Andy Feng/iStock Editorial via Getty Images

Late last week, one of the weaker names in the market was Chinese electric vehicle maker NIO (NYSE:NIO), after the company reported its first quarter results. Investors focused on weaker than expected guidance for Q2, but it was already known that the situation in China was going to pressure results for the period. The most important part of last week’s earnings report was management’s commentary on upcoming production plans, which showed that massive growth is finally about to come.

For Q1, revenues came in at $1.56 billion, which was up more than 24% year over year, and came in a little ahead of estimates. One of my main issues with NIO is that it usually reports results so late in the quarter that these numbers seem basically irrelevant, since we’re almost done with Q2 already. On the bottom line, non-GAAP earnings per ADS beat by three cents, but this is still a company that’s losing plenty of money at this time.

The main reason for shares dropping after Thursday’s report was the following headline – management guided to between $1.47 billion and $1.59 billion in revenues for the second quarter. Wall Street had anticipated second quarter revenue to reach $1.79 billion. Deliveries are expected to be in a range of 23,000 to 25,000, with even the high end of that being a sequential decline from Q1’s 25,768 units. As a reminder, Q2 is the first full quarter for deliveries of the ET7 sedan, which saw just 163 deliveries late in Q1.

I’m pretty much discounting this guidance miss, just because the analyst average seemed so ridiculous going into last week’s report. NIO had already reported its April and May delivery numbers, which were heavily pressured by China’s covid lockdowns. Even though we knew June would be better, supply chain issues are still a problem, so to think revenues were going to jump over $200 million sequentially seemed highly questionable. Management is basically guiding for a monthly record in terms of June vehicle deliveries, and yet it is still likely to fall a bit short of Q1’s quarterly total. I think analysts were just waiting to see what was reported and then adjust, but the result was a headline of very weak guidance.

NIO investors have been waiting for several quarters now to see production really ramp up. It has been over a year now since the company announced a new production agreement with its partner JAC to double factory output to 240,000 units a year. Still, though, the company hasn’t been able to report even 26,000 deliveries in a single quarter. The company is also in the process of building out its own facility called NeoPark. During the conference call, management provided this key update regarding production, with “F2” referring to NeoPark:

For the production capacity of our first plant with JAC-NIO, as we have mentioned, we will continue to ramp up its production capacity in Q3. I think probably at least in the second half of the year, our overall plant capacity should reach 20,000 units per month. It can be — it’s not probably too hard for us to see when.

And then for the F2’s ramp-up pace, actually, first, we will kick off the delivery of ET5 from this plant in Q3. So it will start production in Q3 and that we try to reach 10,000 units within quite a short period, probably three, four months. I think that’s our plan.

Of course, next year, as we introduce more models into this factory, the overall production volume of F2 will continue to rise.

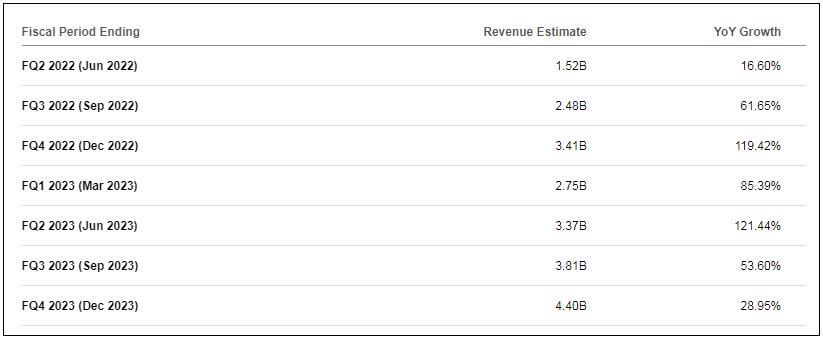

It remains to be seen how quickly NIO will actually reach these rates. As I’ve detailed in the past, the company’s growth timelines haven’t worked out as some may have hoped. All it takes is some more supply chain issues or another round of covid lockdowns, and these production rates won’t be seen until sometime in 2023. This kind of tremendous growth in units is expected to drive a major surge in NIO revenues, with analyst estimates shown below.

NIO Revenue Estimates (Seeking Alpha)

This significant expected revenue growth in the next 12-18 months is a main reason why the average price target on the street is double what NIO shares closed at on Friday. The valuation seems quite reasonable currently, with the stock going for 1.9 times expected 2023 sales, as opposed to fellow Chinese EV names like XPeng (XPEV) going for 2.1 times and Li Auto (LI) at 2.2 times. Of course, EV giant Tesla (TSLA) trades for over 6.2 times projected sales for next year, as investors are certainly willing to pay a lot more for that name.

In the end, NIO reported so-so results last week, but the more important thing is that production is about to really start ramping. Investors sold the stock because of guidance that was seen as weak, but covid shutdowns in China have been known for some time. The company is set to double or even triple its production in the coming few quarters, which should lead to a significant increase in revenues. That’s why the street is so bullish on this stock at the moment, but of course the company has to execute for shares to see that projected upside.

Be the first to comment