greenbutterfly

NIO (NYSE:NIO) ended FY 2022 with a strong delivery performance in December, which saw the highest level of deliveries in the entire year. In December, NIO delivered more than 15 thousand electric vehicles and sedan deliveries are rapidly closing in on a 10 thousand monthly delivery volume. NIO is going to launch new products in mid-2023 as well, but the electric vehicle company nonetheless faces muted delivery growth prospects considering growing uncertainty about a full Chinese economic reopening due to a surge of new COVID-19 infections!

Strong December deliveries, but overall delivery picture disappointed in FY 2022

NIO delivered 15,815 electric vehicles in December which was the highest monthly delivery volume in the entire year of 2022. Despite a strong finish in FY 2022, however, NIO’s December delivery performance must be seen in the context of the EV company lowering its fourth-quarter delivery outlook due to registration challenges and persistent supply chain challenges.

NIO warned of weaker than expected Q4’22 deliveries at the end of December and projected to deliver 38,500-39,500 electric vehicles to customers which, in the worst case, could have represented a decline of up to 8,500 EVs compared to the firm’s earlier guidance. NIO’s actual fourth-quarter deliveries totaled 40,052 electric vehicles so the company beat its high-case forecast by 552 EVs and at no point in the firm’s history was the quarterly delivery volume higher than in Q4’22. With about 40 thousand EVs delivered in Q4’22, the electric vehicle start-up saw delivery growth, on a per unit basis, of 60% year over year.

NIO had the second-largest delivery volume in December after Li Auto (LI) which delivered more than 21 thousand EVs in the last month of the year. XPeng (XPEV) fell further behind its rivals with deliveries of just 11,292 electric vehicles: XPeng was the only company of the top three EV start-ups that saw negative delivery growth (29.4%) on a year over year basis in December.

|

Deliveries |

October |

Oct Y/Y Growth |

November |

Nov Y/Y Growth |

December |

Dec Y/Y Growth |

|

NIO |

10,059 |

174.3% |

14,178 |

30.3% |

15,815 |

50.8% |

|

XPEV |

5,101 |

-49.7% |

5,811 |

-62.8% |

11,292 |

-29.4% |

|

LI |

10,052 |

31.4% |

15,034 |

11.5% |

21,233 |

50.7% |

(Source: Author)

NIO also had some other good news to report, besides beating its Q4’22 delivery forecast… and this was that monthly sedan deliveries are on track to exceed 10 thousand EVs in the first quarter of FY 2023.

NIO delivered 8,973 ET5 and ET7 sedans in December, showing an impressive month over month growth rate of 45.3%. NIO delivered 7,594 ET5s in December which represents a 7.3 X factor increase over the ET5 delivery volume in October which is when the company delivered 1,030 ET5s. October was also the first full month of production/deliveries for NIO’s second sedan product.

NIO also hit another crucially important milestone as well in December: for the first time ever, sedan deliveries accounted for more than 50% of total deliveries — the actual sedan delivery share was 56.7% in December — and given the momentum in NIO’s EV sedan sales, I believe NIO could easily exceed a 60% share next month. As NIO launches new SUV products in mid-2023 (the EC7 coupe SUV and the ES8 SUV), deliveries of NIO’s sport utility vehicles are likely to receive a boost.

|

NIO ET7/ET5 Metrics |

August |

September |

October |

November |

December |

|

Total Deliveries |

10,677 |

10,878 |

10,059 |

14,178 |

15,815 |

|

NIO Sedan Deliveries |

3,126 |

3,149 |

4,080 |

6,175 |

8,973 |

|

M/M Growth |

26.4% |

0.7% |

29.6% |

51.3% |

45.3% |

|

Sedan Delivery Share |

28.7% |

28.9% |

37.5% |

43.6% |

56.7% |

(Source: Author)

NIO’s valuation

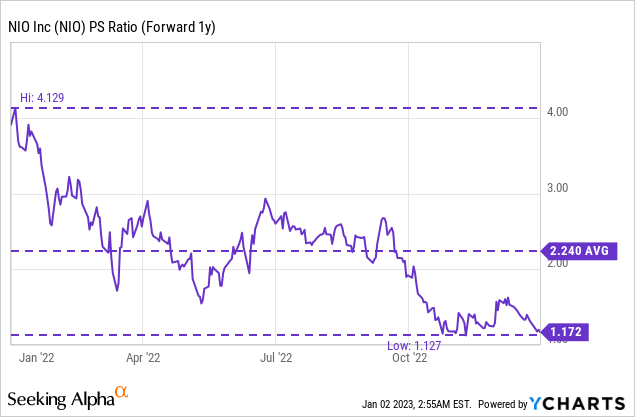

Shares of NIO for now appear to be stuck in a down-trend: shares recently dropped below $10 again which could indicate that NIO is even at risk of becoming a single-digit stock in the short term. Despite good delivery results recently, negative sentiment overhang has built over the last year and will likely continue to weigh on the firm’s valuation. NIO is currently trading at a P/S ratio of 1.2 X which is significantly below its 1-year average P/S ratio of 2.2 X. Given the uncertainty surrounding a full economic reopening in China, I don’t believe the valuation situation is going to improve significantly for NIO in the foreseeable future.

Risks with NIO

The Chinese economy is on track to reopen after a brutal shutdown in FY 2022 that was chiefly responsible for NIO’s erratic delivery picture throughout the year. However, there are risks to the reopening which are related to new COVID-19 outbreaks. A recent surge in new infections could lead to new shutdowns and weakening consumer spending… as well as a muted delivery picture for NIO and the rest of the electric vehicle sector in 2023. What I also see as a risk for NIO is increasing pricing pressure in the EV market due to rising competition and high raw material costs.

Final thoughts

NIO ended FY 2022 with a good delivery performance: in no other month did NIO deliver more electric vehicles than in December 2022. Delivery growth has been once again chiefly driven by an impressive ramp of two of NIO’s last three product launches: the ET5 and the ET7. Sedan deliveries are likely going to continue to drive NIO’s delivery growth in the first half of FY 2023. However, I am not prepared to recommend NIO to investors yet due to growing recession risks and the risks stemming from the recent rise in COVID-19 infections which could result in new shutdowns as well as weaker consumer demand. Despite record deliveries in December 2022, I continue to rate NIO a hold!

Be the first to comment