Andy Feng

NIO Inc. (NYSE:NIO) (“Nio”) is one of the most iconic electric vehicle (“EV”) companies in China. The company was founded in 2014 and has become known for its position as a luxury electric vehicle maker. The company has developed a range of fantastic electric vehicles which rival (and even beat) Tesla (TSLA) in a range of areas from quality to distance per battery. Its unique Battery-swapping technology also acts as a key differentiator, and the company has built a strong community around its brand. Nio recently reported record delivery numbers for the fourth quarter of 2022. Is Nio “the one”… in this post you are going to find out. I’m going to break down its business model, financials, and valuation, let’s dive in.

Nio vs Tesla

As mentioned above, Nio aims its product toward the “luxury” segment of the market. Tesla, by comparison, aims to cater to the mass market long term with an “affordable” EV. In addition, Tesla vehicles have often been criticized for poor build quality. Nio also has a few advantages over Tesla, such as its advanced battery swap technology, which has become popular throughout China. This means car owners don’t have to wait to “charge up” their vehicle and instead can just drive into a battery swap station for a quick changeover, in as little as 3 minutes. Another benefit of the battery swap system is it allows the vehicles to be sold at various price points with different battery sizes for short, medium, and long-range use cases. The company has over 1,300 battery swap stations across China and has partnered with over 550,000 third-party charging stations.

Nio Battery Swap Station (Nio)

Nio has also scored a landmark partnership with Shell to build out a series of 100 battery-swapping stations in China by 2025, and also roll out setups in Europe. Shell and Nio launched their first battery swap and charging station in China in Q3 of 2022. Nio has big plans for Europe, and has already launched in Norway, which is surprisingly the country with the most EVs per capita. In December, the company opened up operations in Sweden, another country that has a high percentage of EVs. In addition, NIO has rolled out its vehicles in Germany and aims to make its vehicles available in 25 countries by 2025.

Nio’s flagship SUV is called the ES8 and is known for its plush leather interior and “luxury” feel relative to a Tesla. At the end of 2021, the company announced its “Tesla Model 3 rival,” a saloon called the ET5, which has up to 620 miles of range, which is greater than the Tesla Model 3 “performance” range of “just” 420 miles. Deliveries of the ES8 started in China in September 2022. Surprisingly, the vehicle model is actually priced slightly cheaper than the Tesla Model 3 “performance,” despite being aimed at the “luxury” category. The price of the NIO ET5 is approximately $46,100 (RMB 328,000), relative to the Tesla Model 3 performance at $48,175, with both prices excluding subsidies. Tesla has started to slash its prices in China, in an effort to boost demand against a tepid macroeconomic backdrop and high competition. I personally think the NIO ET5 is better looking than the Tesla model 3, but of course, that is subjective.

Nio ET5 (Carscoops)

Nio has built up a strong sense of “community” around its brand and product. In the past, the company has hired popular Chinese singers for headline performances. In addition, the company has expanded its “community” strategy to other countries. In 2021, the company collaborated with a viral Norwegian DJ named Alan Walker. Promotional “stunts” such as this help to create a cooler brand and embed that philosophy into a consumer’s mind. I personally believe Nio Day events look more like a rock concert than a car launch event.

Nio events look like a rock concert (Nio day)

Solid Financials

Nio has reported solid financial results for the third quarter of 2022. Revenue was $1.81 billion, which beat analyst estimates by $27.12 million and increased by over 20% year-over-year.

This was driven by the delivery of 31,607 vehicles, which increased by 29.3% year-over-year. Nio has developed its “NT2.0” technology platform, which has enabled it to deliver models using a “cookie-cutter” style template. In October, the company delivered 10,059 vehicles which increased by an outstanding 174.3% year-over-year. This was despite supply chain volatility and component supply issues.

Fourth Quarter Deliveries

Nio recently reported its preliminary delivery numbers for the fourth quarter of 2022. The company set a new record, with December deliveries of 15,815 vehicles, up a blistering 50.8% year-over-year. These vehicles consisted of 6,842 EV SUVs, which included 4,154 ES7s. In addition to 8,973 EV sedans, which consisted of 1,379 ET7s and 7,594 of the new ET5s (Tesla rival), discussed prior.

For the fourth quarter of 2022, the company delivered a solid 40,052 vehicles, which increased by a rapid 60% year-over-year. This growth rate was slightly lower than management’s estimate of 43,000, announced in its third-quarter earnings call. For the full year 2022, Nio delivered 122,486 vehicles, which increased by 34% year-over-year.

As a comparison of scale, Tesla reported deliveries of 405,278 vehicles in the fourth quarter of 2022. This is over ten times the quarterly deliveries of Nio and close to four times its annual figure. Tesla is on another level in terms of both production scale and product demand. Tesla has “vertically integrated” its entire business and has a range of “Gigafactories” globally from Texas to Shanghai and Berlin. Whereas, Nio has only recently opened its first “fully owned” factory in Hefei, China. The majority of NIO vehicles are made via a joint partnership with JAC. Therefore, I would expect Nio to have lower margins than Tesla, due to both scale and vertical integration reasons. But let’s also not forget Nio has a market capitalization of “just” $16 billion. Whereas, Tesla has a market capitalization of ~$338 billion, after a major decline in share price, which I reported recently.

NIO JAC factory celebrating 200,000 cars (Q1,22 NIO)

Nio has continued to build out its network of chargers and reported, 1,315 power swap stations and over 7,159 chargers globally.

Profitability and Balance Sheet

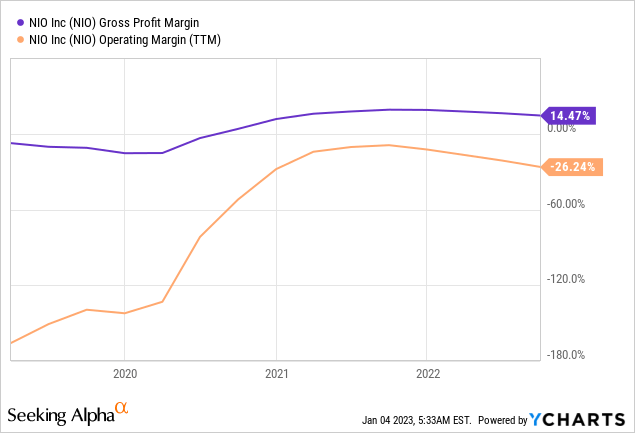

Back to the third quarter financials, the company reported a gross margin of 13.3%. This metric was down substantially from the 20.3% reported in the same quarter last year. This was driven by lower automotive regulatory credits which previously gave the company higher margins. The company also reported a vehicle margin of 16.4%, which was down slightly from the 18% reported in the same quarter of 2021. This was mainly driven by higher costs per battery unit and lower vehicle financing subsidies.

Nio reported earnings per share [EPS] of negative $0.35, which missed analyst estimates by $0.21. This was driven by a combination of higher costs and a devaluation in RMB assets, relative to the strength of the U.S dollar.

Its R&D expenses rose by 146.8% year over year to $422 million (RMB 2.9 billion). Overall, I don’t deem this to be a bad sign, as investing in product improvement is necessary to stay ahead in the EV market.

Its SG&A expenses rose by an eye-watering 48.6% year-over-year to $392 million (RMB 2.7 billion). This was driven by an increase in personnel costs, in addition to network expansion and marketing. Overall, I believe some of these costs were necessary given the launch of new vehicle models, but over time I would like to see this declining.

Nio has a solid balance sheet with $7.47 billion in cash, cash equivalents, restricted cash, and short-term investments. The company has fairly high total debt of $3.795 billion, but the majority of this is a long-term debt of $1.762 billion, which is manageable.

Advanced Valuation

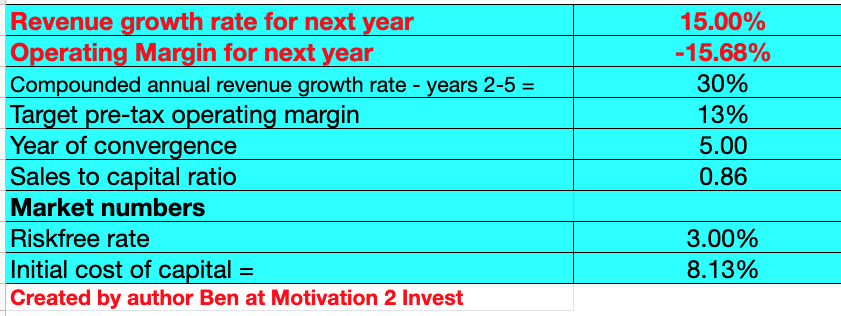

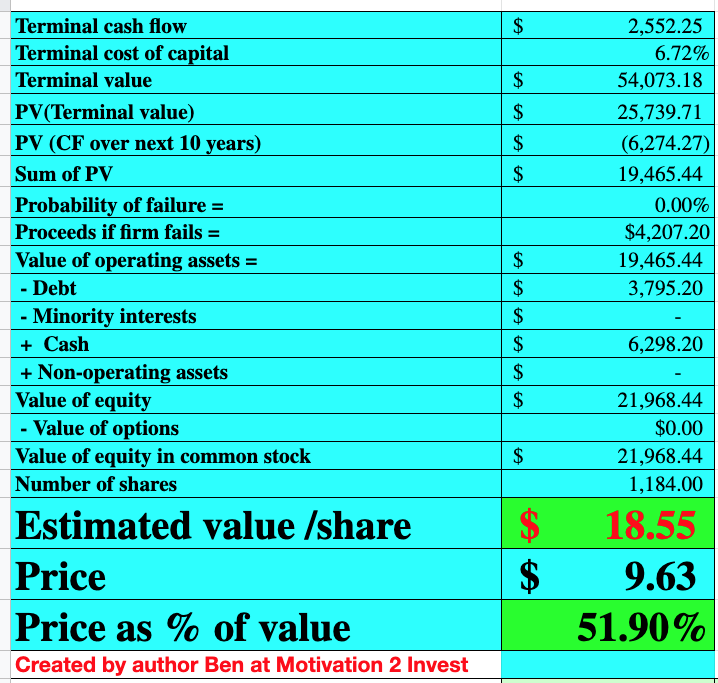

I have plugged the latest financial data into my advanced valuation model, which uses the discounted cash flow (“DCF”) method of valuation. I have forecast 15% revenue growth for next year, which is less than the prior growth rate of over 20%. I am expecting this lower growth due to the macroeconomic environment, and even the great Tesla has reported slowing demand in China. The positive is in years 2 to 5, I have forecasted a steady growth rate of 30% per year, as I expect an economic recovery.

Nio stock valuation 1 (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation, I have capitalized R&D expenses, which has lifted net income. In addition, I have forecast a 13% operating margin in the next 5 years. This is optimistic, but possible if the company can continue to scale its operations and improve efficiencies with scale. As a comparison, Tesla has an operating margin of approximately 18%, with an R&D adjustment. Thus, I believe Nio will have lower margins than Tesla, as it doesn’t have the scale and infrastructure. But the company can still increase its operating margin long term. The fact Nio is aiming at the “luxury” market is also a positive for pricing power.

Nio stock valuation 2 (created by author Ben at Motivation 2 Invest)

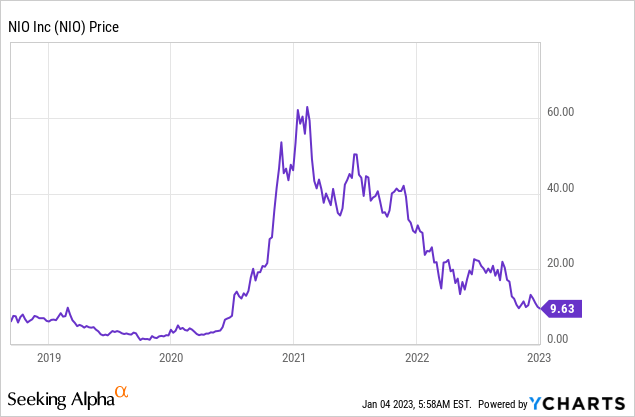

Given these factors I get a fair value of $18.55 per share. Nio stock is trading at ~$9.63 per share at the time of writing and thus is ~48% undervalued.

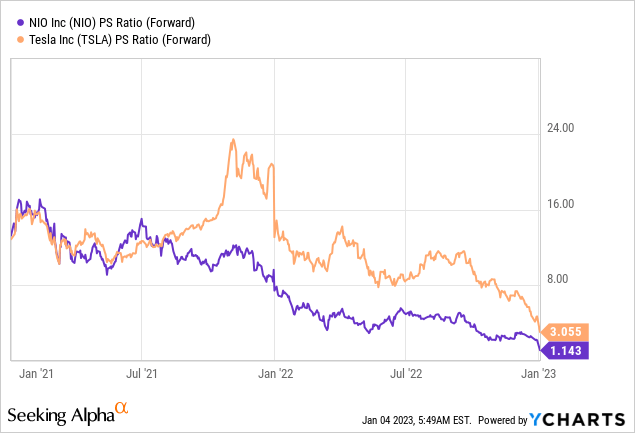

For an extra datapoint, Nio trades at a price-to-sales ratio = 2.59, which is 75% cheaper than its historic 5-year average. The stock also trades cheaper than Tesla, which trades at a PS ratio = 3.

Risks

Recession/lower EV Demand

A European recession is forecasted, which is expected to have a knock-on effect against China due to its large number of exports. Barclays has recently slashed its Chinese exports from 1% growth estimated prior to a 2% to 5% decline in 2023. Tesla recently reported lower demand for its EVs in China and has been slashing prices in the region. Therefore, it would not surprise me if Nio sales dropped in 2023 also. I have taken this into account with a slower growth forecast for next year.

Final Thoughts

Nio has developed a strong position in the luxury EV market in China. Its battery swap technology and major community feel act as a key differentiator. The company is poised to benefit from the growth in the Chinese EV industry and its plethora of subsidies on offer. NIO Inc. stock is undervalued intrinsically and relative to its historic multiples, thus it could be a great long-term investment.

Be the first to comment