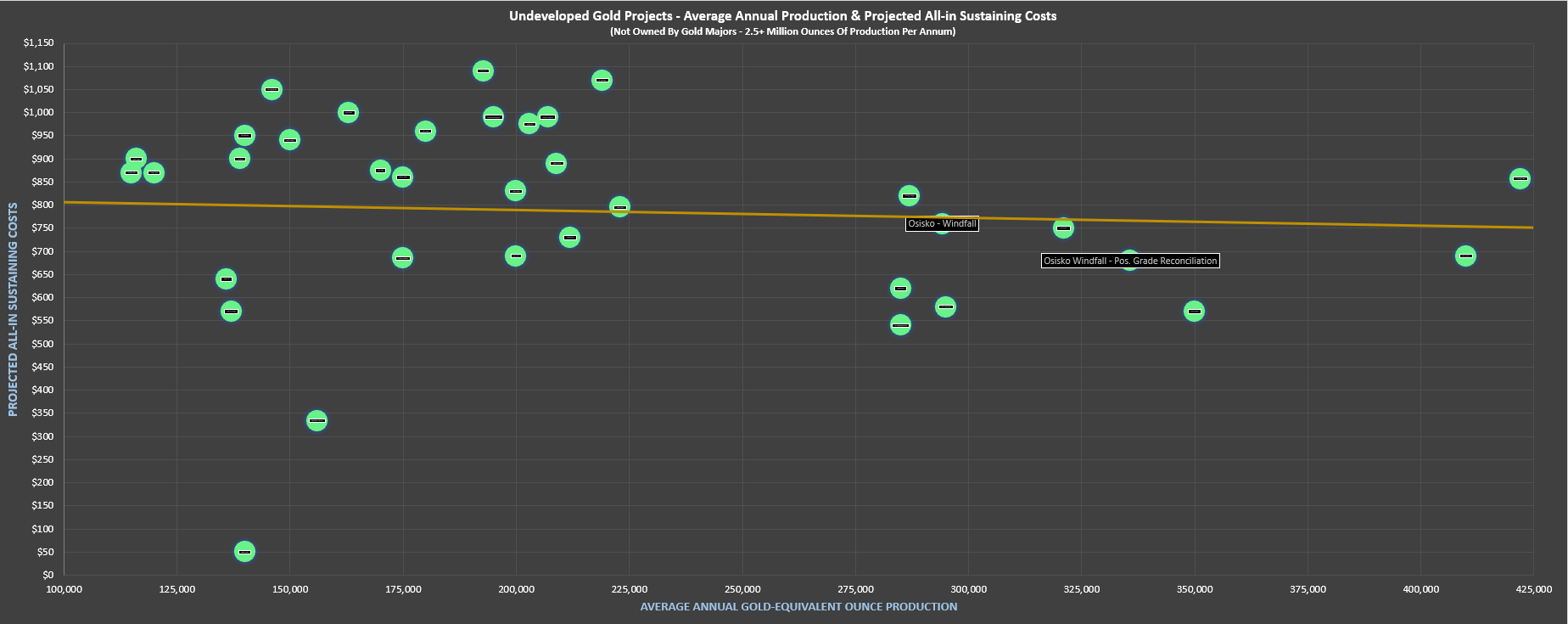

Additionally, if recoveries can be improved, this could add another few thousand ounces as well, assuming a 100-basis point improvement in recovery rates or results that are more consistent with bulk samples completed to date. So, when we look at the blow charts, which compare costs and production vs. peers, I don’t think it’s a stretch to use the “Osisko Windfall – Pos. Grade Reconciliation” block shown on the chart vs. the base case “Osisko – Windfall” block to better gauge how Windfall looks vs. other undeveloped gold projects not held by major mining companies (2.5+ million ounces of gold production per annum).

Undeveloped Gold Projects – Average Annual Production vs. Projected AISC (Company Filings, Author’s Chart & Estimates)

Beginning with the above chart, the best projects would fall to the lower left, with this chart comparing average annual production (horizontal axis) and all-in-sustaining costs (vertical axis). The most impressive projects on the list are Skeena’s (SKE) Eskay Creek, Kinross’ (KGC) Great Bear, Eldorado’s (EGO) Skouries, Lidya’s Hod Maden, Rupert’s (OTCQX:RUPRF) Ikkari and G Mining’s (OTC:GMINF) Tocantinzinho. As we can see, Osisko stacks up very well with one of the largest production rates and relatively low costs, which are over 10% below the peer average for projects of this scale and 40% below the current industry average ($1,250/oz).

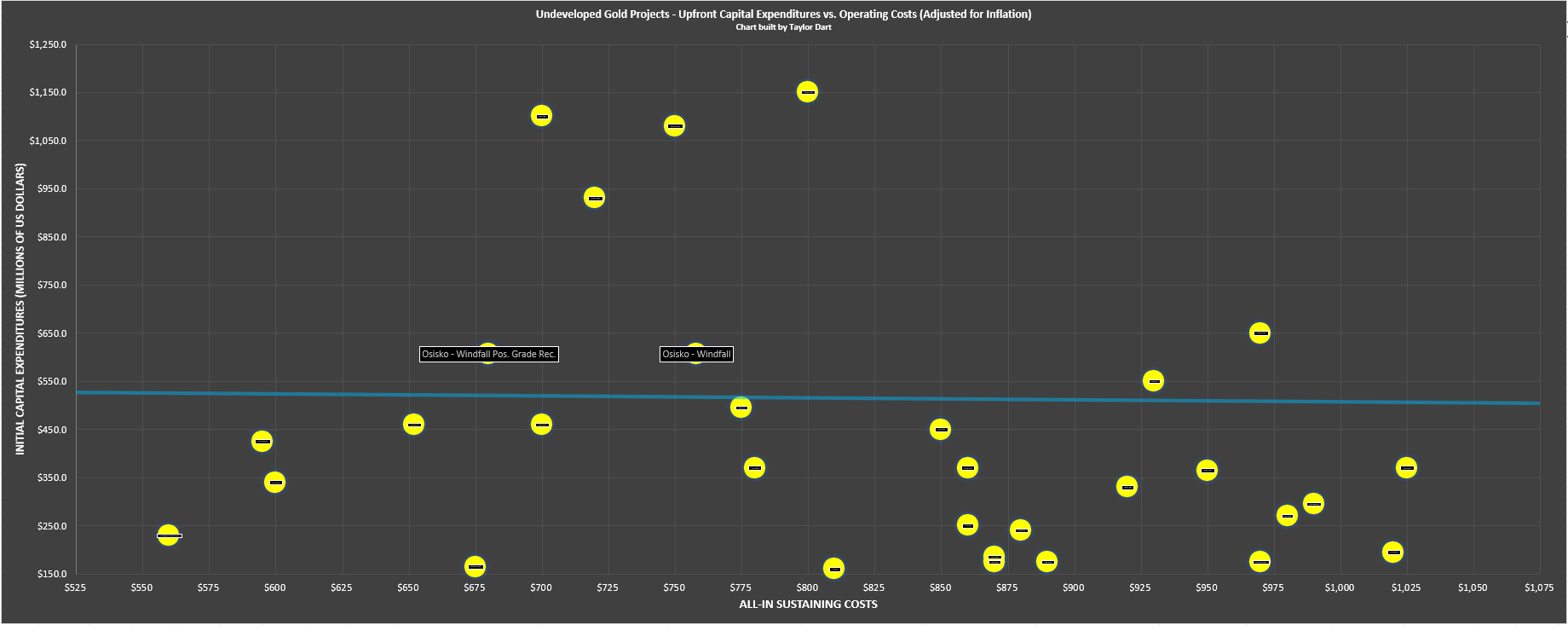

Undeveloped Gold Projects – Upfront Capex vs. AISC (Company Filings, Author’s Chart & Estimates)

Looking at the second chart, the best projects lie to the bottom left, with all-in-sustaining costs measured by the horizontal axis and upfront costs to build these projects on the vertical axis. Once again, Windfall stands head and shoulders above its peers from a capex/operating cost standpoint, being one of the top 10 lowest-cost projects among undeveloped gold/silver projects. Plus, while capex is high at $600+ million, this is very modest relative to its production profile. For comparison, most 300,000-ounce plus per annum projects will cost well over $900 million to build, with Springpole (OTCQX:FFMGF), Stibnite (PPTA), and Mt. Todd (VGZ) being just a few examples. Hence, Osisko’s Windfall has it all, with ~60% AISC margins, a meaningful production profile that makes it a cash-flow machine, and a reasonable upfront capex bill which suggests Osisko will be able to fund it independently.

Before we dig into the valuation, it’s important to note that the Windfall mine plan focuses solely on resources within ~1,100 meters from the surface. However, mineralization has already been intersected at a depth of ~2.5 kilometers at Windfall, and other major gold systems in Ontario/Quebec have been mined well past 2.0 kilometers. Given Windfall’s impressive mineral endowment within the first 1,100 meters, I don’t think it’s unreasonable to assume that Osisko’s global gold resource of 7.4 million ounces could increase to 12.0 to 15.0 million ounces by the end of the decade when it comes to resource growth along strike, at depth, and regional upside.

Windfall Mineralization (Company Presentation)

So, for investors that were a little underwhelmed by the results of the Feasibility Study, I wouldn’t lose too much sleep, given that this is about as conservative as it gets. In fact, today’s 10.4-year-mine life with an After-Tax NPV (5%) of ~$1.09 billion could ultimately be a 20.0-year mine life when all is said and done, yielding an NPV (5%) of $1.70 billion. Plus, that upside exists without material positive grade reconciliation or pulling ounces forward with a higher throughput rate (sinking a shaft to increase throughput rates or concurrently mining a satellite deposit like Golden Bear).

Valuation

Based on ~406 million fully-diluted shares and a share price of US$2.48, Osisko Mining trades at a market cap of ~$1.01 billion. For some investors looking at many producers trading at less than 1.0x P/NAV, this might make them shy away from Osisko Mining which is still at least 30 months from its first gold pour and trading at 0.92x P/NAV (~$1.09 billion at $1,750/oz gold price). However, it’s important to note that this mine plan is based on just half of the contained resources. Plus, it places zero value on the upside from regional opportunities (Golden Bear, Fox, Fox West), zero value on likely resource growth at depth, and ascribes no value to the recent Lynx 4 high-grade extension 625 meters down plunge from the nearest resource block included in the Q3 2022 mineral resource estimate.

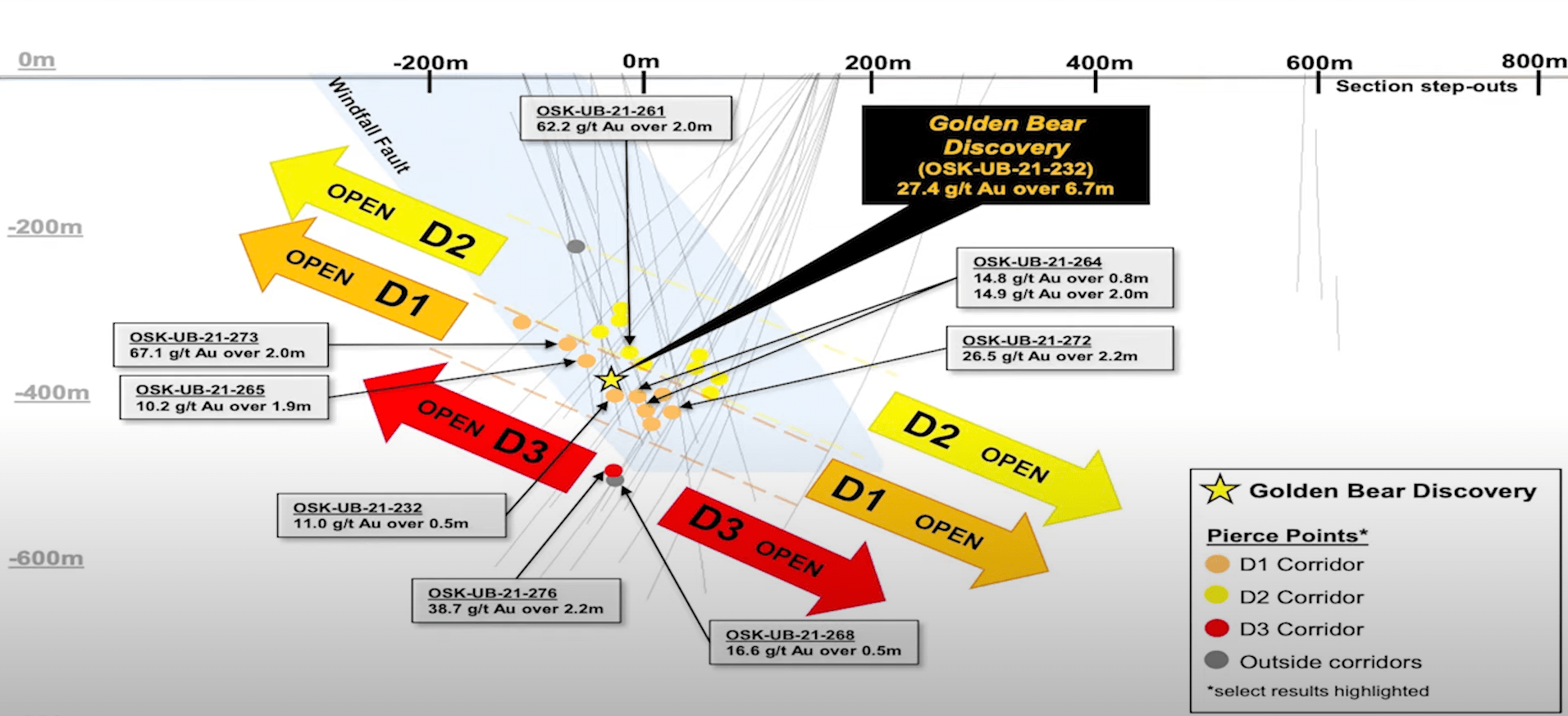

For those unfamiliar, the Golden Bear discovery just north of Windfall is nothing to sneeze at, with a highlight hit of 6.7 meters at 27.4 grams per tonne of gold, multiple 100-gram-meter intercepts within a very small drill program, and the same geology and similar alteration to Windfall, suggesting the possibility of a very nice satellite deposit.

Golden Bear Discovery (Company Presentation)

In addition to this, this mine plan uses what I believe to be ultra-conservative grades relative to the performance of bulk samples and conservative recovery rates (93.1%), suggesting that there’s an upside from a grade outperformance and improved recovery standpoint. If we see improved grades and increased recoveries, this benefit flows directly to the bottom line since the company is still taking the same amount of tonnes out of the deposit each day, but it could get an extra gram of gold on the other end. Finally, from a bigger-picture standpoint, the mine plan is based on just six square kilometers of a ~2,400 square-kilometer land package (Urban Barry). So, with it already looking like this relatively tiny footprint could host 11.0+ million ounces when factoring in resource growth at depth, there’s considerable upside here.

Osisko Land Package, Windfall Camp & Val d’Or Mining Camp For Scale (Company Presentation)

To summarize, the current mine plan does not do this asset justice, and trying to value Osisko based solely on the current mine plan and associated After-Tax NPV (5%) could be a big mistake.

If we apply a fair value of $150/oz to inferred resources (~3.0 million ounces), this represents $450 million in value outside of the current reserve base. Suppose we add another $300 million in exploration upside at Windfall along strike and at depth, assuming the addition of just 1.0 million ounces of additional reserves ($300/oz valuation), which could be very conservative given that I see 11.0-million-ounce resource potential being attainable. Finally, we’ll subtract $150 million in corporate G&A, assuming that Osisko is not acquired and operates this mine independently. The result is that the fair value for Osisko increases to $1.69 billion, or a fair value of US$4.16 at a 1.0x P/NAV multiple.

The result is that Osisko has a 68% upside to fair value. Still, investors are getting any new major discoveries (zero value ascribed to regional opportunities only near-mine), any upside from improved recovery rates (optimized gravity circuit), and positive grade reconciliation (extreme grade capping and bulk same outperformance) for free. Hence, I would argue that this fair value for Osisko of US$4.16 is conservative. It could end up being even more conservative in a takeover scenario, given that suitors are willing to pay well above 1.0x P/NAV for the best discoveries in the safest jurisdictions, as we saw with Fronteer Gold (2011), Kaminak (2016), and Great Bear (2021). In fact, I would argue that Windfall stands up very well to these projects (Long Canyon, Coffee, Dixie).

In fact, Kinross paid $1.45 billion for Great Bear despite it being at least seven years away from production (2029 first gold pour) and without a resource in place yet, suggesting that Osisko is dirt-cheap being five years ahead (Feasibility Stage) with a market cap of $1.01 billion.

Kinross Acquires Great Bear (Kinross News Release)

So, what’s next?

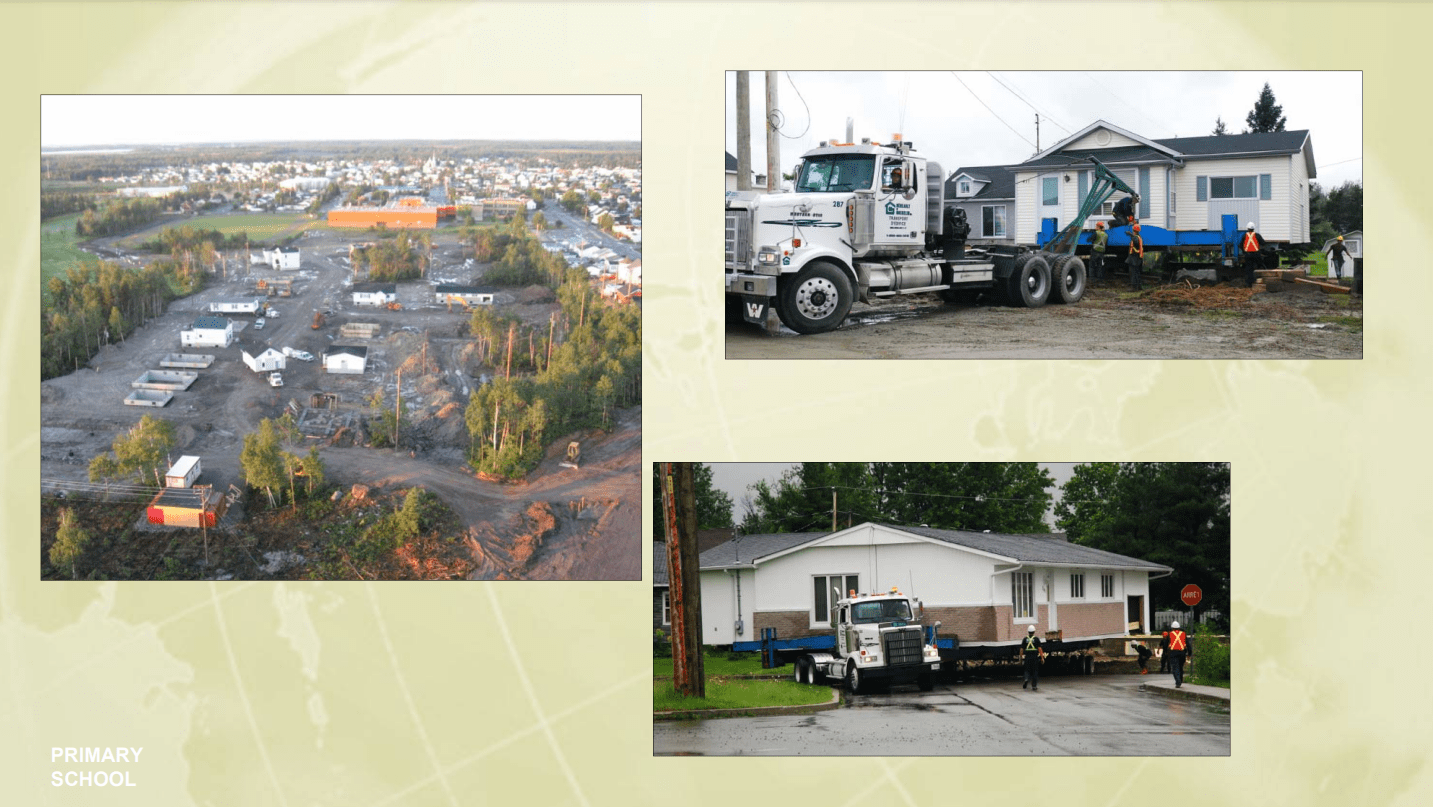

Osisko has disclosed that its next steps are an Environmental Impact Assessment in early 2023 and financing, with a hope to make a construction decision and be fully permitted by early Q2 2024. That timeline would allow for the first gold pour at Windfall by Q4 2025. Some investors might criticize Osisko and suggest that this timeline is too aggressive for a project that is not yet permitted. However, Osisko entered a similar phase of the development stage roughly 15 years earlier at Canadian Malartic, but one that was much more complex given that it had to move a town and construct a much larger ~55,000 tonne per day plant and associated infrastructure (16x the size of Windfall’s plant). It began town relocation in Q3 2008 and produced its gold by April 2011, with one year to permit and ~18 months for a much larger build.

Canadian Malartic Model Pit & Town Relocation vs. Windfall Site (Company Presentation)

As the image above shows, Osisko 1.0 had to relocate over 200 residential homes and five institutional buildings, which is a significant difference vs. the company’s relatively small footprint in a more remote area southwest of Chibougamau in the Eeyou Istchee James Bay region of northwest Quebec, roughly 270 kilometers from Val d’Or and 115 kilometers east of Lebel-Sur-Quevillon. Hence, I don’t think a 1-year permitting process is unreasonable. Plus, I would expect strong support for the project with over $5.0 billion in projected gross revenue, a relatively small environmental footprint, and the creation of nearly 700 direct permanent jobs during operation for the province of Quebec.

Finally, some detractors will note that Osisko previously discussed a 2024 gold pour and that it’s missed its earlier assumptions, and because of this, there’s no reason to trust the current goal of a fall 2025 gold pour. While this is true, the priority with high-grade nuggety deposits should be to de-risk as much as possible before construction so that one doesn’t end up with a Madsen (OTCPK:LRTNF), Phoenix (RBYCF), or a Brucejack, which all considerably underperformed their estimates from a grade standpoint, with two of them being de-listed and shareholders suffering massive losses.

Fortunately, the latter didn’t suffer the same fate as Pure Gold and Rubicon, but Brucejack has underperformed expectations from a grade standpoint vs. its initial projections. However, in Osisko’s case, the company has aggressively drilled this deposit with the completion of 1.7 million meters of drilling. It also has an exploration ramp down to 640-meter vertical depths in Lynx. So, with considerable underground development being complete and very high confidence in the resource model, I see this as very positive. Hence. I would not be surprised to see Windfall surprise on the upside and perform better than planned vs. other nuggety deposits in Canada.

Osisko Mining 1.0 – Town Relocation (Company Presentation)

In summary, the timeline might look aggressive, but this isn’t a team that I would bet against from a timeline standpoint, given the incredible job done to bring the massive Canadian Malartic Mine into production on a very tight schedule with a bigger and more complex build.

Summary

Osisko’s Windfall looks like the closest the sector has to another Fosterville when it comes to deposits not owned by mid-tier or major gold companies, with the potential that this could be a ~330,000-ounce per annum operation at sub $700/oz all-in sustaining costs. In the hands of a senior gold producer that might build a shaft in addition to dual-access ramps to boost mine production rates, this could have ~460,000-ounce per annum potential with a throughput rate closer to 5,000 tonnes per day and similar grades. So, with few comparables sector-wide and this being a sought-after project, investors have two ways to win: Osisko bringing this into production or an accelerated re-rating if a larger mining company launches a takeover bid to acquire the company.

Finally, it’s worth noting that the unique part about Windfall is that this is a project that could be financed with mostly debt due to its rapid payback (~41% after-tax IRR at $1,800/oz), meaning that investors don’t have to worry about an avalanche of share dilution as we saw from Marathon (OTCQX:MGDPF) and Ascot (OTCQX:AOTVF). Hence, with more than one avenue to a re-rating, several catalysts on deck (project financing, regional drilling results, potential new discoveries), and the potential for Osisko Mining to be the 2nd lowest-cost producer in North America in 2026, I see the stock as a Buy on dips.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment