Sundry Photography

The market has recently been rewarding former high-growth companies that have reset their expectations much lower once they jump over these low bars. Okta (NASDAQ:OKTA) looks like great near-term opportunity if this trend continues.

Company Profile

OKTA is a software company that allows clients to authenticate and manager user identifications for apps and services across multiple devices. Their offering is compatible with public clouds, on-premises infrastructures, and hybrid clouds. OKTA uses a software-as-a-service (SaaS) business model where it primarily generates revenue through the sale of multi-year subscriptions to its offerings.

The company sell two primarily solutions. The Workforce Identity Cloud is used by customers to secure their workforce and to be able to create secure solutions to collaborate with partner networks. The offering has multiple modules, which are priced from $2 per month per user for SSO single sign-on up to $11 per month per user for identity governance with unlimited flows. It also has an advanced sever access solution for $15 per server per month. Its Workforce Identity Cloud offerings and pricing can be found here.

OKTA’s Customer Identity Cloud, meanwhile, is used by companies to provide secure experiences for their customers or end users. The firm offers 3 plans, including an Enterprise Offering, B2C Plan, and a B2B. This offering comes from OKTA’s acquisition of Auth0, which it acquired for $6.5 billion in May of 2021. Pricing and plan detail can be found here.

The acquisition of Auth0 was done to help OKTA become a one-stop shop in the identification security market. Talking to TechCrunch in November, CEO Todd McKinnon said:

“We bought them to change, and we bought them because we needed change to win this customer identity market. Our strategy is that we have to win both the workforce market and the customer identity market. And the only way we’re going to turn identity into one of these most important platforms for every company is we have to [own] both use cases.”

Opportunities

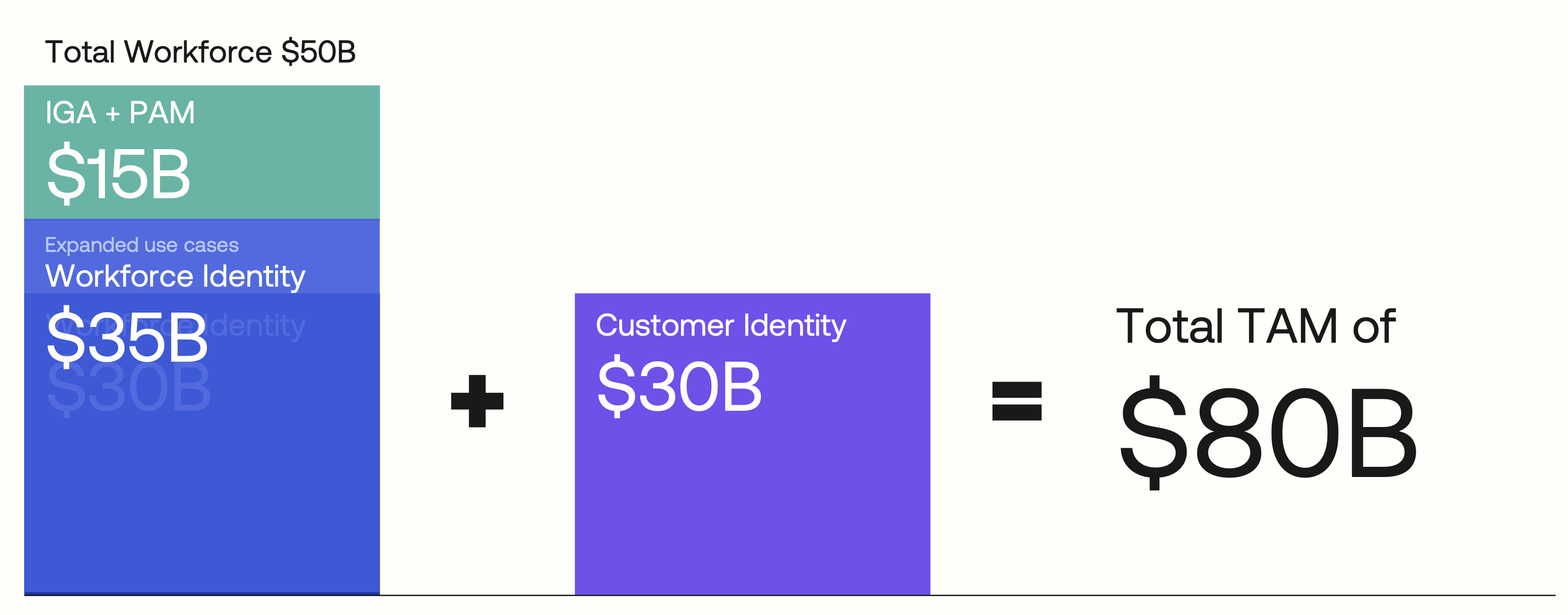

Cybersecurity and ways for companies to protect their data and their customers’ data is one of the most important issues facing enterprises big and small. Making sure a user is who they claim to be is one step in this process, and the market that OKTA is attacking. Identity is a large market, which OKTA puts at a TAM of $80 billion – $50 billion for workforce identity solutions and $30 billion for customer facing identity solutions.

Company Presentation

Meanwhile, the secular trends towards the continued movement to the cloud, more cloud-based apps, and more infrastructure going to the cloud, as well as remote work, all play into companies needing to know who has access to their networks. It’s a growing market and the proliferation of more devices and cloud-based apps only fuels the industry’s growth. Gartner has predicted that cloud-native platforms will serve as the foundation for more than 95% of new digital initiatives, up from less than 40% in 2021.

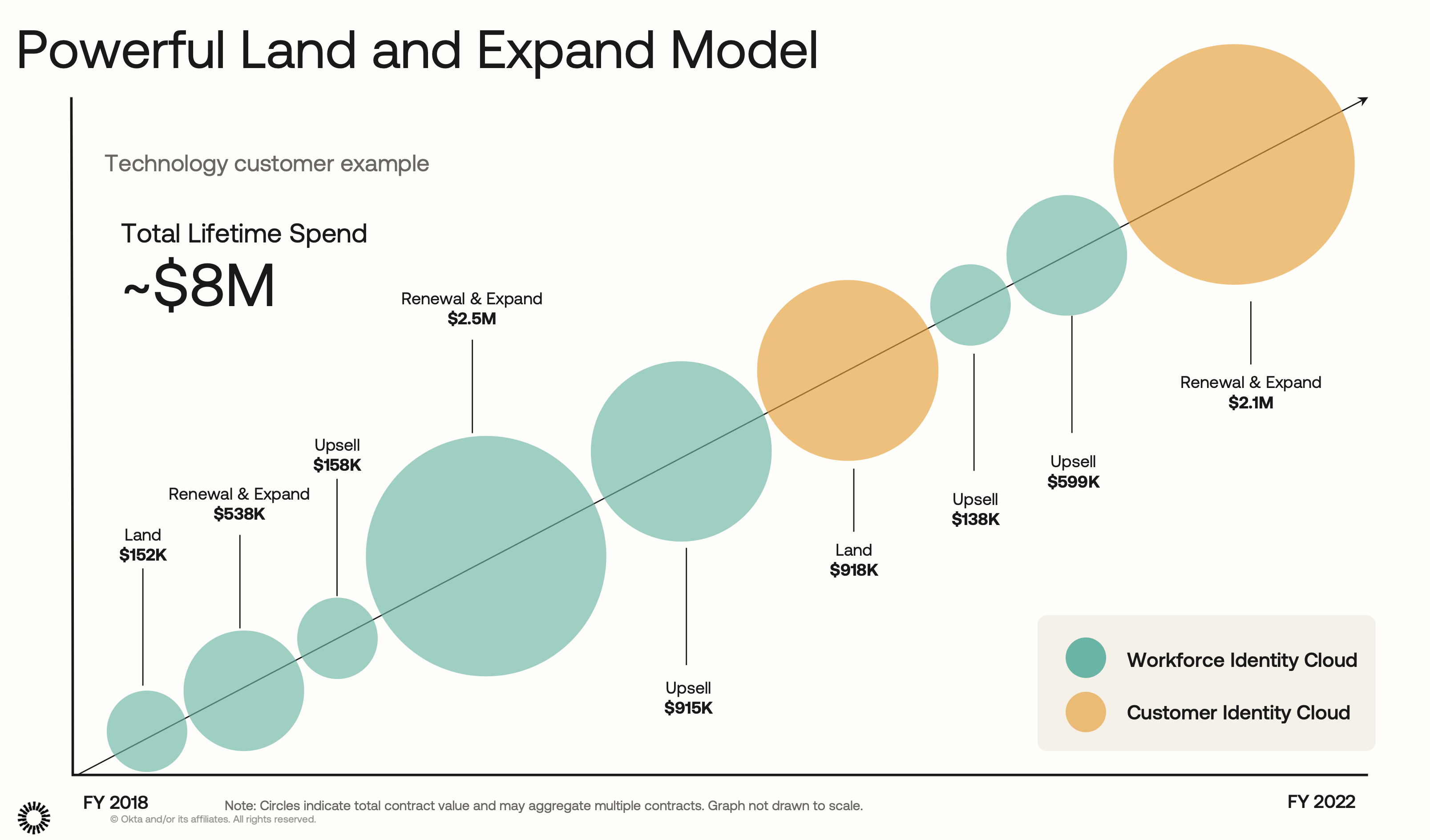

With the acquisition of Ath0, OKTA still has a lot of cross-sell opportunities. This hasn’t gone as smoothly as hoped given integration issues and attrition of Auth0 salesforce reps. However, the company has done a good job upselling new modules in the past and the ability to sell both workforce and customer identity solutions together should be an opportunity.

Company Presentation

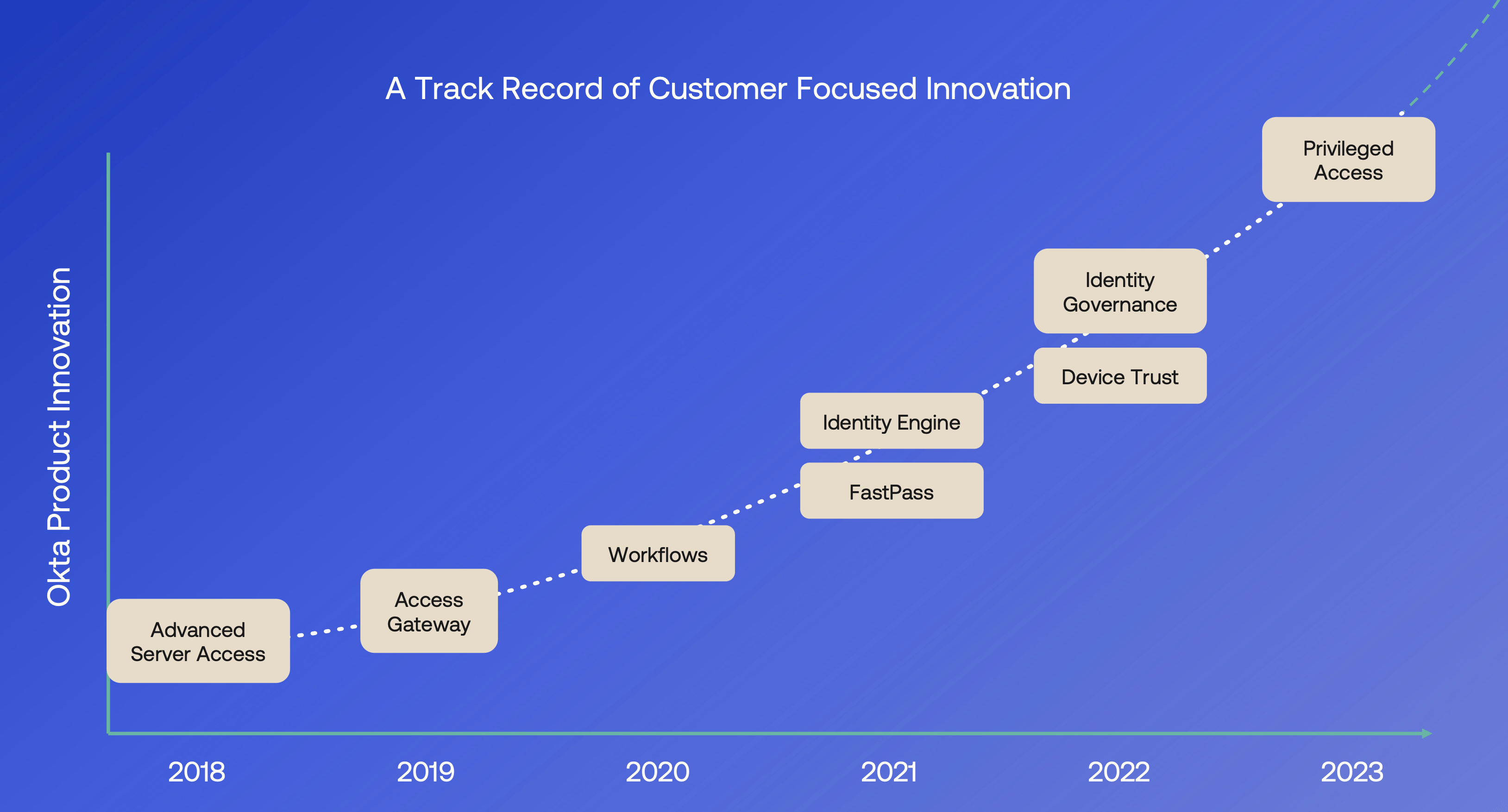

Innovation and adding new modules is another big opportunity. OKTA has done a good job of introducing new workforce identity products over the years. This is a key way to drive growth, and the company will add a privileged access module this year.

Company Presentation

Perhaps one of OKTA biggest opportunities in the near term is a low bar. In late November, the company forecast that FY24 revenue growth would slow to 16-17% versus the consensus calling for 27% growth.

On its Q3 2023 earnings call, CFO Brett Tighe said:

“With our continued focus on expense control, we are focused on achieving non-GAAP profitability for FY ’24 and an operating margin in the low single digits. We’re also targeting a meaningful increase to free cash flow and free cash flow margin over FY ’23, and we’ll provide more specific cash flow comments on our Q4 call. From a revenue perspective, we are factoring in the execution challenges we faced this year, the go-to-market leadership transition and the growing uncertainties of the macroeconomic environment. We estimate total revenue to be in the range of $2.130 billion to $2.145 billion or growth of 16% to 17%. While we had initially planned on providing an update on our long-term targets, we believe it’s prudent to wait and revisit this once we have increased visibility and confidence in the macro environment.”

These numbers appear pretty conservative, and stocks often perform well after companies reset the bar lower and then leap over it.

Risks

Competition, especially from Microsoft (MSFT), is one the biggest risks OKTA faces. MSFT’s E3 and E5 bundles have identity security as part of their offering. Thus, if a company is primarily using a MSFT stack, it essentially doesn’t need OKTA.

Speaking at the Needham Growth conference in January, Tighe was defiant that MSFT was a huge challenge, saying:

“But what I would say is, I mean, MSFT has always been there, and MSFT will always be there. There is no world where Active Directory doesn’t exist or Azure AD doesn’t exist, right? I mean the vast, vast majority of our customers have MSFT, right? They’re a great competitor. They’re a great company.

“If you want to be a single-stack company, MSFT is going to win. We’re not going to be able to compete with an E3 or E5 agreement if it’s 100% of your stack is on MSFT, right? But I think there’s less and less of those customers out there, right? You have to believe in a world where ServiceNow, Salesforce, Workday, Zoom, I can keep going for the next 20 minutes on number of companies out there wouldn’t exist. And that’s where I think OKTA really shines.

“So once you step out of that single-stack mentality, that’s where we do well. And I think — I mean, we do well even — actually, for years, we’ve done a great job. We’ve been doing access in the MSFT products better than they have. You can look at the ratings on their website. But I mean, they’re going to make them better, right? Like it’s their stack. They’re going to make it better. You can’t expect that to continue.”

In addition to MSFT, OKTA has faced other challenges. Sale productivity has been down, and the company has seen a lot of attrition with its salesforce, particularly on the Auth0 side as the company has run into integration issues. Part of the problem appears to be hiring too many new reps (it recently announced layoffs) and its compensation was not high enough to retain top reps.

To this end, there will also be some disruption as the company changes salesforce leadership to address these problems. The company has already said it doesn’t see much improvement on sales productivity for 2024.

Valuation

SaaS companies are generally valued based on a sales multiple given their high gross margins and the companies wanting to pump money back into sales and marketing to grow.

On that front, OKTA is valued at a P/S ratio of about 5.5x based on the FY 24 (ending January) consensus for revenue of $2.17 billion. Based on the FY25 sales consensus of $2.57 billion, it trades at a P/S multiple of 4.7x.

In the past, the company has often traded at over 25x LTM sales. However, growth is slowing from 40-50% a year to around 18% over the next two years.

FinBox

If the stock could re-rate to a 6x multiple of its FY25 revenue, OKTA would be $100 stock.

Conclusion

Currently the market has been rewarding beaten-up growth stocks that have been able to jump over vastly lowered bars. The jumps in the stocks of Roku (ROKU), Roblox (RBLX), and HubSpot (HUBS) this week are good examples.

OKTA is another really good example of this set-up. The company has already taken down not just Q4 expectations but FY24 expectations as well. OKTA has some challenges to continue to overcome, but it’s set itself up nicely to jump over a low bar.

Meanwhile, despite the rebound in the stock price, it is still trading at the lower range of where it has traded historically and where many SaaS names trade currently. That’s a good recipe for a nice post-earnings pop if investor sentiment doesn’t change between and when the company reports results in a couple of weeks.

Be the first to comment