ChamilleWhite/iStock via Getty Images

Investment Thesis

It is evident that NIO Inc. (NYSE:NIO) will face a challenging YoY comparison from FQ2’22 onwards, given the massive impact of China’s ongoing Zero Covid Policy in Shanghai. The company would need to go above and beyond the impossible to achieve its delivery guidance of at least 23K vehicles in FQ2’22, given that Tesla (TSLA) had also struggled to reach pre-lockdown deliveries in May 2022. Given the complexity of auto supply chains, it is unlikely that NIO would be able to report an impressive YoY comparison in FQ2’22, thus suggesting a stagnant stock valuation and prices moving forward, if not a retracement. As a result, we would advise interested investors to wait and observe a little longer before adding more NIO stock to their portfolios.

Risk-averse investors would be well advised of NIO’s potential delisting from the NYSE stock market, though it is also apparent that a secondary listing in Singapore has been completed. The “unreliability” of investing in the Chinese stock market has to be considered as well, in the context of President Xi’s impending third-term reelection in November 2022, thereby potentially extending the intermittent lockdowns till then.

Nonetheless, despite the multiple uncertainties, we reiterate our stand since our previous analysis, that NIO remains a promising EV stock with an interesting battery swap concept. As one of the leading companies in China, the company stands to gain critical market share from Tesla in China, in the EU market, and potentially in the US market, upon its eventual entry in the future.

Therefore, NIO stock is highly suitable for speculative long-term investors, despite its current lack of profitability and the political uncertainty in China.

NIO Reported Slowing Revenue Growth And Sustained Un-Profitability

NIO Revenue and Gross Income

S&P Capital IQ

NIO reported revenues of $1.56B in FQ1’22, representing a YoY increase of 27.8%, though in line sequentially. The deceleration in revenue growth is partly attributed to supply chain production capacity for now, though we expect to see improvements by H2’22. However, it is also apparent that there is increasing pressure on its gross margins, given that the company reports YoY lower gross margin of 14.6% in FQ1’22 compared to 19.5% in FQ1’21. With rising battery and chip costs, we expect NIO’s gross margins to continue declining in FQ2’22 before potentially recovering once the price hikes kick in by FQ3’22.

In FQ1’22, NIO also delivered 25.7K vehicles for the quarter, representing in line sequentially and an exemplary increase of 37.6% YoY. NIO CEO William Bin Li said:

Despite the volatilities of the supply chain and the challenges in vehicle delivery resulting from the recent COVID-19 resurgence, we witnessed robust demand for our complementary products and achieved an all-time high order inflow in May 2022. (Seeking Alpha)

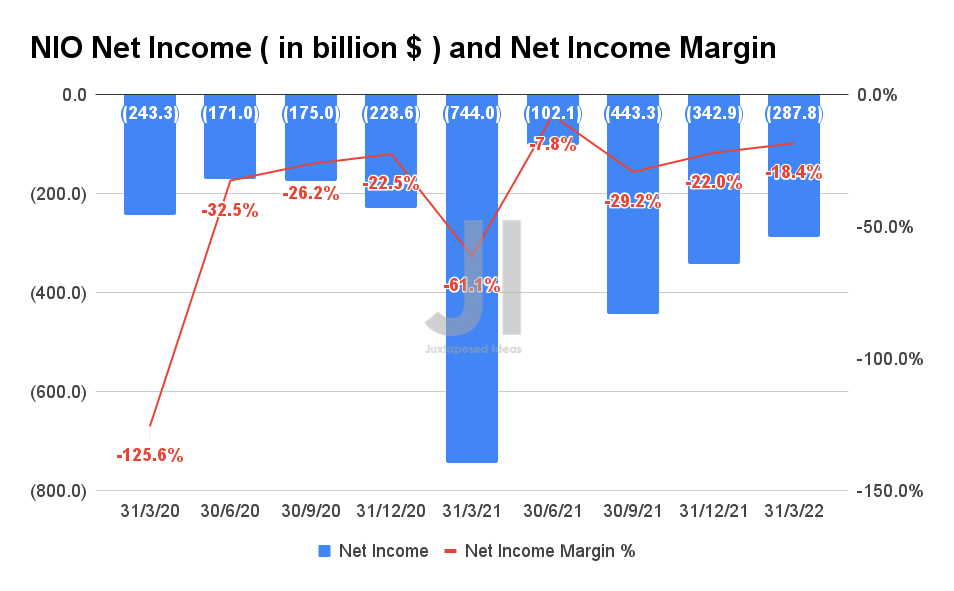

NIO Net Income and Net Income Margin

S&P Capital IQ

NIO reported net incomes of -$287.8 and net income margins of -18.4% in FQ1’22, thereby highlighting its lack of profitability since its incorporation in 2014. The company has also been increasing its operational costs exponentially with a total of $595.6M expenses by FQ1’22, representing 38.1% of its revenues and an increase of 207.1% YoY. Nonetheless, given that NIO has kept its operating expenses relatively stable at an average of 33.6% in the past eight quarters, it is apparent that the management has been rather disciplined in cost control as well.

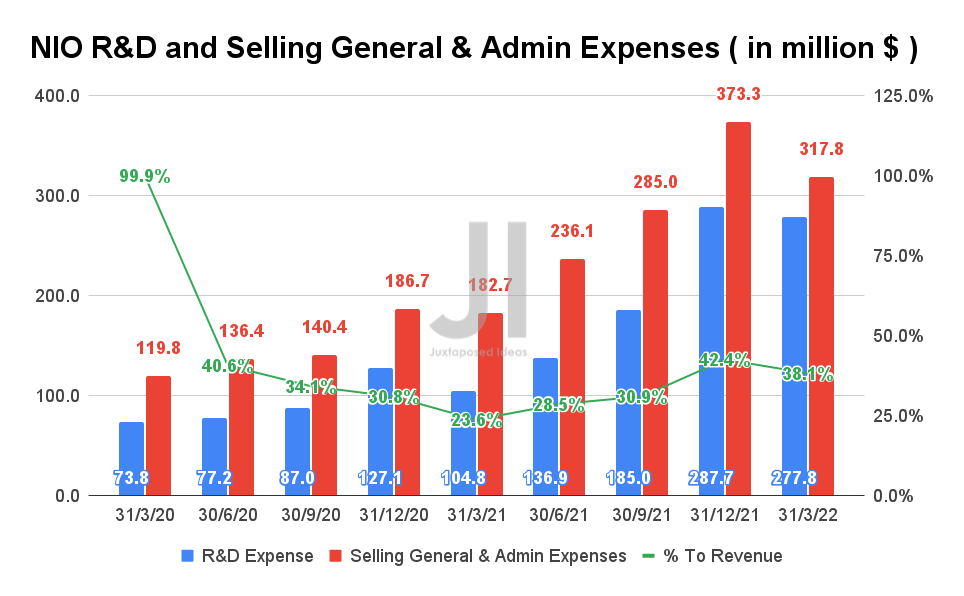

NIO R&D and Selling General & Admin Expenses

S&P Capital IQ

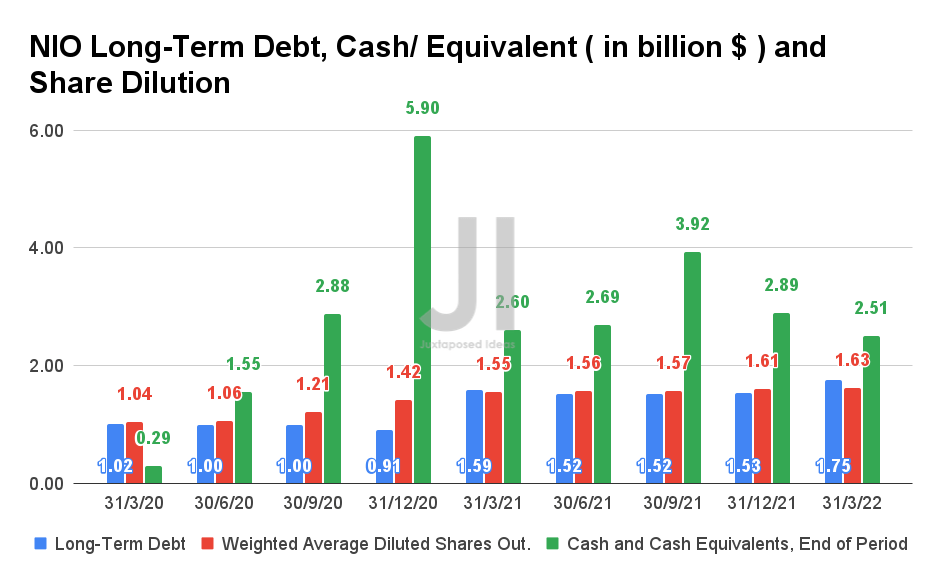

NIO Long-Term Debt, Cash/ Equivalent, and Share Dilution

S&P Capital IQ

Due to its lack of profitability, it is evident that NIO will likely rely on a combination of long-term debt and share-based compensation (SBC) for its expanding operations. By FQ1’22, the company had increased its reliance on debt by over 11-fold from $0.15B to $1.75B, while also diluting its shareholder by 55.5% since its IPO in September 2018. In FY2021 alone, NIO spent $158.5M in SBC, while drastically increasing the expenses to $74.6M by FQ1’22, representing an increase of 390.2% YoY. Assuming a similar rate of SBC expenses, we may expect the company to report up to $300M for FY2022. That would be a concern for many early investors, given that the company is not expected to report net income profitability until FY2024.

NIO Will Most Likely Fail To Deliver In FQ2’22

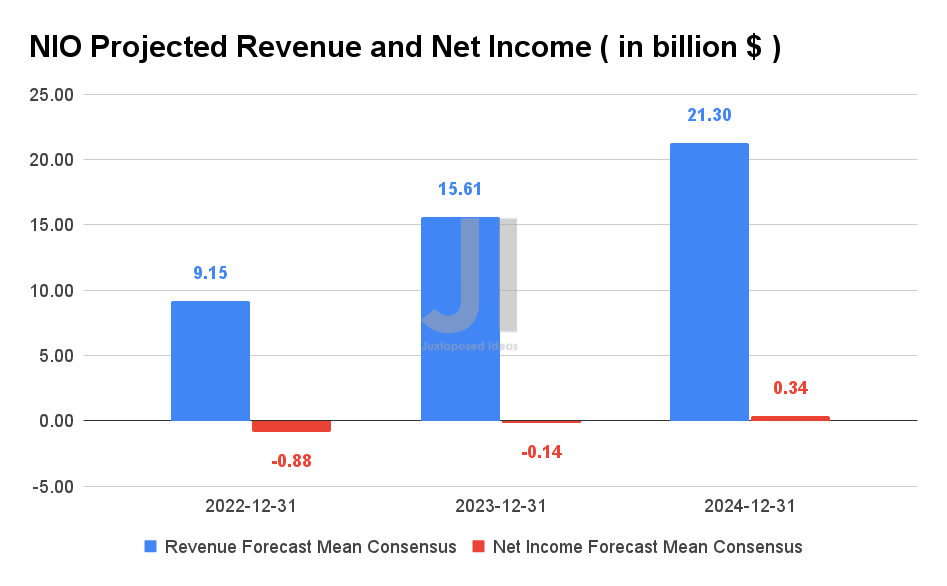

NIO Projected Revenue and Net Income

S&P Capital IQ

Over the next three years, NIO is projected to grow its revenue at a CAGR of 55.36% while also achieving profitability by FY2024 with a net income of $0.34B. For FY2022, consensus estimates that the company will report revenues of $9.15B with net incomes of -$0.88B, representing impressive YoY growth of 61% and 50%, respectively.

Nonetheless, given the ongoing Zero Covid Policy in China, there is a likelihood of a downwards re-rating for NIO’s FY2022 revenue, given Shanghai’s continuous lockdowns. The company itself had guided FQ2’22 revenues in the range of $1.47B to $1.59B against consensus estimates of $1.79B, representing up to a 5.7% decline QoQ though a 12.2% growth YoY. We are also not convinced of NIO’s delivery guidance of at least 23K vehicles for FQ2’22, given that the company had only delivered 5.074K and 7.042K vehicles in April and May 2022 respectively, thereby requiring an ambitious delivery of 10.884K vehicles in June 2022. Though rather unlikely, we shall anticipate its delivery update by early July 2022.

In contrast, we may expect improvement by H2’22 once NIO successfully expands its production capacity while also entering the auto market in Germany, The Netherlands, Sweden, and Denmark. Nonetheless, it is also important to note that these require an easing of China’s Covid policy while a stabling of the global supply chain issues. We shall continue to monitor the situation.

In the meantime, we encourage you to read our previous article on NIO, which would help you better understand its position and market opportunities.

- NIO: Down 55% With Supercharged Growth – Time To Buy Now

So, Is NIO Stock A Buy, Sell, or Hold?

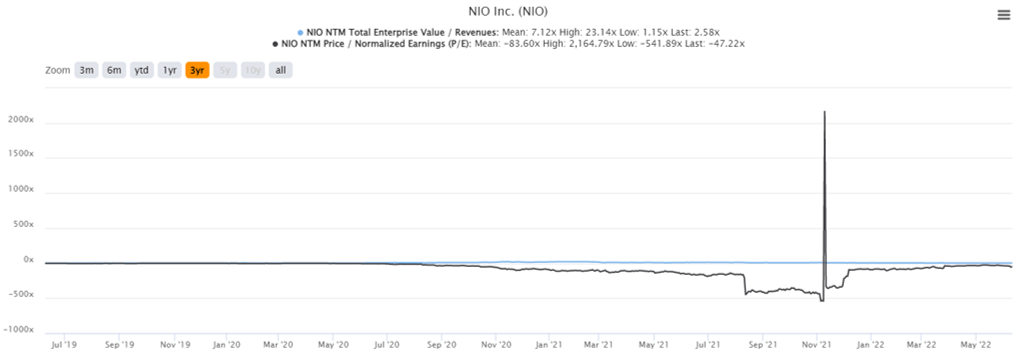

NIO 3Y EV/Revenue and P/E Valuations

S&P Capital IQ

NIO is currently trading at an EV/NTM Revenue of 2.58x and NTM P/E of -47.22x, lower than its 3Y mean of 7.12x and -83.60x, respectively. The stock is also trading at $18.14, down 67% from its 52 weeks high of $55.13, though at a 55.4% premium from its 52 weeks low of $11.67. It is apparent that the NIO stock has been on sideways price action since our last analysis in April 2022.

NIO 3Y Stock Price

Seeking Alpha

Given the macro issues and China’s unrelenting Zero Covid Policy, we are of the opinion that pain will not be ending anytime soon. If any, the relaxation of its Covid lockdowns may only happen after President Xi’s re-election in November 2022, if any. Therefore, NIO’s delivery would likely continue to be impacted until then, further reducing any chances of stock recovery in the short term.

Though consensus estimates had rated NIO as an attractive buy with a price target of $38.33, we are of a more conservative opinion of a potential retracement by early July 2022, assuming that the company could not deliver on its FQ2’23 vehicle target. As a result, we encourage investors to wait for a deeper retracement before adding to their portfolio.

Therefore, we rate NIO stock as a Hold for now.

Be the first to comment