Goodboy Picture Company/iStock via Getty Images

NuStar Energy (NYSE:NS) posts blow out earnings for the 4th quarter, reporting a record quarter with promise. It couldn’t have happened at a more needed time. At this point, the most important achievement that NuStar must accomplish is to pay off the Preferred D shares without increasing other debt nor cutting the dividend for the ordinary shares. So often in the investing world, the answers are “blowing in the” face of the forward winds of change approaching, with opportunities for those navigating through windshields rather than rear-view mirrors. The past can be valuable, but only when the rear whistles the same tune as the shield. Shall we turn our focus into its face and experience the cooling north winds from the hot summer afternoons? Put on the goggles and hat, take down the top and enjoy the breeze.

The 4th Quarter/2022 Year Result

We begin with a short review of the 4th Quarter. NuStar generated record 4th quarter EBITDA at $197 million, the bulk coming in transportation, pipelines. For the year, the company generated EBITDA of:

- $173 million for the first quarter of 2022.

- $175 million for the second quarter of 2022.

- $178 million for the third quarter of 2022.

- $197 million for the fourth quarter of 2022 (highest fourth quarter adjusted EBITDA in our company’s history).

- $725 million total, with management targeting $700-$740.

Also, management noted that the Permian handled a “record-breaking average of 584,000 barrels-per-day, that’s up 13% over the same quarter of last year.”

The company closed the year with a leverage ratio of 3.98 up from 3.79 in the 3rd quarter, but still below the company target of 4. The total debt now equals $3.3 billion. The revolver availability remains over $775 million. The total debt includes the $225 million added through extinguishing approximately one-third of the Preferred D shares in November.

Management notified investors of its 2023 EBITDA target, spreading out the range to $700-$760 million. It seems notable that $790 million is the four-quarter expansion of the 4th quarter result. Capital expenditures also were announced at $130-$150, unchanged from the 2022.

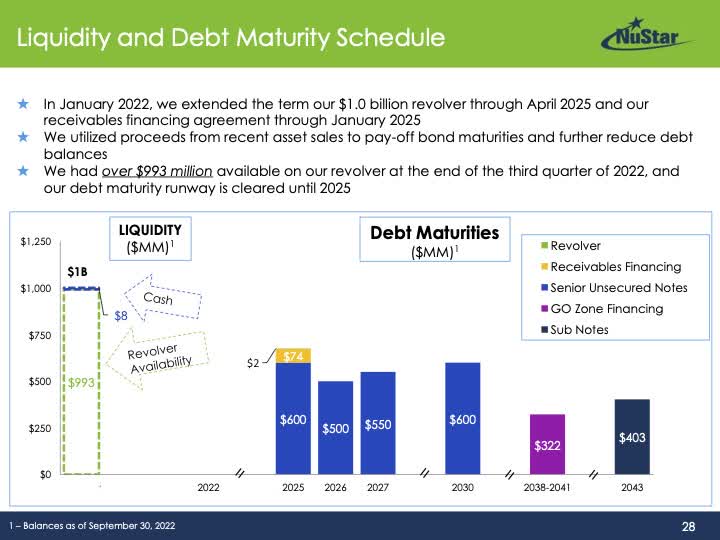

The Debt Structure

NuStar has had to pay unprecedented attention to its balance sheet, with several issues of preferred stock still on the books. The preferred D, the most egregious with interest rates above 12%, must be extinguished before the company can really move forward with dividend growth. Noted above, NuStar has $3.3 billion in debt. We included a slide from the last presentation outlining the debt and its structure.

NuStar Wells

The slide lacks the $225 million now added to the revolver. The company has time to pay down the D issue before any significant refinancing of debt comes due. The question, discussed in several articles, will the company have the cash to do so without breaking the critical leverage level? For investors, the key markers can be assessed by following total debt and in particular the amount of the revolver at the end of each quarter.

Future Plans, Market Health & Estimates

Management reaffirmed its plans to null-out the “Series-D units in 2023 and 24, which is about two years ahead of our original schedule.” This is the single most critical target while still investing a measurable level of capital.

When asked about the state of the business particularly the Permian, Danny Oliver, manager of EVP, Business Development & Engineering, answered:

It’s kind of the same story we had last year. We’ve forecasted some growth in the Permian, although it’s a little bit lower growth rate than we saw in ’22, but if our producers are more active than what we have forecasted, we could see some growth there.”

Oliver, also, noted that the inflation will dampen EBITDA growth in the Permian. Again, our take on performance is a wait and see, though it won’t be negative.

With respect to Corpus Christi Crude System, “we have forecasted at the MVC levels and so there’s really no downside there, but we could — we could see some upside if we see volumes start to pick up, which we’ve actually seen some at least in January.” In January, volumes averaged near 400,000 per day up almost 10% from the December quarter average.

Finally, continued strength in the West Coast assets is expected, with it likely being higher than forecasted.

When asked the effects from expected longer shutdown plans in the refining industry for 2023, management answered that it depends. Some shutdowns will actually increase volumes because of the nature of the transpiration network, while others will reduce volumes. All in all, management expressed its belief that this higher level of shutdowns might in the end be a wash.

An overall statement from management on growth hints that it continues at increased rates. Brad Barron, CEO, opined: “By systematically scrutinizing every dollar of spending, we have been able to significantly increase our cash flow with systematic changes that will continue to reap benefits in 2023 and beyond,”

Our sense is that the EBITDA range of $700-$760 million is on the conservative side. The four-quarter expansion of the 4th quarter results places EBITDA closer to $800 million.

Cash Flow

With enough cash flow paramount, a simple test exists for investors to watch, changes in total debt coupled with watching the revolver. A simple evaluation of cash flow involves an expansion of the coverage ratio for the December quarter. During December, the DCF equaled $90 million, with a ratio of 2. A four-quarter estimate equals $180 million, an amount within a reasonable range to cover almost all if not all of the revolver.

What We Continue to Do

We continue our practice of receiving distributions while selling covered calls. The stock price is showing higher lows during the past few months, a sign that investors are reacting positively to improvements. We have moved our strike prices up to $17.5 and plan to move up to $20 in June when our next set expires. And obviously, we collect the $0.40 dividend quarterly.

Risks

NuStar’s business can and will be affected negatively if a severe recession occurs. If this were to happen, it would be at an extremely inopportune time. It is critical that NuStar finishes the repurchase of its Preferred D shares with the interest rate so egregious. But, even if a recession occurs, demand for petroleum products across the world remains robust and tight. The U. S. is in a pivot spot with a significant cost advantage should U. S. demand falter significantly. We don’t see a scenario other than the extreme shutdown in 2020 that could materially stop NuStar’s progress. In our view, buying on weakness should be in the minds of investors. The cool wind in our face tempers the afternoon heat.

Be the first to comment