John Phillips

Investment thesis

Adyen (OTCPK:ADYEY) is well positioned in the payments industry given its focus on online and e-commerce payments. I am of the view that this will enable it to achieve sustained growth and expansion in margins as the payments industry continues to enjoy secular tailwinds. Adyen continues to see strong commercial traction even during these challenging times, which demonstrates the strong value add Adyen brings to global businesses. The company is investing in the future of its business by accelerating its pace of hiring when others are slowing down hiring or even cutting headcount.

What does Adyen do?

For those who are looking into Adyen as a company for the first time, Adyen operates a global payments platform. It integrates the full payments stack, which includes gateway, risk management, processing, issuing, acquiring and settlement services.

Adyen connects a wide range of global and local merchants across verticals to credit card schemes, including Visa (V) and Mastercard (MA). It offers a common back-end infrastructure for authorizing payments across merchants’ sales channels and feature rich APIs. At the end of the day, Adyen provides a high level of reliability, performance, and data insights to its customers as its key value proposition.

Adyen value chain (Adyen 1H22)

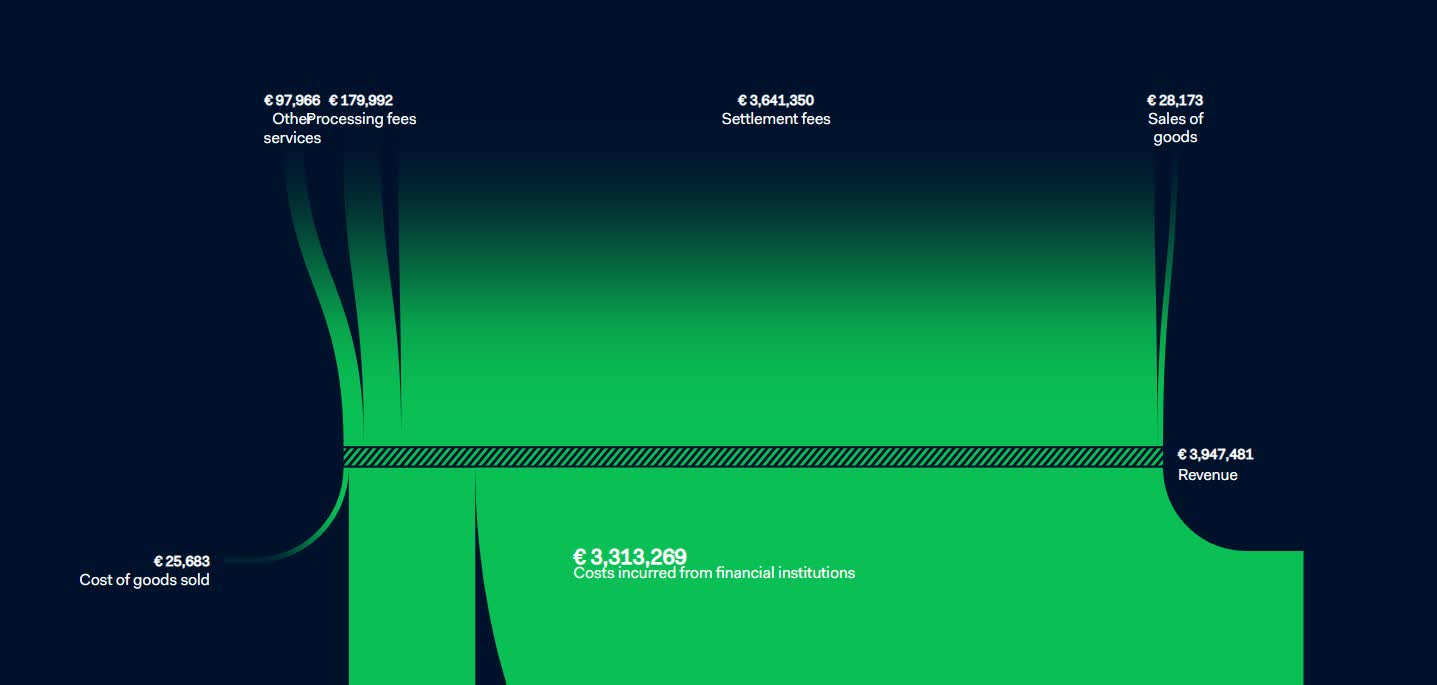

Revenue model

A large part of Adyen’s revenues comes from settlement fees as well as processing fees. Settlement fees, making up the largest portion of revenues, is earned as a percentage of transaction value and when Adyen offers acquiring services. Processing fees are earned when merchants use Adyen’s platforms and is charged based on a fixed fee per transaction. By providing payment processing services, Adyen earns processing and settlement fees.

Adyen revenue mix (Adyen IR)

Product innovation

Released first Adyen designed terminals, NYC1 which is meant for businesses that have made investments into the hardware and want to add payments to their set up, while AMS1 is for businesses that want to be able to access all operational apps via one device.

Roll out Tap to Pay on iPhone in collaboration with Apple, enabling businesses to accept contactless payments on an iPhone, without needing to purchase additional hardware. This offering is made directly to retailers like Nike (NKE).

One of the product innovations that Adyen brought in 2022 was the expansion of its financial product suit for platforms. This expanded to card issuing, business financing and bank account. Adyen is well positioned to capitalize on the significant opportunity in financial services. Adyen is able to provide an end-to-end solution and highly integrated solution for financial services platforms. For example, Grab chose Adyen as its partner to deliver GrabPay.

Adyen’s commercial developments

I think that Adyen continues to show strong momentum in business partnerships across markets and these commercial developments indicate the competitive advantage that Adyen brings to its customers as a global financial technology platform.

Firstly, Adyen recently announced that Instacart selected it as an additional payments processing partner. Instacart is a leading grocery technology company in North America. Instacart had this to say about how they chose Adyen as a payments partner, with their key considerations being scalability and seamless customer experience:

We’re pleased to welcome Adyen as an additional payments partner that will enable us to continue to scale and ensure our customers have a seamless experience all the way through checkout.

Secondly, in December of 2022, Adyen introduced unified commerce to Japan as it launched its in-person POS payments solutions powered by its platform. I think that the Japanese market looks attractive for Adyen because of the fact that it is one of the few platforms in Japan that can centrally merge payments data from stores and e-commerce sites and the only one that do it at a global scale. With this new launch, it enables merchants in Japan to tap into the same Adyen tools that the largest and global merchants use to optimize authorization rates, block fraud and provide a seamless cross-channel experience.

Thirdly, Adyen looks to be expanding its partnerships from the Europe region to the United States. McDonald’s (MCD) was one such global firm that looked to expand its mobile app partnership to the United States after having worked with Adyen since early 2020. To quote McDonald’s United States CIO’s comment on Adyen:

As consumer demand evolves, Adyen has responded to our needs in a rapidly changing market. Adyen has handled mobile volumes during peak events, such as promotions and rush times. Additionally, they helped improve the success rate for customers registering their preferred payment types to their digital profile and reduced card declines during order placement by using Real-time Account Updater technology.

Lastly, Fast Retailing’s (OTCPK:FRCOY) UNIQLO chose Adyen to provide omnichannel payments services to the company, to power payments for the brand’s in-store and online checkout in multiple markets. This allows for UNIQLO to have better consolidation and reconciliation of payments information across multiple channels.

Adyen first half 2022 results

In the recent first half of 2022 results, Adyen grew TPV by 60% year on year to €346bn. This was 5% ahead of market consensus of €328bn. As a result, net revenues increased by 37% year on year to €609m on a constant currency basis. This compares to the 43% and 53% year on year growth on a constant currency basis in the second half of 2021 and first half of 2021, respectively.

That said, there was about an 8% miss in EBITDA, which came in at €357m, with EBITDA margins of 58.6%. This was due to the accelerated pace of hiring as well as event and travel costs returning.

With travel volumes increasing in the first half of 2022, this impacted Adyen’s volume mix. As a result of the return and recovering of travel globally, this resulted in full stack volumes falling to 78% in the first half of 2022, compared to 83% in the prior year. This was due to the fact that Adyen does not typically offering acquiring to airlines.

Growth in North America for the quarter was at 52% and represented 25% of Adyen’s revenues in the first half of 2022, up from the 18% of revenues the region contributed 2 years ago.

There was an acceleration of headcount increase in the first half of 2022, with an increase of 395 in the first half of 2022, compared to the increase of 226 in the second half of 2021. As a percentage of sales, employee costs made up 26% of sales in the first half of 2022.

While Adyen did not provide near-term guidance, the management continued to reiterate its medium-term mid 20s to low 30s net revenue growth goal and longer-term EBITDA margin target of more than 65%.

Investing in the future of Adyen

As we see many of Adyen’s technology peers reduce headcount during this uncertain period, Adyen CEO Pieter recently announced in a letter to employees that the company remains in investment mode today and will continue to hire at the same cadence in 2023.

I think that given that the competition for talent has somewhat eased in recent times, this gives Adyen an excellent opportunity to add to its headcount to invest towards its long-term goals.

Management did highlight that the reason for continued investment was necessary as a result of the fast-changing payments industry as well as the financial product suite in its infancy stage. As a result, the investments to be made for new hires will go towards its long-term goals. The new hires will be mainly to meet Adyen’s long-term technical and commercial needs. The management also expects that in 2024, these investments made today will bring Adyen to the next maturity level, and that’s when they will cool the hiring pace and allow an expansion of the operating leverage in the business model.

This increase in headcount does imply near-term headwinds to operating leverage and margins. As the management only expects to slow down the rate of hiring in 2024, this implies that there could be a higher probability that the market’s estimate of EBITDA for 2023 may be too high.

Valuation

My target price for Adyen is $18.63, implying 29% upside from current levels. This is derived from a blend of DCF valuation and relative valuation based on EV/EBITDA. Adyen has traded at a 1-year forward EV/EBITDA multiple of 70x since 2018 and has enjoyed a premium multiple over peers. I assume a 45x forward multiple for Adyen given where peers are trading at today. On the other hand, for the DCF model, I assume a discount rate of 9% to be used for Adyen’s valuation. I think that this presents an opportunity to invest in a leading payments platform positioned for long-term growth.

Risks

Macroeconomic downturn

As Adyen’s business depends on transaction volumes, given that consumer spending falls during a macroeconomic downturn, there are risks that a worse than expected downturn could lead to lower transaction volumes.

Rapidly changing payments landscape

As a result of the payments landscape seeing rapid changes in the past few years, as consumers pivot towards mobile and e-commerce, Adyen needs to be able to keep up with the times and innovate.

Credit risk

Although the risk is small, Adyen is exposed to the credit risk of the merchant customers if they fail. This is particularly relevant in the current macroeconomic environment when the economy is weak and deteriorating.

Regulatory risks

As a result of regulation changes in the payments industry, companies like Adyen needs to keep up with these changes and are highly exposed to regulatory risks. Some regulations include the EU interchange cap that came into effect in 2015, and the EU’s Second Payment Services Directive (“PSD2”)

Conclusion

I think that Adyen looks like a key beneficiary as more people spend online and as e-commerce adoption increases globally. The company provides a high level of performance, reliability and data insights to customers, resulting in a strong value proposition. This continues to bring new partnerships to Adyen as more of its existing customers expand current partnerships and as Adyen attracts new customers into its ecosystem. The company remains to invest in key strategic areas and focuses on bringing in the necessary talent needed to bring the business to the next level. My target price for Adyen is $18.63, implying 29% upside from current levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment