Justin Sullivan

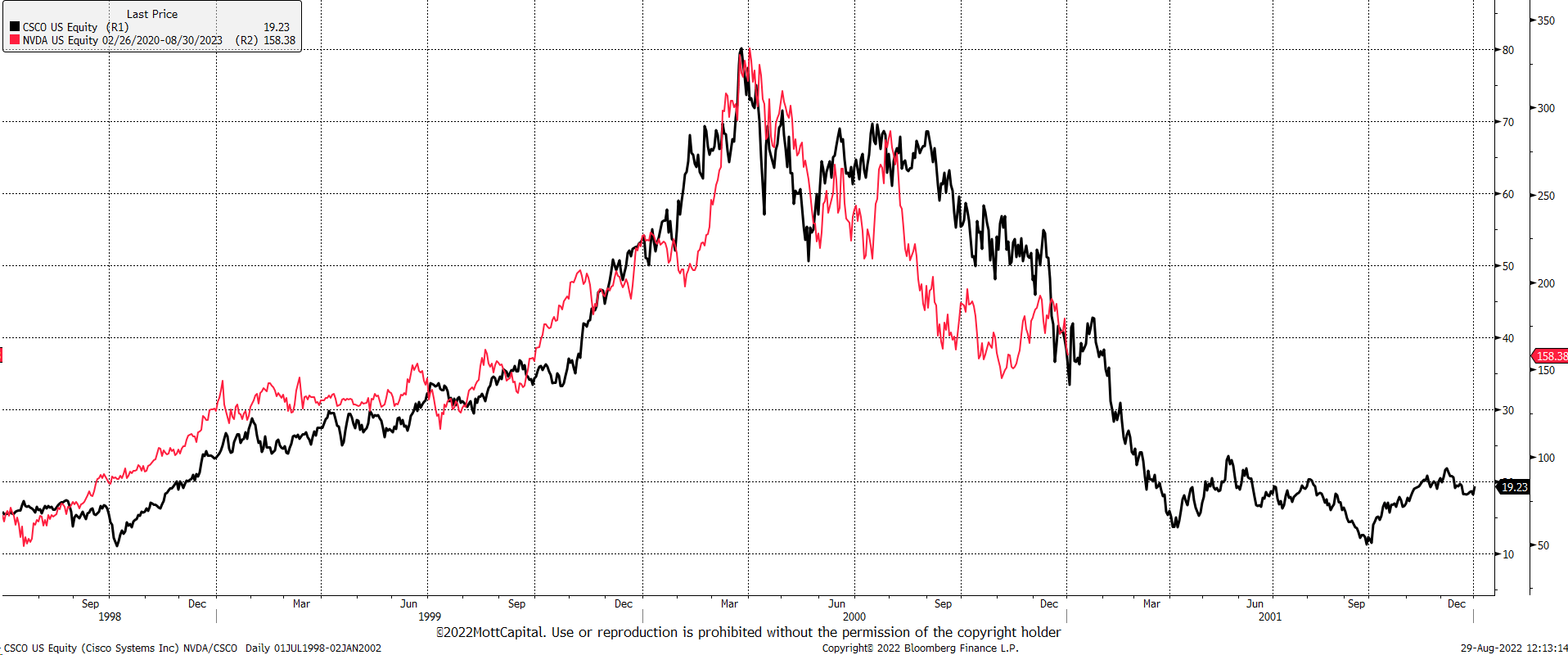

The similarities between Nvidia (NASDAQ:NVDA) of today and Cisco (CSCO) of 2000 continue. The analogs between the two companies, separated by more than 20 years, are remarkable and have continued since I first pointed them out in December 2021.

Terrible Results Pave The Way

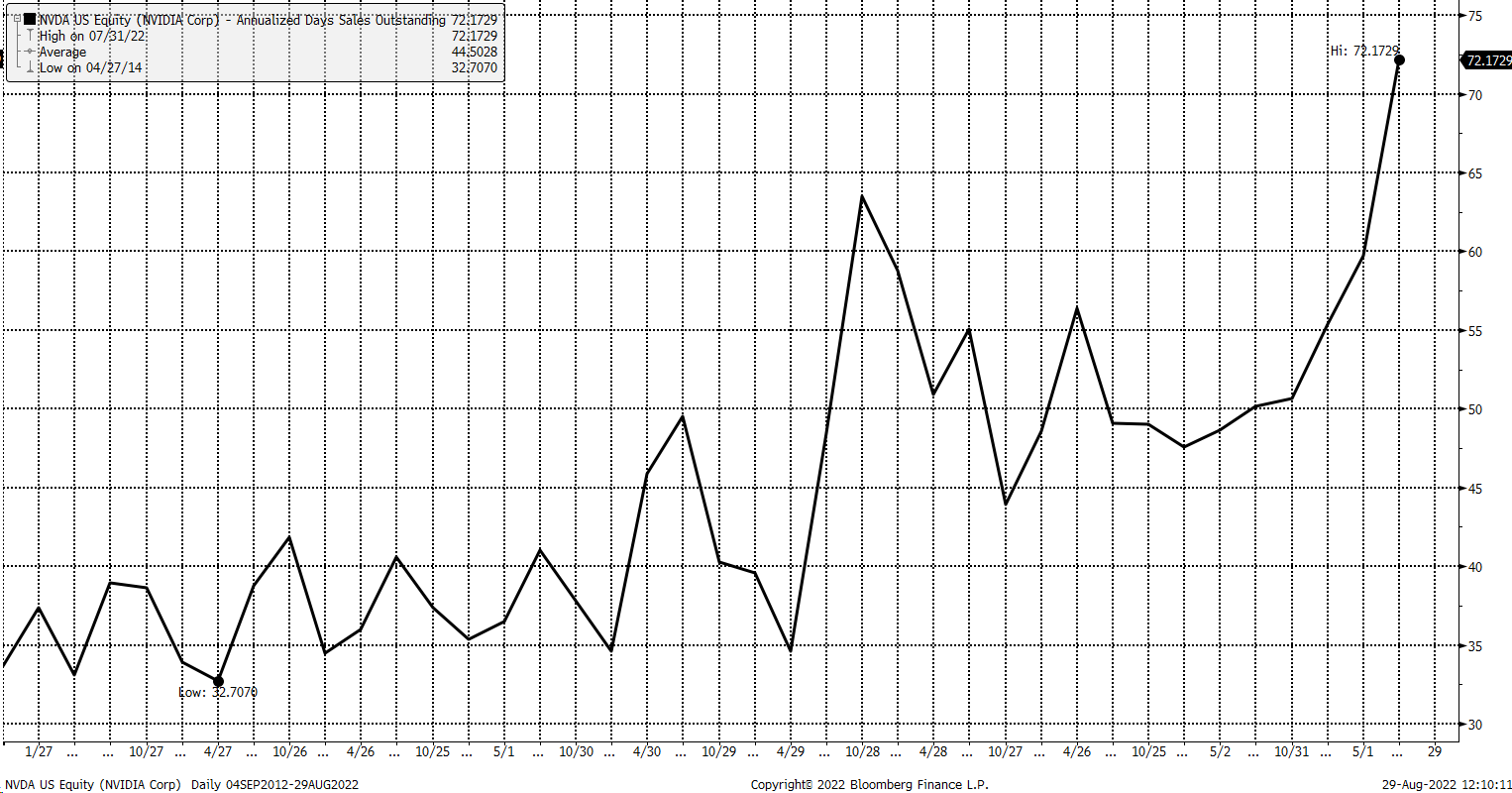

Nvidia’s horrible fiscal second quarter results and third quarter guidance were jaw dropping, and perhaps the only aspect more shocking was that the stock went up the next day. The company already had pre-announced fiscal second quarter results, so there was no surprise. But the surprisingly weak receivable days were eye-popping outside of the horrible sales guidance. Receivable days were up to 72.2, much higher than expectations of 53.7, and the highest number of receivable days in a decade.

Bloomberg

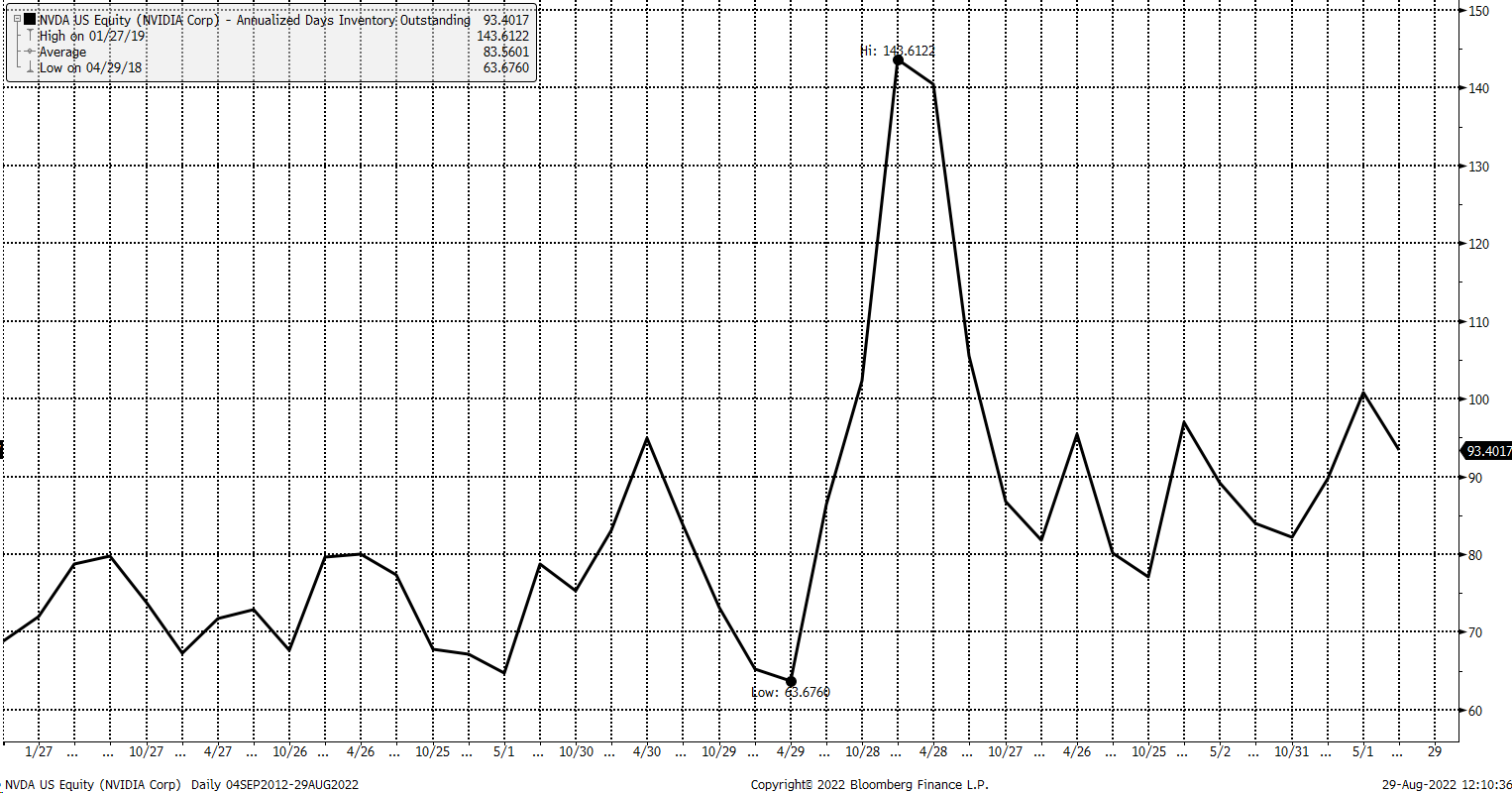

Additionally, the days inventory outstanding remains at elevated levels around 93.40. That was expected and down slightly vs. last quarter, but receivable and inventory outstanding are both historically very high numbers and are certainly not seen during the “good times.”

Bloomberg

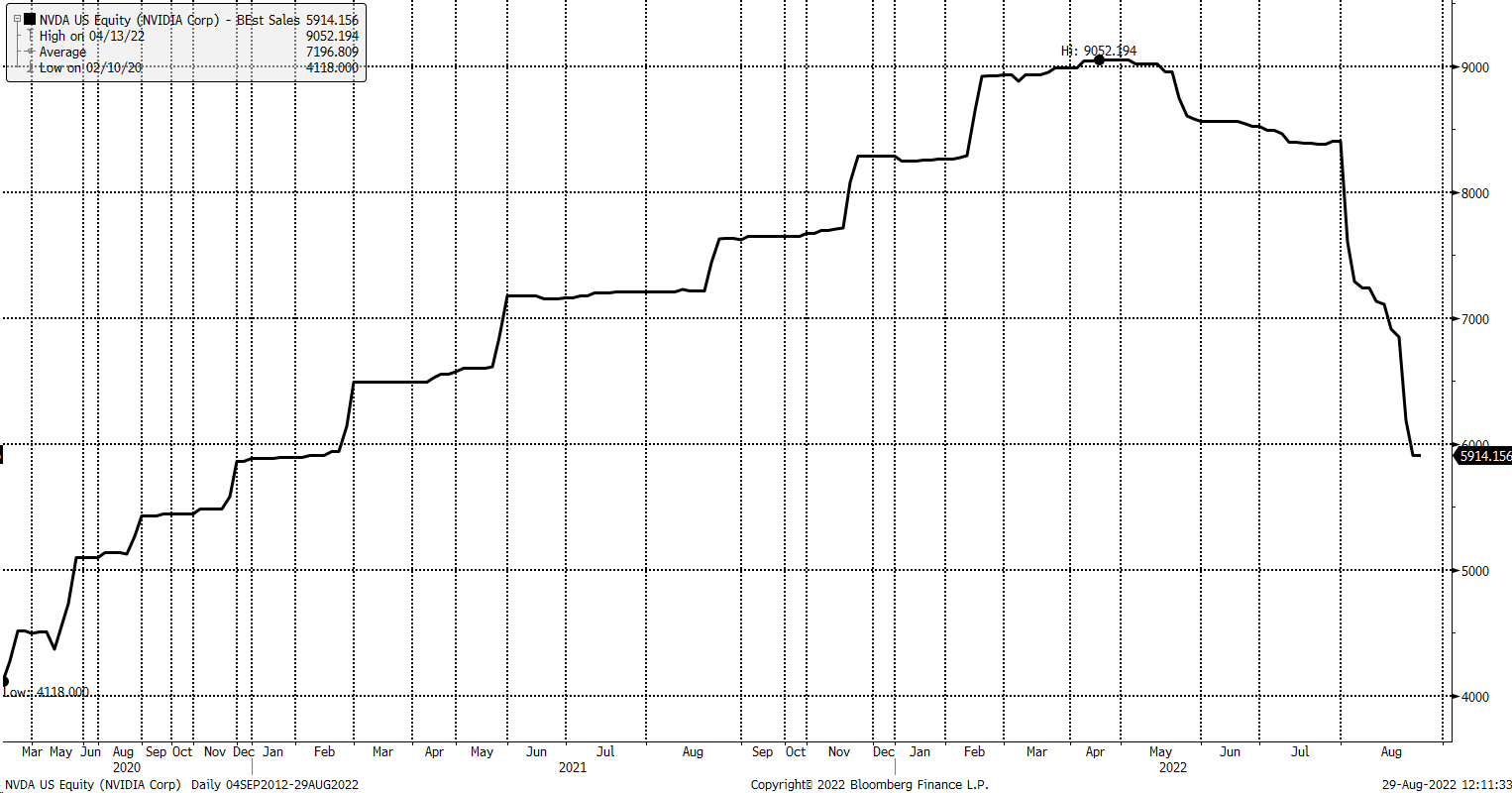

There are few words to describe how bad the sales guidance was at $5.9 billion, nearly 15% below analysts’ consensus estimates of roughly $6.9 billion. The third quarter estimates were down from around $9.0 billion in mid April. That pushed full-year revenue estimates down to $27.2 billion from a peak of $34.9 billion, a massive decline in estimates. Analysts now see sales growing by 1.2% in fiscal 2023.

Bloomberg

Due to the weak sales estimates and growth, earnings are forecast to decline in 2023 by 20.6% to $3.53 per share. Analysts see revenue bouncing back next year, climbing to around 13.9% to $31 billion, boosting earnings by 29% to $4.56.

But at this point, there may be more questions than answers, and given how much inventory the company is carrying and how long it takes for Nvidia to get paid, the outlook for next year may not be too rosy. If one thing is sure, uncertainty is much higher today than it was 90 days ago. This means that even though the stock has fallen materially in 2022, the stock is probably nowhere near cheap, trading with a PE of nearly 35.

Nvidia is cheaper today than it was at the end of 2021. However, with a historical PE average of 26.8, and with all of the questions. It seems more appropriate for the stock to trade with a comparable multiple to that seen in 2018, the last time the company struggled, which was below 20.

Bloomberg

For the stock to trade at 20 times earnings, Nvidia would be worth $91.20 per share. A steep discount to the current price of roughly $159 on Aug. 29.

Cisco’s Revenue Plunged Too

Sounds crazy, sure, but as I have pointed out on a few occasions, the stock is following a very similar path to Cisco in late 2000 from a technical and now fundamental standpoint.

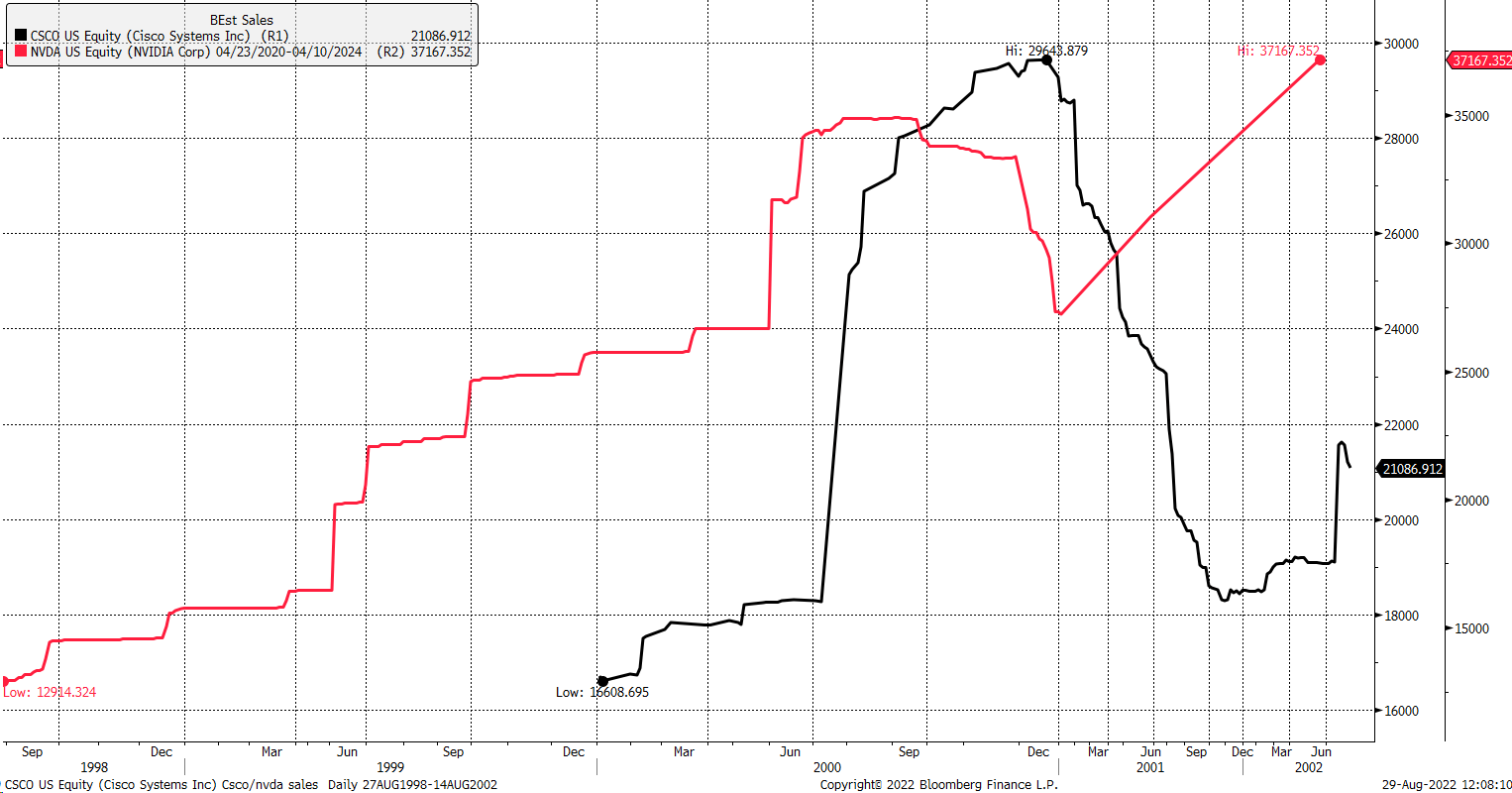

The last time I focused on this was April, when I noted that the stock might take a profound turn for the worst. At the time, the bulls were relatively straightforward. They believed that Cisco’s biggest downfall was its revenue plunging in 2000, ultimately leading to a significant share decline and that Nvidia was positioned very differently with expectations for strong revenue growth.

Fast forward a few months later, and suddenly Nvidia’s sales estimates are sharply declining, just like Cisco in 2000. The one difference at this point in the equation is that analysts still believe that Nvidia’s sales will recover during the next two years. In 2000 it’s clear that Cisco’s sales didn’t recover for a long time. Maybe Nvidia’s sales will recover and not follow Cisco’s path. After all, it’s a different time, but it seems remarkable and should at least raise eyebrows.

Bloomberg

The Valuation Drop is Similar Too

Even from a valuation perspective, Nvidia has fallen like Cisco in 2000, with the price-to-sales ratio on a trailing twelve-month basis coming down sharply since peaking.

Bloomberg

Where Nvidia goes from here is not a pre-determined course and can undoubtedly shift and end up different than Cisco over the long term. It isn’t to say Nvidia’s stock will stagnate for the next 22 years like Cisco’s. But it’s worth noting that the similarities between the two stocks and fundamentals are jaw dropping.

Bloomberg

Based on the path of Cisco in 2000, the next major turn in Nvidia could occur over the next 30 days and is, at the very least worth thinking very hard about. If 30 days come and go and Nvidia’s shares are sharply higher, then the good news is that Nvidia may have a different fate than Cisco, and the similarities end with it.

Be the first to comment