BlackSalmon/iStock via Getty Images

Elevator Pitch

My investment rating for OneConnect Financial Technology Co., Ltd.’s (NYSE:OCFT) [6638:HK] stock is a Hold. The spotlight is on OCFT’s strategic pivot focusing on a narrower product portfolio and larger clients. Based on the company’s recent financial performance, it is premature to judge the success of OneConnect Financial’s new strategy. In that case, a Hold rating for OCFT is the most appropriate.

Company Description

OneConnect Financial describes itself as “a technology-as-a-service provider for the financial services industry in China” in the company’s press releases. OCFT was first started in December 2015, and its shares have been listed on New York Stock Exchange and the Hong Kong Stock Exchange since December 2019 and July 2022, respectively.

As highlighted in its Q3 2022 financial results presentation, OCFT generated more than half or 51% of its top line in the first nine months of 2022 from the Gamma Platform. In its media releases, OneConnect Financial refers to the Gamma platform as “a technology infrastructural platform for financial institutions.” OCFT’s digital banking offering, digital insurance offering, and its virtual bank known as Ping An OneConnect Bank contributed the remaining 28%, 19%, and 2% of the company’s 9M 2022 revenue, respectively.

Strategic Pivot

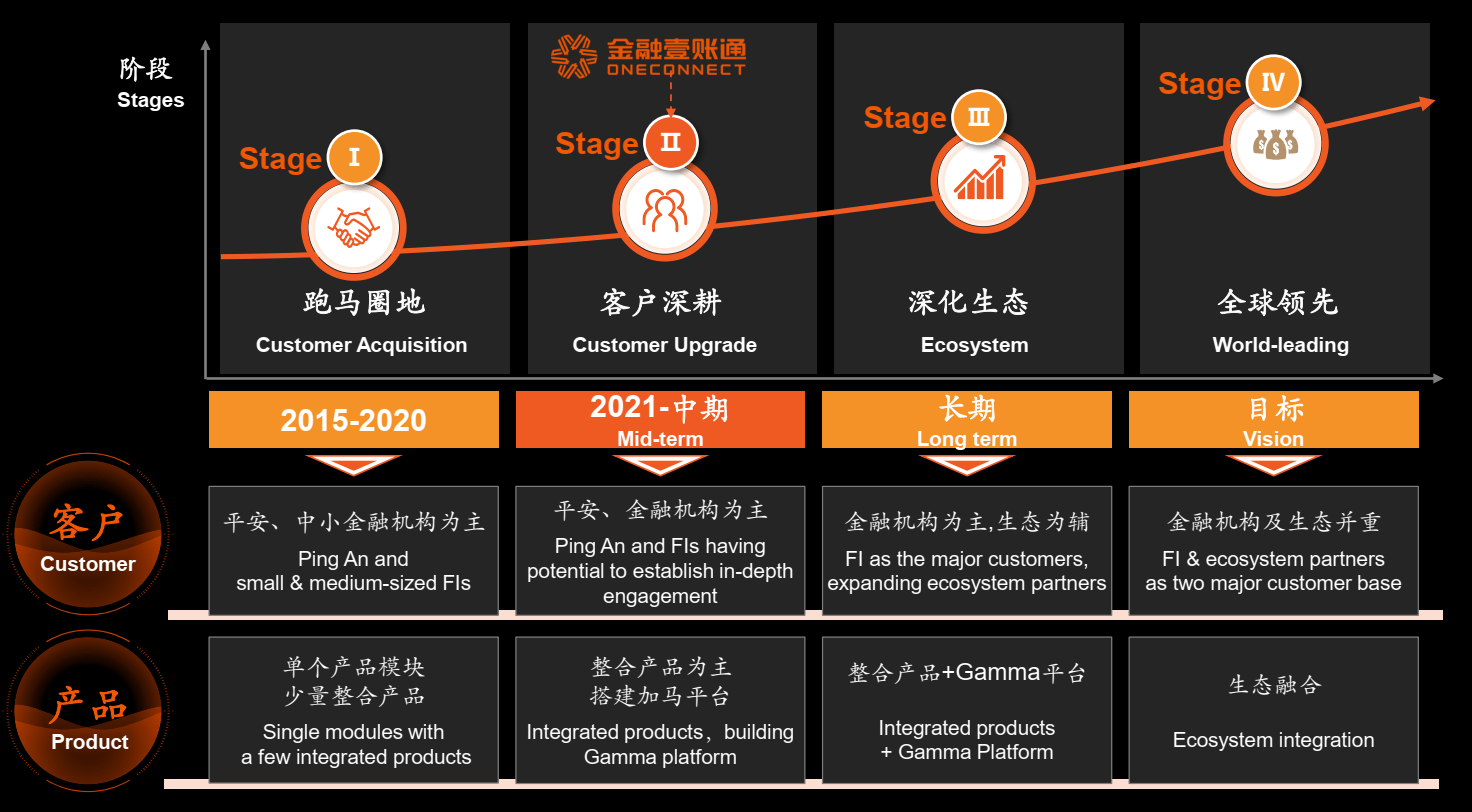

Earlier in September 2021, OneConnect Financial announced its new strategy of “strengthening the company’s customer base, products” via measures such as “minimizing low-production business and optimizing its structure.” In this article, I analyze how OCFT’s strategic pivot has impacted the company’s financial performance.

OneConnect Financial’s Strategic Pivot

OCFT’s Q3 2022 Results Presentation

Product Strategy Changes Have Led To Narrowing Of Losses

OCFT previously marketed its offerings to its existing and potential clients in the form of multiple single modules between 2015 and 2020. This was very inefficient, and resulted in OneConnect Financial having a bloated cost structure. Since late-2021, OCFT has initiated a new strategy with a focus on selling a few selected integrated products, which include its Gamma platform and other offerings such as digital insurance and digital retail banking.

The changes to OneConnect Financial’s product strategy have paid off for the company as indicated by the company’s recent financial metrics.

Net loss for OCFT has narrowed from -RMB270 million in the third quarter of 2021 and -RMB245 million in the second quarter of 2022 to -RMB133 million for the most recent quarter as per S&P Capital IQ data. OneConnect Financial’s actual operating loss of -RMB155 million in Q3 2022 turned out to be much better than the sell-side analysts’ consensus financial forecast of -RMB272 million.

Pivoting to a new strategy focused on a handful of integrated products (as opposed to multiple single modules) has boosted OneConnect Financial’s bottom line. As an illustration of how OCFT has become more efficient with a more focused product strategy, the company’s selling, general & administrative (SG&A) expenses have been on a downwards trend. The SG&A-to-revenue ratio for OneConnect Financial decreased from 34.8% for Q4 2021 to 31.4% in Q1 2022, before declining further to 26.5% and 24.4% for Q2 2022 and Q3 2022, respectively.

Looking forward, the sell-side analysts predict that OneConnect Financial will register a narrower normalized net loss of -RMB576 million in fiscal 2023 (versus OCFT’s FY 2022 expected bottom line of -RMB892 million) as per S&P Capital IQ’s consensus data. In my opinion, the market’s consensus profitability expectations are realistic, as OCFT should continue to generate cost savings relating to the streamlining of its product portfolio.

Slowing Revenue Growth And Client Concentration Risk Are Key Concerns

OneConnect Financial’s strategic pivot is a double-edged sword; while OCFT’s profitability has improved as a result of the product strategy changes, this has in turn hurt the company’s near-term revenue growth prospects. Also, customer concentration risk is still a major risk factor for OneConnect Financial.

OCFT achieved a marginal YoY revenue growth of +0.4% for the recent Q3 2022, which is significantly below the company’s top line expansion of +17.2% YoY and +24.3% YoY for Q2 2022 and Q3 2021, respectively. Apart from COVID-19 restrictions in Mainland China which limited in-person interactions (and marketing of the company’s products), OneConnect Financial’s top line was also negatively impacted by the company’s pivot towards integrated products.

The company acknowledged at its prior Q3 2022 earnings briefing on November 11, 2022 that its product portfolio changes came “at the expense of some projects (being lost) and (revenue) growth rate.” It is likely that OCFT will need a longer-than-expected period of time to adapt to its new product strategy change and resume rapid top line growth again. Based on the market’s consensus financial estimates obtained from S&P Capital IQ, OneConnect Financial’s revenue growth rate is projected to moderate from +24.8% for FY 2021 to +9.7%, +10.2%, and +13.6% for FY 2022, FY 2023, and FY 2024, respectively.

Separately, it is also disappointing that OCFT hasn’t made any meaningful progress in diversifying its client base and reducing its customer concentration risks.

Besides product portfolio optimization, OneConnect Financial’s strategic pivot also involves targeting larger financial institutions as customers to reduce the reliance on its biggest clients. OCFT’s recent metrics suggest that the company has to put in more effort to mitigate client concentration risks. The percentage of revenue generated by OneConnect Financial’s top two customers was 67% in Q3 2022 and the same as that for Q3 2021 as revealed in OCFT’s Q3 2022 results presentation.

Closing Thoughts

I award a Hold rating to OneConnect Financial Technology. More time is needed to monitor the progress of OCFT’s strategic pivot to determine if it is a success. On the positive side of things, OneConnect Financial’s cost structure has become leaner. On the negative side of things, OCFT’s top line growth has been adversely affected by the strategic changes.

Be the first to comment