Kinwun/iStock via Getty Images

Elevator Pitch

Niu Technologies’ (NASDAQ:NIU) shares are rated as a Hold. NIU’s undemanding valuations have factored in the concerns about weaker-than-expected top line expansion for Niu Technologies in the short term to a large degree. But there aren’t any indicators of a shift in China’s pandemic policy or a weakening of lithium prices, which are the catalysts needed to drive a re-rating of NIU’s share price. Therefore, I have decided that a Hold rating is suitable for Niu Technologies.

Niu Technologies Overview

Started in 2014 and listed on Nasdaq in October 2018, NIU calls itself a company that “designs, manufactures and sells high-performance electric motorcycles, mopeds, bicycles and kick-scooters” in its media releases. In the company’s most recent fiscal 2021 20-F filing, NIU claims to be the pioneer of the “smart electric two-wheeled vehicle” category in China.

According to its Q2 2022 investor presentation slides, NIU boasts a network of 3,329 franchised stores in China as of June 30, 2022, and the company also sells its vehicles in 52 countries (apart from China) through distributors. In addition, Niu Technologies’ vehicles are available for purchase on its own e-commerce store and other third-party e-commerce platforms.

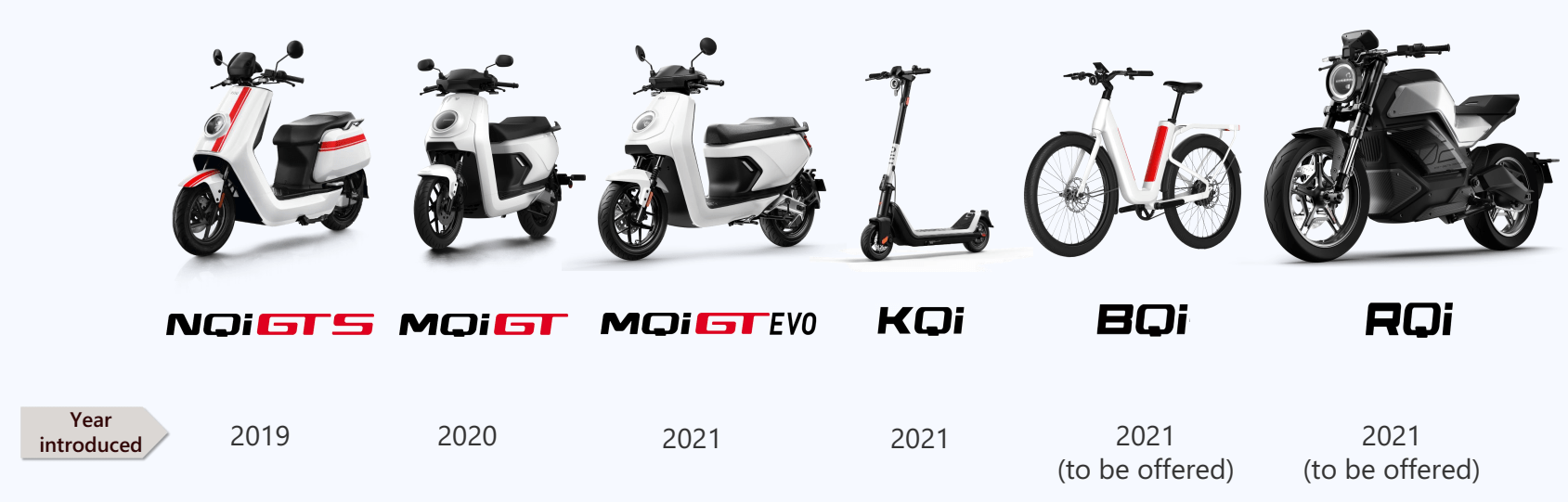

Niu Technologies’ series of vehicles is highlighted in the charts presented below.

NIU’s Vehicle Line-Up For The Chinese Market

NIU’s Q2 2022 Investor Presentation

Niu Technologies’ Vehicle Models Available For Sale In The Europe And The US

NIU’s Q2 2022 Investor Presentation

New Vehicle Models Launched By NIU In The Indonesian Market

NIU’s Q2 2022 Investor Presentation

Revenue Contraction In Recent Quarter Driven By Lockdowns In China

Niu Technologies’ top line decreased by -12% YoY to RMB828 million in the second quarter of 2022. This is worthy of note, as Q2 2022 represented the first time that NIU’s revenue contracted in the past nine quarters. Moreover, the company’s second-quarter sales turned out to be -43% below the sell-side’s consensus revenue estimate in USD terms.

Although NIU does distribute its vehicles in markets outside China, the Chinese market still contributed the vast majority or 85% of Niu Technologies’ FY 2021 top line as revealed in its 20-F filing. As such, COVID-19 lockdowns in Mainland China, which were at their worst in the second quarter of this year, were a significant drag on NIU’s most recent quarterly sales.

Moving forward, NIU should witness positive revenue expansion again in the second half of the current year, assuming that the analysts are right. Based on the market’s consensus financial forecasts taken from S&P Capital IQ, the sell-side sees Niu Technologies achieving top-line growth (in RMB terms) of +50% YoY and +58% YoY for Q3 2022 and Q4 2022, respectively.

However, the analysts could be too optimistic about the extent of sales recovery for NIU in 2H 2022, as I will touch on in the next section.

Uncertainty Over Near-Term Revenue Recovery

NIU stressed at the company’s Q2 2022 earnings briefing that “we remain cautious with the sales rebound in Q3 (2022) due to unclear COVID impact and temporary slowdown in retail sales introduced by the lithium-ion battery price hike.”

The prevailing view is that China will only make significant changes to its current COVID-zero policy next year. According to a recent September 23, 2022 Bloomberg news article, analysts from Goldman Sachs (GS) are of the opinion that the relaxation of COVID-19 restrictions in Mainland China is likely to only happen after “the Lunar New Year peak travel season (January-February 2023) and next March’s (2023) parliament session.”

In other words, there is a risk of recurring lockdowns in different parts of China between now and early 2023, which could disrupt Niu Technologies’ business operations. As an example, China’s Hainan experienced lockdowns in August 2022, and NIU acknowledged at its most recent quarterly results call that there was a “temporary impact on our sales” in Hainan which contributed 4% of the company’s FY 2021 revenue.

Separately, the increase in the cost of lithium-ion batteries has led Niu Technologies to raise its average selling prices of its scooters powered with lithium-ion batteries by +7% in the second quarter of this year.

It is reasonable to assume that certain price-sensitive consumers might opt for the less expensive scooters fueled by lead-acid batteries instead. In its FY 2021 20-F filing, NIU emphasized that it chose to compete in “the lithium-ion battery-powered electric two-wheeled vehicles market”, because lithium-ion batteries are “more ecofriendly”, “safer, lighter and more compact” than lead-acid batteries. This means that the rise in lithium-ion battery costs is negative for Niu Technologies’ revenue outlook in the short term given its focus on lithium-ion battery scooters.

The cost of lithium-ion batteries isn’t expected to ease anytime soon. An August 30, 2022 South China Morning Post article cited research from “London-based commodities consultancy CRU Group” which predicted that “lithium prices are expected to remain high at around US$65 to US$70 per kg till the first quarter of next year (2023).”

Niu Technologies’ recent share price performance suggests that investors are also unconvinced that NIU will be able to stage a very strong sales rebound in the latter half of the current year. Year-to-date in 2022, Niu Technologies’ stock price dropped by -72.5% which underperformed the S&P 500’s -23.8% correction by a substantial margin. NIU’s shares didn’t perform well in the recent one month as well, with its shares down by -25.4% versus a milder -9.9% pullback for the S&P 500.

In view of the significant drop in NIU’s shares, it is relevant to review the stock’s valuations which I highlight in the next section of the article.

NIU Stock Valuation

NIU’s current valuations are undemanding on an absolute basis and as compared to historical levels. The concerns regarding slower-than-expected revenue recovery for Niu Technologies have been adequately priced into its valuations.

A Comparison Of Niu Technologies’ Current Valuations With Historical Averages And Peaks

| Niu Technologies’ Valuation Multiples | Current Multiple As Of September 26, 2022 | Three-Year Historical Mean Multiple | Three-Year Historical Peak Multiple |

| Consensus Forward Next Twelve Months’ Enterprise Value-to-Revenue | 0.3 | 2.3 | 6.4 |

| Consensus Forward Next Twelve Months’ EV/EBITDA | 3.5 | 17.9 | 43.4 |

| Consensus Forward Next Twelve Months’ Normalized P/E | 8.7 | 35.0 | 96.1 |

Source: S&P Capital IQ

As per the chart presented above, the market values NIU at less than a third of its forward revenue, a low single-digit forward EV/EBITDA multiple, and a forward normalized P/E multiple below 10 times. Also, Niu Technologies’ current valuation multiples are significantly lower than its three-year historical mean and peak multiples.

Closing Thoughts

I assign a Hold investment rating to Niu Technologies. A Sell rating will be too harsh, as NIU’s valuation multiples are already very depressed. But a Buy rating isn’t warranted yet, as long as China sticks with its COVID-zero stance and lithium prices stay elevated.

Be the first to comment