BitsAndSplits/iStock via Getty Images

Oaktree Specialty Lending (NASDAQ:OCSL) is the type of stock that seems perfectly suited to today’s market conditions. Much like a bank, it lends money, so it can capture revenue from the current period’s rising rates. Unlike a bank, it does not hold deposits, so it doesn’t need to worry about yield curve inversion squeezing margins. It all looks like a recipe for success in today’s high yield environment.

Granted, you wouldn’t think that by looking at OCSL’s stock chart. Since inception, the stock has fared poorly, having fallen 44.5% since it went public. It has paid countless dividends in that time, but the stock started off at $36.37, fell to $20.37, and paid $9.9 in dividends along the way (ignoring the newly merged-in Oaktree Strategic Income). So, the dividends have not yet made up for the capital losses.

This year, that could start to change. The Fed’s interest rate hikes have resulted in a situation in which yields on bonds are going higher. Today, OCSL yields 10.62%.The company appears to be trading at a small discount to its assets, as it only lists a 10.6% yield on the actual portfolio–though the small 0.02% difference could be explained by the IR team rounding down. At any rate, you collect a significant yield on OCSL even if the dividend is not increased once in a 10-year period.

Why does OCSL have such a high yield? It’s a function of both dividend growth and a declining share price. OCSL has booked a solid four consecutive years of dividend growth, but in the last 12 months, the stock went down. That has resulted in a truly mind blowing yield. OCSL wasn’t always the ultra-high yield stock people think of it as today. At the start of 2009, the stock cost $18.68 and went on to pay $0.77 in dividends that year. So, the yield was only 4.12%.

OCSL dividends 2009 (Oaktree Specialty Lending)

Today, investors are being compensated much better for the risk they assume by holding OCSL. The company has steadily grown its revenue, gross profit and earnings over the last five years, and it has maintained its healthy balance sheet. Its stock nevertheless declined right along with the markets. So we have a lower price with a higher yield, apparently without a big increase in fundamental risk. There may be an opportunity here. In this article I’ll explore why I’m excited about OCSL in 2023, and why the company’s future may be better than its past.

What Oaktree Specialty Lending Does

Oaktree Specialty Lending is a business development company (“BDC”) that lends money to businesses. As a BDC, it is required to pay out 90% of its earnings as dividends, and gains tax-exemption by virtue of doing so. Due to the BDC arrangement, OCSL shareholders avoid double taxation – which occurs in regular corporations whenever they turn profits. So there are tax benefits to a structure like that of OCSL.

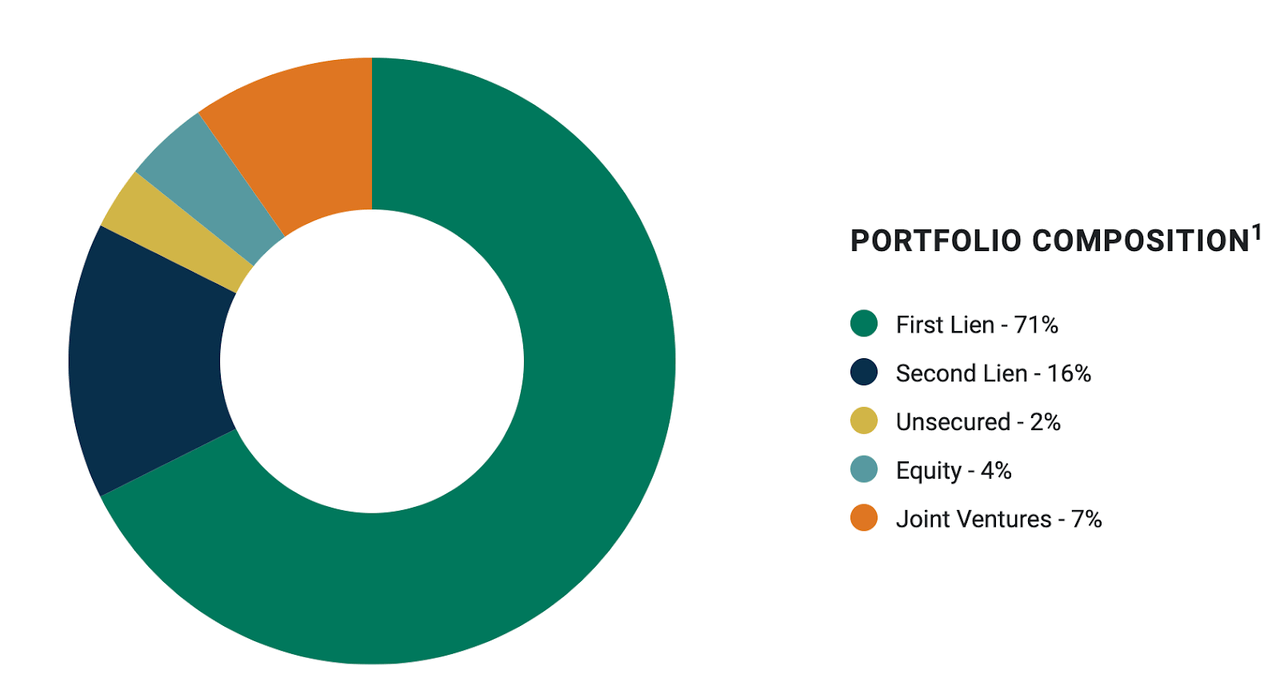

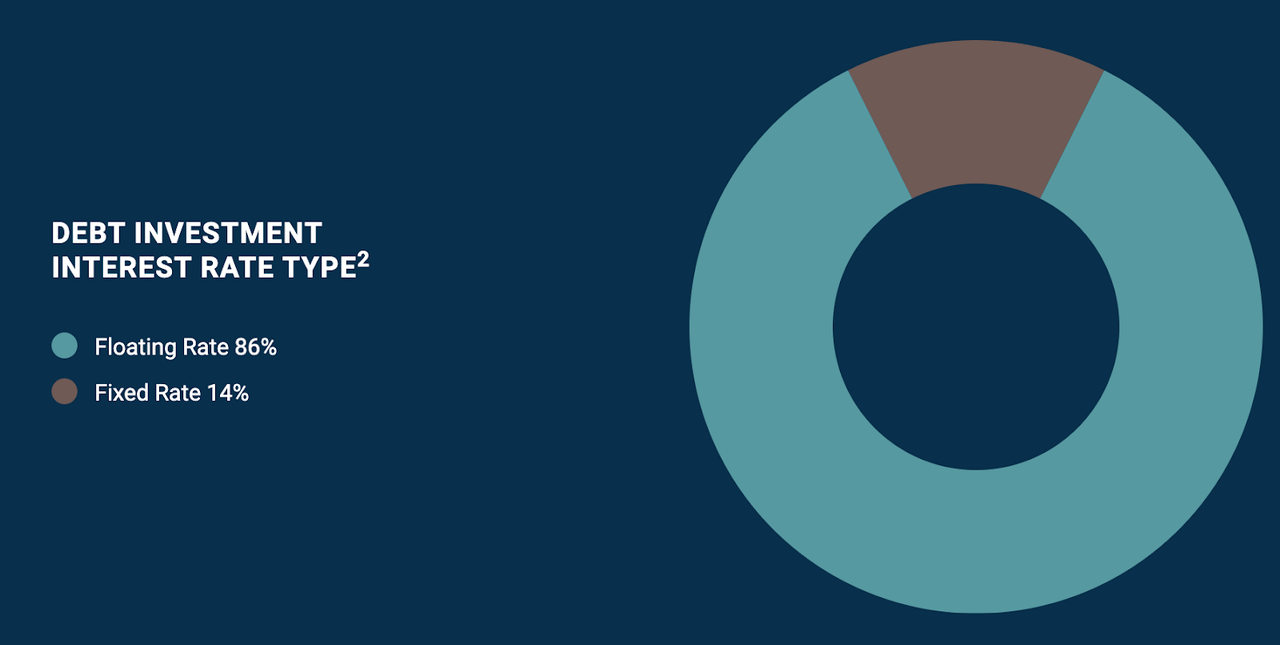

What kind of loans does Oaktree issue?

According to Oaktree’s website, the breakdown is:

-

71% first lien.

-

16% second lien.

-

2% unsecured.

-

86% floating rate.

-

14% fixed rate.

Types of loans (Oaktree Specialty Lending) Floating vs fixed (Oaktree Specialty Lending)

So, most of Oaktree’s loans look pretty sound. They are generally high yield loans, but they’re backed by collateral, so Oaktree has recourse on most of them if they go into default. Having this characteristic in a high yield portfolio is a good thing, because high yield debt is generally thought to be at elevated risk of defaulting.

In addition to its portfolio, we can also look at Oaktree’s business model. It’s a lender, but it’s not a bank, so the risk profile is different from that of a bank. How does Oaktree’s risk profile differ?

The main difference is that Oaktree doesn’t take deposits. One of the main criticisms of banks is that they “borrow on the short end of the yield curve, lend on the long.” A lot of a typical bank’s assets are savings accounts, which may be withdrawn at any time, and checking accounts, which are getting drawn down on a daily basis. These accounts don’t typically pay much interest, but banks also offer term deposits (e.g. CDs), which do face some pressure to match the treasury yield. In theory, inverted yield curves put pressure on bank margins. That hasn’t really been seen since the yield curve inverted last year–banks have been putting out very strong earnings lately – but margin pressure is likely to be seen if the yield curve inverts further.

It’s here that OCSL really stands out. The company does not take deposits, rather it finances its operations by borrowing money in amounts that it chooses. This is very different from bank deposits which simply increase when customers deposit, and decrease when customers withdraw.

Because Oaktree borrows when it pleases, it can reduce the risk of margin pressure stemming from an inverted yield curve.

Let’s say you’re an Oaktree credit portfolio manager. You just closed a deal to loan someone a million dollars at 5% interest over five years, now you need to come up with the money. Now, Oaktree has $23.5 million in balance sheet cash, you may be able to access some of that to issue the loan. Let’s ignore it for a moment and pretend you have to borrow in order to make the loan. Because you’re a BDC, not a bank, you may opt to issue a bond at 4%, ensuring a 100 basis point spread between the money you borrowed and the money you lent. Because you’re not taking deposits, you can always negotiate your financing like this. A banker doesn’t have this advantage, and is therefore more exposed to yield curve risk than a BDC lender is.

Oaktree Specialty Lending: Recent Results

Having looked at an advantage that OCSL “theoretically” enjoys, let’s see if that advantage is actually yielding results.

In its most recent quarter, OCSL delivered:

-

$0.38 per share in investment income, up 11.76%.

-

$0.20 per share in EPS, down 10.5%.

-

$6.79 in NAV per share, down 1.45%.

-

$97 million in new loans originated.

-

A 1.08 debt/equity ratio.

-

$1.35 billion in total debt.

-

$0.18 in quarterly dividends per share, up 6%.

A pretty solid showing. Obviously, net income went down a bit, but remember that GAAP net income is impacted by non-cash factors. Had OCSL been structured as a closed end fund, it simply would have reported the 11.76% jump in investment income as a gain. Also, the results on a full year basis were pretty strong. Some highlight metrics included:

-

$1.44 per share in investment income, up 11.6%.

-

$0.80 per share in net income, up 20%.

So, the full year showing was pretty good as well. This very brief review of OCSL’s recent earnings corroborates what I said earlier about the company’s relationship to today’s macro climate: namely, that it should benefit from the higher rates in the long run. Obviously, it’s possible to look at these results in far more depth than I did just now, but the “highlight metrics” are a good early indicator that things are going well at OCSL.

Valuation

Now it’s time to look at OCSL’s valuation. At today’s prices, the company trades at:

-

9.65 times adjusted earnings.

-

8.37 times forward GAAP earnings.

-

4.7 times revenue.

-

1 times book value.

Overall, these multiples are fairly low. The price/sales multiple is pretty high, but thanks to OCSL’s incredibly high margins, it does not translate to a high P/E ratio. So, you’re not paying too much for what you’re getting with Oaktree Specialty Lending.

A Risk to Watch Out For

So far, most of the factors I’ve looked at are flattering to Oaktree Specialty Lending. The stock is cheap, and the company is profitable and growing. Looks like a slam dunk buy. Indeed, I do consider OCSL a buy, but not a strong buy, as there is one risk to beware of:

A high debt level.

As I mentioned earlier, OCSL’s debt/equity ratio is higher than one. This means that the company has more in debt than it has in equity. This creates a number of issues. First, interest expenses for high-debt companies tend to be high. Second, companies with high debt/equity ratios can see their equity grow smaller still when new borrowing is needed. Third and finally, OCSL has only $23.5 million in cash on a $2 billion portfolio: to issue enough loans to grow the portfolio meaningfully, new debt issuance virtually has to occur. So, there is some balance sheet related risk here.

The Bottom Line

The bottom line on Oaktree Specialty Lending is that it’s cheap, it’s profitable, and it’s growing. A historical track record of growth doesn’t necessarily mean continued future growth, but OCSL has got high interest rates serving as a tailwind right now, so there’s plausible reason to think the company will continue growing. The amount of debt this company holds is substantial, but not fatal: a 1.08 debt/equity ratio is not that high. On the whole, it looks like a solid high-yield opportunity.

Be the first to comment