Mila Naumova/iStock via Getty Images

One of the more interesting companies that I’ve come across recently is a firm called Oil-Dri Corporation of America (NYSE:ODC). This firm, in a nutshell, produces and sells sorbent products. In recent years, management has done a pretty good job growing the company’s top line. However, profitability has been somewhat volatile and, this year especially, the company is experiencing some pain. To be perfectly frank, this firm is far from an excellent prospect. But given how cheap shares are, especially if we assume an eventual return to normalcy, it may not be a bad prospect to consider. All things factored in, I ended up rating the enterprise a soft ‘buy’ for the long run even though I wouldn’t be surprised if the business suffers more on the bottom line in the near term.

A niche business

As I mentioned already, Oil-Dri focuses on the production and sale of sorbent products. Although management goes into real detail about the specifics of their formulations, a better approach for this article might be to just focus on the primary products that the company sells. First and foremost, the company sells a variety of products under the agricultural and horticultural categories. These include Absorb, which is an agricultural and horticultural carrier and drying agent, and Verge, which is an engineered granule used as a carrier and drying agent. These two products are used in other products that act as alternatives to liquid sprays. For instance, they are often sold for lawn and garden applications. Agsorb is blended into fertilizer-pesticide blends With the purpose of helping the blends to absorb moisture and improve flowability. The company also has another product under this category called Flo-Free, which is a highly absorbent microgranule that is used as a flowability aid, largely by grain processors and other large handlers of bulk products in order to soak up excess moisture.

Under the animal health and nutrition solutions category, the company produces mineral-based solutions geared toward ensuring the intestinal health of animals, ranging from poultry, to swine, and more. The company’s offerings even extend to promoting the health of dairy cattle livestock. Another category worth mentioning is referred to as bleaching clay and purification aid products. Bleaching clays are used by edible oil processors to absorb soluble contaminants that caused oxidation problems. Other products, such as Ultra-Clear, can be used as a purification and filtration medium for jet fuel and other petroleum-based products. On top of this, the company also has a line of offerings under the cat litter products category. Under the scoopable and non-clumping categories, the company sells two different brands. One of these is Cat’s Pride, while the other is Jonny Cat. The company also provides litter box liners and offers some of its products in a pre-packaged, disposable tray for the clients who want them. Psalm activities provided by the company include the production of private label cat letters and Co packaged products. Under the latter of these categories, the company has a long-term supply agreement with Clorox (CLX) to supply that company’s requirements for its Fresh Step coarse cat litter.

Some of the company’s activities also include other industries. For instance, under the industrial and automotive products categories, the company produces and sells clay, polypropylene, and recycled materials that helped to absorb oil, acid, paint, ink, water, and other liquids. On top of this, the company also produces sports products such as soil conditioners that are used in field construction or stop dressing to improve drainage and other functions. Its Pro Mound packing clay is used in the construction of pitchers mounds, catchers stations, and even batters boxes. And the company also has another product called Rapid Dry that operates as a drying agent used to Wick away excess water from the infield.

Author – SEC EDGAR Data

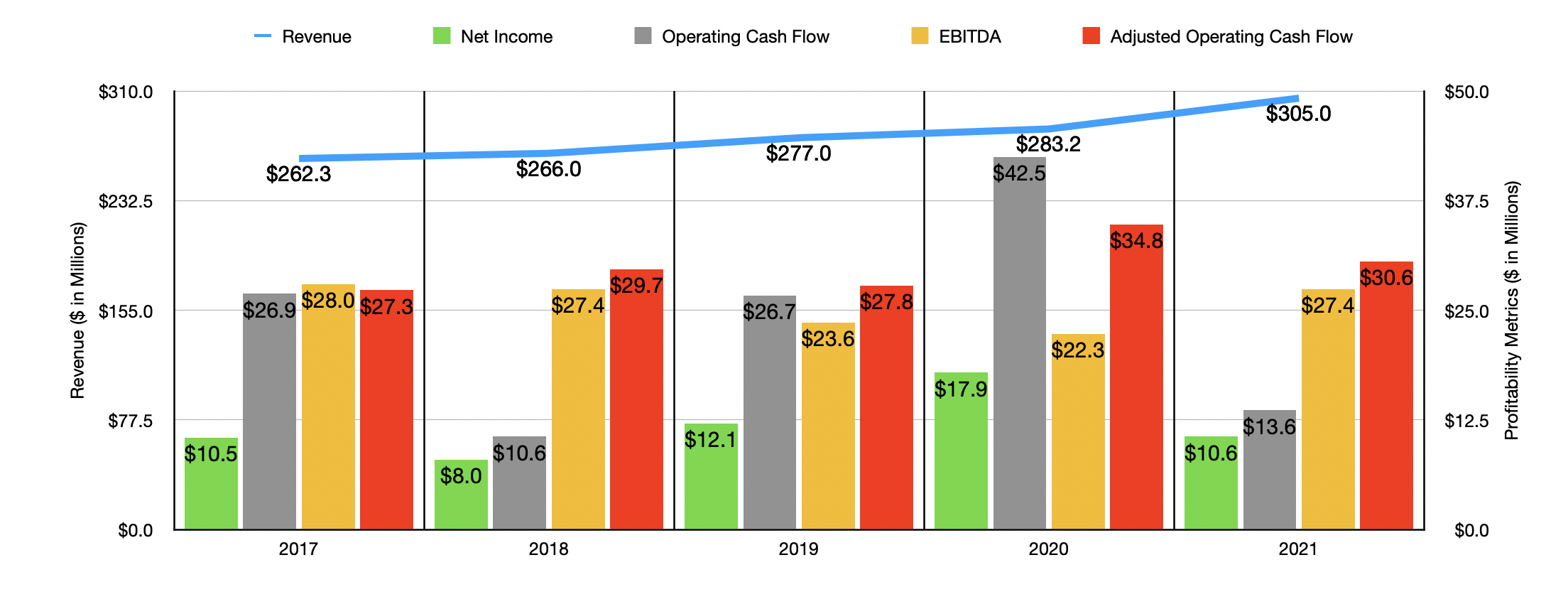

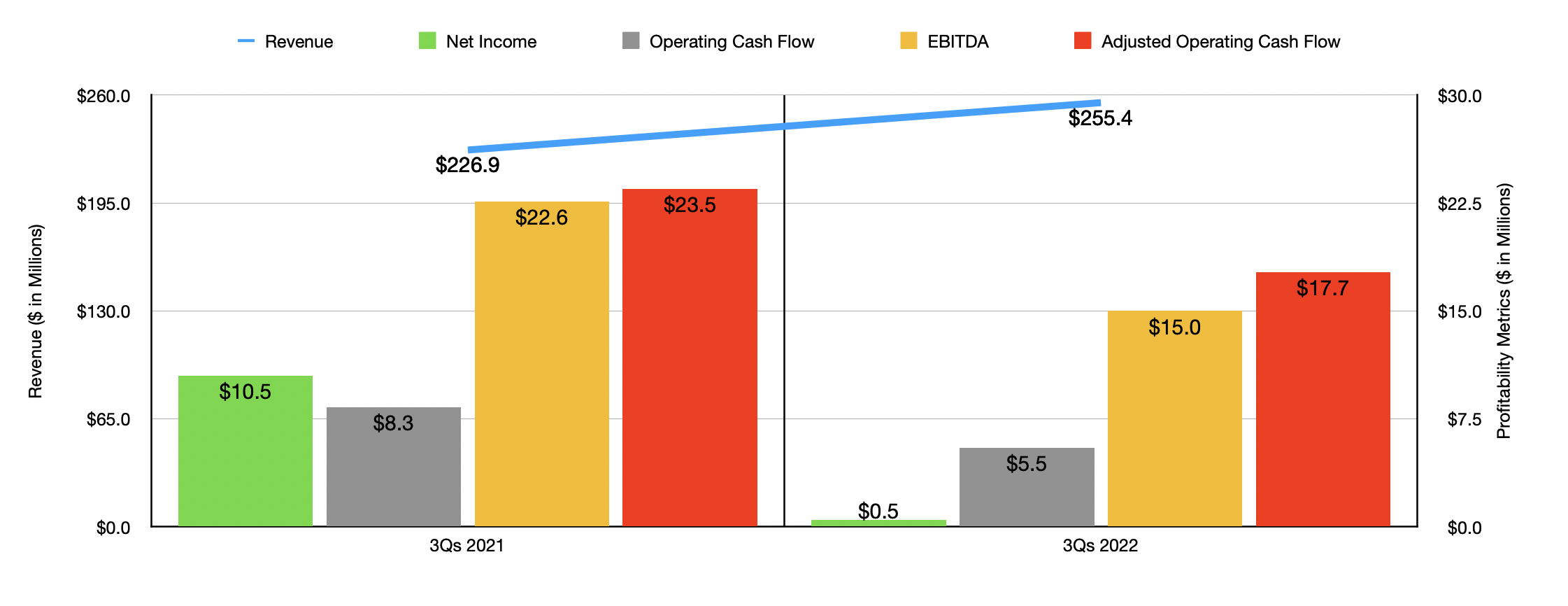

Over the past few years, the management team at Oil-Dri has done a pretty good job growing the company’s top line consistently. Revenue has risen in each of the past five years, climbing from $262.3 million in 2017 to $305 million last year. Growth on the company’s top line has so far continued into the 2022 fiscal year. Revenue in the first three quarters of the year, for instance, came in at $255.4 million. That represents an increase of 12.6% under the $226.9 million generated the same time one year earlier. This rise in revenue has been driven by a combination of higher pricing and higher volumes sold. This seems to be especially true when it comes to the cat litter industrial, and sports categories. The growth under the industrial and sports categories was particularly strong, coming in at 22% year over year. It is worth noting that

Although the general trajectory for revenue has been positive, profitability has been quite volatile. Between 2017 and 2021, net income bounced around in a narrow range of between $8 million and $17.9 million. Last year, profits totaled $10.6 million. Other profitability metrics have been somewhat more stable. Operating cash flow did drop from $26.9 million in 2017 to $10.6 million in 2018. But after that, it began a consistent incline, rising to $42.5 million in 2020 before ultimately dropping to $13.6 million last year. This decline in cash flow was not as bad if you adjust for changes in working capital. In this case, the metric would have fallen from $34.8 million to $30.6 million. Meanwhile, EBITDA has been stuck in a narrow range, moving from a low of $22.3 million to a high of $28 million. Last year, the metric came in at $27.4 million.

Author – SEC EDGAR Data

Unfortunately, the company has seen some weakness so far this year. Even though revenue increased, net income fell from $10.5 million to just $0.5 million. Operating cash flow dropped from $8.3 million to $5.5 million, while the adjusted figure for this declined from $23.5 million to $17.7 million. And finally, EBITDA also dropped, going from $22.6 million to $15 million. This decline in profitability and cash flows was driven by increased costs that the company experienced. In the first nine months of the 2022 fiscal year, for instance, the company suffered a 32% rise in Free costs, thanks to higher commodity costs. Packaging costs per ton also increased by 32% for the same reason, partly thanks to increased resin and pallet costs. The cost of natural gas per ton was even higher, essentially doubling year over year because of higher natural gas prices. In short, while the company did try to transfer some of its costs over to clients, it was not able to do this fully.

Author – SEC EDGAR Data

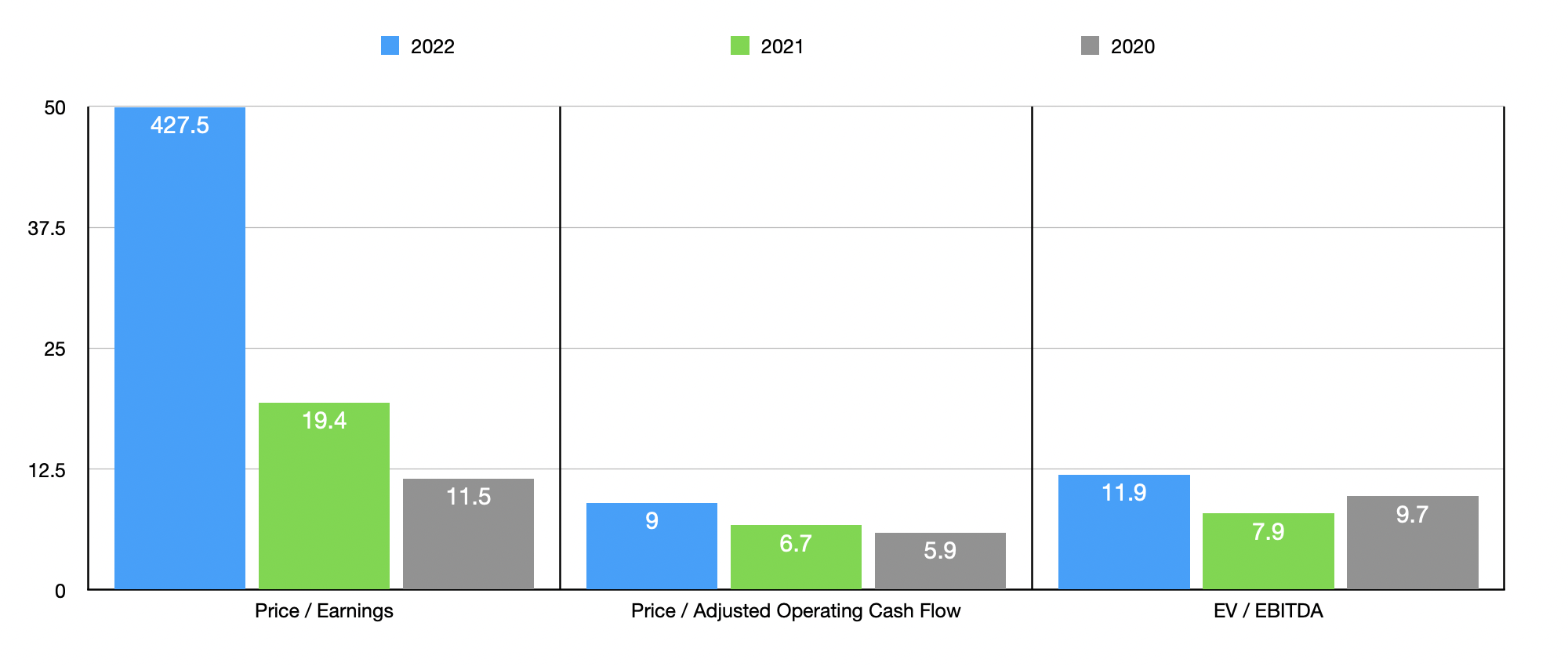

When it comes to the 2022 fiscal year as a whole, management has not provided any real guidance. But if we annualize results seen for the 2022 fiscal year as a whole, we should anticipate net income of roughly $0.5 million. Adjusted operating cash flow should be roughly $23 million, while EBITDA should come in lower at $18.2 million. Using these figures, we can see that the company is trading at an astronomical price-to-earnings multiple, on a forward basis, of 427.5. That compares to the 19.4 reading we get using 2021 results and is up from the 11.5 reading we get using 2020 results. The price to adjusted operating cash flow multiple, meanwhile, is much lower at 9, while the EV to EBITDA multiples should be 11.9. Although low, both of these are higher than the 6.7 and 7.9 readings we get, respectively, using the 2021 data. Using the company’s 2020 figures, these figures would be 5.9 and 9.7, respectively. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, the four companies with positive results were trading at multiples of between 10.6 and 46.4. Clearly, Oil-Dri was the most expensive of the group. Using the price to operating cash flow approach, on a forward basis, the range was between 15.4 and 98.7. In this scenario, Oil-Dri was the cheapest of the group. And when it comes to the EV to EBITDA approach, the range was between 10.1 and 32.9, with two of the five companies cheaper than our prospect.

| Company | Price/Earnings | Price/Operating Cash Flow | EV/EBITDA |

| Oil-Dri Corporation of America | 427.5 | 9.0 | 11.9 |

| Energizer Holdings (ENR) | 10.6 | 40.2 | 10.9 |

| Central Garden & Pet Company (CENT) | 15.8 | N/A | 10.1 |

| Spectrum Brands Holdings (SPB) | N/A | 19.7 | 25.3 |

| WD-40 Company (WDFC) | 46.4 | 98.7 | 32.9 |

| Reynolds Consumer Products (REYN) | 22.1 | 15.4 | 15.3 |

Takeaway

Based on all the data provided, I’m definitely intrigued by the business model of Oil-Dri. At present, the company is experiencing some pressure on its bottom line. But given the circumstances and given how much its own products are based on some rather vital commodities, none of this should be a surprise. In the short term, it could ultimately pose more problems for the company. But in the long run, much of this pricing will stabilize, allowing the company to return to a more normal state. Because of this, I’ve decided to rate the firm a soft ‘buy’ at this time.

Be the first to comment