SolStock/E+ via Getty Images

Investment Thesis

Bright Horizons (NYSE:BFAM), facing down the challenges in 2020 brought by the pandemic, has been on a healthy recovery path. However, we see challenges remain in its near-term cash flow and long-term supply/demand dynamics from its clients due to the societal changes following the pandemic. We remain optimistic about its long-term growth but would re-assess its prospect with slower growth in the near term.

Company Overview

Bright Horizons Family Solutions, founded in 1986, is a global provider of high-quality early education, child care, backup care, and workplace education services. The company partners with employers to support workforces by providing child care services to help their employees personally. It has approximately 1,100 early education and childcare centers in the U.S., U.K., the Netherlands, Australia, and India. It serves more than 1,350 large enterprise employers.

Strength

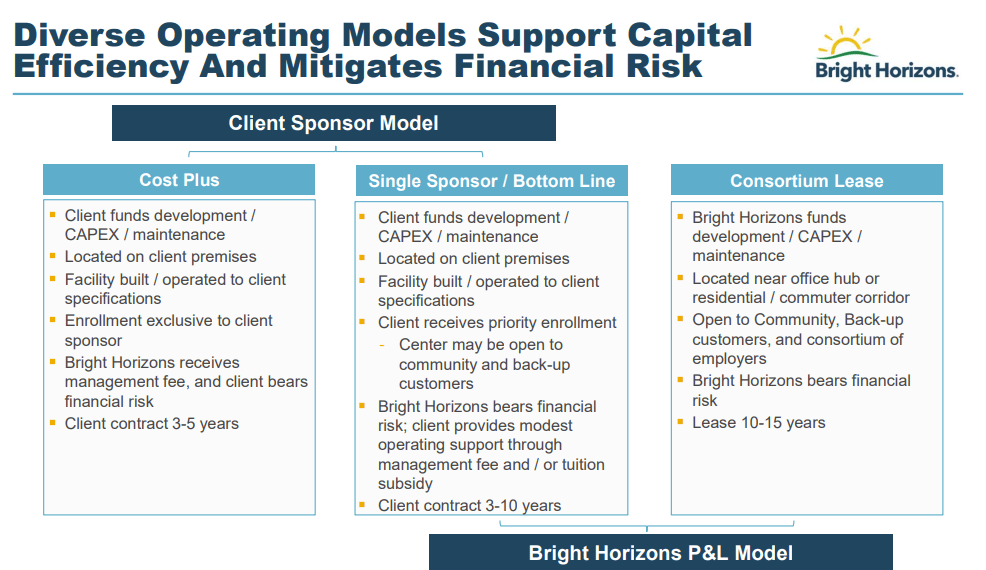

Bright Horizons is one of the largest providers of employer-sponsored childcare services around. Its business model is centered around this employer-sponsored model, in which a single employer or consortium of employers enter into a long-term contract to provide child care at a center located at or near the employer sponsor’s worksite. The strength of this service model is that most of these contracts are at multi-year lengths. The facilities the company’s childcare centers are situated in are usually leased or owned by the sponsors, being part of a large office building where the sponsor’s office is located.

BFAM Operating Models (BFAM Q3 Presentation)

They are usually spacious and have large outdoor areas that can accommodate a capacity of 128 children in their U.S. centers. Most of the centers have lease terms ranging from 10 to 15 years, with renewal options. So once a Bright Horizons center is set up and operating, it is at little risk of losing clients even when the contracts are due for renewal after multi-year operations. Simply put, it has no other competitors on site.

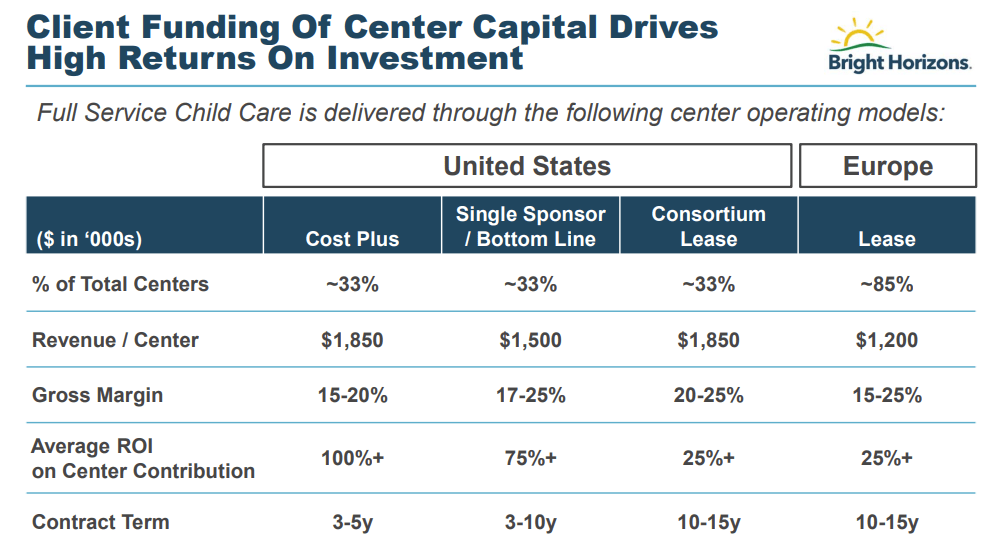

Of course, most of all, Bright Horizons’ strength has to be providing high-quality caring services. As an investor, when examining a company in the nature of caring for people, especially children, we believe its quality of service should be first and foremost focused. The company is in the premier price range as a private early education provider for children aged from infant to pre-k. It institutionalizes the childcare service and develops its in-house educational model to meet or exceed applicable accreditation and rating standards in all its key markets, including U.S., U.K, and Europe. It not only has continuous in-house training for its staff, but also supports the teachers in obtaining nationally-recognized certifications through training and educational programs. This focus on quality has to be the backbone for a long-term investment. With quality and scalability, it has been able to turn the typical low-return childcare services into a sustainably profitable operation with enrollments from both its sponsors and the local community. The company estimated that it has about six times more employer-sponsored centers in the U.S. than its closes competitor.

BFAM Care Center Return Analysis (BFAM Q3 Presentation)

Weakness/Risks

The most immediate risks to Bright Horizons’ steady-as-she-goes growth model have been the Covid-19 pandemic and the subsequent change of a hybrid working model.

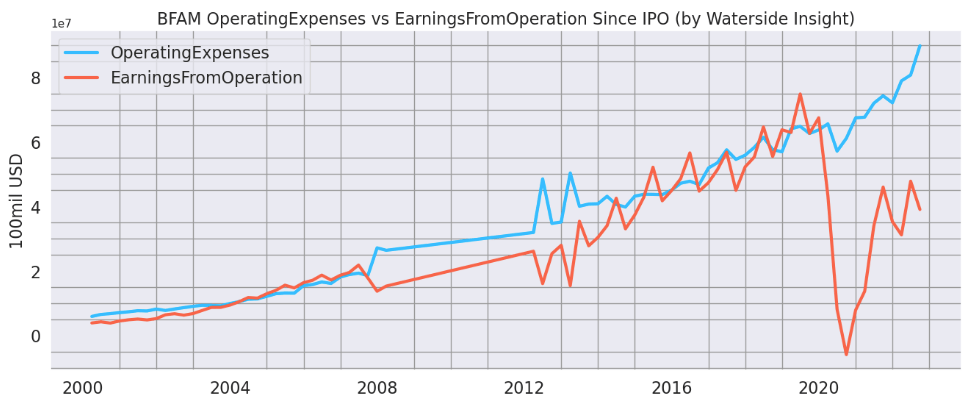

During the depth of the pandemic, the company’s enrollment growth became challenging, and costs rose. Managing precautionary and preventive measures and disrupted staff availability has increased its operating expenses by over 10-20% compared to pre-pandemic. And its earnings from operation took a hit and is still in the process of recovering. In 2020, the company’s per-center gross profit margin dropped from the usual 20-25% to 14%.

BFAM Operating Exp vs Earnings (Calculated and Charted by Waterside Insight with data from the company)

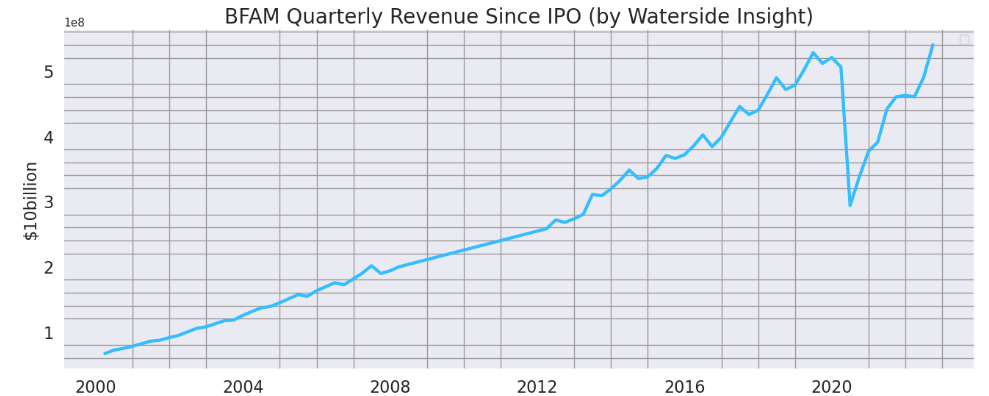

On the other hand, the hybrid working setup, which could be a more permanent change to the office occupying pre-pandemic situation, could decrease the appeal for the employees to have a childcare center close to the office instead of home. The market for early education and childcare services is highly fragmented. The work-from-home trend will further exacerbate this characteristic, which makes Bright Horizons’ market penetration become harder than before. Although in revenue, the company has recovered to the pre-pandemic level.

BFAM Quarterly Revenue (Calculated and Charted by Waterside Insight with data from the company)

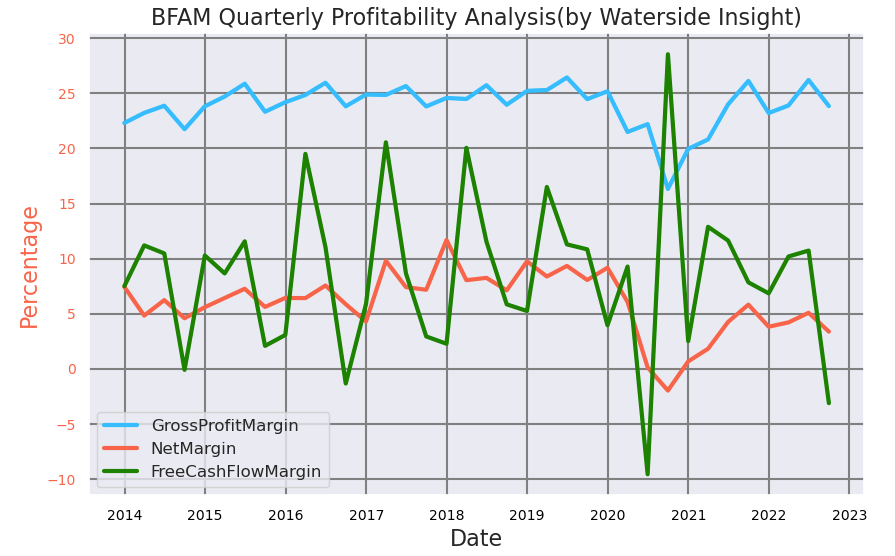

But if we dig deeper, we can see although its gross profit margin has recovered, its cash flow and net margin continue under pressure. In particular, its free cash flow has dropped negatively in the latest quarter.

BFAM Quarterly Profitability Analysis (Calculated and Charted by Waterside Insight with data from the company)

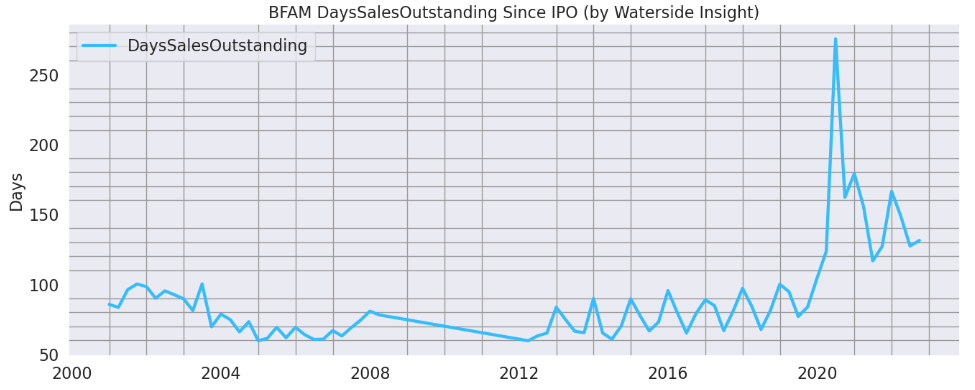

The enrollment that initially took a hit during the pandemic has not fully recovered yet. We can see it from its days of sales outstanding. It is still almost double its 2019 level.

BFAM Days of Sales Outstanding (Calculated and Charted by Waterside Insight with data from the company)

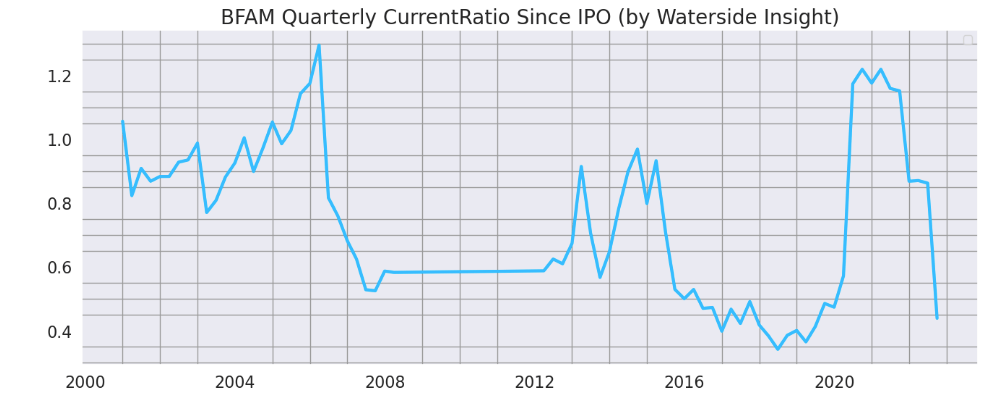

What’s more, its current ratio has dropped to only 0.5 times.

BFAM Quarterly Current Ratio (Calculated and Charted by Waterside Insight with data from the company)

While Covid and the other subsequent outbreaks continue to trouble our youngest citizens in recent times, the government support for childcare centers is wearing off as of the end of last year. Most of the federal and state support programs are no longer in the running. Bright Horizons recognized $50.9 million for 2021 and $83.5 million for 2020 from government support in helping reduce the cost and the need for operating subsidies from sponsors. These weaknesses above could partly help explain the drop in its cash position. What we are seeing is both short-term challenges and a longer-term shift of dynamics that present challenges to the company’s growth prospects.

In its 2022 10-K, Bright Horizons outlined that for a new center built under the P&L model, it will take about three years for the center to mature into a steady enrollment. If we assume 2020 was the reset for the company’s care centers, could we count the three years pattern for them to once again “mature” into steady enrollment in 2023? Or would business-usual take on a new look with a lower profit margin, high cost, and more unpredictable enrollment? The company mentioned in its 10-K that it planned on more center acquisitions for 2023. This could be a chance for it to diversify to more locations that could appeal to both employers and the community. To answer our previous questions, we think this reset since 2020 will have a longer run time than three years, and businesses will grow slower in general. The recent weakness will continue into 2023, and it will probably take more time for Bright Horizons to find its new horizon.

Financial Overview

BFAM Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

In Q3 last year, Bright Horizons’ revenue was $540 million, which increased by 17% YoY. The company’s net income declined to $18.2 million or $0.31 per share from $26.8 million or $0.44 per share YoY. Overall, its financials continued on a trajectory of recovery from the slump in 2020.

Valuation

Based on all our analysis above, we use our proprietary models to make a fair valuation assessment on the stock with a ten-year horizon ahead. In our most bullish scenario, Bright Horizons is pulling in more growth in 2023 but continues reconciling with its challenges in the long term; the stock is valued at $59.05. In our most bearish scenario, the company faces setbacks in the next two years and recovers afterward with slower growth in general; it is valued at $48.45. In our base case, its growth slows in the next two years but recovers to a trajectory similar to pre-pandemic; it is valued at $55.90. We believe Bright Horizons does have some near-term challenges that it needs to handle and resolve. They may or may not be solvable with simple acquisitions or the opening of more strategic care centers. And it also reflects our society’s preference as a whole.

Conclusion

We believe high-quality childcare is fundamental to a country’s living standard, which is why Bright Horizons’ services are important and always in demand. However, the pandemic and its aftermath changes have been challenges to the company and perhaps will remain so for a longer period of time. We like the fundamental business model and the quality of its care services as the appeal to a long-term investment option. However, the current prices are still too high for our valuation. We will sell at current prices and look for more growth prospects and a lower valuation.

Be the first to comment