Robert Way/iStock Editorial via Getty Images

While Beijing is on a crusade to consolidate its power within China’s tech industry, companies from the EV industry so far have avoided major interferences from the state. After the passage of Provisions on the Management of Automobile Data Security last year, China’s EV manufacturers haven’t been targeted much anymore in comparison to others. As a result, companies such as NIO (NYSE:NIO) managed to thrive and accelerate the deliveries of their electric vehicles, which led to the improvement of their top-line performances.

In the past, I’ve already covered NIO. Since the company has recently released its full-year earnings report and started to deliver new electric models, I believe that it’s a good time to update my thesis. To this day, I’m still convinced that the company has an enormous opportunity to become one of the major EV firms in China, but at the same time, it lacks the infrastructure and a favorable environment to successfully expand to other markets. Therefore, I continue to view NIO as a short to near-term long play, as its stock has an opportunity to appreciate in the foreseeable future.

Firing On All Cylinders

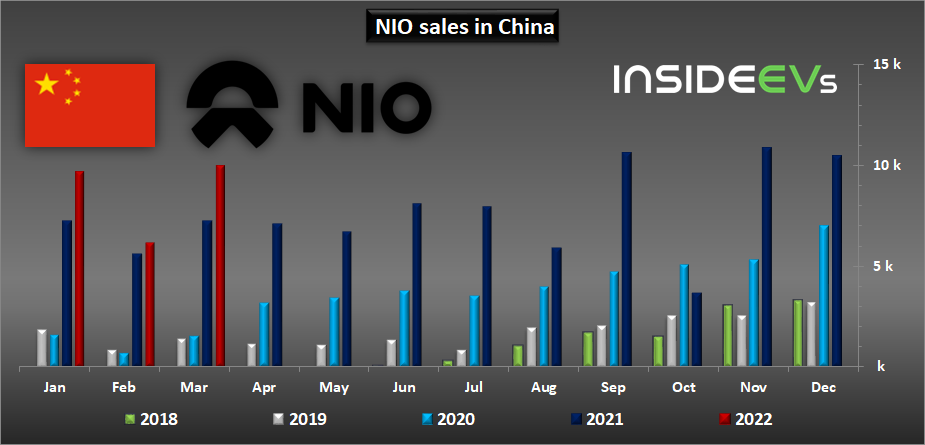

Currently, there are around 300 EV brands in China alone and NIO is already one of the most popular brands among them all. The company has made great progress since releasing its first electric SUVs such as ES6, ES8, and EC6 a few years ago, and the latest earnings report for FY21 shows that the demand for its vehicles is still high. Last fiscal year alone NIO delivered 91,429 vehicles, which represents a 109.1% Y/Y growth. Its total revenues for the period increased by 122.3% Y/Y to $5.67 billion, while its gross profit of $1.07 billion was up 264.1% Y/Y. At the same time, NIO is still not a mature brand in compassion to legacy automakers and as a result, it continues to be unprofitable. Its net loss in FY21 stood at $630.3 million, down 24.3% Y/Y.

Despite that net loss, the company continues to successfully increase brand awareness within China, which makes me believe that sales of its vehicles will continue to grow with each passing month. The latest deliveries data, which came out last week, shows that in March alone NIO delivered nearly 10,000 vehicles, while in Q1’22 it delivered 25,768 cars, up 28.5% Y/Y. In addition to that, in late March NIO launched its newest flagship electric sedan ET7, which has received a warm welcome from the public. However, it will have a significant impact on deliveries only in Q2 and beyond.

NIO sales (Insideevs)

More Opportunities Ahead

The main advantage for NIO is that its business is located in China, which is the biggest EV market in the world that has all the chances to continue to grow in the following years. While China remains the biggest consumer of coal among other nations, it still realizes the need to reduce its carbon footprint to meet its ongoing environmental challenges. China was among the signatories of the Paris Agreement in 2015 and it has an ambitious goal of becoming a carbon-neutral nation by 2060. The country is already the biggest investor in renewable energy and Beijing believes that the EV industry will be crucial in helping the country achieve its climate goals.

By 2035, Beijing aims at making sure that all the cars that are sold on the mainland are either hybrid or fully electric. Thanks to this, NIO has all the chances to continue to increase the deliveries of its vehicles each year, as it operates in a highly favorable environment. The latest data shows that the demand for EVs is only going to increase, as consumers themselves are preferring to purchase an electric vehicle instead of an ICE vehicle, which wasn’t the case some time ago. Nearly 15% of all car sales in China were electric in 2021, significantly higher in comparison to the U.S. market, and NIO is already one of the most popular EV brands out there.

To improve its performance, increase the potential customer base and close the gap in deliveries to competitors such as BYD (OTCPK:BYDDF) and Tesla (TSLA), NIO has been executing its plan of entering the mass market. As I’ve already mentioned above, NIO has launched its first flagship electric sedan ET7, and at the same time, it plans to expand its lineup of vehicles to serve a greater demographic. The company already has plans to produce a mid-size class sedan, SUV, and a minivan under the names ET5, ES7, and EF9, respectively, in the foreseeable future. At this stage, it’s too soon to tell how their deliveries will impact the income statement, but one thing that’s certain is the fact that NIO is no longer a luxury SUV play anymore. Over the last couple of years, the company has increased its brand awareness and expanded its ecosystem of vehicles and auxiliary services, which together helped it to gain a solid foothold in the Chinese EV market. Thanks to this, NIO now has the opportunity to penetrate a much broader customer base, which in the end should lead to the creation of an additional shareholder value.

Risks

While Beijing so far hasn’t directly interfered in NIO’s affairs, as it’s the case with tech firms, there’s always a risk that the situation will change at any time. Since the majority of NIO’s operations are conducted in China, there’s always a possibility that its business could be affected by the change in policy that could lead to devastating losses. There were already talks about the consolidation of China’s EV industry, which could involve interference from the state. Therefore, NIO is safe for now, but there’s no guarantee that it will be the case in the future.

In addition, the resurgence of Covid-19 in China signals that the pandemic is far from over. Due to the lockdown in various Chinese provinces, NIO has announced that it temporarily suspends the production of some of its models due to supply chain issues. If Covid-19 continues to be an issue for China, then NIO’s future deliveries could disappoint investors in the foreseeable future.

Last but not least, there’s little chance that NIO will be able to penetrate outside markets due to the lack of infrastructure and an unfavorable political environment for Chinese firms in places such as Europe or the United States, which I will broadly cover in my next article on the company.

The Bottom Line

As Beijing’s eyes are focused on tech firms, NIO should be considered China’s next dark horse, as it operates in a high-growth industry and in a favorable position, which makes it easier for it to achieve its goals. While there were concerns about whether NIO will be able to successfully compete with its peers due to the fact that it outsources the production of its vehicles to a third party, those fears were relatively overblown. The FY21 report shows that in the fiscal year, NIO’s vehicle margin was 20.1%, up from 12.7% a year ago. For comparison, one of NIO’s competitors XPeng (XPEV), which itself produces its vehicles, had a vehicle margin of only 11.5% in FY21. Therefore, not having its own production facility is not that big of a deal for NIO at this stage.

In addition, at the current price, NIO is also a better investment in comparison to its Western peers. Right now, the company’s stock trades at 3 times its forward sales, as its revenues are expected to grow at over 70% Y/Y in FY22 and be around $9.92 billion. For comparison, its counterparts such as Tesla (TSLA) and Rivian (RIVN) trade at 13x and 18x their sales, respectively. On top of that, with a consensus price target of ~$40 per share, which represents a growth of ~100% from the current price, NIO could be considered relatively cheap right now.

My only issue with NIO is that geopolitics along with the inability to successfully expand outside China are the main reasons why it’s hard to justify a long-term long position in the company. However, the good news is that China is still a pretty big and promising market with a lot of room for growth in the foreseeable future, and it’s one of the main reasons why I plan to hold NIO’s shares at least for the near term without overexposing my overall portfolio to it.

Be the first to comment