Solskin

A hedge knight must hold tight to his pride. Without it, he was no more than a sellsword” ― George R.R. Martin

In today’s article, we’re returning to a small-cap developmental firm named Equillium, Inc. (NASDAQ:EQ) for the first time since our initial article on it back in May 2021.

We concluded that research piece in the following way:

Equillium is an intriguing little developmental company whose platform appears to have some potential. The company is well funded and well-thought of by the analyst community. The problem is that Equillium is years away from any potential commercialization. In addition, there are no options against the equity available at this time. This rules out a covered call strategy, which is the only way I would take a small ‘watch item’ position in EQ right now. However, this is a name we will keep an eye on and circle back in the years ahead as its pipeline advances.“

We’re now a year and a half away from that conclusion and Equillium posted some encouraging interim results from a mid-stage trial late in September and also made a small acquisition during last month. Therefore, it seems a good time to circle back on this small cap concern. An updated analysis follows below.

Seeking Alpha

Company Presentation:

August Company Overview

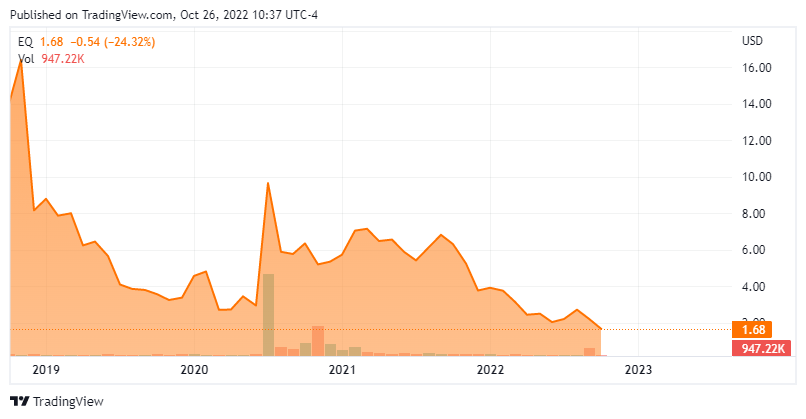

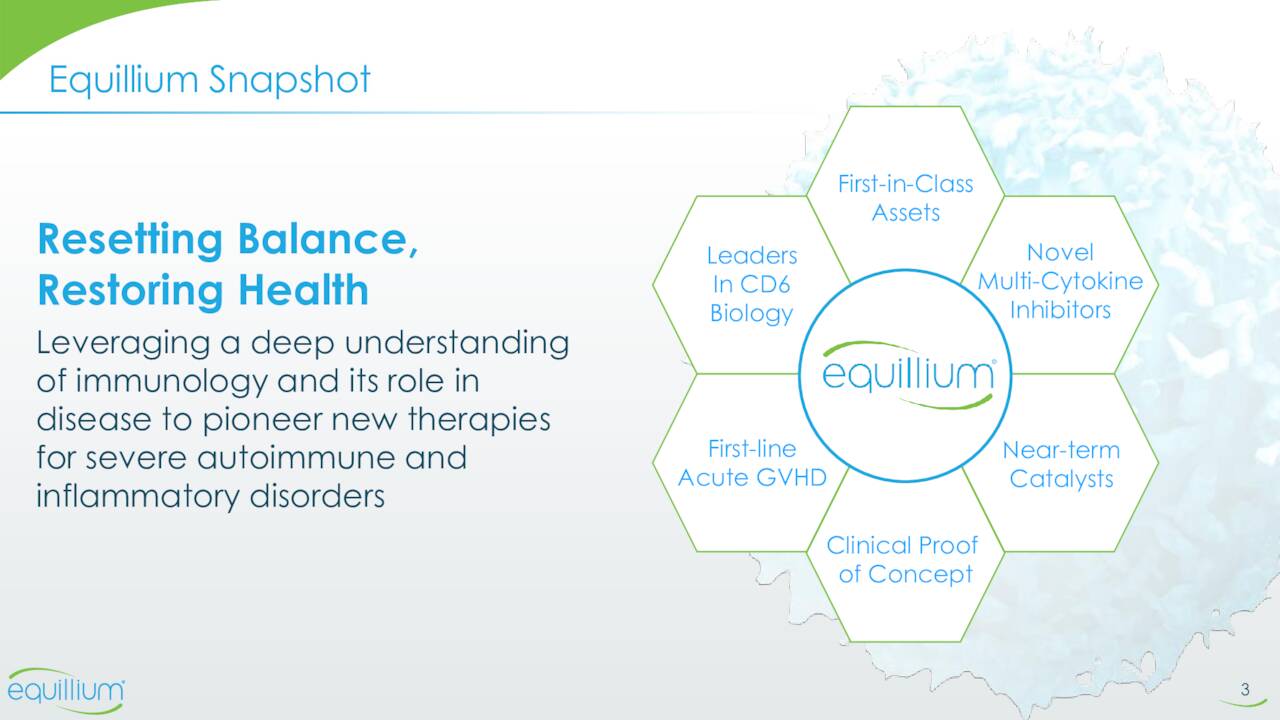

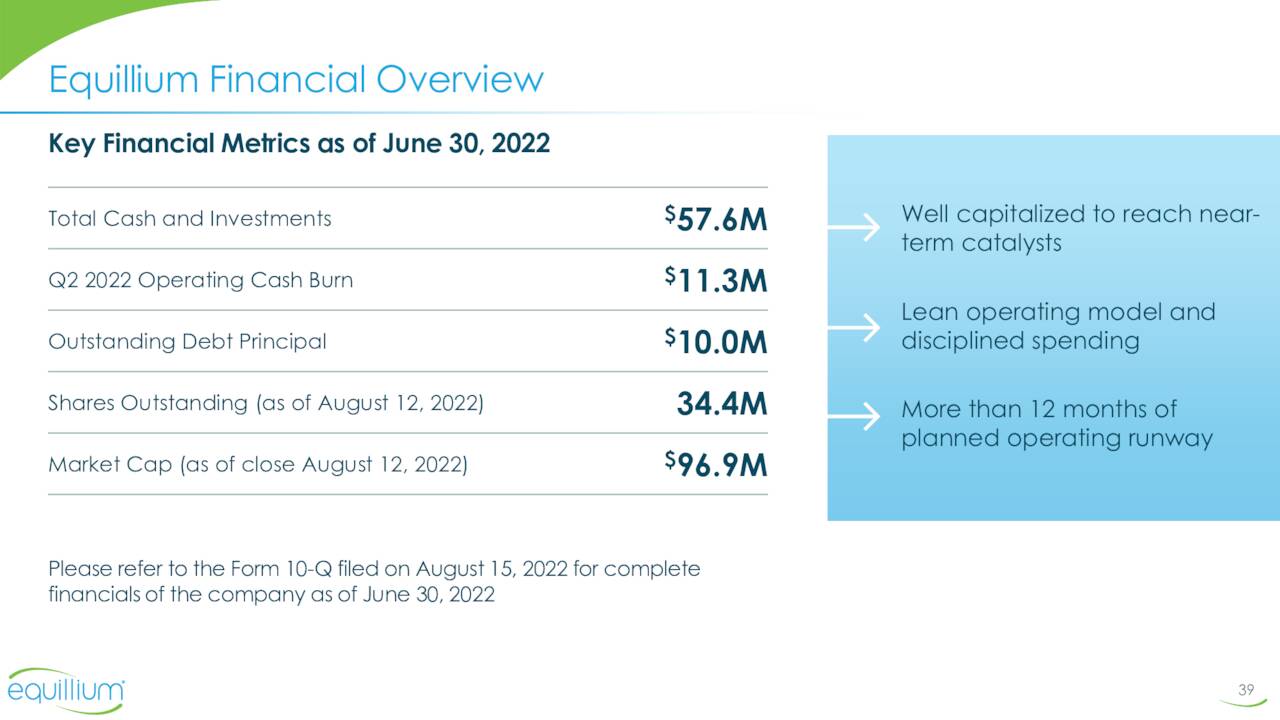

Equillium, Inc. is a San Diego headquartered clinical stage biotech company. The company is leveraging its understanding of immunobiology to develop novel therapeutics to treat severe autoimmune and inflammatory disorders with high unmet medical need. The shares currently trade just north of $1.50 a share and sports an approximate market capitalization of $60 million.

August Company Presentation

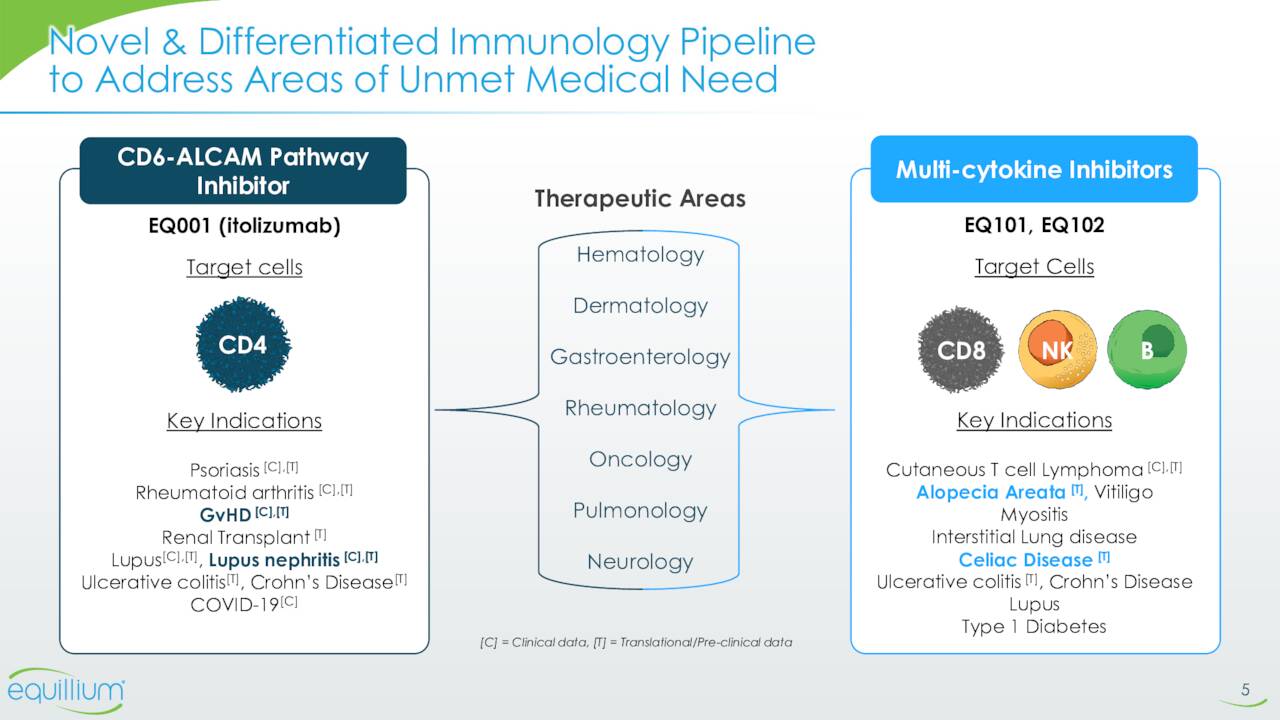

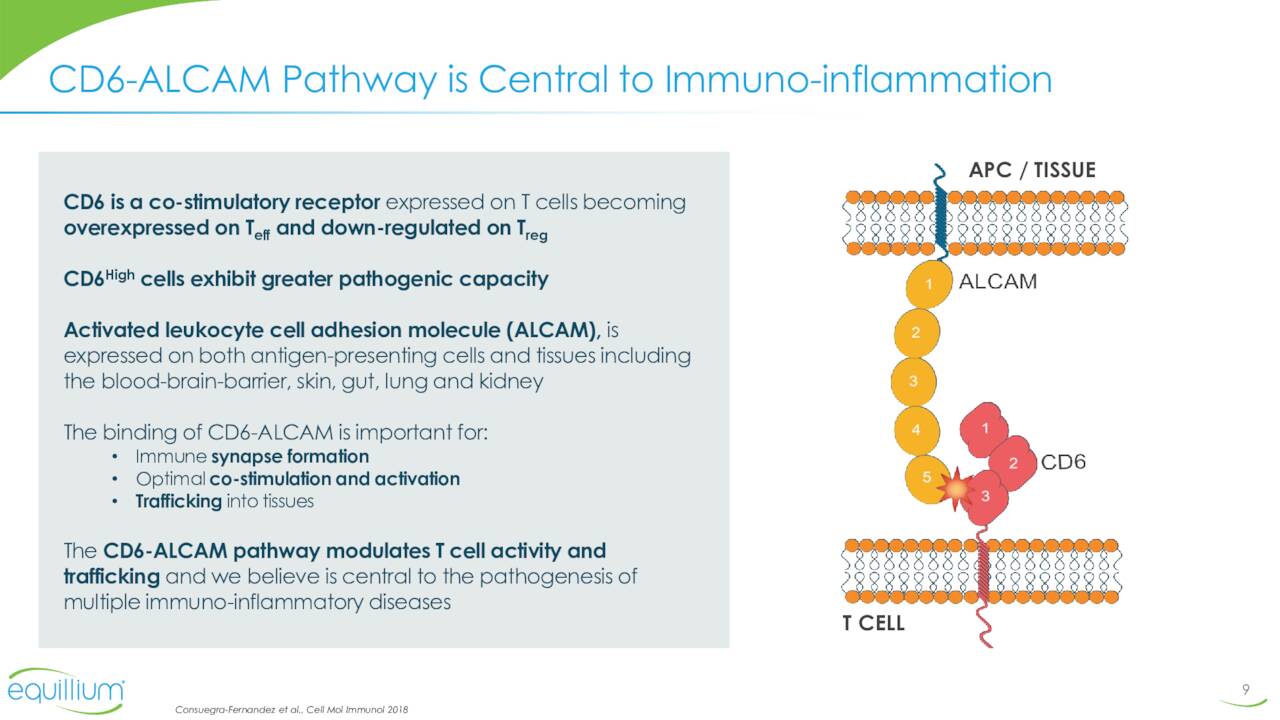

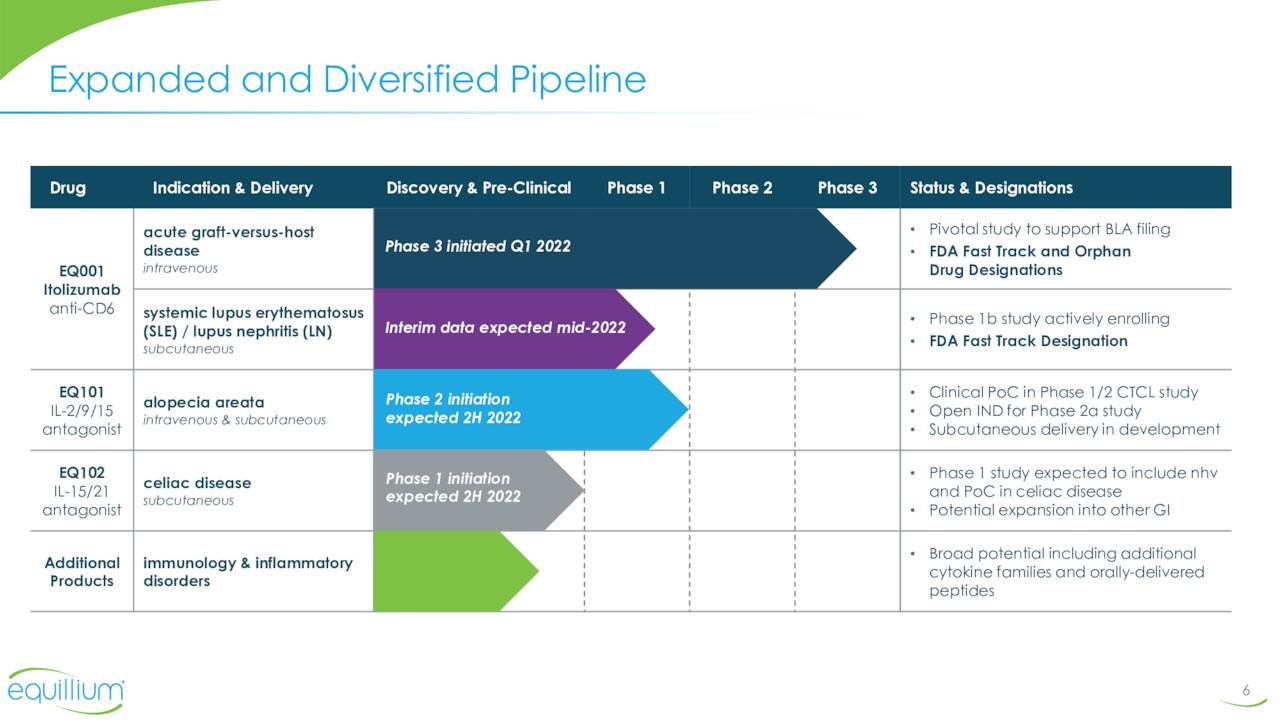

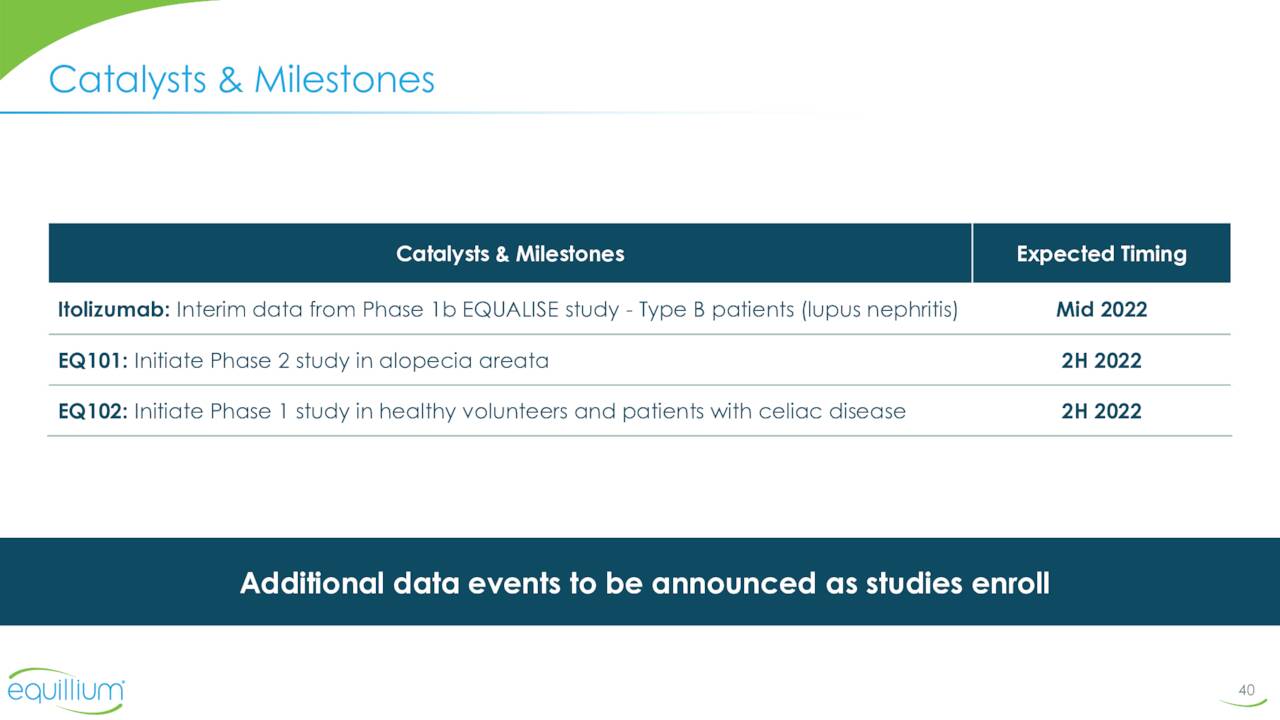

The company’s lead pipeline asset is called Itolizumab. This compound is a first-in-class monoclonal antibody that targets the CD6-ALCAM signaling pathway. This pathway plays a central role in modulating the activity and trafficking of T cells that drive a number of immuno-inflammatory diseases. Itolizumab is currently being evaluated in a Phase 3 trial for patients with acute graft-versus-host disease (aGVHD) as well as in a Phase 1b study ‘EQUALISE’ for patients with lupus/lupus nephritis. As of the close of the second quarter, patients in this study ‘EQUATOR’ were being enrolled. Investors should get more data around the enrollment status of this key trial when the company reports third quarter results around mid-November.

August Company Presentation

As previously mentioned, the interim results from the Type B portion EQUALISE were released in late September. This triggered a rally in the stock and also saw several buy reiterations from analyst firms (see next section).

August Company Presentation

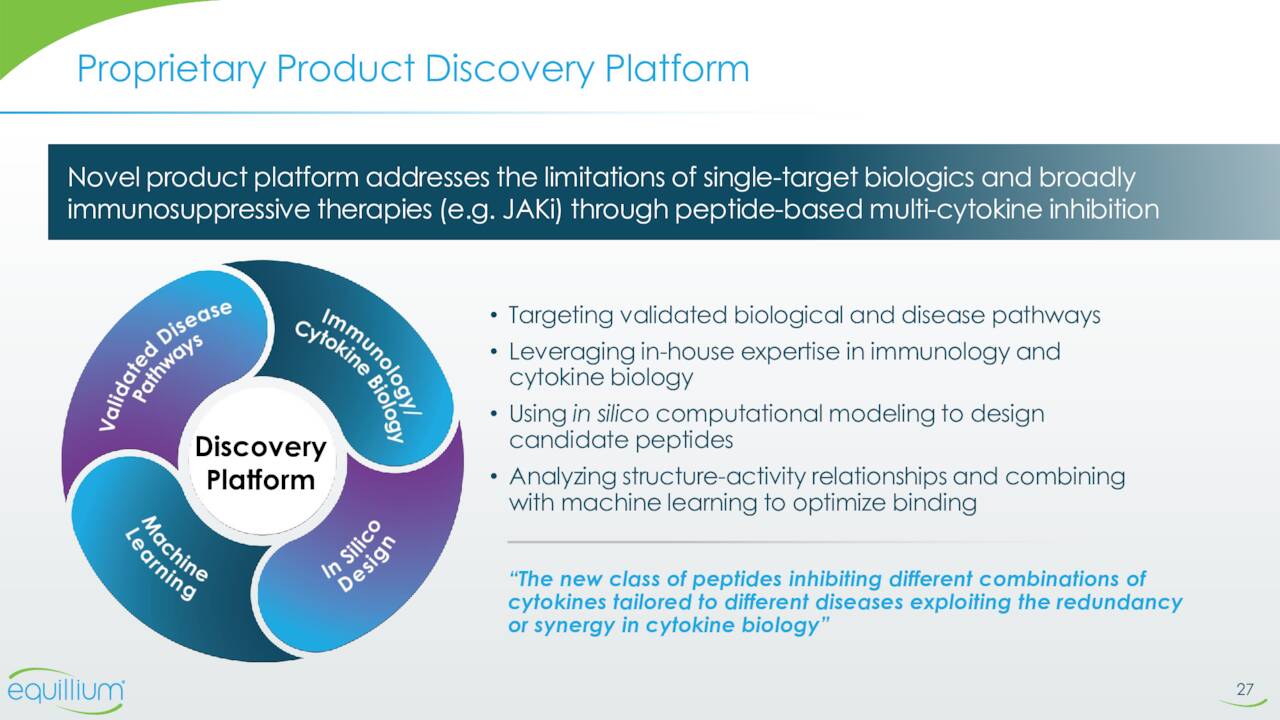

The main part of the rest of Equillium’s pipeline consists of EQ101 and EQ101. Both compounds were developed off the company’s multi-cytokine platform. This platform creates composite peptides that selectively block key cytokines at the shared receptor level targeting pathogenic cytokine redundancies and synergies while preserving non-pathogenic signaling. This thesis is that this approach will avoid the broad immuno-suppression and off-target safety liabilities that may be associated with other therapeutic classes, such as JAK inhibitors.

August Company Presentation

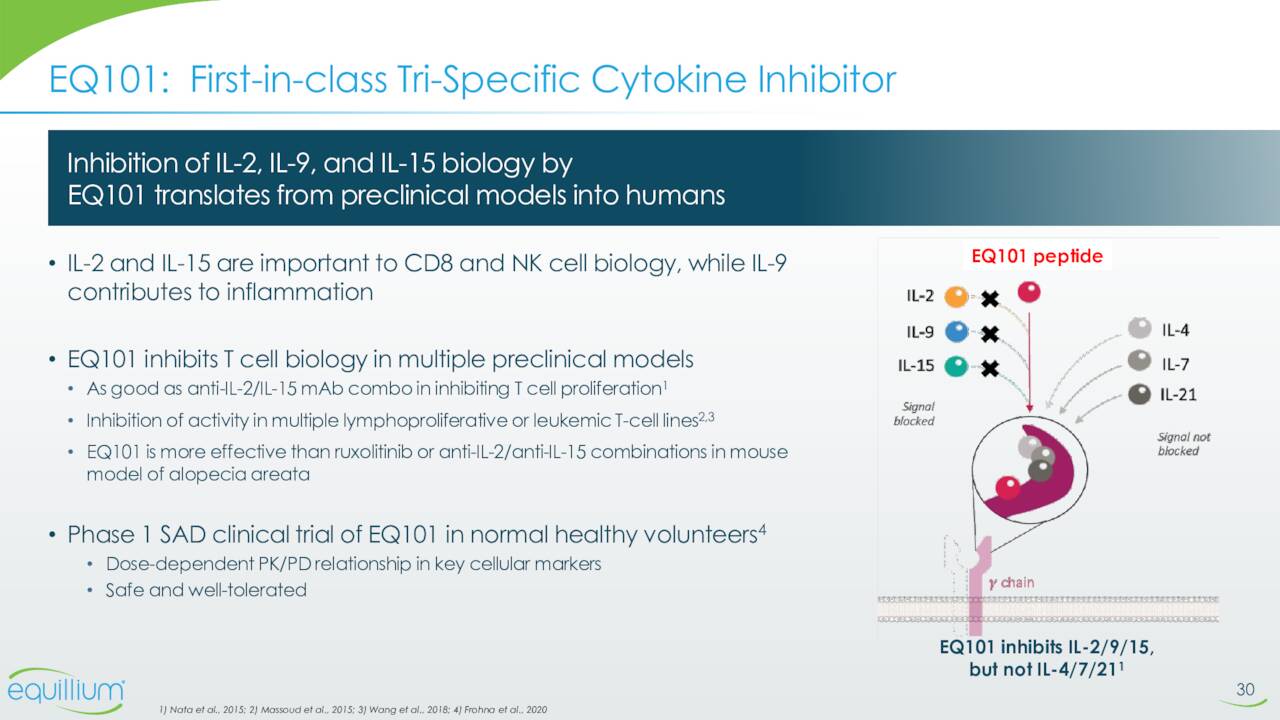

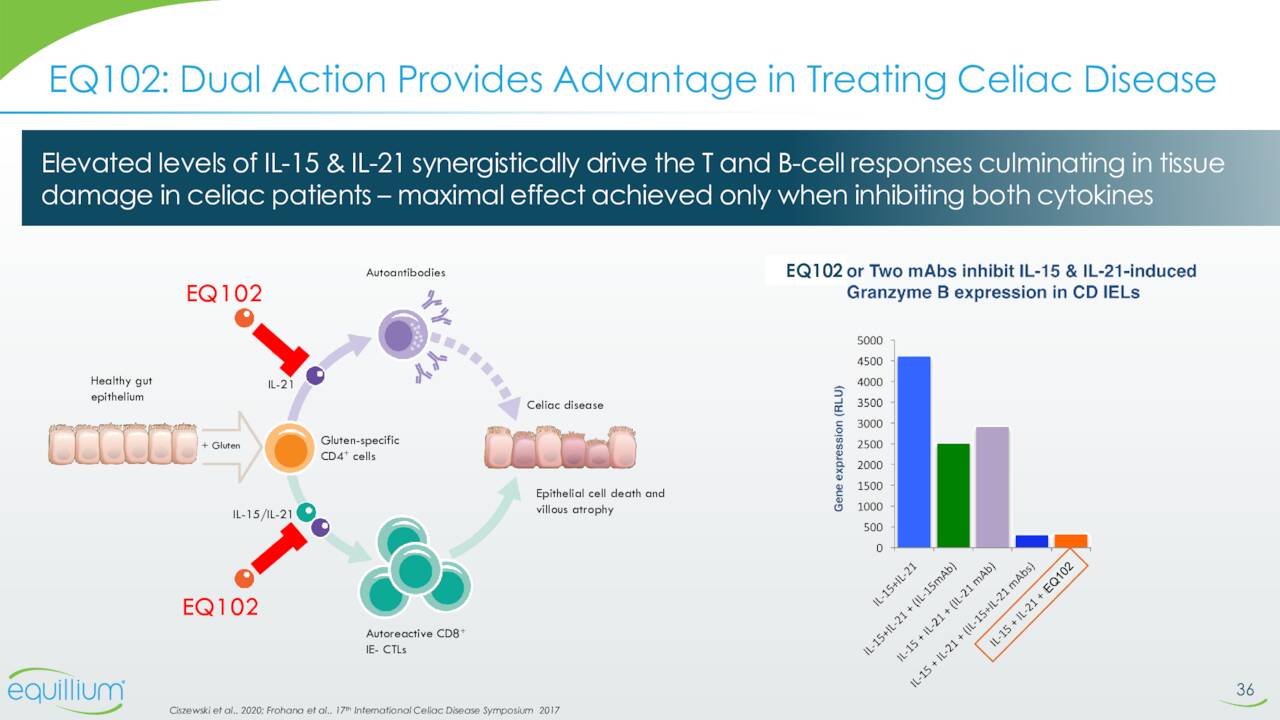

EQ101 is a first-in-class, tri-specific inhibitor of IL-2, IL-9 and IL-15. It’s being reading for a Phase 2 study to evaluate it to treat alopecia areata. This trial should begin enrollment before the end of this year. Phase 1 study in normal healthy volunteers to evaluate EQ102 in treating celiac disease patients should initiate before yearend as well. EQ102 is a bi-specific cytokine inhibitor that selectively targets IL-15 and IL-21.

August Company Presentation

In early September, the company announced that it had reached a definitive deal to acquire Metacrine (MTCR) in an all-stock transaction. This acquisition brings into Equillium’s pipeline a compound called MET642. This is an orally delivered FXR agonist that Metacrine’s management claims is the potentially first-in-class, non-immunosuppressive treatment for inflammatory bowel disease. MET642 has completed a Phase I clinical trial for the treatment of ulcerative colitis. Metacrine’s market cap at the time of the announcement was less than $25 million.

August Company Presentation

Analyst Commentary & Balance Sheet:

Over the past month, Stifel Nicolaus, SVB Securities ($12 price target), H.C. Wainwright ($20 price target) have reissued Buy ratings on the stock. Here’s the commentary from the analyst at SVB Securities.

We continue to see the potential for itolizumab as an emerging immunomodulatory treatment across multiple autoimmune diseases, including LN, and look forward to topline results from the full Type B portion of the trial expected in mid-2023“

Approximately seven percent of the outstanding shares are currently held short. The company’s CFO has sold just under $60,000 in aggregate via three transactions so far this year. That’s the only insider activity in Equillium, Inc. in 2022. The company ended the second quarter of 2022 with just over $55 million in cash and marketable securities on its balance sheet against approximately $10 million in total debt obligations.

August Company Presentation

The company burned through just over $10 million in cash during the second quarter. The acquisition of Metacrine last month brought $33 million worth of cash with it, extending Equillium’s cash runway into 2024.

Verdict:

Equillium seems to have evolved to an intriguing “sum of the parts” story even as it remains a high risk/high reward clinical-stage concern. The stock sells for basically the net cash on its balance sheet after the recent acquisition of Metacrine is integrated.

August Company Presentation

For that – an investor gets several intriguing drug candidates in early to mid-stage development. Once enrollment status is updated on the company’s next earnings call around EQUATOR, a better potential timeline for Itolizumab potential approval for aGVHD should be able to be put together. The company also should have some trial readouts in 2023 and currently enjoys solid support in the analyst firm community. Given all this, EQ seems worthy of being promoted to “watch item” status and merits a small allocation within a well-diversified biotech portfolio pending further developments.

Two times in life you do not waste time arguing with someone: when you are wrong, and when you are right.”― Liz Faublas

Be the first to comment