Peter Blottman Photography/iStock via Getty Images

Investment thesis

We believe the company’s fundamentals hit bottom in Q3 FY12/2022 results, and there will be sequential improvements to come particularly in gross profitability. However, Oatly (NASDAQ:OTLY) needs to raise substantial cash in the next 12 months which will be a key risk event – until we have more information on the deal structure we believe the shares are not investable. We rate the shares as neutral.

Quick primer

Oatly AB was founded in 1994 specializing in sustainable nutritional health products based on oats, such as milk, ice cream, “oatgurts” and chilled drinks. The technology was originally developed by scientists at Lund University in Sweden.

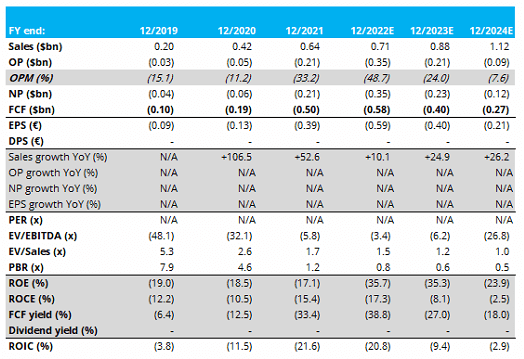

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Bloomberg, Karreta Advisors)

Our objectives

We revisit our sell rating from January 2022, with the shares having corrected 63%. Over the last 12 months, the company has experienced a significant deceleration in sales growth, falling profitability, changes in senior management, ongoing production problems, and macro challenges with cost inflation. Management also announced an overhead and headcount reduction program in Q3 FY12/2022 results.

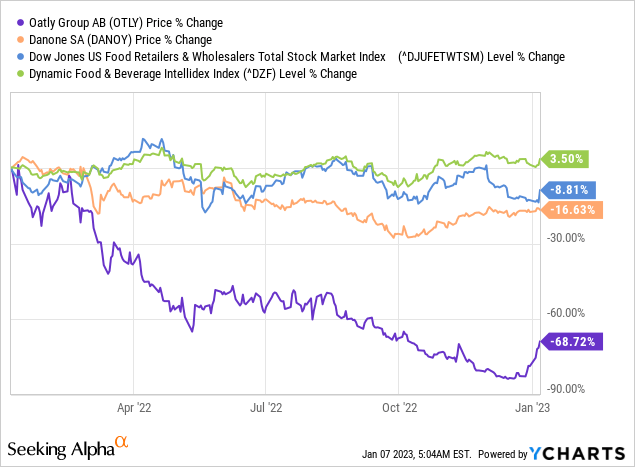

Oatly’s shares have vastly underperformed its core peer Danone (OTCQX:DANOY) with its ‘Alpro’ plant milk brand, and food and beverage-focused market indexes.

In this piece, we want to assess whether the shares are now attractive given the major drawdown. In particular, we pay close attention to cost reduction initiatives, the outlook for cash burn and financing risks, and management.

Aiming for profitability

A potent negative mix of events resulted in Q3 FY12/2022 results experiencing a collapse in gross margin from 26.2% to 2.7% a year previously. The negative impact came from a mix of cost inflation, lack of production in the US, and the lack of demand in Asia (primarily China with ongoing COVID-19 restrictions). Things would indeed have been worse without price hikes, which were successfully introduced in the key US market. The strong dollar also had a negative foreign translation impact on revenue, which grew 7% YoY (underlying growth was 15% YoY, with constant rates YoY).

With this performance, we believe management had little choice but to announce a cost reduction program (page 6). Although Q3 FY12/2022 results highlight the relatively volatile profitability profile of the business, we believe that this is a bottom, and margins are set to improve from here. Our reasoning is that 1) underlying consumer demand for Oatly products remains high, and further successful price hikes are likely to combat cost inflation, 2) production concerns in Ogden appear to be on the mend, allowing for stock to reach customers, and 3) although we expect this to be a moving target, loosened COVID-19 restrictions in China should help normalize customer behavior and drive sales volume.

With current consensus forecasts pointing to continued operating losses into FY12/2025, we remain skeptical that the business will become profitable in the medium term. However, we believe operating losses will no longer deteriorate and will gradually improve.

Cash and management

With a net cash position of USD115.9 million, and a revolving credit facility of approximately USD320 million (with an accordion of an additional USD76 million), in the short term, the company has access to liquidity. However, with ongoing high capex demands, it is inevitable and well-understood that the company requires financing – CFO Hanke has commented that Oatly is working on ‘multiple financing tracks’. In essence, the company needs to raise substantial cash within the next 12 months with sustained cash burn.

With debt financing becoming more expensive, Oatly may be tempted to use equity. Arguably, Oatly is attractive in terms of its brand, manufacturing assets, expertise in oat products, and growing global footprint. At the right price, a business or a group of investors may be attracted to buying a stake in the company. If external parties were to become equity holders, we would not be surprised if this became the trigger for founder CEO Toni Petersson to stand down, and recent recruit Jean-Christophe Flatin to be promoted from his current position as global president.

The problem for existing shareholders is twofold. Firstly, a debt raise will result in an indebted balance sheet which will place a discount on valuations, limiting any upside. Secondly, an equity raise is likely to be significantly dilutive. The scale of any financing we expect will be large, as Oatly is not in a position to generate any free cash flow and management are probably not keen to keep coming back to the markets for cash.

Valuation

With no earnings and negative free cash flow, the shares are expected to trade below book value at 0.8x in FY12/2022. Oatly shares remain in value territory, but we feel that a significant level of risk has been priced into the shares.

Risks

Upside risk comes from sequential improvements in gross margins in the short to medium term, as the company successfully navigates through price hikes and cost management. A change of CEO is likely to instill greater confidence in the company and act as a positive catalyst.

Downside risk comes from equity financing with massive dilution, as well as taking on substantial leverage via debt. However, this is in part reflected in the current share price.

Conclusion

We believe Oatly has hit bottom in Q3 FY12/2022 and fundamentals are set to improve from here. However, the challenge of raising cash in a satisfactory manner will be a significant risk event. We are no longer bearish on the shares, but believe that it remains too risky to go long without more information about how Oatly will re-finance. We change our rating to a neutral stance.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment