THEPALMER/E+ via Getty Images

Investment Thesis

It’s been a few months since I first wrote about OneWater Marine (NASDAQ:ONEW). Although the results since then have been satisfactory, I have come to realize that perhaps I left out a significant part of the picture in that research.

In this article, I want to reconsider some aspects of the business and its future based on the annual results that the company presented last November. I will also update the valuation according to the new guidance provided by management. While I still believe the company is a ‘buy,’ there are key aspects about its profit margins and cash generation that should be taken into account before investing, aspects that I did not mention earlier.

Seeking Alpha

Business Overview

OneWater Marine operates as a recreational boat retailer in the United States. They offer new and pre-owned boat sales, finance and insurance products, as well as other related services. OneWater Marine represents various boat brands and typically has a network of dealerships across different regions.

The products offered by the company span from Jet Ski and Recreational Yachts to Saltwater Fishing boats, providing a diverse range of options to meet various needs. However, it’s important to note that the company primarily sells third-party brands. This approach has both positive and negative aspects.

- On the positive side, offering a wide variety of products can attract a larger customer base without the need to invest heavily in research and development or manufacturing plants. This strategy allows the company to cater to different market segments and preferences.

- On the downside, relying on third-party brands means the company has less control over its supply chain. Additionally, it necessitates the storage of a significant amount of inventory. This reliance on inventory can result in negative working capital, a situation we will explore further later on. Balancing the benefits of a diverse product range with the challenges of supply chain management and inventory control is a key consideration for the company’s overall strategy.

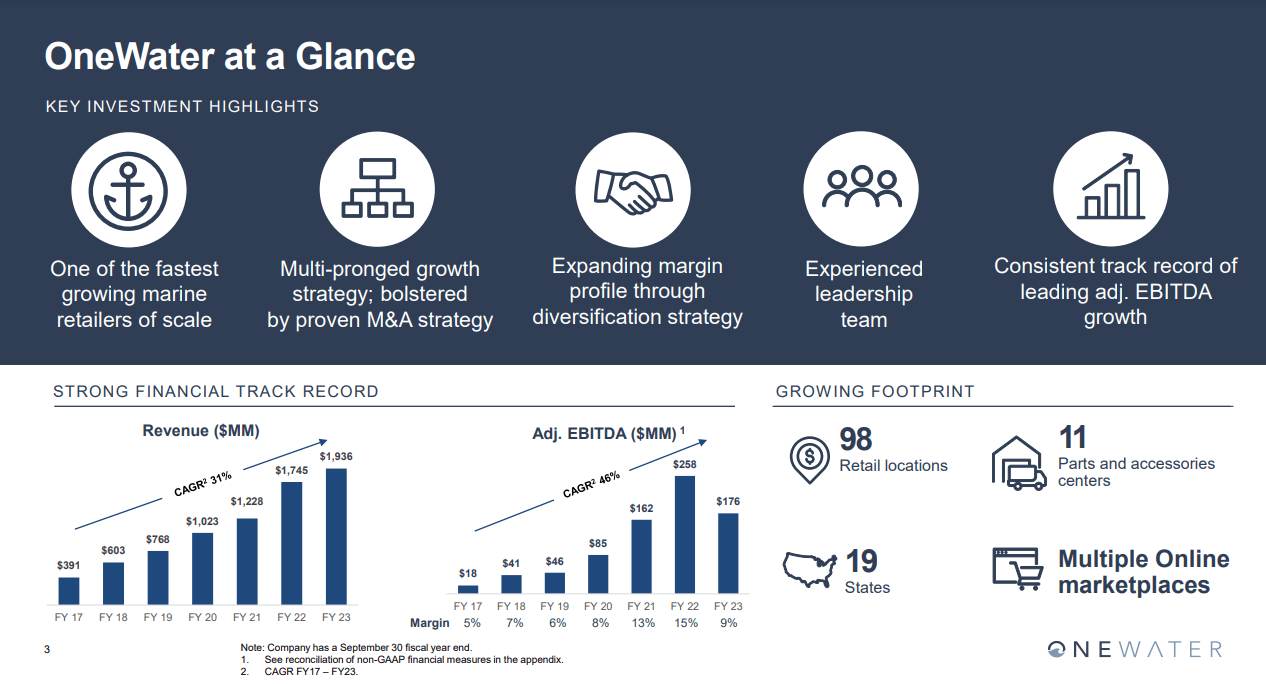

While the core business itself may not be characterized by high-growth, the company has strategically leveraged the fragmented nature of its market to expand by acquiring other small retailers at favorable prices. The consistently high Return on Capital Employed, averaging 25% since 2018, highlights the efficiency of this growth strategy. For more detailed insights into this aspect, I delve deeper into the topic in my previous article. This approach allows the company to capitalize on opportunities in the market and enhance its overall market presence and competitiveness.

OneWater Investor Presentation

Full Year 2023 Results

In November of last year, the company announced the results of its fiscal year 2023. The results presented were as follows:

- Revenue increased 11%

- Same-store sales increased 3%

- Gross Profit decreased 3.3%

- EBITDA decreased 81%

- EPS: -$2.69

Growth was not bad, although 75% of the growth was due to acquisitions made. However, the profitability of the year was disastrous. One detail that must be highlighted is the fact that during the year, the company recorded an intangible asset impairment charge.

The charge is primarily related to the write-down of goodwill and identifiable tangible assets that were reported in our Distribution segment and was largely driven by the recent decline in the segment results, the stock price and the overall valuation.

CFO Jack Ezzell Q4 Earnings Call

Although accounting requires you to record it as a loss on the Income Statement, an impairment does not result in an actual cash outflow. This does not mean that it should be taken lightly, as it indicates that the company either did not evaluate its assets well or that they are deteriorating. However, if we want to evaluate purely operational performance, it is worth adjusting the profits by adding back the value of the impairment. The adjusted results would be as follows:

- EBITDA decreased 18.5% or almost $44 million year over year

- EBITDA Margin: It went from 13.5% to 9.9%.

- EPS: $7.60 decreasing -16.8% year over year

- Net Margin: Went from 7.5% to 5.6%

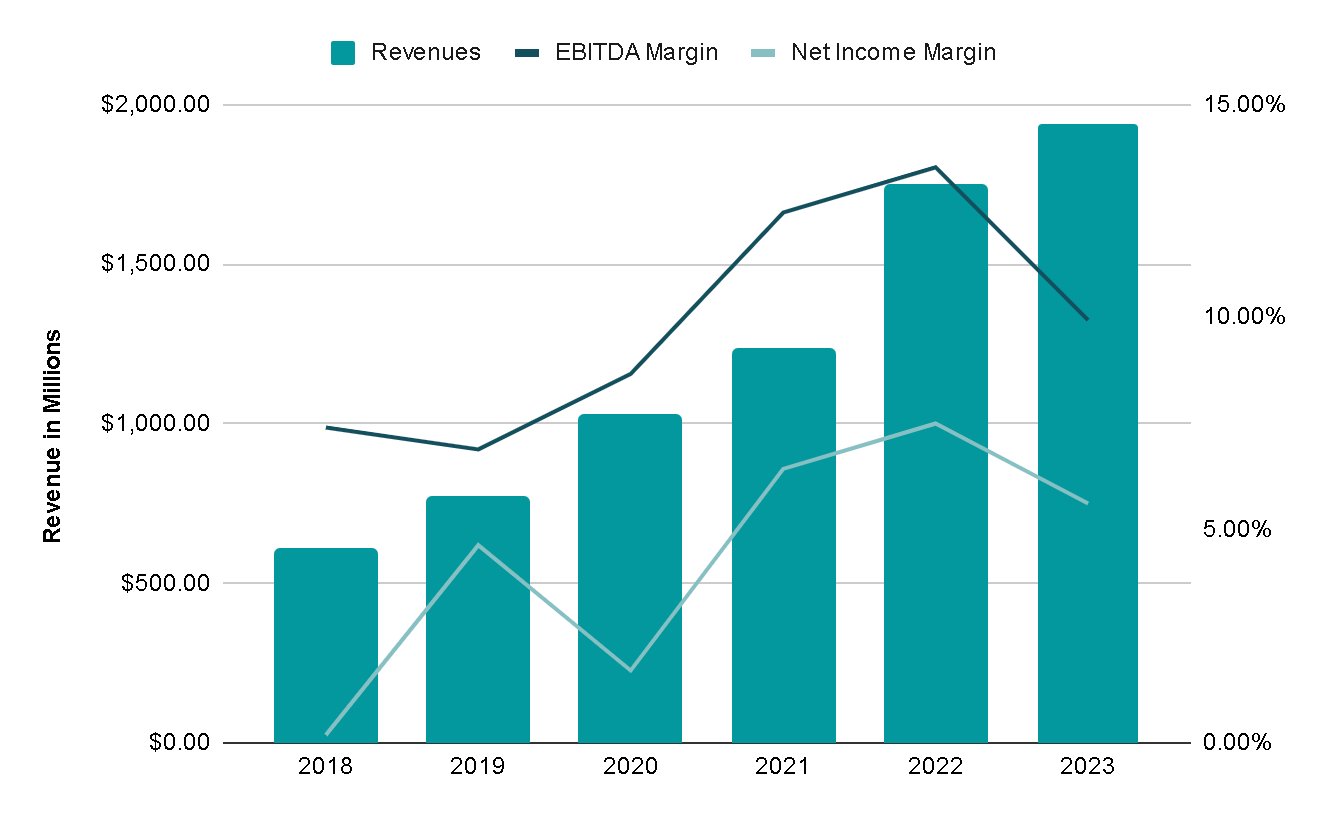

These are still unfavorable results, but I find it very interesting that, when put in context with the last five years, it seems that a normalization of margins is occurring. Between 2018 and 2020, EBITDA margins averaged 7-8%. However, I believe that in 2021 and 2022, when the Federal Reserve started printing money and providing stimulus, it increased consumption and caused the company to be abnormally profitable. Therefore, the return of the EBITDA margin to 10% is considered normal, and I would not be surprised to see it return to the 8-9% range it presented in 2020. I would expect the same for the Net Margin.

Author’s Representation

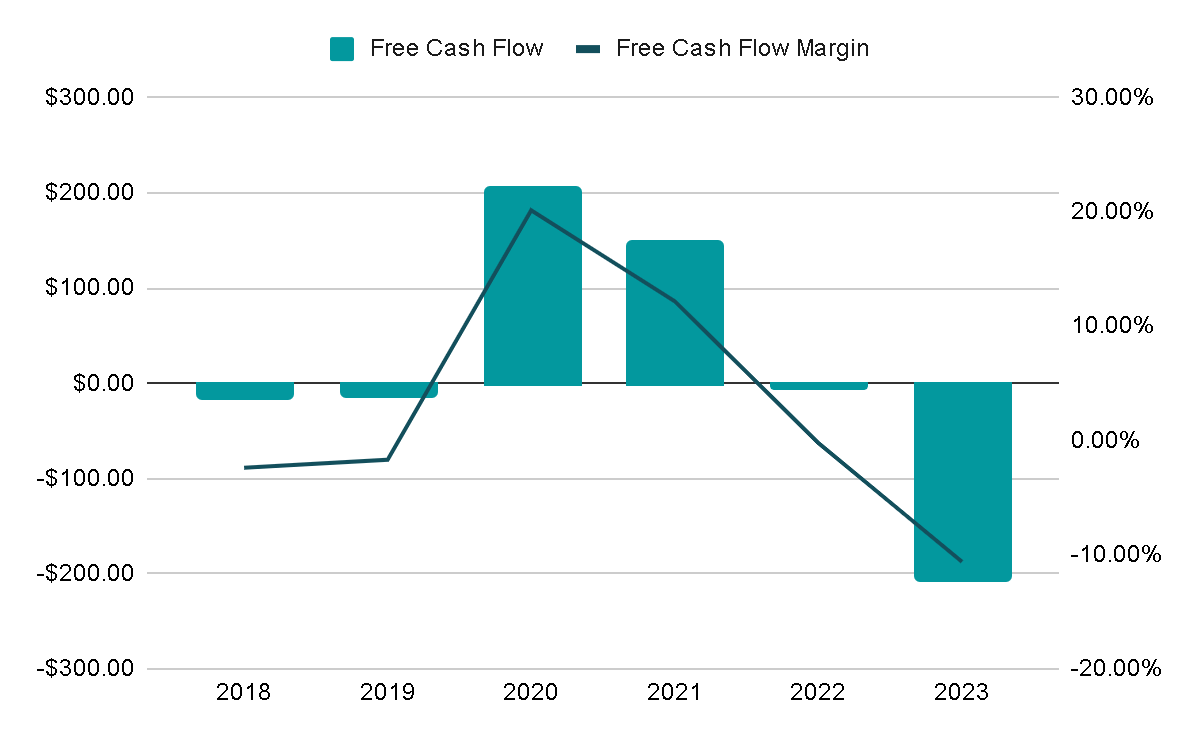

This can be observed in the Free Cash Flow as well. This year it was -$200 million, even considering that the impairment is not reflected in this financial statement. This is attributed to a $232 million increase in inventories, which is normal for this company that usually operates with high inventories. Only during 2020 and 2021 was the company extremely generating cash flow, which, again, seems to me to be an anomaly. Now, we are witnessing the normalization of this trend.

Author’s Representation

Services are the Way

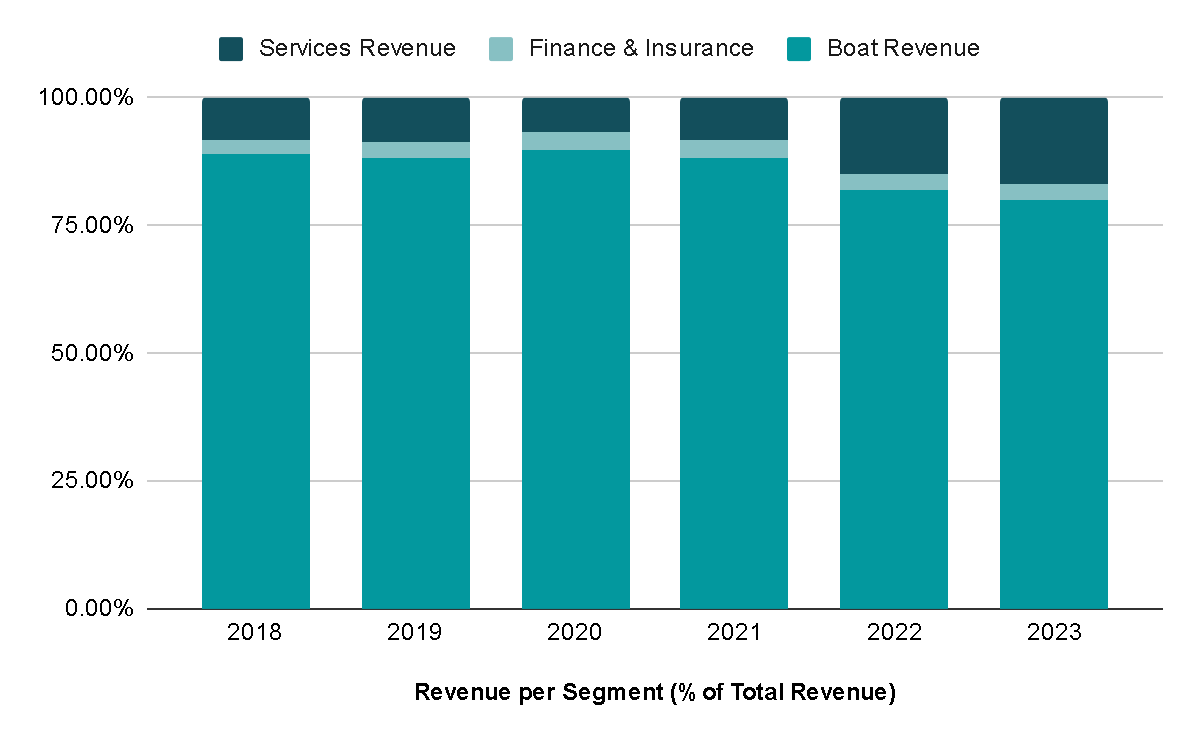

The results are unfavorable in general terms, and the explanation lies in the business being affected by both operational normalization and a worsening economy. This has led clients to postpone the purchase of yachts and boats, as evident in the previously mentioned increase in inventories. This underscores the highly cyclical nature of the company. However, there is a ray of light on the horizon to mitigate this impact, and it is the Services segment. During FY2023, it already represented 16.5% of revenue compared to 14.6% the previous year and 8% five years ago.

Author’s Representation

In my previous article, I emphasized that it seemed crucial for the company to focus on improving this segment, and this year’s results provide clear proof of why this is the case.

A significant point of emphasis is the decreasing weight of boat sales in the company’s revenue mix, while services such as maintenance are gaining greater relevance. This shift is vital as it mitigates the company’s risk during economic downturns.

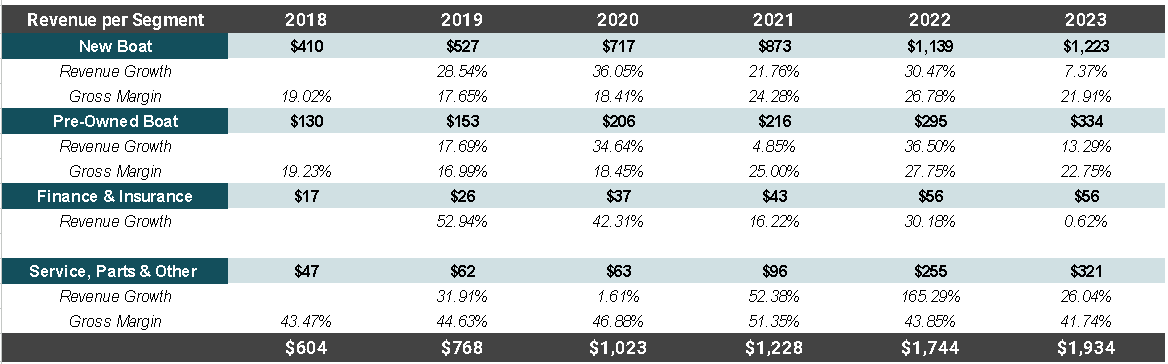

During FY2023, revenue from New Boats grew by 7%, which is not bad considering the less-than-ideal macroeconomic environment. However, this growth is notably lower than the average annual growth of 30% in previous years, and the Gross Margin fell by 18%. On the other hand, Services, which includes maintenance or replacement of boat parts, experienced a robust 26% growth this year. The Gross Margin in this segment only decreased by 5%, demonstrating how this segment acts as an effective defense against exposure to the economic cycle. It significantly improves the quality and predictability of the company.

Author’s Representation

Updated Valuation

In summary, it is evident that the company is being influenced by the macroeconomic environment, and its results are undergoing normalization. However, despite these challenges, it managed to achieve organic growth of 2.7%, and its margins are approaching those of 2020. This assures us that we are not dealing with inflated profits due to abnormal returns.

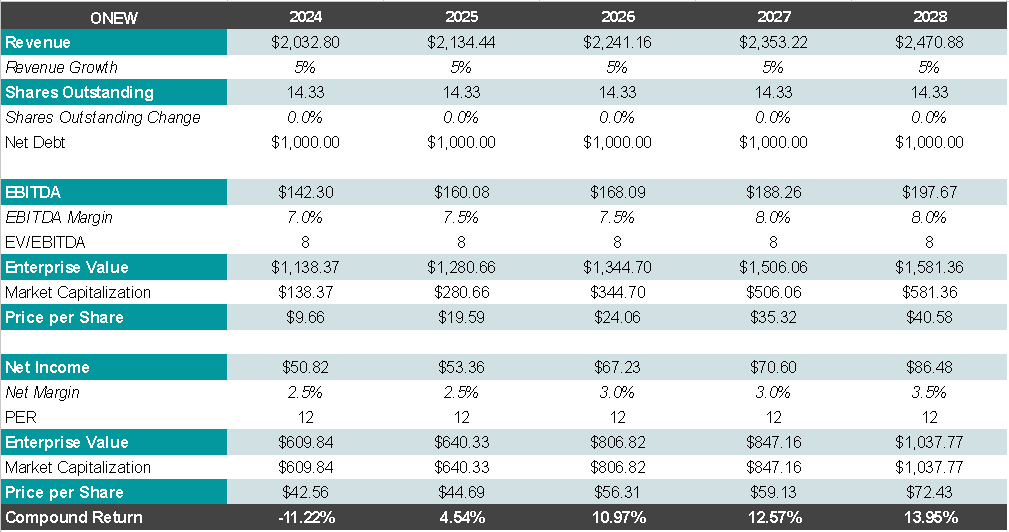

To assess the potential return at the current price, I will estimate that the company will continue to grow organically at a rate of around 2-3%, with an additional 2-3% contributed by inorganic growth, resulting in a total annual revenue growth of 5% in the coming years—a reasonable and conservative assumption, in my opinion.

Author’s Representation

If we project margins more in line with a typical environment and assume a slight expansion in subsequent years due to economies of scale and cost optimization, we could expect earnings per share to be around $3.55 this year and potentially reach $6 USD within five years, assuming no dilution or buybacks. Applying an exit multiple of 12x the earnings, the expected annual return would be around 14%, which is quite attractive given the cautious nature of the valuation.

This estimate aligns somewhat with the guidance provided by management during Q4 2023:

We expect adjusted EBITDA to be in the range of $130 million to $155 million, and earnings per diluted share to be in the range of $3.25 to $3.75.

CFO Jack Ezzell Q4 Earnings Call

Final Thoughts

After annual results, I now find myself considerably more cautious regarding my opinions of the company. While the company has delivered a great return since I wrote my previous article, I did not correctly emphasize how inflated the earnings were and that a cyclical company always appears cheaper when it is at the peak of its cycle.

Despite all this, it seems to be different now. Profits are deflating, the business has continued to grow decently organically in the face of an economic slowdown (although it’s not a severe recession), and the most attractive aspect is the notable increase in the Services segment. If we add to this a compelling return, making a conservative valuation, since just with acquisitions the 5% assumed growth should be met and the organic growth would still need to be added, it makes me think that at the current price, the company is still an interesting investment option.

Be the first to comment