Lisa-Blue

Ormat (NYSE:ORA) is a rare asset in that it is one of the few large-scale geothermal owners that is publicly traded, and mostly focused on geothermal. Most of the other large geothermal owners are either state-owned, or part of a large group where geothermal represents only a small percentage of their operations. That makes Ormat stand out, as the 2nd largest geothermal owner & operator in the world. This explains to a large degree its high valuation.

Geothermal is an interesting technology in that it has the highest capacity factor of any renewable resource, and therefore complements nicely with other more intermittent renewable energy technologies, such as solar and wind. It can contribute base-load power with high reliability. In Ormat’s case, it owns & operates a combined ~1.1GW of geothermal power, storage, solar PV & Recovered Energy Generation. Ormat operates three main businesses, Electricity, Product and Energy Storage. The Electricity business generates electric energy and is responsible for about 88% of revenue, Product sells geothermal technology and services to third parties, representing about 8% of revenue. The Energy Storage business specializes in storing electric energy and represents about 5% of revenue, it is the segment expected to grow the fastest, however. Roughly 72% of Ormat’s revenue comes from the US, with the remaining 28% from international markets.

Market Size

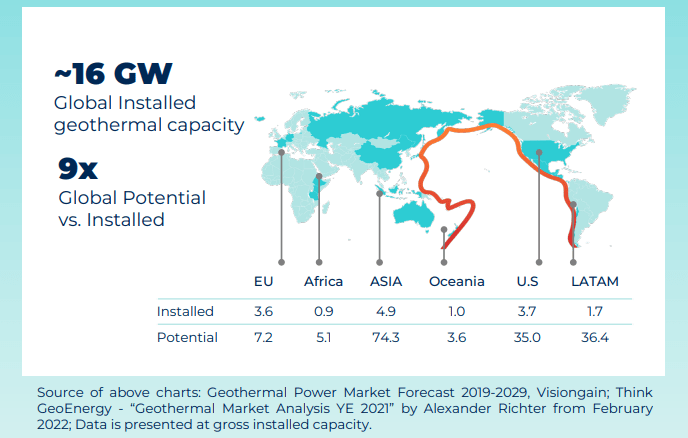

There are currently ~16GW of geothermal installed around the world, but the potential is massive, estimated at 9x versus what currently exists. Just in the next two years ~1,250 MW of geothermal binary capacity is expected to be released. This growth is what makes Ormat interesting, as it is expected to benefit significantly.

Ormat Investor Presentation

Financials

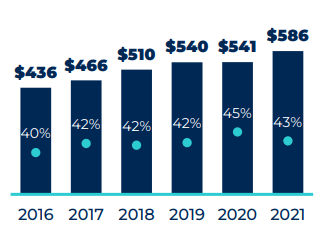

So far, the company has delivered some revenue growth and modest gross margin expansion. In five years, revenue grew from $436 million to $586 million, a ~6% CAGR. Meanwhile gross margins improved ~300bps to around 43%.

Ormat Investor Presentation

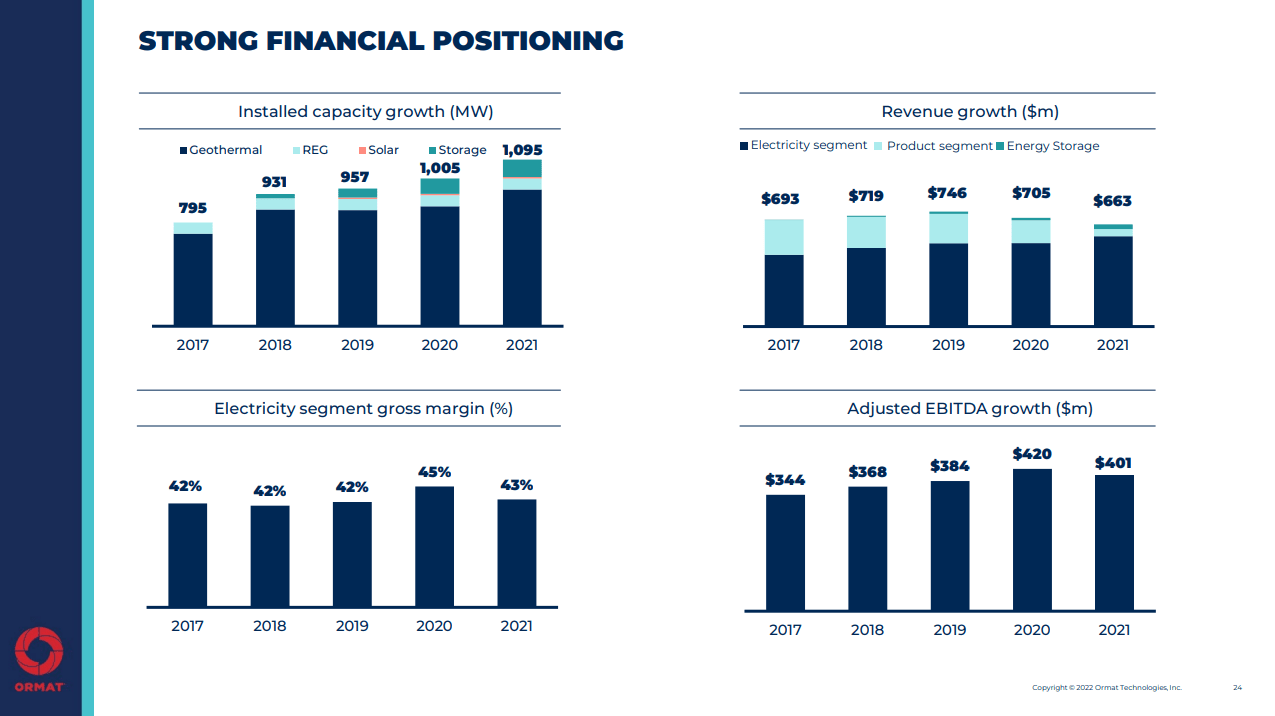

We find these results a little disappointing given that the company grew its installed capacity during the same times period from ~795 MW to 1,095 MW. What seems to have happened is a sharp decline in the Product segment, the one that sells technology and services to third parties. This segment used to be very significant around 2017, but its contribution was significantly reduced in 2021. From the company’s commentary, their growth should come mainly from Energy Storage and Electricity, we therefore are not expecting a rebound from the Product segment.

Ormat Investor Presentation

Growth

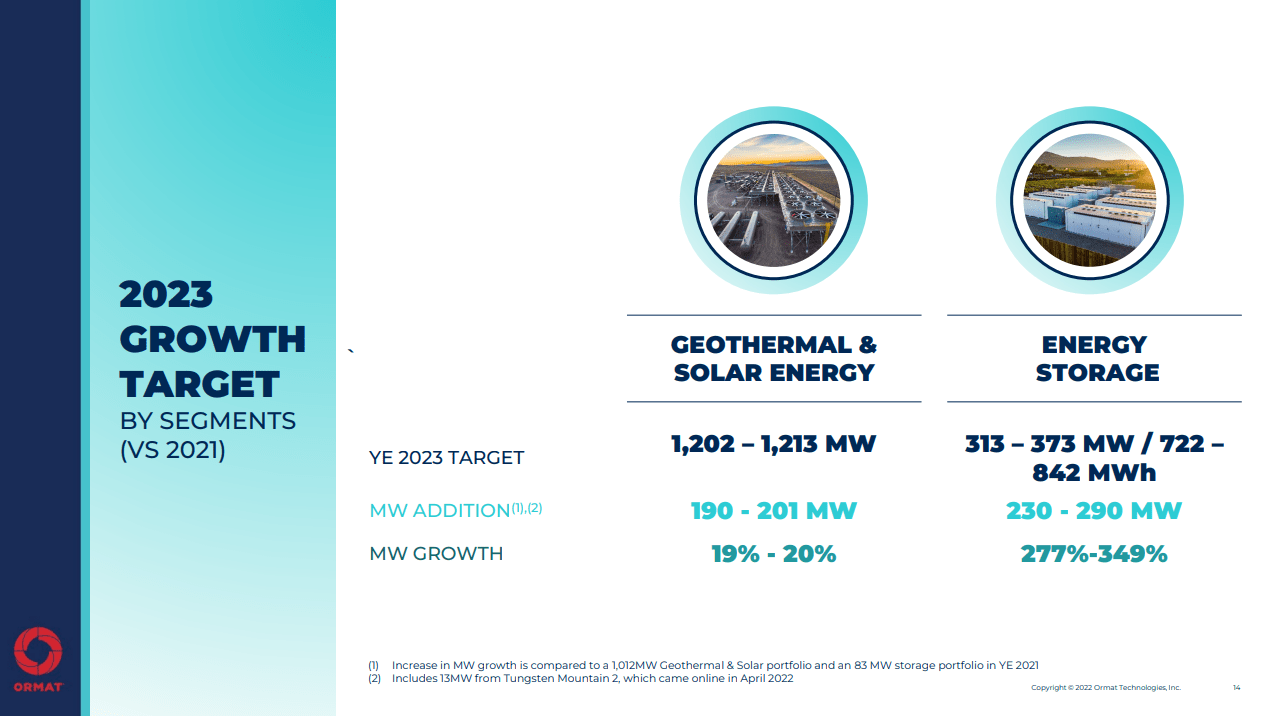

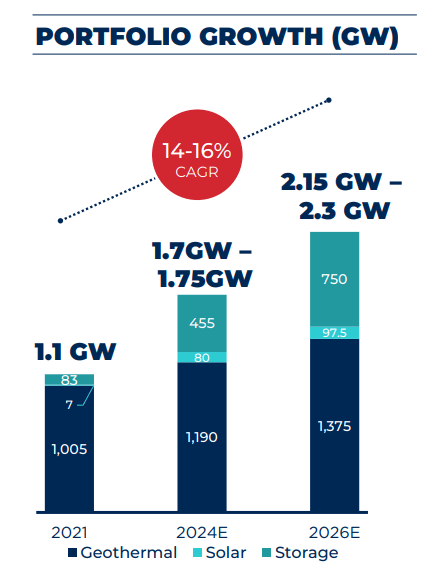

Ormat is expecting a significant increase in Solar and Geothermal capacity and explosive growth in Energy Storage. It is targeting a year-end 2023 portfolio of 1.5GW to 1.6GW, which would represent growth vs 2021 of between ~38% to 45%.

Ormat Investor Presentation

The company does not expect to stop there, but instead to continue growing at a 14-16% CAGR, which would translate into a portfolio of close to 2.3 GW by 2026. That would basically double the size of the company’ assets in 5 years. As can be seen, most of the growth is expected to come from Energy Storage.

Ormat Investor Presentation

Balance Sheet

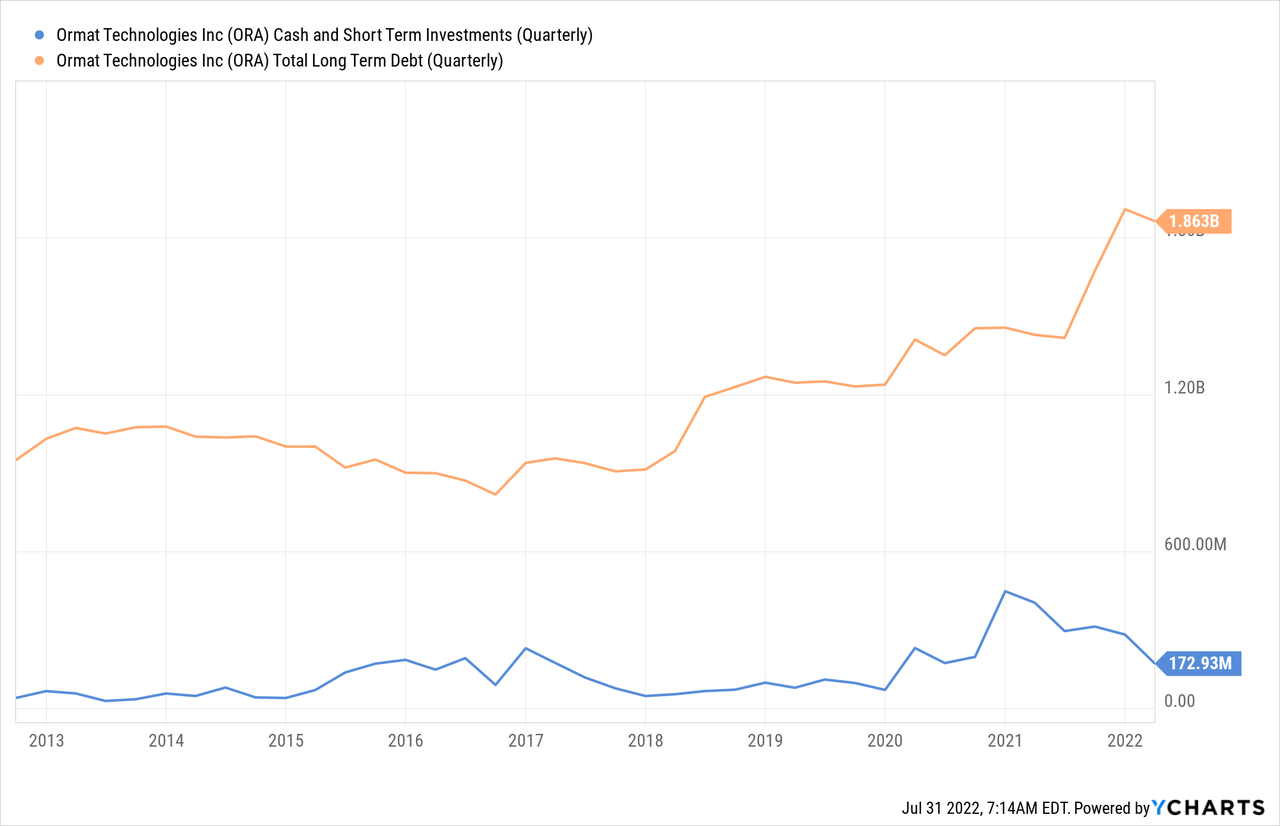

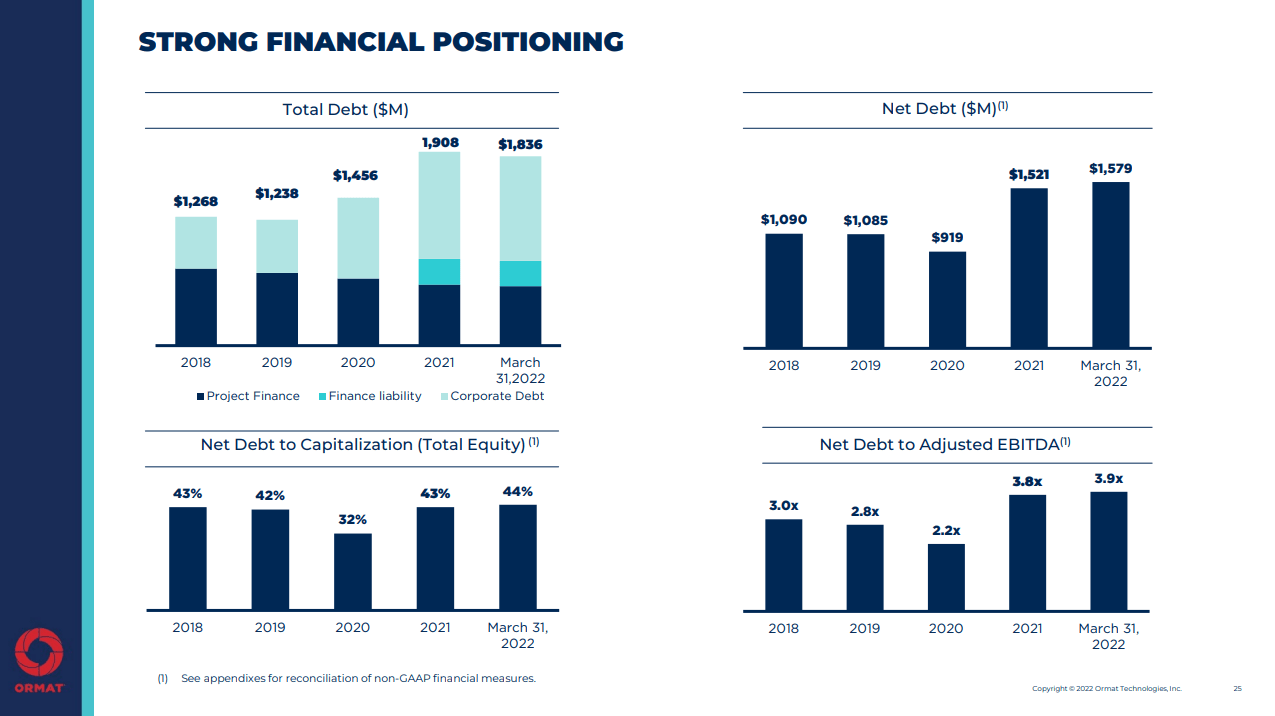

Ormat has been leveraging its balance sheet to finance its growth, and that has resulted in long-term debt approaching $2 billion.

This is still very manageable for the company since it results in a net debt to adjusted EBITDA of ~3.9x. Still, given that most of the debt increase was corporate debt we would not want this to expand much further, especially since net debt to capitalization is already ~44%.

Ormat Investor Presentation

Valuation

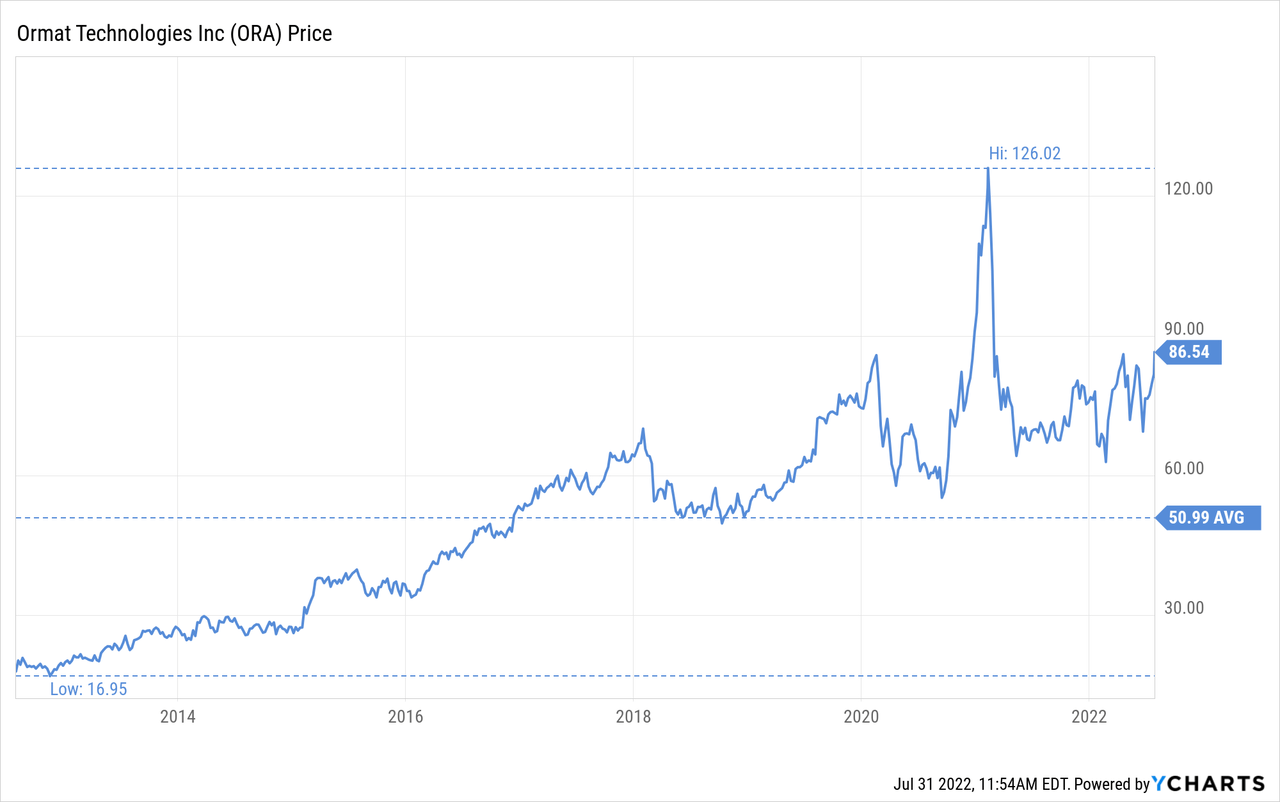

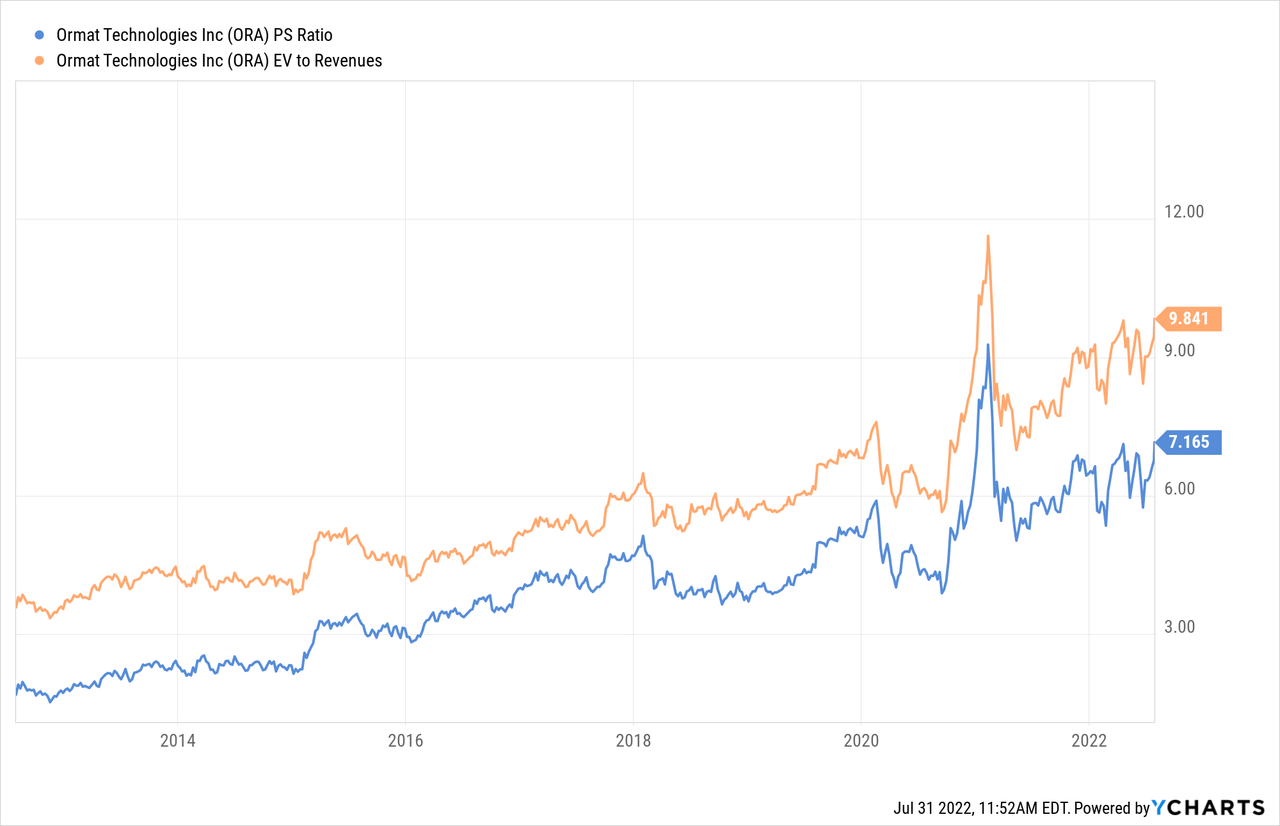

Shares have significantly increased in the last ten years, from a low of ~$16 to a current share price around $86.

The problem we have is that a lot of that growth has simply been multiple expansion. For example, EV/Revenues have expanded from a little over 3x, to more than 9x currently.

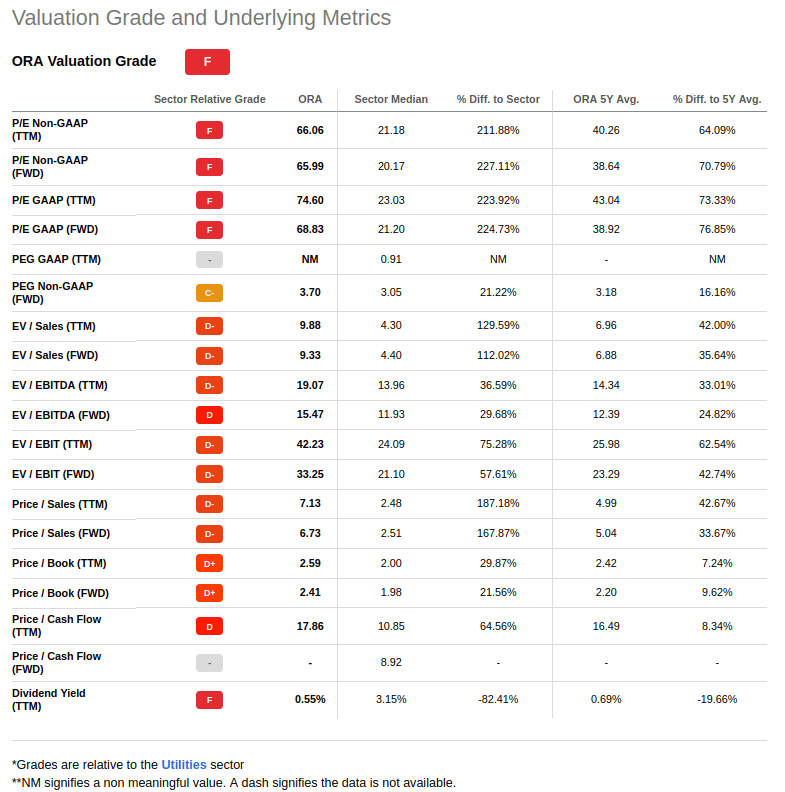

Looking at most valuation metrics for the company on Seeking Alpha we can see that they tell the same story. We believe some of the more relevant ones are price/cash flow, which at 17.8x is about 64% above its utility sector average, and EV/EBITDA which at ~19x is about 36% higher than the utility sector average.

Seeking Alpha

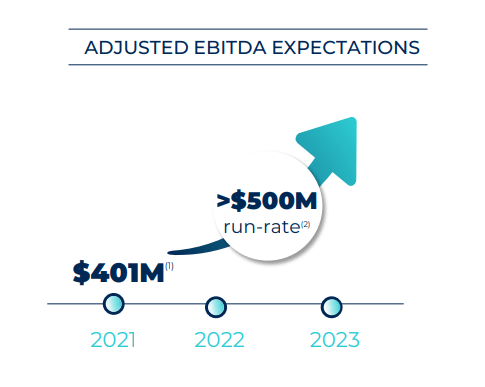

Ormat has a nice growth story, and EBITDA is indeed expected to expand significantly, but we do not believe such premium to other utilities is warranted. On the positive side, adjusted EBITDA is expected to reach an annual run-rate of more than $500 million by the end of 2022.

Ormat Investor Presentation

So how much do we think shares should be worth? We estimate a net present value of the earnings stream of $65, which would put the shares at ~20% overvalued currently. Notice we are estimating strong earnings growth, and we are using a relatively low discount rate of 7.5%, so we believe we are being relatively optimistic with our assumptions.

| EPS Estimate | Discounted @ 7.5% | |

| FY 22E | 1.31 | 1.22 |

| FY 23E | 1.90 | 1.64 |

| FY 24E | 2.25 | 1.81 |

| FY 25E | 2.59 | 1.94 |

| FY 26E | 2.98 | 2.07 |

| FY 27E | 3.42 | 2.22 |

| FY 28E | 3.94 | 2.37 |

| FY 29E | 4.53 | 2.54 |

| FY 30E | 5.20 | 2.71 |

| FY 31E | 5.99 | 2.90 |

| FY 32 E | 6.88 | 3.11 |

| Terminal Value @ 3% terminal growth | 98.33 | 41.28 |

| NPV | $65.82 |

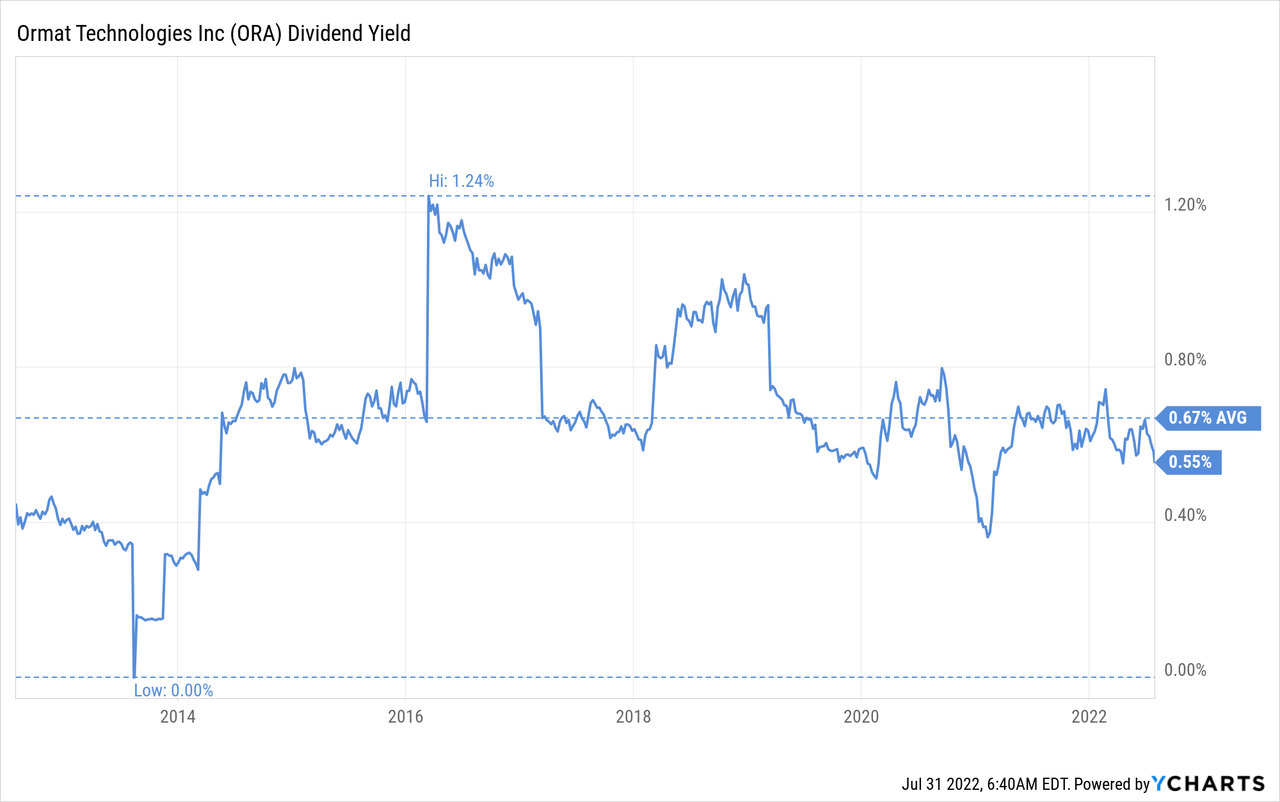

The company does pay a small dividend, but given the low payout and high share price, the dividend yield is tiny, currently ~0.55%.

Risks

We believe that the main risk from an investment in Ormat is the high valuation, which could significantly correct if growth disappoints even slightly. There is also balance sheet risk given the increase in long-term debt, but at this point we believe it is still quite manageable. Fortunately, the technology risk is low given how long Ormat has been developing and operating these types of assets.

Conclusion

We like Ormat’s growth story, especially the explosive growth that the company is expecting in its Energy Storage segment. That said, we are not prepared to pay a huge valuation premium to the utilities sector. We estimate shares to be about 20% overvalued currently and would need to see a healthy price correction before considering the shares. We plan on continuing to follow the company, see how its growth develops, and hopefully there will be an attractive entry price in the future.

Be the first to comment