jetcityimage

Following up with my recent article on Ollie’s Bargain Outlet Holdings (NASDAQ:OLLI), the company recently announced third quarter results. As such, I dove into the results to see how OLLI performed.

OLLI is a chain of discount retail stores with 463 locations across 29 states in the United States. OLLI sources its products from different manufacturers and wholesalers, which it negotiates at discounted prices. The company is then able to offer these products to its customers at attractive discounts.

During the TTM, OLLI generated revenues and net profits of $1.8 billion and $94 million, respectively. OLLI market cap is currently at $2.9 billion, with a YTD decrease of approx. 10%. The company had weak results during the previous two quarters, with margins and cash flows being pressured. On a positive note, management has been deploying excess cash through increases in store count and share buybacks.

The third quarter results had a couple of good notes, nonetheless, the combination of the first 3 quarters was disappointing. The disappointing outcome keeps me from rating OLLI as a buy, the company has a long runway ahead, however, financials need to normalize back to 2021 levels in order for the company to have a brighter future. Let’s get to the financials.

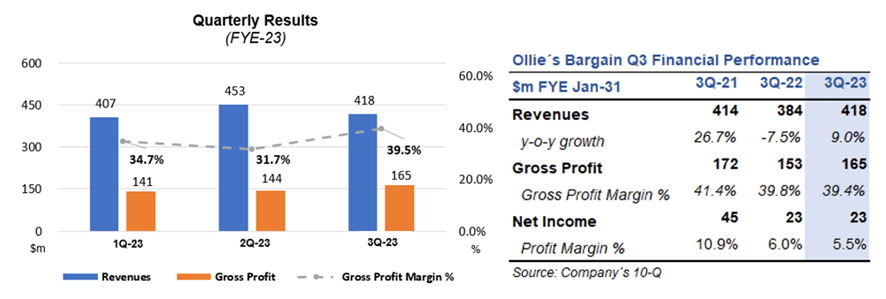

Third Quarter Financials

During the third quarter of fiscal year 2023, OLLI saw an increase in revenues of 9% from $384 million during the same quarter last year to $418 million. The first positive news was that during the third quarter, the company saw its gross margin increase to 39.5%. This is a nice improvement, as during the previous quarter OLLI had delivered one of its worst quarters regarding gross profit margin at 31.7% (see graph below).

Quarter 3 Highlights (Company´s 10-Q)

Despite a better gross profit margin during the quarter, OLLI net income remained flat year-on-year at $23 million as operating expenses increased. Particularly SG&A which saw an $11 million increase to $125 million compared to the same period last year at $114 million.

Lastly, OLLI opened 15 new stores during the quarter and albeit weak, the company finally saw an increase in comparable same-store sales of 1.9%. This is another positive note, as comparable same-store sales during the third quarter of the previous year had plummeted by 15.5%.

Even though the results are not stellar, it is important to note that OLLI was finally able to achieve a gross margin which is very close to the management’s target of 40%. This is important to track as it significantly impacts the net income of the company. It seems like inflation and supply chain pressures have been somewhat depleted or fixed by management, which could positively influence future results. Further to this, same-store sales finally bounced back to positive growth, this will enhance OLLI topline as the company keeps increasing store count at the tune of 45 stores per year, meaning there are two engines driving revenues higher.

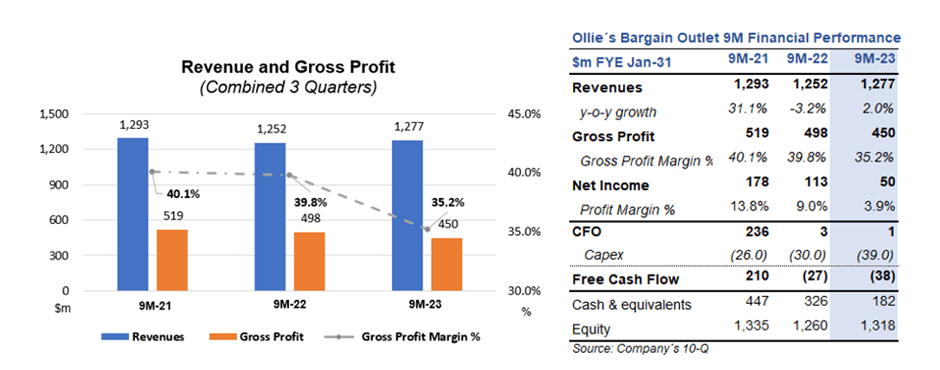

First 3 Quarters Financials

During the first 3 quarters, OLLI revenues slightly increased by 2% as a result of higher non-comparable store sales increase. The company was not able to achieve its gross profit goal of 40%, with a gross profit margin for the 3 quarters of 35.2%. Results were impacted by increased costs related to its supply chain. It is important to note here that the company has had trouble during the previous quarters with increased supply chain costs. Nonetheless, Mr. Swygert, the CEO of OLLI, did mention that the company is seeing some easing in the supply chain costs.

3 Quarters Financial Highlights (Company´s 10-Q)

Operating expenses also saw higher SG&A expenses, which increased to $360 million compared to $329 million during the previous period. This increase was mainly driven by the higher number of stores the company is managing. SG&A as a percentage of sales increased to 28.2% compared to 26.2% during the same period last year. Here we see another item in the income statement which the company is trying to improve through tight cost controls, however, management has not been able to achieve the desired results.

The lower gross profit margin combined with higher operating expenses impacted the net profit for the year, which decreased to $50 million compared to $113 million during the first 3 quarters of the preceding year.

OLLI used a portion of its cash in hand in order to pay for capital expenditures as the company made investments in its York, PA distribution center, which will give it the capacity to distribute an additional 50 stores upon completion. Further to this, management used $30 million to repurchase 602,805 shares of its common stock. As of October 29, 2022, OLLI still has $150 million remaining under its share repurchase authorization.

Despite the use of cash, OLLI remains with a strong liquidity position of $275 million, consisting of: $182 million in cash and cash equivalents and $93 million available under its revolving credit facility.

Looking at the bigger picture, results were disappointing, nonetheless, OLLI remains profitable and with substantial liquidity. We can expect the gross profit margin target of 40% to be missed for FY23, however, it seems like the worst has passed with supply chain costs and inflation easing. Management has signaled tighter cost controls, which combined with lower supply chain costs could produce the necessary costs easing for OLLI to return to higher profitability and extensive free cash flows.

Risks

Competition: OLLI operates in a highly competitive environment, as such the company faces competition from other discount retailers, which could potentially impact their sales and profitability.

Supply chain disruptions: OLLI has experienced disruptions in its supply chain for many months now. This has impacted inventory levels, which has substantially depressed cash flows from operations. Management will need to find ways to implement contingency plans in order to make sure this does not become a new normal.

Inflation: Although OLLI has historically benefited from tough economic environments, inflation has significantly impacted OLLI margins. Management needs to be aware and fast to respond to inflation threats as profit margins can be significantly impacted by higher cost of goods sold.

In Conclusion

The company has failed to deliver the desired results during the first 3 quarters of the year, despite the increase of 9% in revenues, better gross margin and rebound to positive growth in comparable same-store sales during the third quarter, the bigger picture is still disappointing. Management needs to bring financials back in line with their margins goals and until that happens OLLI will keep delivering bitter results. However, it is not all grim, OLLI did deliver a few positive notes, the company remains with a strong balance sheet, management is investing in the company’s distribution centers and store count keeps increasing (Store count close to 500 now). The next few quarters will be key to understanding if FYE23 was a bumpy year or if this is the new normal. As such, I remain with my view for OLLI as a hold.

Be the first to comment