Justin Sullivan

Nvidia’s (NASDAQ:NVDA) top line growth expectedly turned negative in the third fiscal quarter of FY 2023 due to a massive decline in the company’s Gaming business. Although Nvidia managed to beat top line expectations, the chip maker is likely to see more pressure on its top line in the coming quarters as demand for consumer electronics products can be expected to remain weak. While I like Nvidia’s product portfolio and especially the momentum in the Data Center business, I believe the stock is going to re-test its lows!

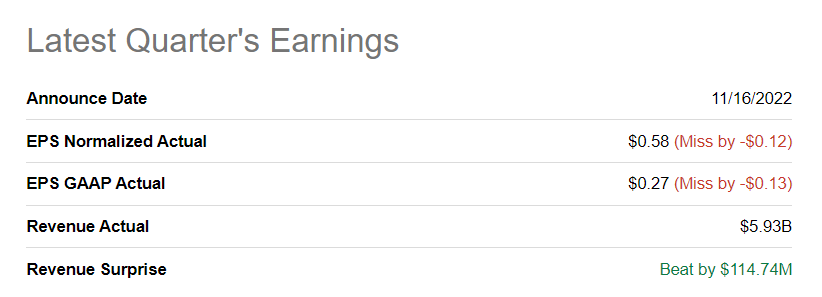

Nvidia beats low FQ3’23 revenue estimates

Nvidia issued a depressing revenue forecast for FQ3’23 (the quarter that ended on October 30, 2022) in August which called for revenues of $5.90B, plus or minus $118M. Last week, Nvidia reported revenues of $5.93B for FQ3’23 which was better than the low-end of the forecast and better than the average prediction of $5.81B. Nvidia missed on earnings, however.

Seeking Alpha: Nvidia FQ3’23 Results

Gaming struggled, Data Centers Gained

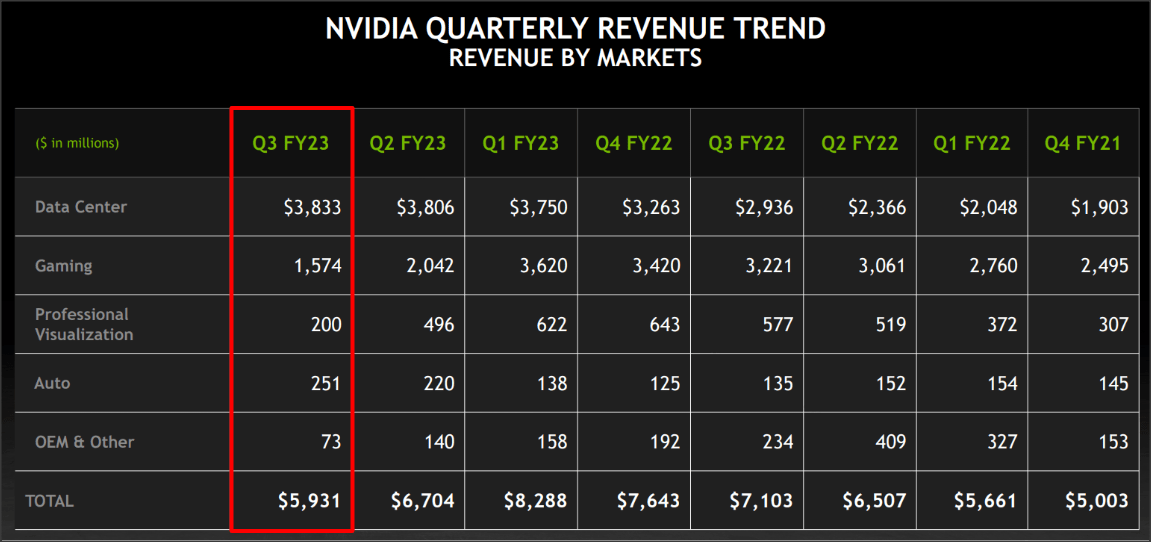

Nvidia generated total revenues of $5.93B in FQ3’23, showing a decline of 17% year over year, largely because the Gaming business continued to struggle. After seeing a 44% quarter over quarter top line drop in the previous quarter, Nvidia’s Gaming segment reported another 23% sequential decline in revenues due to weakening consumer demand, high inventory levels in the industry and pressure on selling prices.

The Gaming segment generated $1.57B in revenues in FQ3’23, showing a decline of 51% year over year and the lowest total revenue amount in years. Part of the problem for Nvidia are high inventory levels in the PC industry, which negatively affects product pricing.

Gaming was the largest revenue contributing segment for Nvidia in the year-earlier period and it exceeded the Data Center business by a considerable margin. Nvidia generated $3.2B in Gaming revenues in FQ3’22 (the year-earlier quarter) due to strong GPU demand from gamers compared to $2.9B in Data Centers. In FQ3’23, Nvidia’s Data Center business generated $3.8B in revenues, more than 2.4 times as much as the Gaming business brought in.

Nvidia: Revenue Trend

The Data Center business kept performing very well for Nvidia and it remains a bright spot for the chip maker going forward. Data Center revenues soared 31% year over year to $3.83B due to strong adoption of Nvidia’s server solutions by corporate clients. Nvidia also secured a big win in November by entering into a multi-year agreement with software company Microsoft (MSFT) to build a new supercomputer. Microsoft’s Azure will be the “first public cloud to incorporate NVIDIA’s advanced AI stack” which would further enhance Nvidia’s position as a leader of full stack artificial intelligence applications.

The PC market decline is in a cyclical decline and it is a problem for Nvidia

The GPU demand surge in FY 2021 resulted in record prices for graphic cards which helped Nvidia report record financial results as well. However, the PC market has seen a significant slowdown this year and it is driving a normalization in Nvidia’s Gaming business. Consumers upgraded their PC equipment during the pandemic to prepare for remote working and studying, but now demand for new PC shipments is dropping off sharply.

Consulting firm Gartner recently estimated that global shipments of PCs declined 19.5% in the third-quarter which marked an acceleration of the market’s decline: in the second-quarter, Gartner calculated a decline in global PC shipments of 12.6%. Intel also heavily down-graded its forecast for the last quarter of the year due to the forcefulness of the down-turn, indicating that the market has not yet bottomed… and this means that Nvidia’s top line will continue to be at risk in the next two or three quarters.

Nvidia’s outlook for FQ4’23

The outlook for the current fiscal quarter is not great either. The chip maker said it sees revenues of $6.0B, plus or minus 2% while its non-GAAP gross margin is expected to be 66%, plus or minus 50 basis points. Based off of Nvidia’s guidance, the chip maker could actually see a quarter over quarter increase of up to 3%.

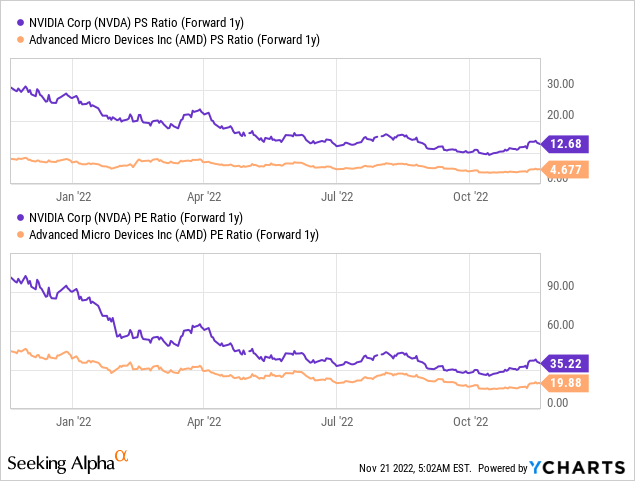

Nvidia’s valuation

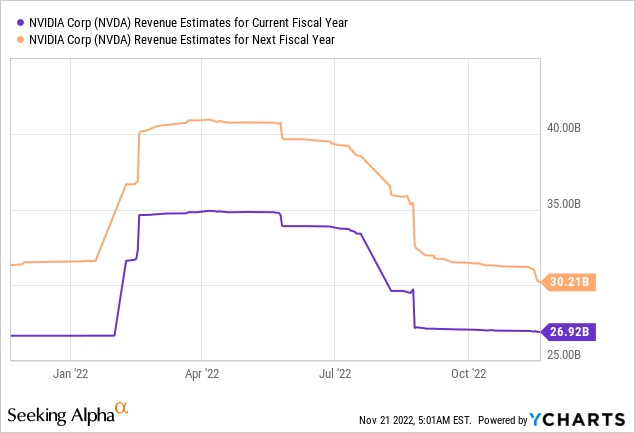

Nvidia’s revenue estimates for this year and next year have started to drop sharply after the chip maker issued a profit warning last quarter. The expectation is now for 0% revenue growth this year and only 12% in the following year.

I prefer AMD (AMD) over Nvidia right now due to AMD’s strong execution in the server market, strong product line-up with its new EPYC processors hitting the market soon and a more compelling valuation relative to Nvidia. AMD’s valuation is much more attractive than Nvidia’s based off of P/S and P/E…

Risks with Nvidia

The most obvious commercial risk for Nvidia is a continual slowdown in the Gaming business which has already been responsible for driving a painful revaluation of Nvidia’s shares to the down-side this year. Should the PC market continue to decelerate, then chip makers will continue to be faced with weakening demand in their consumer-facing businesses. A down-trend in estimates also poses a risk for companies like Nvidia.

Final thoughts

Nvidia’s FQ3’23 results were expectedly not great and the outlook for FQ4’23 could have been worse. But that doesn’t mean that Nvidia is a buy. I believe the PC market will likely remain weak for the foreseeable future as the downturn accelerated in the third-quarter and high inventory levels continue to pose a risk to product pricing. While I like Nvidia’s product portfolio, momentum in Data Centers and recently announced collaboration with Microsoft, I believe shares of Nvidia are going to re-test their lows around $108 in the coming months. Weakening sector fundamentals and a light outlook for FQ4’23 strongly indicate that things could get worse for Nvidia before they get better!

Be the first to comment