Justin Sullivan/Getty Images News

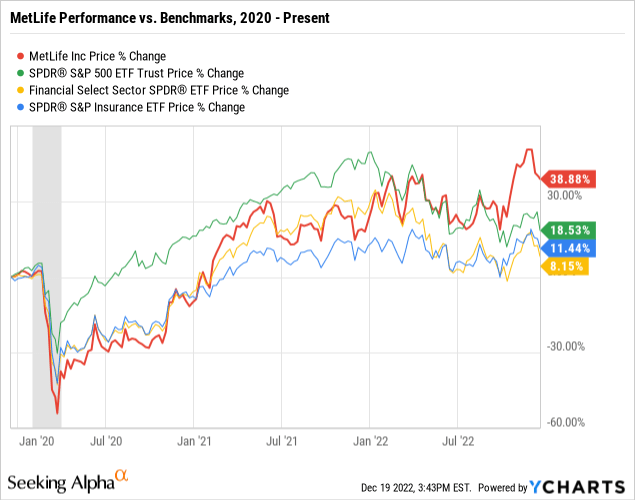

Investors should sell shares of MetLife (NYSE:MET). Despite being up over 12% YTD, these shares are overbought. The firm has been hampered by losses in its investment portfolio, and may be adversely affected by lagging Q4 earnings. MetLife shares have performed well against various benchmarks since 2020, and it is unclear if this trend will continue.

MetLife Background

MetLife began operations in 1868. It has since grown into one of the world’s largest insurance companies, with an estimated 100 million worldwide customers. The firm is headquartered in New York City and led by CEO Michael A. Khalaf.

MetLife has completed numerous acquisitions throughout its history, highlighted by the recent acquisition of Affirmative Investment Management. Affirmative is a top ESG-focused asset manager. The acquisition has bolstered MetLife’s existing asset management segment. MetLife has also disposed of certain business units through sales and spinoffs. In early 2021, MetLife completed the sale of its home and auto subsidiary to Zurich Insurance Group (OTCQX:ZURVY). In addition, MetLife spun off Brighthouse Financial (BHF) in 2017 an order to avoid regulatory headwinds.

With respect to its major shareholders, roughly 75% of MetLife is owned by various institutions. Dodge & Cox, Vanguard, Wellington, and BlackRock (BLK) are the largest of these institutional investors. Insider holdings have not changed much throughout 2022. Moreover, there were not any major open market purchases or sales during the year. The most recent cluster of major insider purchases occurred in 2018. The only major purchases from strategic buyers were MetLife’s own share repurchases at an average of $65 per share. For reference, during 2021, the firm repurchased 72 million shares at an average price of $60 per share.

Business Description

MetLife is a service-driven business with products including life insurance, accident & health insurance, credit insurance, and retirement annuities. The firm also has a substantial asset management presence as one of the largest institutional investors in the United States.

MetLife’s business segments are organized by geography instead of product type. The company’s U.S. segment accounts for over 50% of consolidated revenues and expenses, while the Europe, Middle East, and Asia segment, (EMEA), accounts for under 5% or revenues and expenses. Moreover, MetLife’s Asia segment is its most profitable with a margin exceeding 20%. Its U.S. segment’s margin is around 11%.

MetLife 2021 10K Filing

MetLife’s revenues are driven by its ability to collect insurance premiums and generate interest income from reinvested capital. The firm’s buyer groups consist of institutional customers, including over 96 of the top 100 Fortune 500 companies. Expenses primarily arise from policy holder claims. MetLife also incurs marketing expenses to distribute its products.

Life & Health Insurance Industry Overview

The life & health insurance industry is highly competitive. According to MetLife’s 2021 10-K:

“Certain of the industry’s products can be quite homogeneous and subject to intense price competition. Cost reduction efforts are a priority for industry players, with benefits resulting in price adjustments to favor customers and reinvestment capacity. Larger companies have the ability to invest in brand equity, product development, technology optimization, risk management, and innovation, which are among the fundamentals for sustained profitable growth in the life insurance industry.”

Despite the inherently competitive nature of the industry, there are high barriers to entry for new firms. Four out of the five industry leaders entered the industry prior to 1900. Moreover, these firms have achieved economies of scale owing to their tremendous global reach. There has been a small proliferation of new small and micro capitalization entrants in recent years. While there is not an extensive threat of substitute products, new types of life & health insurance have arisen in recent years. For example, firms like Trupanion (TRUP) have entered the pet insurance niche.

Life & health companies are in a unique situation because their buyers are essentially their suppliers. An insurance company is essentially a pool of its policyholder’s capital. Therefore, since the policyholders are the buyers and suppliers of each insurance product, they have decent bargaining power with insurance companies. Switching policies is not super easy, but can be achieved. If enough policyholders decide that they aren’t satisfied by their current insurance company, they may choose to switch which will damage the existing firm. However, insurance companies have generally gotten themselves in the most trouble due to bad investments in various financial products.

Life & Health Insurance Industry Leaders

MetLife competes with a few other industry giants. Manulife Financial (MFC), Aflac (AFL), Prudential Financial (PRU), and Prudential plc (PUK) make up MetLife’s peer group.

| Ticker | Founded | Headquarters | Employees | Market Cap | Fortune Global 500 |

| MET | 1868 | New York, USA | 45,000 | $57.15B | 121 |

| MFC | 1887 | Toronto, CAN | 38,000 | $33.68B | 277 |

| AFL | 1955 | Georgia, USA | 12,000 | $44.43B | 483 |

| PRU | 1875 | New Jersey, USA | 40,916 | $36.93B | 175 |

| PUK | 1848 | London, UK | 23,000 | $36.14B | 89 |

Warren Buffett looks for “economic castles protected by unbreachable moats.” These five companies are well positioned to withstand economic headwinds. They have shown an ability to grow through mergers & acquisitions in the past, and may continue to devour smaller companies in the future.

Relative Valuation

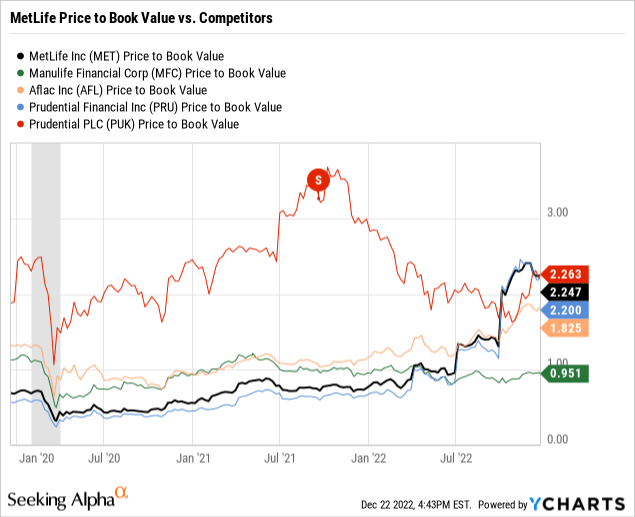

Price/book value is a key metric to consider when analyzing insurance firms. Since most of MetLife’s assets are carried on the balance sheet at fair value, the firm’s balance sheet is an accurate representation of the market value of its assets. A high price/book ratio is not a bad thing when looking at a financial services firm. Oftentimes, a firm will sell at a discount relative to its asset values whenever there are ongoing financial health concerns. This can be thought of as a quasi risk-premium for investors. MetLife, Prudential Financial, and Prudential PLC are all viewed as quite healthy by the market. MetLife has also gone from selling at a discount to its book value to a steep premium since January 2020. The impact of Prudential plc’s spinoff of Jackson Financial (JXN) is also noted on the below graph.

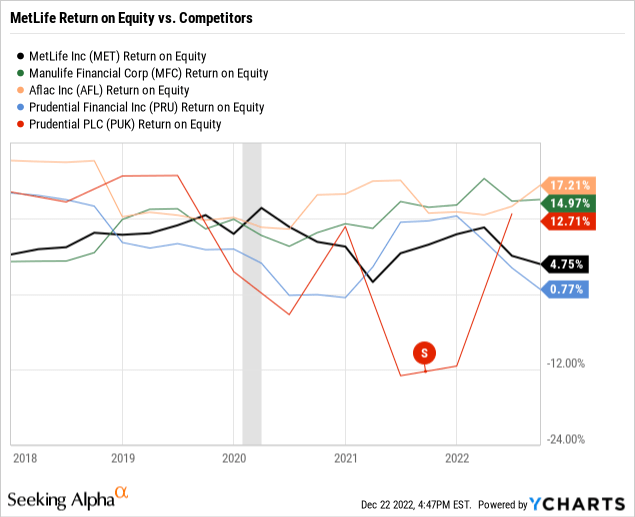

MetLife’s return on equity lags that of its competitors. This means that MetLife is not profiting off of its equity as much as these other firms. If MetLife’s ROE is broken down into its composite parts using an extended DuPont analysis, it is evident that MetLife’s profit margin significantly lags that of Manulife and Aflac. Moreover, while MetLife has a high asset utilization rate, it is makes greater use of financial leverage than Manulife and Aflac. ROE seems to be quite volatile when comparing these companies, and it is likely that higher margins can help MetLife boost its ROE.

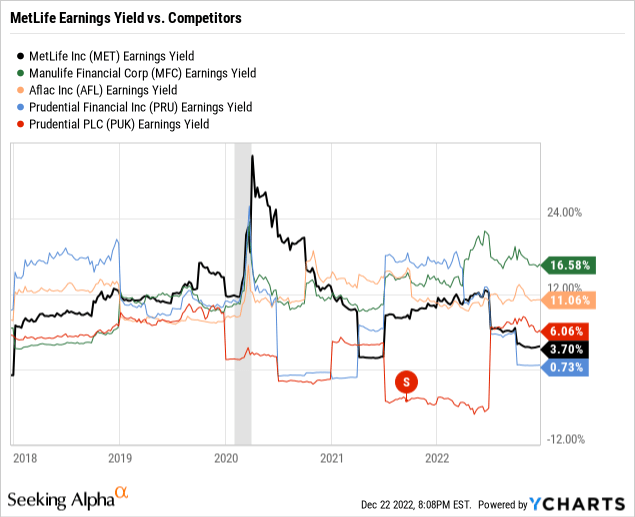

A firm’s earnings yield is the inverse of its price/earnings ratio. A high earnings yield is generally preferable as it means that a company has a high earnings per share per each share of outstanding stock. MetLife’s earnings yield is significantly behind that of Manulife and Aflac.

DCF Valuation

There are multiple methods to intrinsically value a security. At its core, intrinsic valuation consists of estimating future cash flows and discounting these values based on the time value of money. This is especially challenging for firms like x because of uncertainty stemming from earnings volatility. I am a big fan of NYU Stern Professor Aswath Damodaran, and have kept in mind his critiques of using traditional DCF models for financial services firms. I understand the merits of his suggested use of the dividend discount model or excess return model, but I feel that the current economic environment has made dividend policy challenging to predict. Therefore, I have chosen to stick with the traditional DCF model for MetLife. The model’s assumptions are discussed in detail below.

MetLife Filings/Author Calculations

Assumptions:

- Drawn out recession between 2023 and 2025.

- Ten year treasury yields ease.

- MetLife experiences substantial declines in earnings per share prior to recovery.

- A stub period is used to illustrate the fact that cash flows do not occur at the beginning of each period.

MetLife Filings/Author Calculations

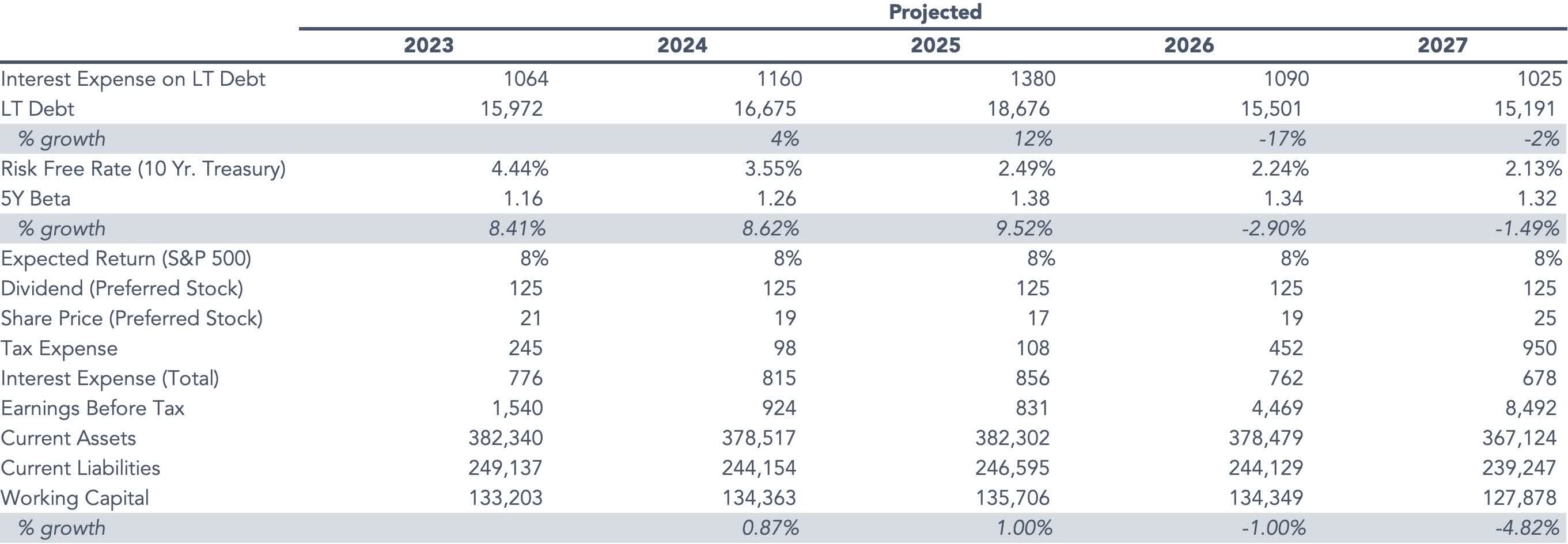

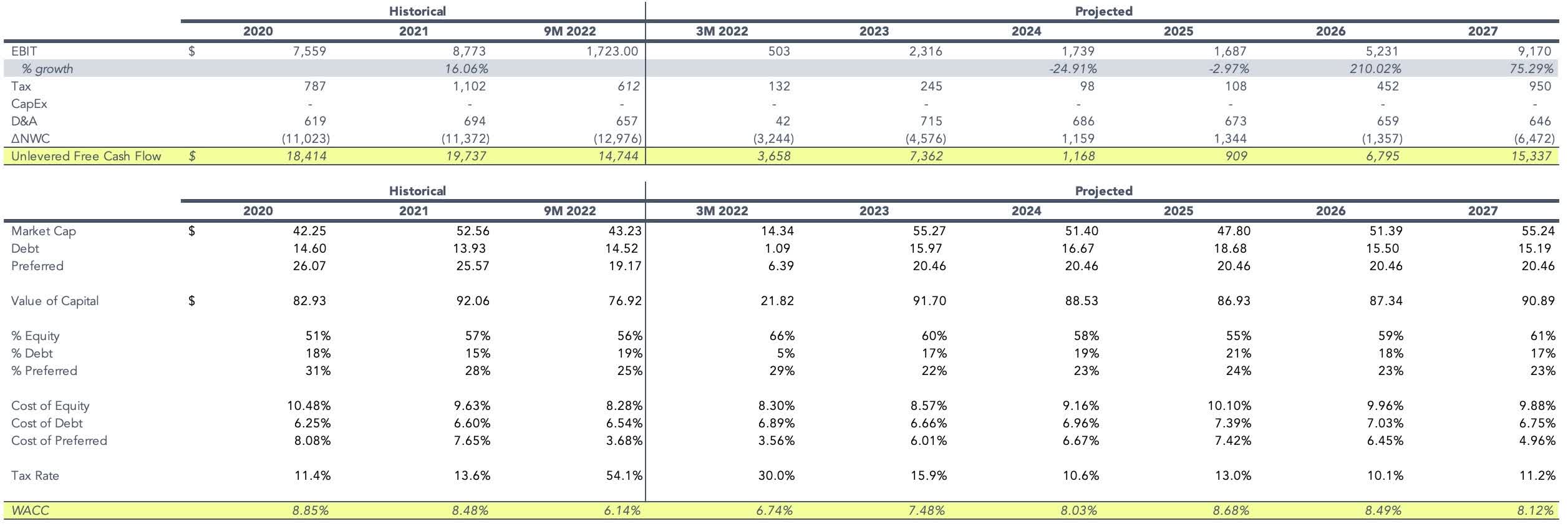

In the model, MetLife experiences declining free cash flow and a rising weighted average cost of capital. The firm has made limited use of long term debt financing relative to its usage of common and preferred stock.

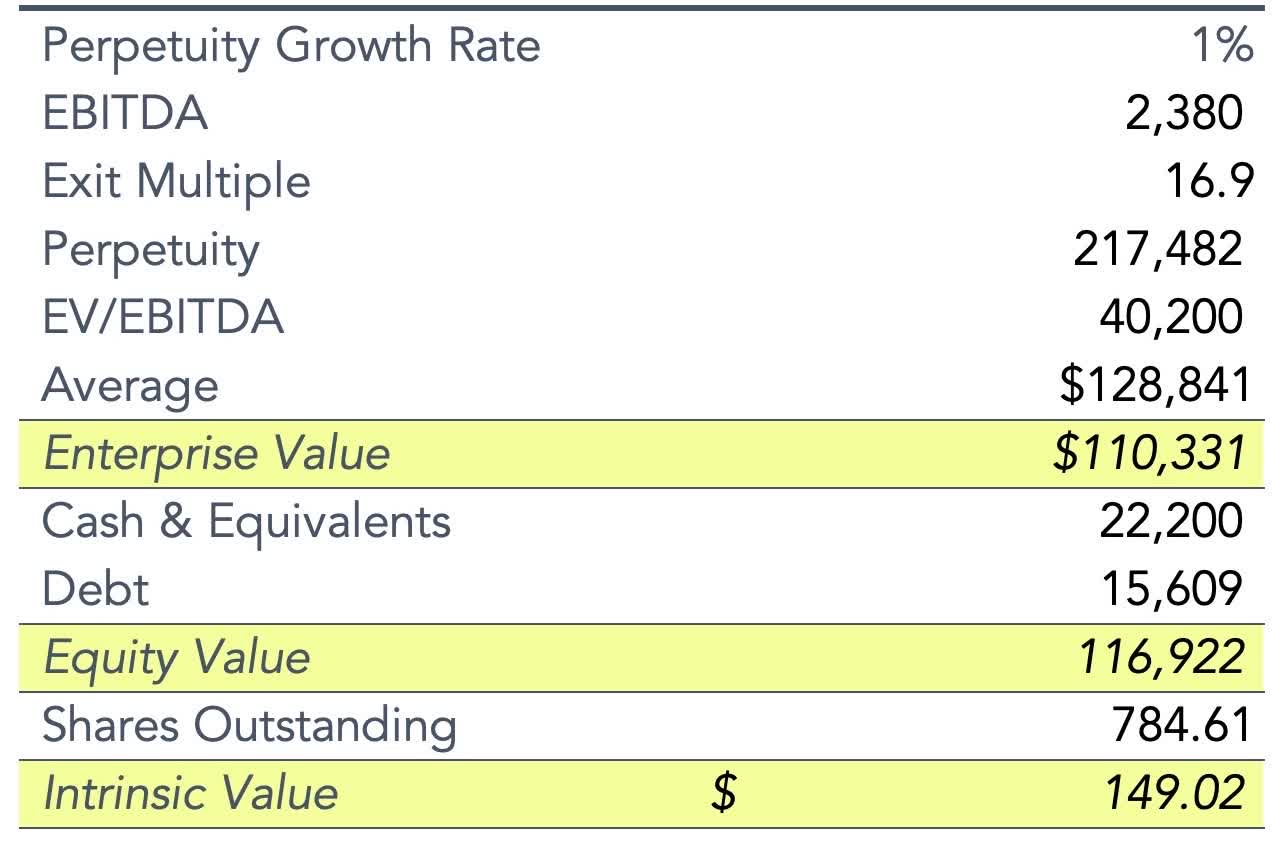

The terminal value calculation was achieved using an average of the Gordon growth method and exit multiple method. Conservatism was used in the estimated 1% perpetuity growth rate. It was surprising to arrive at an intrinsic value of $149. I attempted to make this DCF as bearish as possible. MetLife’s free cash flows were kept quite lower than they had been during prior economic downturns. For example, MetLife’s free cash flow has not dipped below $5 million in over 15 years. I also tried to keep the discount rates as high as reasonably possible. I believe that this model creates a convincing argument for the intrinsic merit of MetLife’s business. The firm has shown a knack for generating free cash flow. Moreover, the firm has done a nice job keeping a reasonably conservative capital structure by limiting the usage of debt.

MetLife Filings/Author Calculations

MetLife’s Dividend

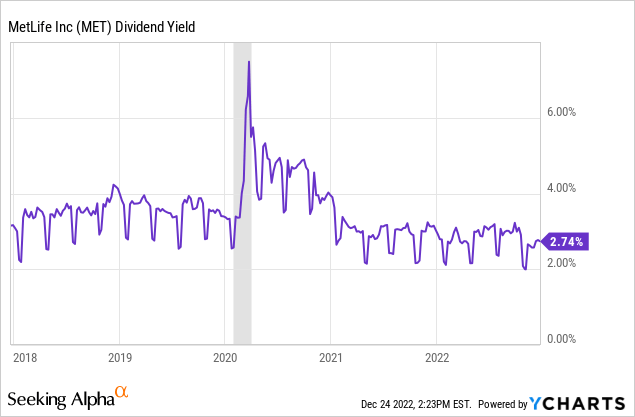

MetLife rewards shareholders via a handsome dividend. The firm has aimed to keep a relatively consistent dividend yield over the past five years. Moreover, MetLife has further rewarded shareholders via repurchases of large quantities of its shares over the past through years. The firm has shown a willingness to maintain these policies through difficult economic periods, and it is a good indication that the firm places such emphasis on returning its cash flow to shareholders.

Key Risk Factors

There are several key risks that investors should consider:

- MetLife has several notable commitments and contingencies. It is currently the defendant in an ongoing asbestos-related lawsuit where the firm could be expected to pay out substantial legal damages. In addition, MetLife is also the defendant in a lawsuit brought on by the State of New York alleging company fraud.

- The firm has been noted by Morningstar (MORN) for its low ESG risk profile.

- MetLife reinvests policyholder capital in various assets. Some of these assets bear little risk, while others are quite risky. For example, commercial loans represent 63% of MetLife’s investment in mortgage loans. Commercial loans are generally viewed as riskier than residential loans, and investors should bear this risk in mind. Nonperforming loans are currently low and have not substantially grown over the past year. Moreover, MetLife has a $327 million exposure to derivative securities. Derivatives are notorious for their role in the 2008 Global Financial Crisis.

- A substantial amount of MetLife’s assets are held in unconsolidated variable interest entities. A VIE is an off-balance sheet vehicle that is used when the company holds a significant variable interest but is not the primary beneficiary in an enterprise. VIEs are not uncommon amongst financial services company, but do pose a noticeable risk given the fact that they are not represented on a company’s balance sheet. As of September 2022, MetLife has almost $70 million of investment securities off its balance sheet. Should these securities go bad, MetLife has a maximum loss exposure of $73 million.

- MetLife is dependent on the stability of its credit rating. The firm currently boasts an Aa3 rating from Moody’s, an AA- rating from S&P, and an AA- rating from Fitch. The firm also has a solid borrowing foundation from a $3.2 billion credit facility.

Investment Conclusion

I feel that it is wise to wait on MetLife. The firm is undoubtedly a fundamentally good business with many makings of a buy. I am however afraid that the market has over rewarded them for this merit. Insurance companies have generally been well-rewarded in 2022 due to the adage that interest rate hikes generally help their business. I am alarmed that despite MetLife’s Q3 earnings decline, the stock has continued to rise. Reversals in the Fed’s monetary policy may cause the market to reevaluate its pricing of MetLife. I can’t tell the future and I don’t want to rely too heavily on the past. I also won’t ask anyone to buy something that I myself am unwilling to buy. Maybe MetLife will continue to outperform the market, but I have significant doubts regarding its valuation. If Q4 earnings are not as expected, trouble could be ahead.

Be the first to comment