IR_Stone

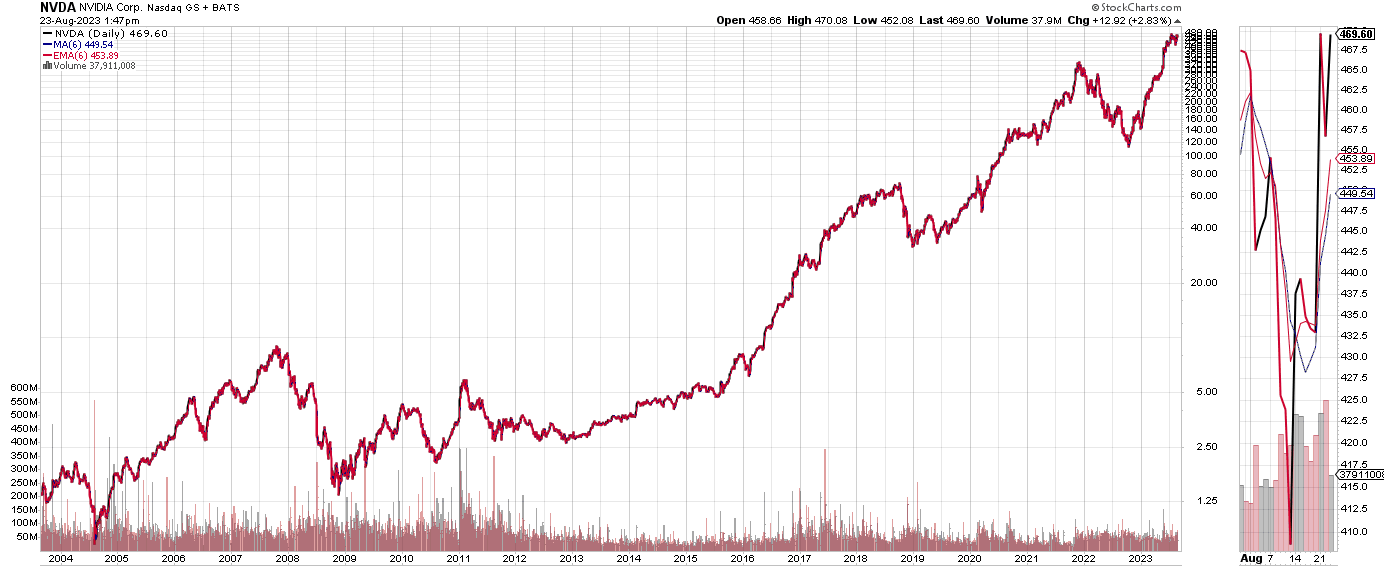

The rise of the FANGMANTIS stocks has been spectacular to see. To put this into perspective let’s take a quick look at the chart for Nvidia:

StockCharts

The graph is deceptively logarithmic so let’s pull out some mind-boggling return statistics. Nvidia (NASDAQ:NVDA) traded at 0.75 cents in August of 2004, which is 19 years ago. The company currently trades at $493. That’s a 627 fold return over that time period.

The company is now forecast to essentially take over the world of digital infrastructure and data centres, with a 3.05% weighting in the S&P 500 index and a market cap above $1 trillion.

I intend to make the case for the fact that the odds – and gravity in the form of excited expectations- are stacked against the company and the growth rates that have been achieved are very unlikely to be sustained.

Fundamental Analysis of Nvidia

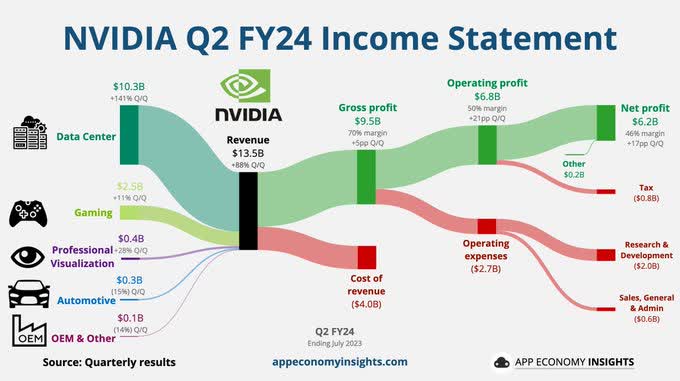

The latest Q2 earnings report registered a record $13.51 billion in revenue, which was up 88% from Q1 and 101% from the same time last year.

Their data centres reported $10.32 billion in revenue. The founder and CEO Jensen Huang was positively ebullient:

“A new computing era has begun. Companies worldwide are transitioning from general-purpose to accelerated computing and generative AI.”

Nvidia’s outlook for 2024 is even more spectacular – they expect revenue of $16 billion and gross margins of 71.5% to 72.5%, which represents a healthy – albeit much slower – 18.5% growth from here.

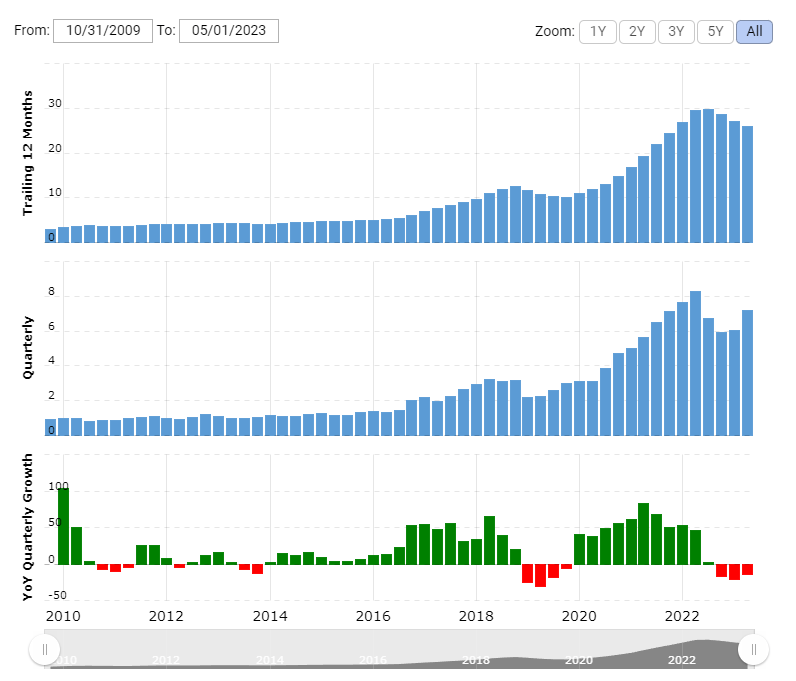

Have a look at revenue since 2010:

Macroeconomics

Data Centre is the largest revenue driver at $10.32 billion, followed by Gaming at $2.49 billion, and small revenue streams for Professional Visualization and Automotive.

The Data Centre business is really in the driving seat here. Analysts believe that they are the wide moat leader in AI graphics processors and as such revenue for this area of the business has gone from $3 billion in 2019 to $15 billion a year ago, to what could be as much as $41 billion in revenue for next year (2024). Hence why the share price has appreciated significantly as it prices in this growth. That’s regardless of whether it materialises, though.

The business trades on a hefty premium. It trades on a 237.4x price earnings ratio for the trailing 12 months and a forward PE of 57 (based on highest EPS forecast of 8.75 next year) according to the Nasdaq.

There is a lot that could be said about valuation. In my view, Nvidia has definitely gotten ahead of its skis and trades on a very high valuation. However, it does have a reasonable ability to turn that revenue into actual profit and so one must be careful jumping into a short prematurely:

App Economy Insights

The visualization from App Economy Insights really demonstrates that net profit is a significant proportion of revenue – this means it’s a profitable business that is turning out cash and hence can afford another $25 billion in share buybacks, that further drive the share price up. We’re not talking about the no-profit EBITDA valued businesses that got re-rated in 2022.

It is surprisingly reminiscent of another company.

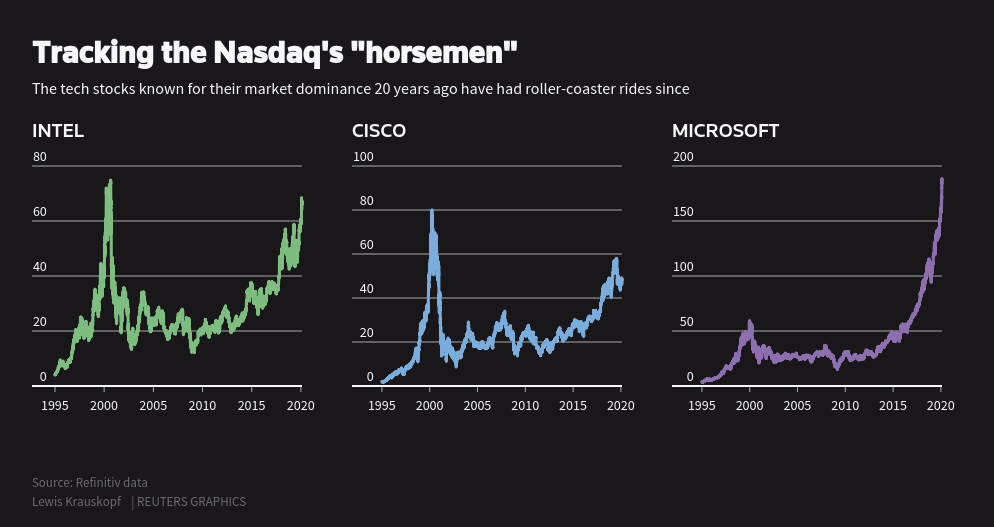

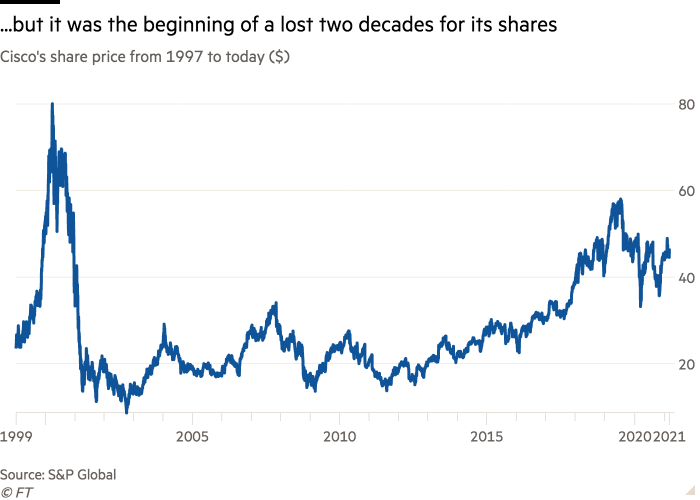

Rhymes with Cisco

The fact that Nvidia has similarities with another tech darling – Cisco – has not escaped market participants. The following chart was making the rounds on Twitter during earnings week:

Refinitiv

S&P Global

Cisco powered the rapid rise of the internet and the hardware that was required to build it out. The company had a similar impressive burst of revenue as it produced the switches, routers, and tools necessary to build out digital infrastructure. It became the most valuable company in the world at the height of the dot com boom and it also traded on 240 times earnings. Once the bubble popped, Cisco’s plunge was biblical.

If you compare the revenue growth and the share price, another interesting tidbit is that Cisco didn’t stop growing before the crash. It managed to double revenue again in 2001, all the while, forward looking investors dumped the stock. So don’t underestimate the possibility of the same happening to Nvidia.

Insider Selling & Shelf Offering Are Warning Signs

Putting fresh money to work in Nvidia at >$500 per share is a risky investment. The company has experienced stellar growth and it is now priced in for 100% top line revenue growth, annually, which simply is not sustainable.

I would go a step further than this: I’d say that there’s no mega-cap stock, that has ever traded at 100x earnings, and not thereafter avoided a 30-50% drawdown within the subsequent 3-5 year period.

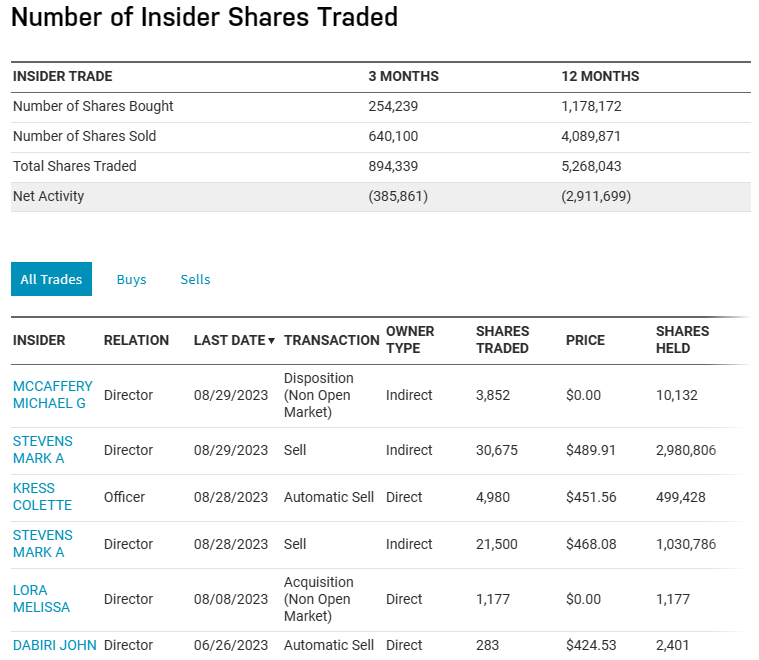

Insiders clearly agree as there has been disproportionately more insider selling than buying, with a recent director sell for 30,675 shares ($15 million) and multiple transactions unrelated to tax selling:

Nasdaq Website

Beyond the insider selling, in March of this year the company filed a shelf offering for $10 billion offering various types of stock and debt issuances in the open market. This allows the company to register a new shares with the SEC and adjust the timing of sales and when they offer them to the market. This may indicate that the board of Nvidia believe, essentially, that the company at current valuation levels is at or above fair market value.

If they felt that the company was below fair market value they could – instead – be purchasing and cancelling shares to create shareholder value.

Overall Assessment

Nvidia is an amazing company bringing value to the market through its data centres and the expansion of AI. However, from a valuation perspective the company clearly trades on a very lofty price multiple and it is unlikely to sustain the level of revenue growth to maintain this valuation for long. Management clearly see the same thing and are offering additional shares to the market, and selling their own shares in significant volume. For that reason I rate Nvidia a Hold.

For those who believe the company is in a bubble we do have one idea for a short position in the company.

There are two methods for shorting Nvidia. A risk-limited options play would be to take the following longer-dated positions:

- September 2024 Bear Call Spread on NVDA that buys to open 490C and sells to open 480C. This results in a net credit of $440 today and would pay out $440 if the price is below $484.40 by September 2024

The best investors tend to avoid purchasing growth at any price. Those who are long Nvidia from $475 and above need to be asking themselves: have they appreciated and evaluated the growth on offer against the price being paid? Are they aware of the risks associated with overpaying for a company regardless of where we are in the cycle?

Be the first to comment