JacobH

Novonix Limited (NASDAQ:NVX) (OTCQX:NVNXF) is an Australia-based battery technology company that’s also trying to become a synthetic graphite producer. It aims to become the first producer of North American-made synthetic graphite to supply the booming and strategically important Anode Material Market.

The company has taken some major steps in that aim and has attracted a lot of attention in doing so. It has locked-down a sizeable investment from a key input supplier, signed an agreement with what will certainly become a major customer, and has been selected to receive a large grant from the US Department of Energy (‘DOE’). On the surface, this stock, which is down over 70% in the last year, may look like a bargain, but issues have cropped up over the last few months that may give investors pause. In this article, we’ll review those issues and discuss the long-term prospects for Novonix’s stock.

Company Background

Novonix’s two primary business lines are its Battery Technology Solutions Division and its Anode Materials Division. The Battery Technology segment is based in Halifax, Canada and makes lithium-ion battery cell test equipment used by battery manufacturers such as Panasonic and CATL. It’s where all of the company’s current revenue comes from, however, those amounts are certainly nothing to write home about.

Novonix’s customer cash receipts for Q2, which ended on Dec 31 (the company uses a Jul-Jun fiscal year), amounted to only $2.2 million while customer cash receipts for the first six months of its fiscal year amounted to $4.1 million. Those numbers aren’t much different from the prior year when Q2 results also came in at $2.2 million and the six-month number was about $3.9 million. Battery Technology, therefore, barely showed any year-over-year growth.

Novonix lost money in both the prior fiscal year and is also losing money this fiscal year. Part of that is due to elevated R&D expenses, which came in at about $1 million last quarter, but a lot of it also has to do with high staff and admin costs which combine to about $9 million in Q2 alone.

However, the case that’s most often made for investing in Novonix is not centered on the Battery Technology Division but rather the growth that will eventually come from the Synthetic Graphite operations. That’s what initially attracted my attention to the stock and what many investors most likely believe will eventually bring in the big bucks.

Battery Anode Material

Novonix’s Anode Materials division is located in Chattanooga, Tennessee and is preparing to one day manufacture synthetic graphite Anode Materials to be used in the making of lithium-ion batteries. However, the company has yet to generate any revenue at all from the sale of synthetic graphite.

So far, Novonix has purchased a 400,000 square-foot facility in Chattanooga, which it has named Riverside, and is currently working to prepare the facility for the eventual start of production.

The company’s synthetic graphite intentions have certainly garnered a lot of attention. Phillips 66 (PSX), the world’s largest producer of petroleum-based needle coke, a key input for synthetic graphite, acquired a 16% stake in Novonix for $150 million in August 2021. And last January, the two companies signed a technology development agreement to jointly-develop the next generation of anode materials.

After the Phillips deal, Novonix went on to sign an exclusive agreement with Kore Power Inc., a US-based private company, to supply it with graphite anode material. Kore plans to build a battery cell production facility in Arizona and wants to begin commercial production in Q4 of 2024. The deal also saw Novonix take a 5% stake in Kore in exchange for cash and stock.

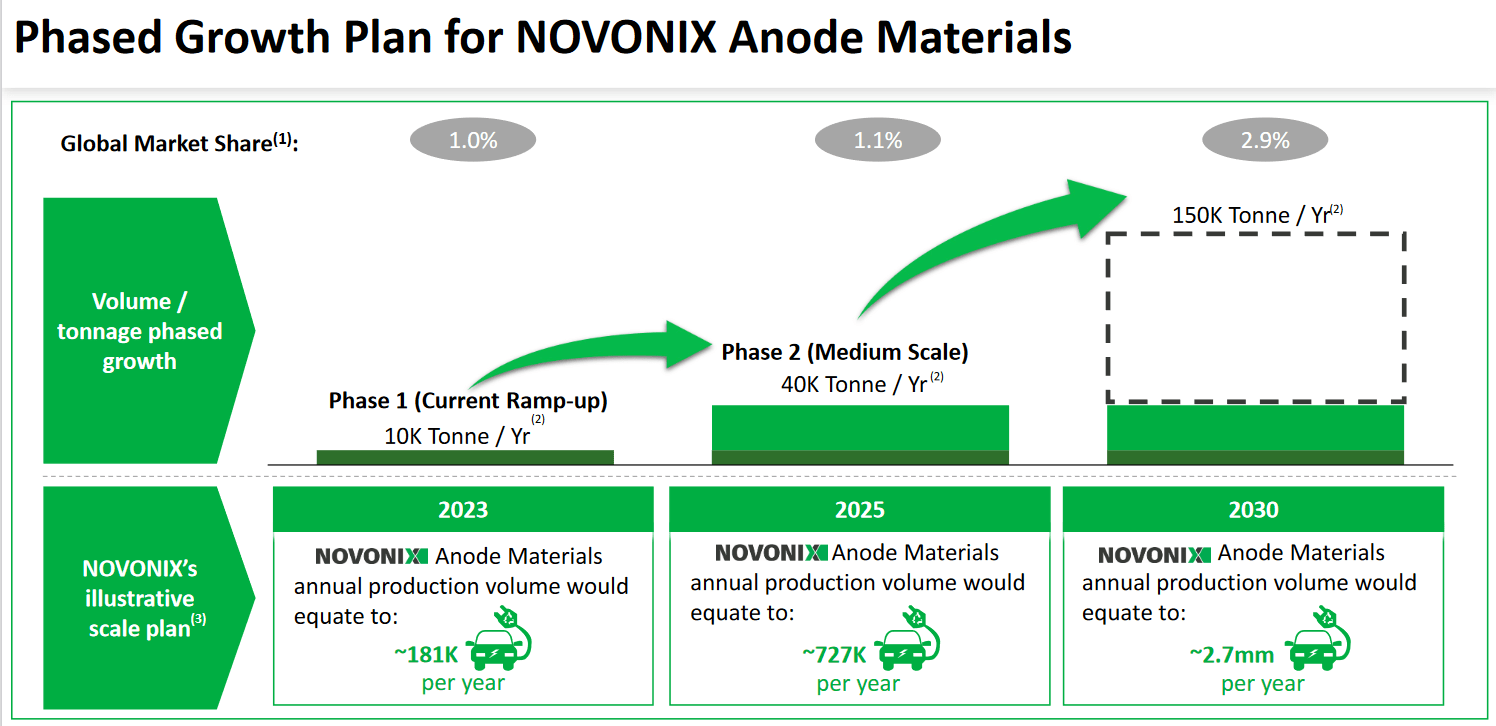

That occurred in January of last year, and at the time, Novonix had an ambitious timeline for when it wanted to start production. As can be seen in the exhibit below, the company was planning to begin production this year at a run rate of 10ktpa before gradually scaling up to 40ktpa by 2025 and be producing an impressive 150ktpa by 2030.

Investor Presentation

And the milestones kept coming. In October, the company announced that DOE had selected it to receive a US$150 million grant through the Bipartisan Infrastructure Law, part of the government’s efforts to expand the domestic production of battery materials. The funds will be used to build out the company’s synthetic graphite division.

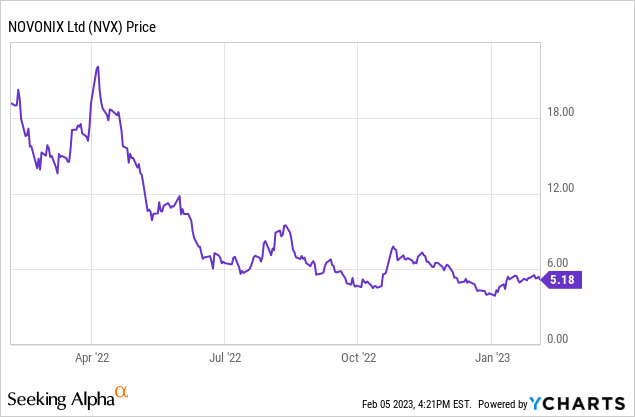

Things were going well for the company, so the sharp decline that its share price was experiencing may not have seemed warranted. The stock, which had been trading in the high teens at the beginning of the year, fell continuously throughout the Spring and Summer and since the end of last year has been trading in the $5 to $6 range.

Revised Schedule

However, at the end of last year the firm made an announcement that seemed to put this low valuation into context. Management announced that:

The Company plans to begin construction of a new production facility in 2023… plans to adjust the previous production output targets of Riverside from 10,000 tpa in 2023 to now match the KORE supply agreement volumes and any subsequent volumes from supply agreements the Company may enter.

And recall that commercial production at Kore will begin in Q4 2024, meaning that:

NOVONIX is expanding production of the Company’s Riverside facility in Chattanooga, TN to a target of 10,000 tpa output at full operation to support KORE’s requirement. This will begin at a rate of approximately 3,000 tpa in 2024 and ramp to approximately 12,000 tpa in 2028, to match KORE’s required volume.

What all of this means, is that instead of producing 40ktpa of synthetic graphite in 2025 and be approaching the 2030 targeted amount of 150ktpa by 2028 as was previously announced, Novonix will instead be producing a meager 12ktpa in 2028. Investors, who were expecting to see the production of 10ktpa this year, will now have to wait until Q4 of next year to see the first sales revenue from the Synthetic Graphite Division. That’s assuming everything goes according to plan, of course.

Takeaway

None of this has anything to do with Kore as it has always planned to start production in Q4 of next year; what has changed, however, is Novonix’s ability to sell its synthetic graphite. The fact that it has had to drastically cut forecasted production, “to now match the KORE supply agreement volumes and any subsequent volumes from supply agreements the Company may enter,” tells investors they haven’t been able to line up any additional customers for Riverside’s output. And bear in mind that this is at a time when auto OEMs are so desperate to secure battery material that car companies such as GM (GM) have begun investing directly into the mining sector.

If Novonix can’t get its graphite out the door now, then when? The battery materials boom and the elevated prices that come with it will not last forever. Already, competitors are positioning themselves to fill demand. Syrah Resources Limited (OTCPK:SYAAF) is gearing up production of natural graphite at its gigantic Balama property in Mozambique, and it has plans to begin producing Active Anode Material at its Louisiana facility this year.

Novonix needs to strike while the iron is hot, so until it can line up new customers for its product, the stock will be rated a Sell in my view.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment