vitranc

Broadmark Realty Capital (NYSE:BRMK) is a national hard-money lender REIT, with a $900 million loan book.

The company specializes in high-risk, high-interest loans that are backed more by collateral than by the borrower’s credit history or credit score. I wrote a buy rated article on the company in June. The company’s stock has fell 40% since.

The reasons behind the recent fall are multiple. BRMK was recently hit by higher provisions for loan losses, property management expenses, and interest charges. The company’s CEO and CFO resigned, with the company’s Chairman and founder now at the helm. Its dividend was cut in half (something that was expected).

Still, I believe BRMK is an opportunity. The biggest risks I see ahead are twofold: extreme default levels, big enough to draw NAV down 50%; and higher property management expenses, that put a drag on recurring earnings.

These risks are counteracted by 90% equity financing and a 40% discount on tangible book value per share. This provides the company with three protections: defaults have to be catastrophic to put NAV below the current share price; the company can sell property at steep discounts to avoid managing it without putting NAV below the current share price; and the company can increase rates because higher leveraged competitors have to leave the market.

Note: Unless otherwise stated, all information has been obtained from BRMK’s filings with the SEC.

Business description

National hard-money lenders: Hard-money lenders concentrate on short-term loans (one to three years) that carry a high interest and are collateralized by carved-out assets, sometimes with recourse covenants or personal guarantees. These loans are mostly used as bridges until longer-term cheaper financing can be arranged.

High interest equals high default risk: Credit is a commodity, and the credit market is very competitive. That means an informed borrower will tend to find the lowest interest possible for its statistical risk bracket. The fact that BRMK was able to charge 10% rates during 2021, a time when the Federal rate hit 0%, talks about the risk of its loan-book.

Credit score versus asset based lending: HMLs make their living by concentrating on a particular type of borrower that does not qualify for much cheaper bank loans. With lower capital supply, the credit spread on these loans is high. The profitability of an HML is based on the idea that the higher credit spread more than compensates for the higher risk. To further reduce risks, HMLs concentrate on asset collateral and recourse covenants.

Concentration in the center-west: 75% of the company’s loan book is concentrated in Washington, Colorado, Utah and Texas.

Ultra low leverage: BRMK is 90% equity financed, registering only a $100 million note paying 5%, issued in November 2021. This greatly reduces risk, given that a credit loss is not multiplied by leverage across the book, and that interest income loss is not operationally multiplied by interest costs down the income statement.

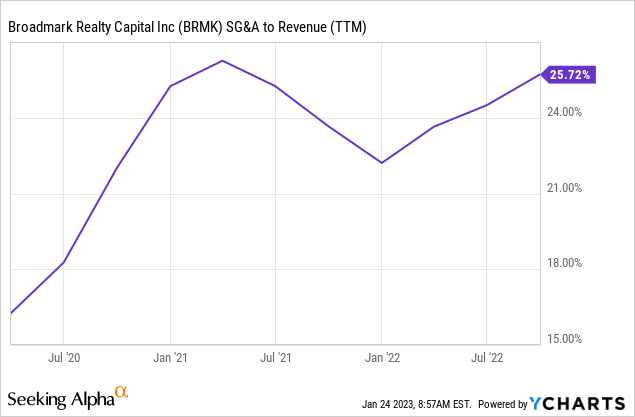

Lean operation: The company’s operational expenses made a small percentage of interest income. Unfortunately, BRMK is adding property management expenses on its foreclosed properties. Property management expenses not run at half the level of G&A expenses at the quarterly level, from being almost negligible one year ago.

Conservativeness: The company did not increase its book significantly during the 2021 boom. This conservativeness is in part generated by REIT taxation, which makes the company distribute 90% of earnings, which makes it difficult to accumulate capital and expand book.

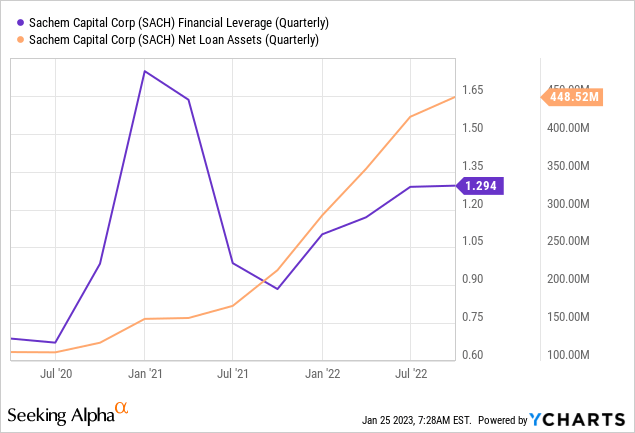

Still, other REITs took cheap leverage in order to expand their books, and BRMK did not. An example of this is Sachem Capital Corp (SACH), another HML, but much more leveraged (1.3 against 0.09 for BRMK) and with an exploding book.

Low insider ownership, no strong shareholder: The company’s managers and directors hold only 3% of the company’s stock. The largest shareholders are ETF groups like Vanguard and BlackRock, with less than 9% participation each (according to the company’s proxy statements for FY22). I generally prefer a company where managers have skin in the game and where there is at least one strong shareholder.

Recent developments

The situation has not been good in general for BRMK, several negative developments have driven the stock’s price down 50%, only to recover some 10% back.

Dividend cut: When I wrote my latest article on BRMK in June 2022, the company was not covering its dividend with cash. A cut was imminent, but the yield seemed interesting even after the cut. The company then decided to cut the dividend in half, from $0.84 to $0.42 yearly (paid monthly).

Resignation of CEO and CFO: The company’s CFO resigned in October, followed by the CEO in November. The resignation of the CEO was communicated on the same date as the 3Q22 results (more on this below). The Interim CEO position is now occupied by the company’s founder and Chairman, who occupied that position since the company went public in 2019 until 2021.

The company granted RSUs to the newly elected CFO and Interim CEO for $750 thousand that will hit SG&A expenses in 4Q22.

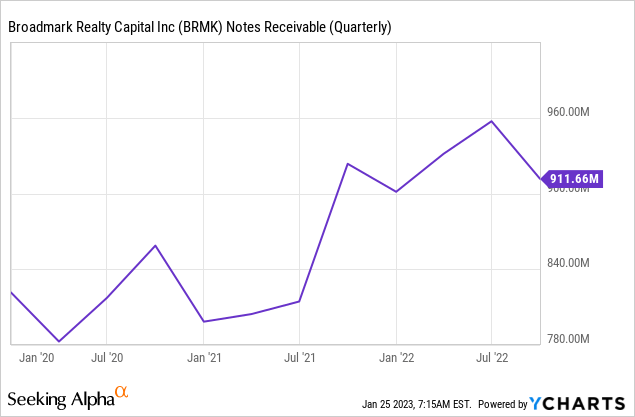

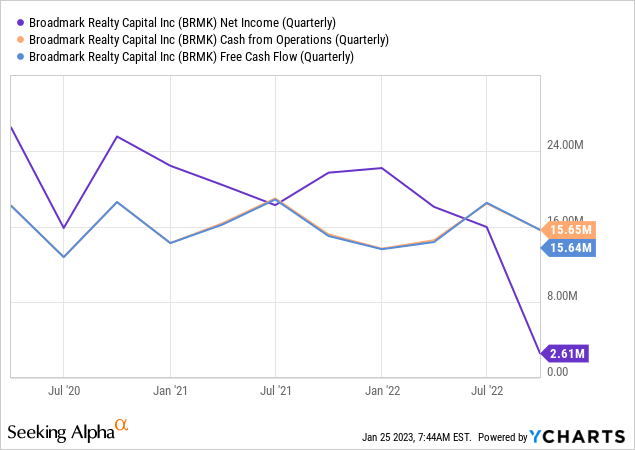

Higher delinquencies: The company’s delinquent loans increased 15% since 2021, representing $115 million as of 3Q22 against $100 million in December 2021. The company reports $286 million in non accruals but that includes committed but not released funds as well.

Higher loan loss provisions: More defaults, but particularly the foreclosure of a hotel property that has become difficult to sale, prompted the company to recognize $13 million in loan loss provision allowances in 3Q22 alone. This represents a huge drag on quarterly earnings.

Property management expenses: BRMK seized property book now stands at $93 million, from $68 million in December 2021. The book would have jumped to $121 million hadn’t been for a financed sale for $28 million of residential condos. The biggest contributor was a senior housing development, carried at $50 million. As a reader accurately pointed, managing properties is much more expensive than managing loans. Quarterly property management expenses, close to non existent one year ago, now run at $1.5 million.

Valuation and risks

With all of these negative developments, plus interest rates that continue rising, plus the company’s risky loan book, how am I bullish on the stock? The answer comes from Howard Marks’ comment that ‘a low-quality asset can constitute a good buy’.

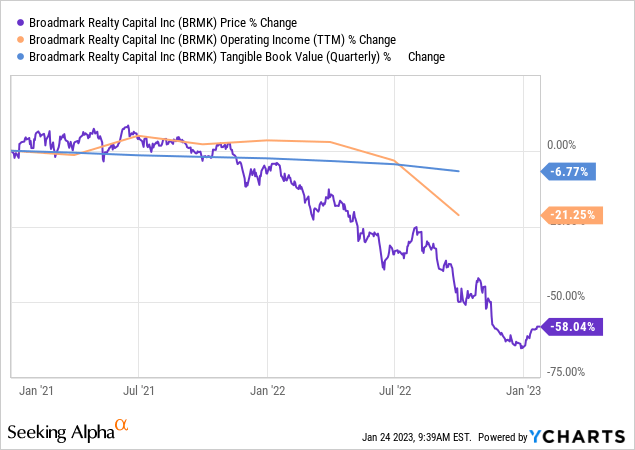

In my opinion, BRMK’s risks are more than discounted on its current price. While tangible book value has fell 7%, and operating income another 21% (this is before loan loss provisions), the stock’s price is today 58% lower than two years ago.

Higher delinquencies: The main risk for BRMK is the danger of posting more delinquencies. This has cascading effects because it increases allowances for loan losses and materialized losses (by selling properties below their recorded value). It also increases managerial expenses, reducing operating income and putting the dividend at risk.

Balance sheet protection: The company currently has $7.27 per share of tangible book value, against a stock price of $4.2. That represents a 43% discount. Because the balance sheet is mostly equity financed, for that discount to materialize, the company needs to post loan losses for an equivalent 43%. That means that almost one in every two loans is completely lost, or that every loan was overpriced by 100%.

The dividend cut is a capitalization strategy: The biggest drag on earnings has been higher loan loss allowances. These are non cash expenses that recognize that an asset’s value (a note receivable) is not as high as it was thought to be. However, because accrual income is reduced through higher allowances, the company has to distribute less dividends. The cash difference is being used to capitalize the company, something that is usually difficult for a REIT.

Recurring cash income protection: When the company posts a loan loss allowance, it is recognizing a past event. This talks more about the company’s previous decisions (and its financial sustainability as considered in the balance sheet) rather than current profitability.

On the other hand, if more loans go into non accrual, the company seizes on property or does not recover the full value of its loans, this affects future income generation. This happens for two reasons: the book is reduced, and therefore its ability to generate income decreases; and expenses (particularly property management) increase.

Smaller loan book: I believe the first risk (smaller book) is counteracted by higher rates. BRMK’s obtained $90 million in interest revenue on a $849 average loan book in FY21. This represents a 10.6% average rate, against a reported average rate of 10.2% for 3Q22. That means the recent rate increase has not been translated to new originations. My belief is that as higher leveraged competitors leave the scene, BRMK will be able to increase its rates without reducing its loan book or increasing credit risk.

Higher property management expenses: On the expense side, the highest risk comes from managing foreclosed properties. But this risk can be eliminated if the company sells those properties quickly. Again, the equity financed balance sheet and the deep share price discount on NAV per share provide a margin on safety on property sales below recorded value.

Higher interest expenses: The company did not have to pay financial expenses on the $100 million in notes (5%) one year ago. These imply $5 million more per year in expenses.

Income considerations: If the current rate is maintained, at 10%, on the same loan book of $900 million, we are thinking of $90 million in yearly interest income, plus another $20 million in origination fees. Against these BRMK will post SG&A expenses of $30 million, and another $6.5 million in interest expenses ($5 million from the notes, $1.5 million from maintenance of a credit facility). This leaves $73.5 million before property management fees, and loan loss allowances.

With a yearly dividend of $55 million and a market cap of $566 million, property management fees should climb to $18 million (from the current $6 million annualized) to affect the cash used to pay the dividend, or to reduce the FCF multiple below 10x. Remember that loan loss allowances affect our calculation of book based valuation, not income based.

Conclusion

BRMK has seen some rough quarters, and more pain could wait ahead. However, I believe current valuations imply a catastrophic event in terms of loan losses. Approaching the company’s valuation from an income perspective as well as from a book perspective renders an important margin of safety.

From comments in previous posts, my understanding is that the bear case is based on these catastrophic scenarios, where the book is worth very little and there are massive defaults.

Be the first to comment