NATTAWUT SAKIT/iStock via Getty Images

Introduction

It’s time to talk about fertilizers. In this case, we’ll discuss the Canadian fertilizer giant Nutrien Ltd. (NYSE:NTR), known for its massive potash exposure. The company has been one of the biggest winners since the pandemic bottom of 2020 as a result of tight fertilizer supply, rebounding demand, and (related) great pricing. Now, the stock is down roughly 37% from its 2022 high at $117. Prices are lower as a result of subdued energy prices, rising supply, and investors shifting their focus a bit from value to growth as the Fed is expected to pivot.

However, I not only remain bullish but believe that NTR shares are due for a substantial rally. Fertilizer supply isn’t easing as much as the market might think. Meanwhile, demand is rebounding, and energy prices are far from back to normal.

I reiterate my bullish call on Nutrien and consider buying rather aggressively, despite having an already large position in agriculture and energy.

So, let’s dive into the details!

Fertilizers Are Hit By Weakness

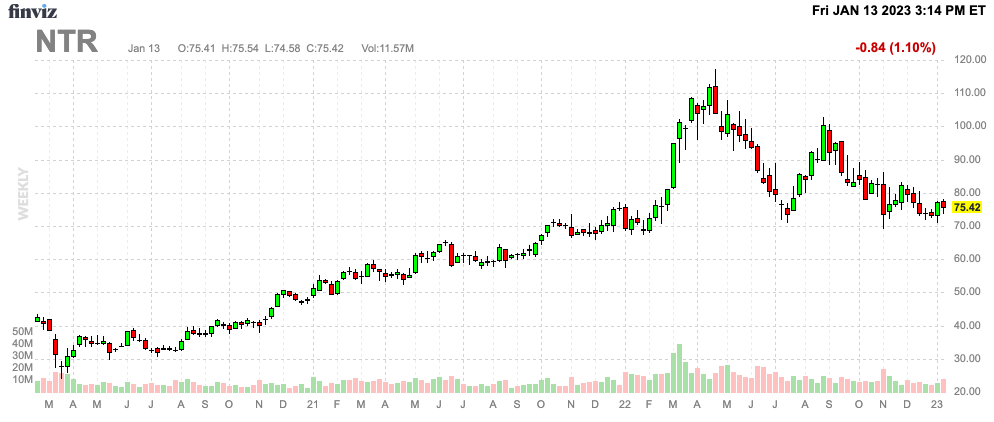

Nutrien is trading 37% below its 52-week high while I am writing this. This is the first downtrend since the end of the first wave of lockdowns in 2020.

FINVIZ

Nutrien, which is the world’s largest producer of potash, and the largest producer of nitrogen fertilizer, is adjusting to changing fundamentals.

As the chart above shows, the company did extremely well in early 2022 – after doubling in 2021. As everyone knows by now, the February invasion of Ukraine caused agriculture and energy prices to explode. Russia and Belarus (its ally) have a huge footprint in the global fertilizer industry.

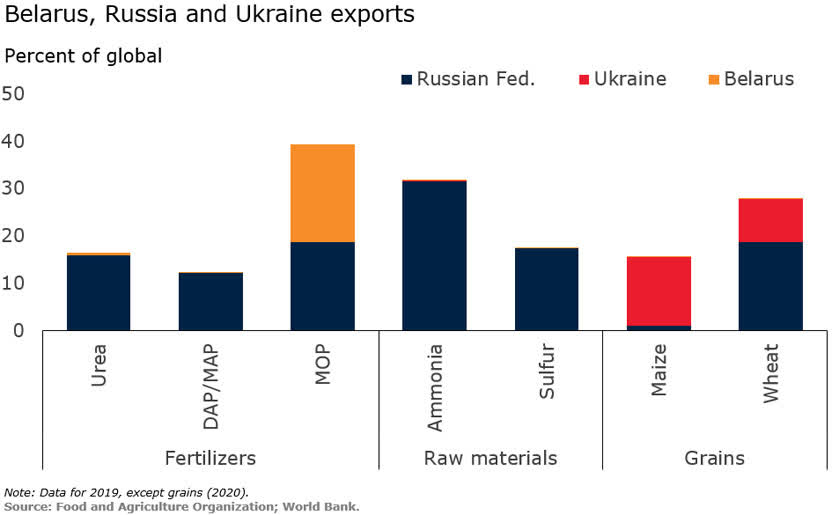

As the graph below shows, the two nations supplied roughly 15% of urea (nitrogen fertilizers), more than 10% of DAP/MAP (phosphates), and 40% of MOP (that’s potash).

FAO, World Bank

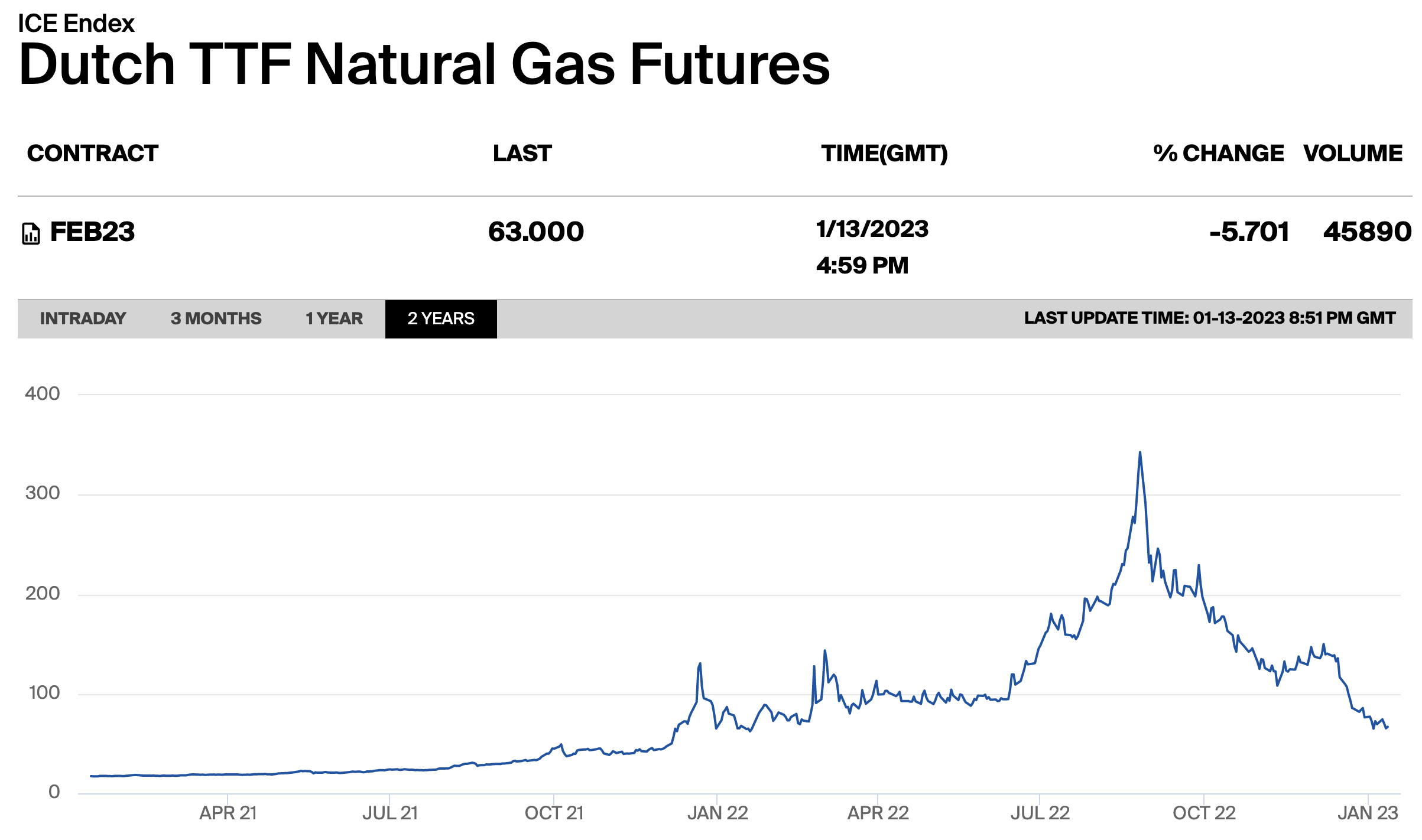

Moreover, Russia cut natural gas flows to Europe, causing a massive imbalance in global supply and demand.

The graph below shows that a mild winter and an end of panic-buying have caused European benchmark natural gas futures to plummet.

Intercontinental Exchange

While natural gas isn’t a driver of potash, it is driving nitrogen prices and overall investor sentiment in the industry. In the first three quarters, Nutrien generated roughly a third of its sales from nitrogen fertilizers.

This is what the comparison between Nutrien and natural gas looks like. In this case, I went with North American Henry Hub futures.

TradingView (NTR, Henry Hub)

Now, the question is whether this downtrend is sustainable. Are we going back to normal in agriculture? Are the energy and agriculture bull markets over?

I don’t think so.

The Fertilizer Bull Case Continues

In November, Nutrien’s President and CEO Ken Seitz said the following:

And our confidence in the outlook for the fundamentals of our business has not changed. Global grain supply remains very tight, with the stocks to use ratio projected to fall to a more than quarter century low this crop year. High energy costs and export restrictions continue to impact global fertilizer production and trade, most notably in Europe.

And we believe these supply constraints will persist well beyond 2022.

Nutrien Ltd.

Essentially, the only thing that has changed since then is that natural gas prices have come down. This is mainly driven by lower-than-expected demand due to global recession fears and the fact that the Chinese economic reopening has been followed by a dramatic surge in COVID cases, hurting demand.

What the market is afraid of is a mix of lower demand and a rebound in supply due to potentially higher exports and lower natural gas prices, increasing production profitability of nitrogen fertilizers. Lower demand, in this case, is caused by farmers cutting back on fertilizers to somewhat offset the impact of rising prices on their farms. In 3Q22, Nutrien sold 6% less potash, as a result of weaker demand in North America.

As reported by Progressive Farmer in December:

Chris Lawson, head of fertilizers for CRU International Ltd., told DTN that much demand destruction has been done to the K market in 2022. It was thought when the war began in February 2022 that this was going to limit the supply of potash, as so much comes from the Black Sea region — so prices increased significantly.

However, the largest K producer in the world, Canada, responded with increased production. This increased Canadian production has helped to alleviate possible supply concerns, even with about 10 million metric tons annually from Russia and Belarus, he said.

In March 2022, Nutrien communicated its plans to improve production by 20% compared to 2020, which means that Potash is responsible for 70% of the added production during this period. The company is likely to have entered 2023 with an annualized production rate of 50 million tons.

Moreover, the company mentioned that it will be entering 2023 after a period of de-stocking, as a result of high prices. Now, these inventories need to be replenished while supply is still constrained.

So that again, heading into 2023, we’ve been through a destocking period, those inventories are going to need to be replenished. And they’re going to be need to be replenished in a market where the supply side continues to be constrained.

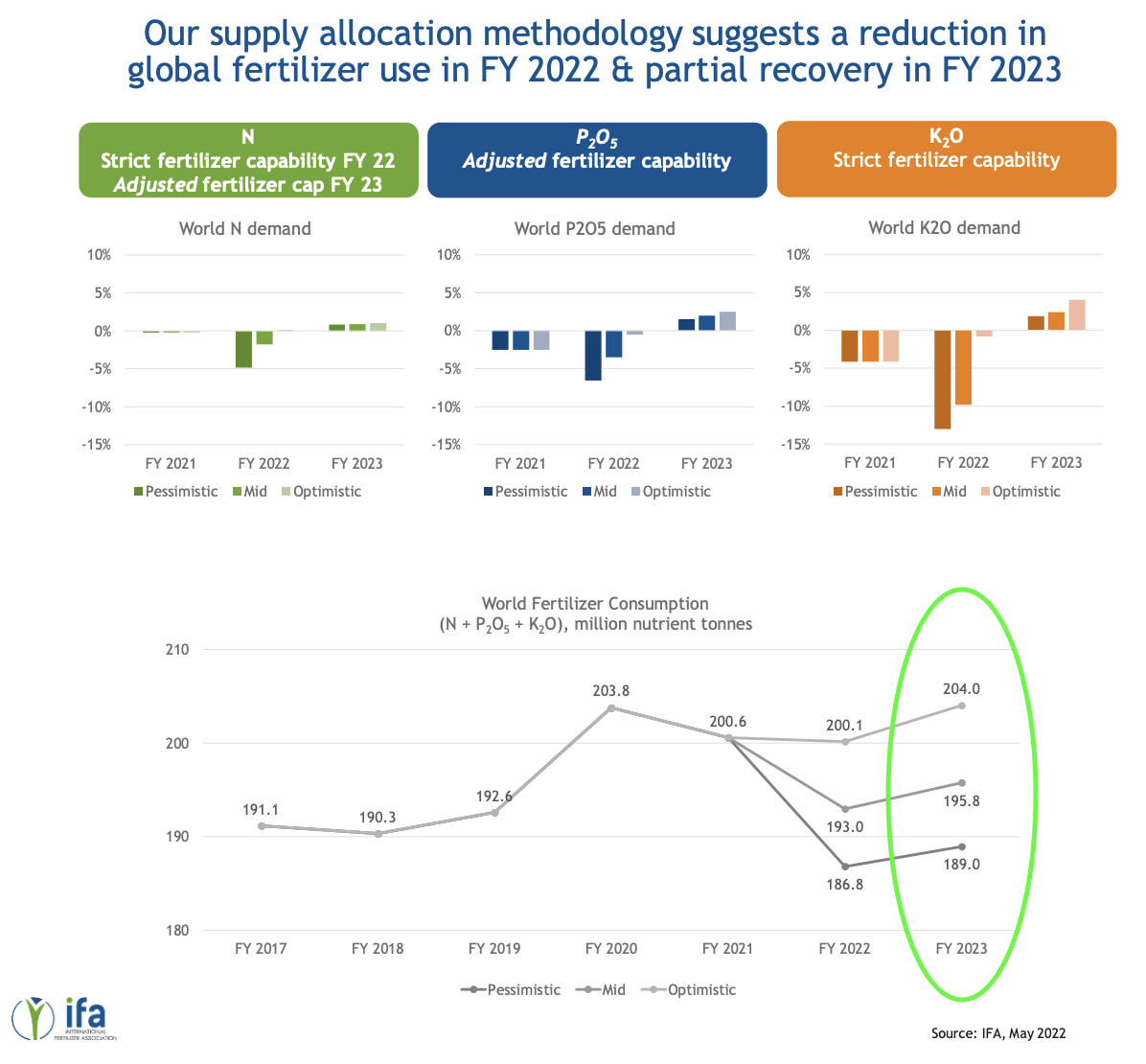

The International Fertilizer Association, which is legally prohibited from forecasting future output, looked into available capacity. That’s different from forecasting output, yet still valuable information. The association finds that potash capacity is the most constrained, followed by nitrogen and phosphates.

International Fertilizer Association

Whereas phosphate capacity is expected to rebound this year, potash is expected to remain constrained for at least three more years. Again, three more years is a huge deal in global agriculture, which relies on affordable and abundant fertilizers, as it has enough other problems to deal with (like drought and outperforming demand growth).

Moreover, demand for all three fertilizers is expected to rebound – even in a very pessimistic scenario. To understand the quote from the International Fertilizer Association below, please be aware that N stands for nitrogen. P stands for phosphates. K stands for potash.

In FY 2023, both the N and the P scenarios were adjusted to account for lower affordability, while the K scenario is expected to directly follow availability. This translates into a partial recovery for all three macronutrients in both the pessimistic and the mid scenarios, and a full recovery in the optimistic scenario.

International Fertilizer Association

With this in mind, Nutrien confirms this view as it sees heavily constrained supply in 2023 as well, which I believe the market is currently underestimating.

[…] the current situation is unique in that global potash supply remains constrained. Potash production and exports from Eastern Europe continue to be impacted by sanctions on Belarus, and restrictions on Russia that are related to the war in Ukraine. For 2023, we forecast exports from Belarus to be down 40% to 60% compared to 2021 levels, and Russian exports to be down 15% to 30%.

Global potash shipments are projected to be between 64 million to 67 million tons in 2023, which is up from 2022 but still well below our unconstrained demand forecasts of over 70 million tons.

Nitrogen Ltd.

Moreover, with natural gas prices being come down so much, I think the risk for nitrogen production profitability is to the downside, which could cause additional supply constraints, especially in the second half of 2023.

So, What About The Valuation?

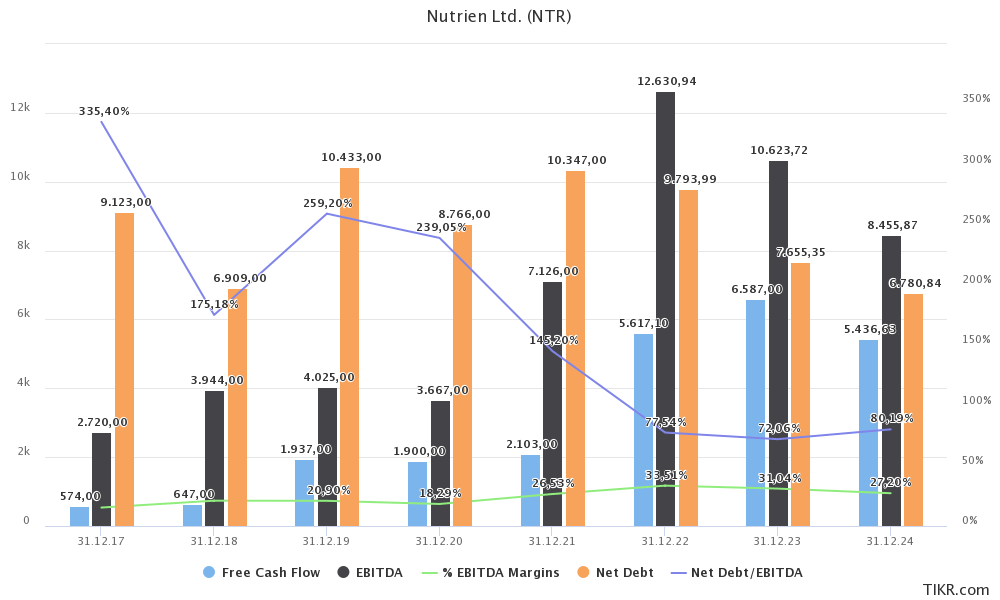

Looking at market estimates, we see that sell-side analysts expect financials to moderate. It’s hard to disagree with that, as the situation we had in 2022 is far from sustainable. However, continuing supply constraints are set to provide the company with:

- Strong multi-year EBITDA growth (compared to pre-pandemic levels).

- High margins, despite moderation. EBITDA margins are expected to remain above 27%.

- Net debt is expected to fall to less than $7.0 billion in 2024, which is less than 1.0x EBITDA.

- Free cash flow is expected to remain above $5.4 billion on a prolonged basis. This implies a free cash flow yield of almost 14%.

TIKR.com

These estimates are based on strong pricing and a production increase to at least 14 million tons of potash in 2023. Even nitrogen production is expected to rebound to 11.5 million tons (up to 12.0 million tons).

Nutrien Ltd.

Using 2023 and 2024 estimates (and $300 million in pension-related liabilities), the company is trading at 4.4x 2023E EBITDA and 5.4x 2024E EBITDA (incorporating moderating EBITDA and lower net debt).

This valuation remains too low as NTR shares historically trade close to 8x NTM EBITDA.

TIKR.com

On July 5, I wrote the following:

Using mid-cycle EBITDA, the company should be trading 15-20% higher than current prices. If we assume that the ongoing agriculture supply remains tight driven by high energy costs, I see at least a 40-50% upside over the next 12 months.

I believe that we’re seeing irrational selling at this point. However, it doesn’t mean we’re through. NTR could fall to $60 if energy continues its downtrend based on demand fears.

In the months after that article, NTR did rise by 37%. Now, the stock is back to where it was as a result of energy and other aforementioned factors.

I continue to believe that NTR should trade at $100 with more long-term upside.

Also, the company’s dividend yield has improved to 3.4% again, thanks to the stock price decline. I expect this dividend to continue its upwards trajectory, thanks to very high free cash flow (double-digit implied FCF yield) and low net debt.

Takeaway

In this article, I reiterated my bullish view on Canadian-based fertilizer giant Nutrien. While the company’s stock price hasn’t been doing so well lately, I believe that fears are overblown. As expected, the main driver of weakness was energy. These headwinds are fading now. Moreover, fertilizer supply is set to remain heavily constrained, which will maintain elevated prices. Nutrien benefits from that. In the case of NTR, it’s not just pricing but also higher volumes, that are set to maintain elevated EBITDA and free cash flow for years to come.

The valuation has not been adjusted to that. Hence, I believe that NTR remains attractively valued with a lot of upside potential in the year(s) ahead.

Hence, I’m looking to add some NTR shares to my trading portfolio in the weeks ahead.

(Dis)agree? Let me know in the comments!

Be the first to comment