Yagi Studio

Nordic Semiconductor (OTCPK:NDCVF) is a Norway-based company that we believe should be in more investors’ radars. It is a leading provider of wireless technology solutions, and it has been increasing revenue at an impressive pace.

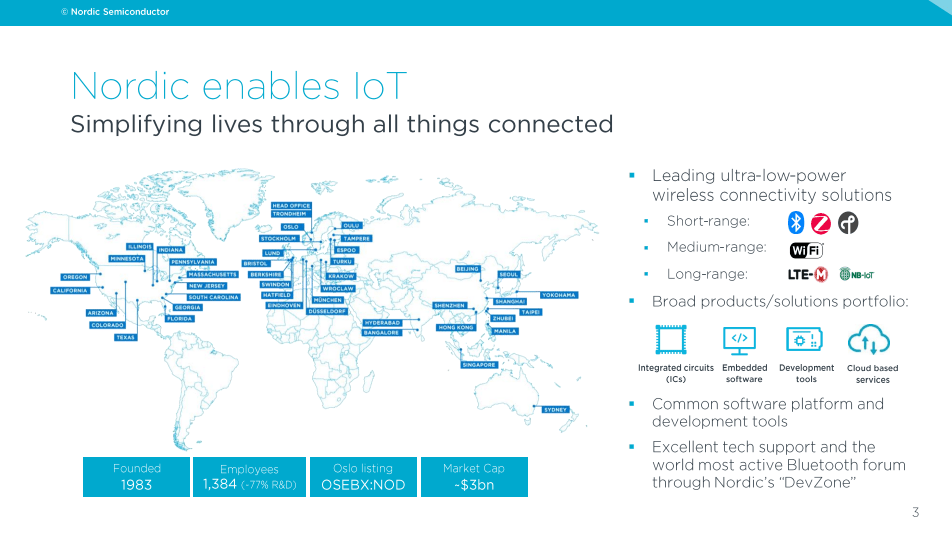

One of the key advantages of Nordic Semiconductor is its focus on low-power technology. The company has solutions that are both energy-efficient and cost-effective, making them ideal for use in a wide range of IoT applications. In particular, the company’s expertise in Bluetooth low energy technology has made it a leader in this segment. The slide below provides a good overview of the company.

Nordic Semiconductor Investor Presentation

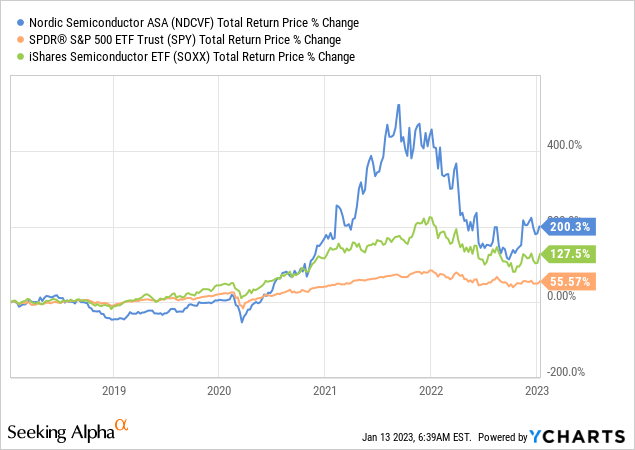

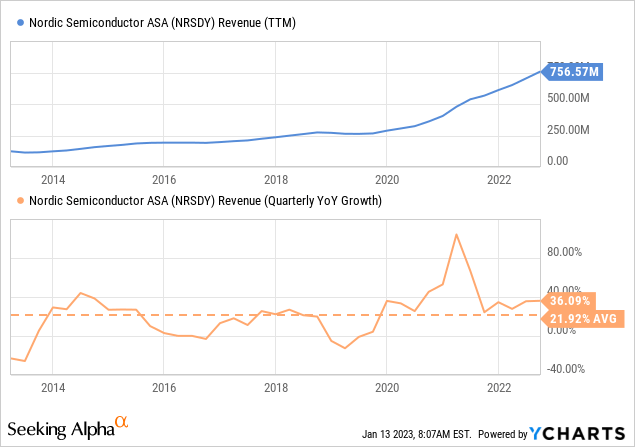

In the last five years, its shares have outperformed both the S&P 500 index (SPY) and the popular iShares Semiconductor ETF (SOXX) by a wide margin. This has been in part thanks to impressive revenue growth coming mostly from its Bluetooth low-energy product segment and quickly improving financials.

Financials

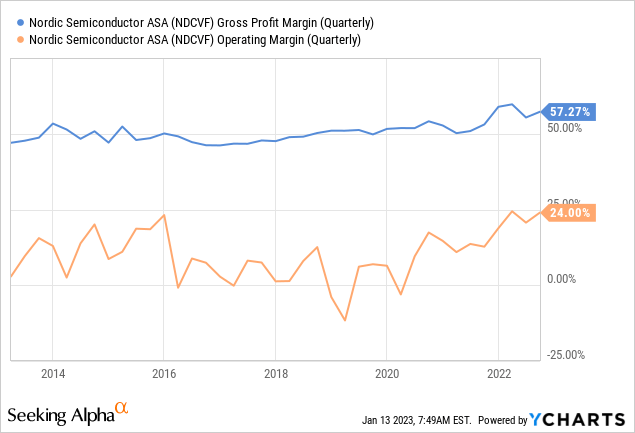

In addition to increasing revenue at a rapid pace, the company has been improving its profit margin at the same time. Gross profit margin is now a very healthy ~57%, while operating margin is around 24% thanks to operating leverage.

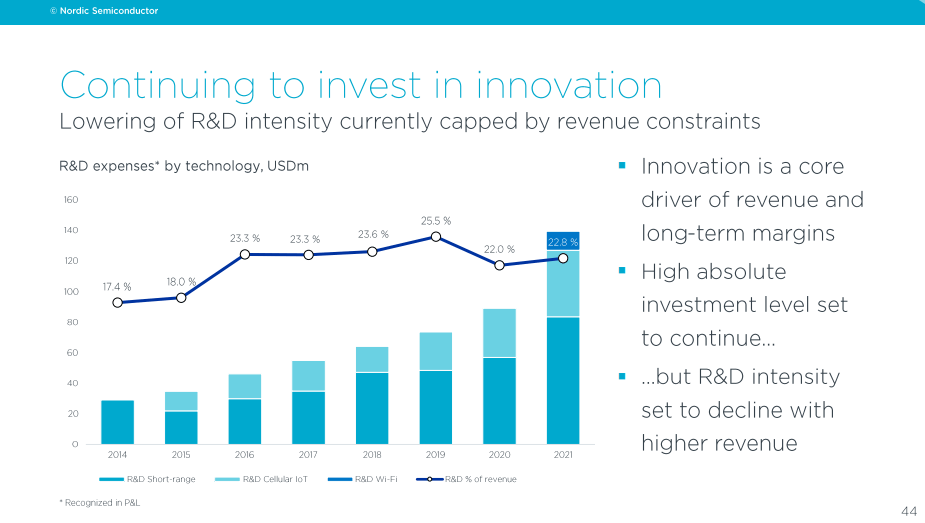

It is impressive to see that the company is profitable while delivering such high growth and investing heavily in R&D. As can be seen in the slide below, the company continues to increase its investment in research and development, even though as a percentage of revenue it is coming down a little bit.

Nordic Semiconductor Investor Presentation

Growth

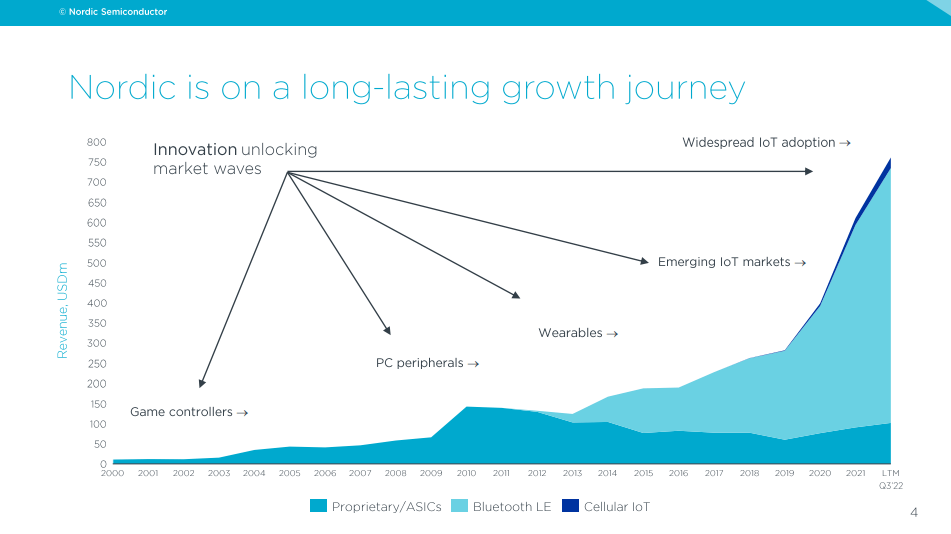

The company’s growth has come in waves, with the most recent one being wearables. Nordic believes its next growth phase will come from widespread IoT adoption. As can be seen in the slide below, a lot of the company’s revenue currently comes from Bluetooth low energy, but cellular technologies are starting to ramp up.

Nordic Semiconductor Investor Presentation

Growth has been very cyclical, at times even negative, but the company has still managed to deliver ~21% average quarterly revenue growth over the past ten years.

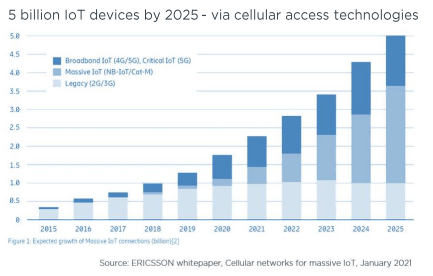

One of the reasons the company is very optimistic about its future growth is that the number of IoT devices connected via cellular access technologies is expected to increase significantly in the next few years.

Nordic Semiconductor Investor Presentation

The number of applications for the company’s products is increasing. It goes from traditional smart devices to things like asset tracking, payments, beacons, and hearing aids.

Nordic Semiconductor Investor Presentation

Competitors

The company has a large list of competitors, some of them very well capitalized large corporations including Broadcom (AVGO), Texas Instruments (TXN), and Qualcomm (QCOM), and other smaller players like Silicon Labs (SLAB) and STMicroelectronics (STM). The list is far from exhaustive, as there are too many competitors to name them all. Still, Nordic Semiconductor’s focus on high-quality devices, developer support, and low-power technology has allowed it to carve out a niche in the market.

Balance Sheet

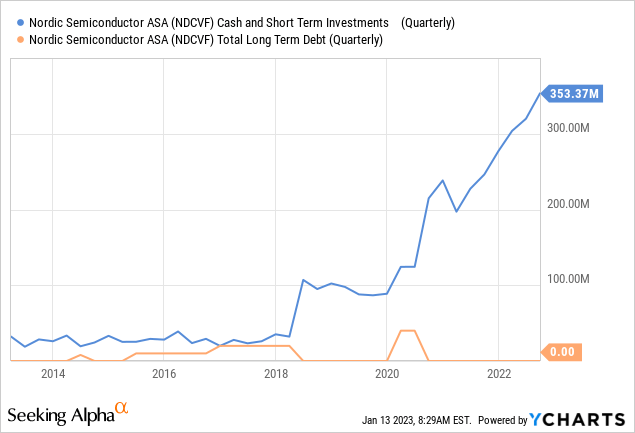

The company has a very solid balance sheet, with basically no long-term debt and a significant amount of cash and short-term investments.

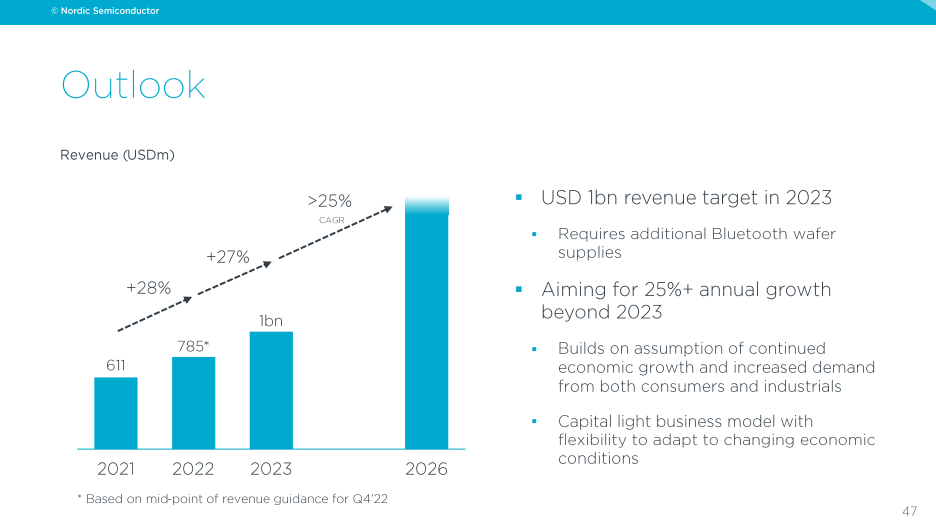

Guidance

Looking forward, the company has a $1 billion revenue target for 2023, and aims for 25%+ growth for the next few years. If the company proves too optimistic, the effect would be mitigated by its fabless/asset light business model.

Nordic Semiconductor Investor Presentation

Valuation

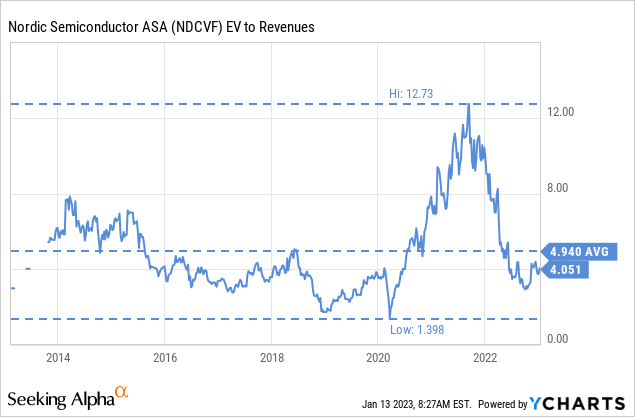

We believe shares are reasonably valued for a high-quality growth company. It is likely that if the company was US based it would have a higher valuation, but being based in Norway the number of investors following the company is more limited.

Despite the company now being much more profitable, the EV/Revenues is below its ten-year average of ~4.9x, at close to 4x.

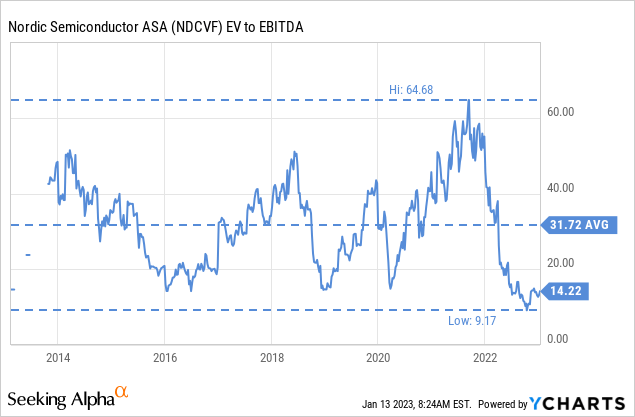

The EV/EBITDA is ~14x, which compares very favorably to the ten year average of ~31x.

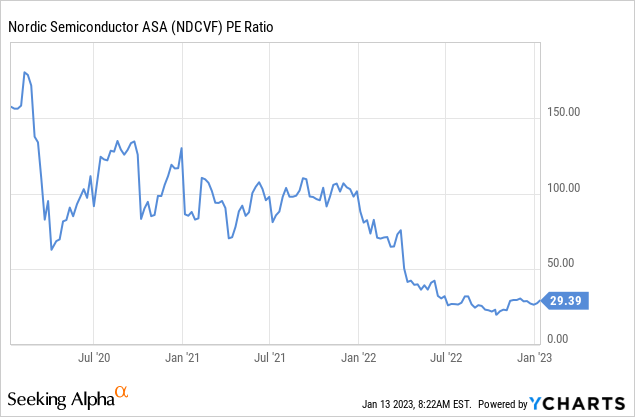

As the share price has come down and the company has significantly improved its profitability, the P/E ratio has quickly dropped from triple digits to ~29x. We would argue that for a company expected to grow revenue at a 25%+ a ~29x p/e is quite reasonable.

Risks

The main concern we have with Nordic Semiconductor is that it faces intense competition from other semiconductor companies, both in terms of technology and pricing. So far the company has been able to generate attractive profit margins, but we worry that should there be a price war in the industry it could erode the company’s profitability significantly.

Conclusion

Nordic Semiconductor is a very interesting company whose growth is leveraged on the growing popularity of Bluetooth devices, and other wireless technologies behind many IoT applications. The company is profitable, and it is growing revenues at an impressive rate. For these reasons, we believe the company deserves to be on investors’ radars. We believe shares are currently very reasonably valued for a quality growth company.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment