Lukas Schulze

Thesis

Nintendo (OTCPK:NTDOY) stock dropped as much as 8% the trading day following the company’s earnings report for the December quarter (7974.T-JP reference). Although results were relatively solid, investors were undoubtedly disappointed that Nintendo reduced the FY 2023 profitability outlook and lowered the sales forecast for the Switch console by one million units, down to 18 million. In my opinion, however, investors should consider that the softer than expected performance in the December quarter 2022 is not unique to Nintendo. In fact, many leading game developers, including Ubisoft (OTCPK:UBSFY), Frontier Development and Take-Two Interactive (TTWO), reported disappointing/ decreasing bookings as compared to the same period in 2021. That said, the demand slowdown is likely an industry-wide problem.

Personally, I lower my EPS estimates for Nintendo through 2025, but I still view NTDOY stock as undervalued. According to my valuation model, NTDOY should be fairly priced at $12.79/share. Nintendo shares remain a ‘Buy’.

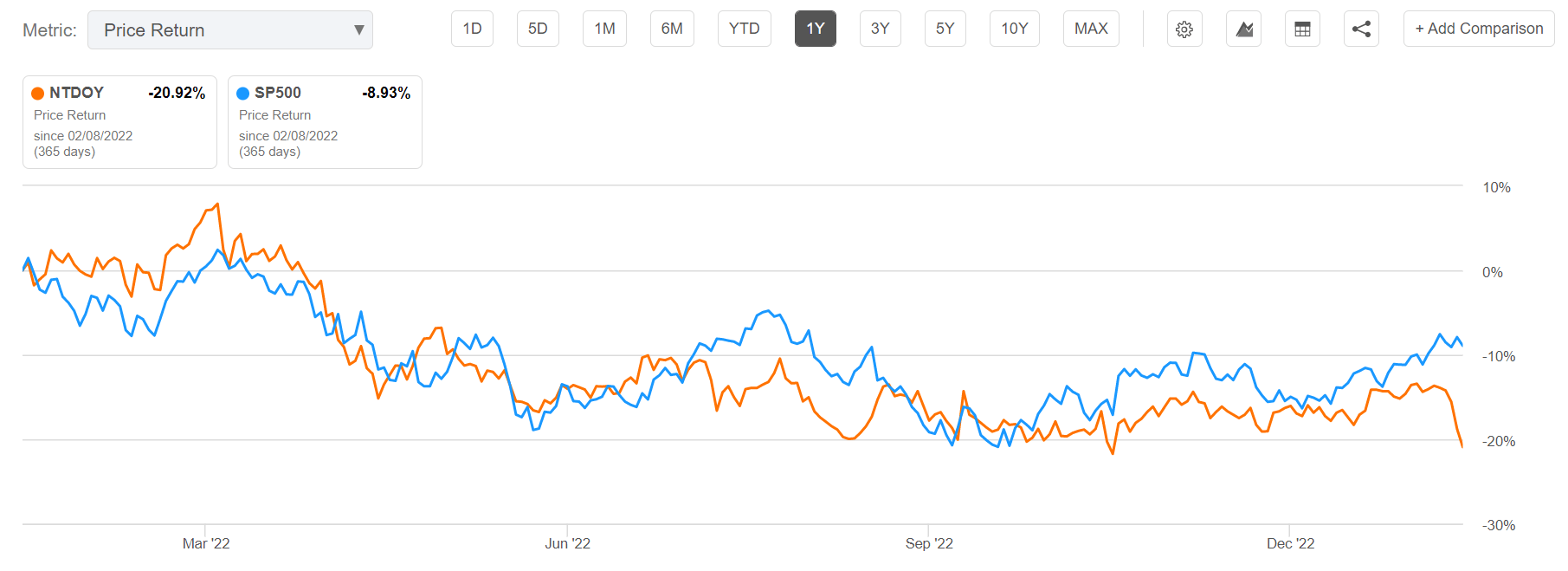

For reference, NTDOY stock is down approximately 21% for the past twelve months, as compared to a loss of about 9% for the S&P 500 (SPY).

Seeking Alpha

Nintendo’s December Quarter

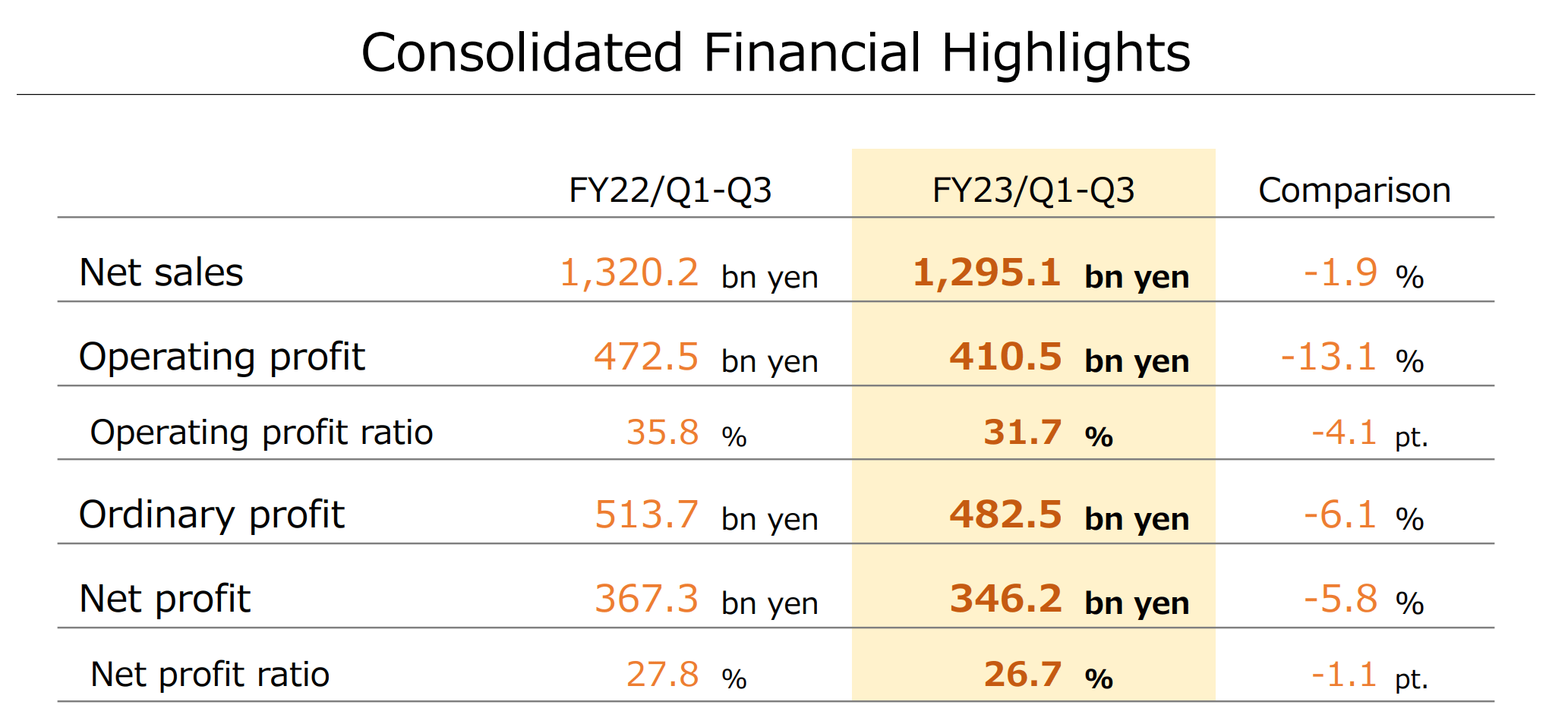

During the nine months ended December 31, 2022, Nintendo generated total revenues of 1.29 billion yen, which compares to 1.32 billion yen for the same period one year earlier (1.9% year over year negative growth). Similarly, Nintendo’s operating income decreased by about 13.1% year over year, to 410 million yen, and net profit, which includes interest income and tax expenses, is down 5.8% year over year, to 346 billion yen.

Nintendo December Quarter 2022 Earnings Presentation

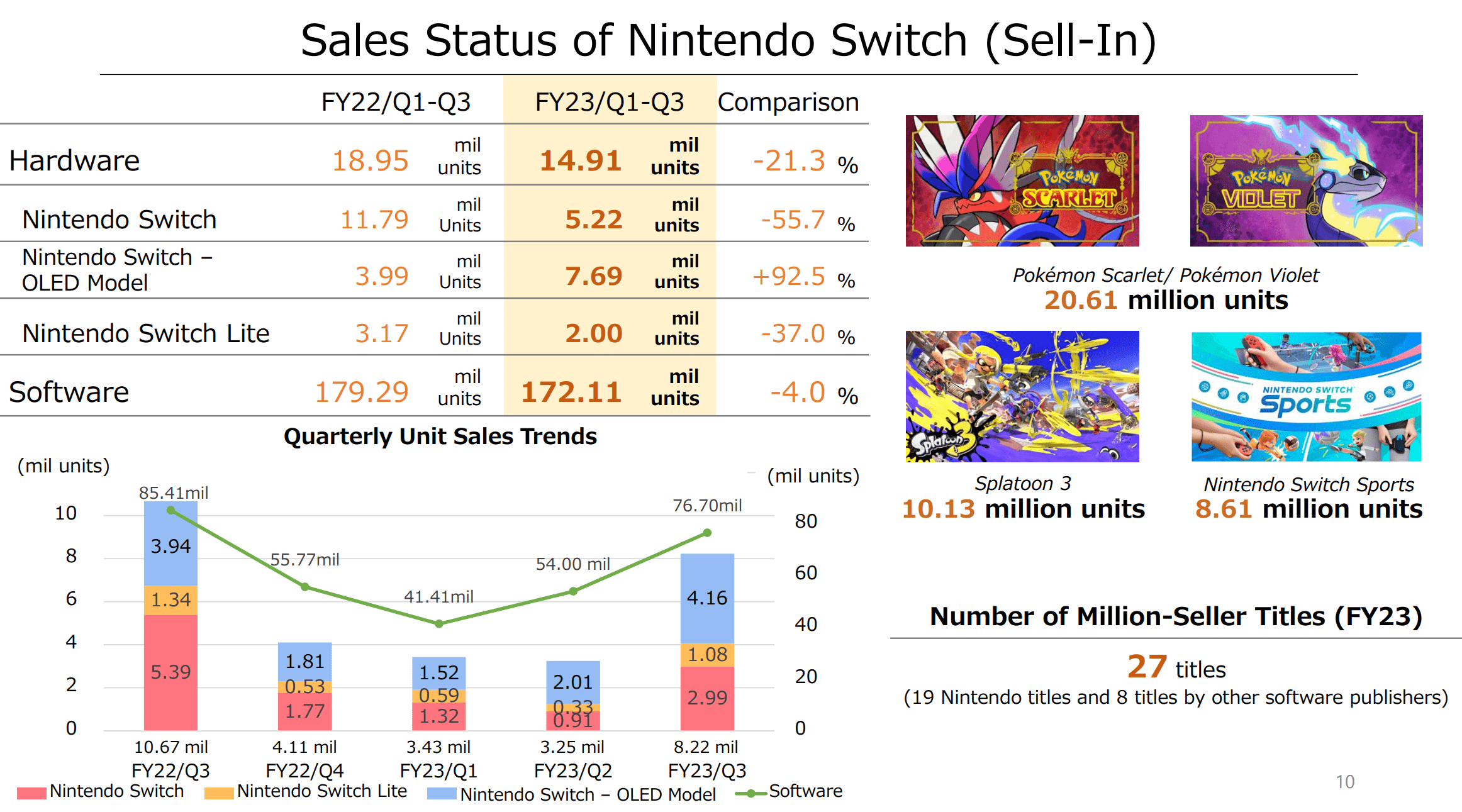

In context of games sales, Nintendo’s Pokémon Scarlet and Pokémon Violet recorded strong sales of 20.61 million units, while other new titles such as Splatoon 3 and Nintendo Switch Sports also performed well. The company had 27 million seller titles (including titles from other software publishers).

However, hardware sales declined 21.3% to 14.91 million units due to continued component supply shortages as well as a softer than expected demand during the holiday quarter–as Nintendo sold only 8.23 million Switch consoles, a 22% YoY decrease.

Nintendo December Quarter 2022 Earnings Presentation

Outlook Disappoints

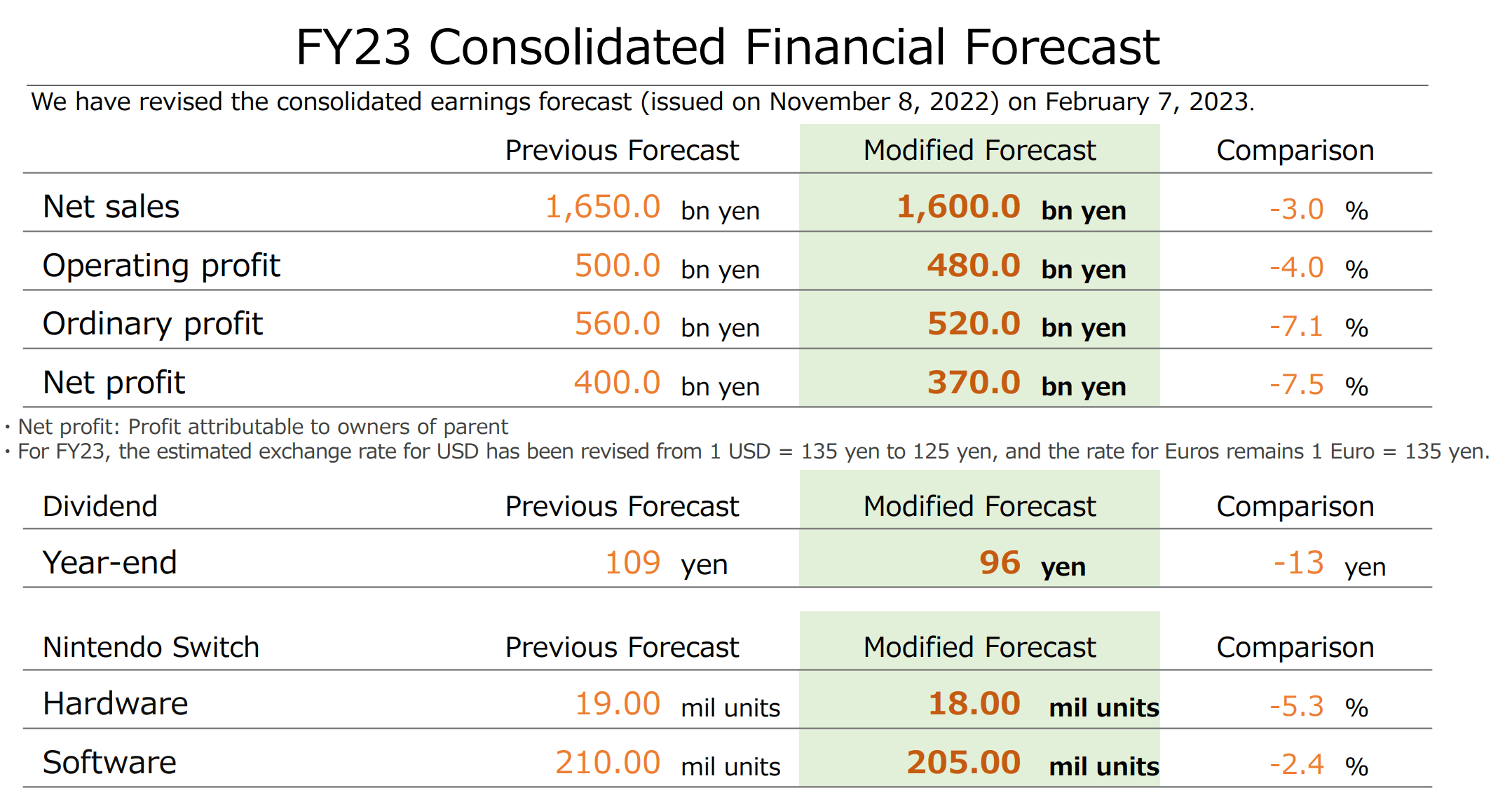

Nintendo revised its outlook for sales of its Switch console and games as well as for its profit for the current fiscal year. The company now projects sales of 18 million Switch units and 205 million software units, down from its previous forecasts of 19 million and 210 million units respectively. Similarly, management has also reduced the net profit outlook to JPY370 billion ($2.8 billion), down from the previously expected JPY400 billion ($3 billion).

According to the company, the Switch’s somewhat unexpected underperformance during the holiday season is the reason for the revision in hardware sales estimates. And, understandably, markets are now concerned that the console has finally entered a maturity stage of structural and accelerating demand decline, after six years of strong performance. The company’s president declined to answer questions about whether a successor to the Switch will be unveiled–adding to the market’s concern about Nintendo’s short-/medium term outlook.

Nintendo December Quarter 2022 Earnings Presentation

In my opinion, investors should consider two arguments why the weaker than expected December quarter 2022 might not fully reflect the company’s potential.

Firstly, the demand slowdown is likely an industry-wide problem, as many leading game developers, including Ubisoft, Frontier Development and Take-Two Interactive, reported disappointing/ decreasing bookings as compared to the same period in 2021. With that frame of reference, once the gaming industry recovers, I argue it is reasonable to assume that Nintendo’s financials should rebound in lock-step with the industry.

Secondly, Nintendo owns one of the world’s most recognizable and loved brands. And management has only recently started to leverage the brand across more value verticals such as theme parks and movies. That said, the Super Mario Bros. movie is scheduled to premiere in the U.S. on April 7 and in Japan on April 28. And SUPER NINTENDO WORLD at Universal Studios Hollywood will open on February 17. If these initiatives are successful, Nintendo management will likely push for more diversification away from gaming, something that could likely support NTDOY stock with both a diversification/ safety premium, as well as a growth premium.

For reference, with NTDOY trading at an EV/EBIT of close to x8.6, the stock is trading at a more than 50% discount as compared to the respective multiple for Disney (DIS).

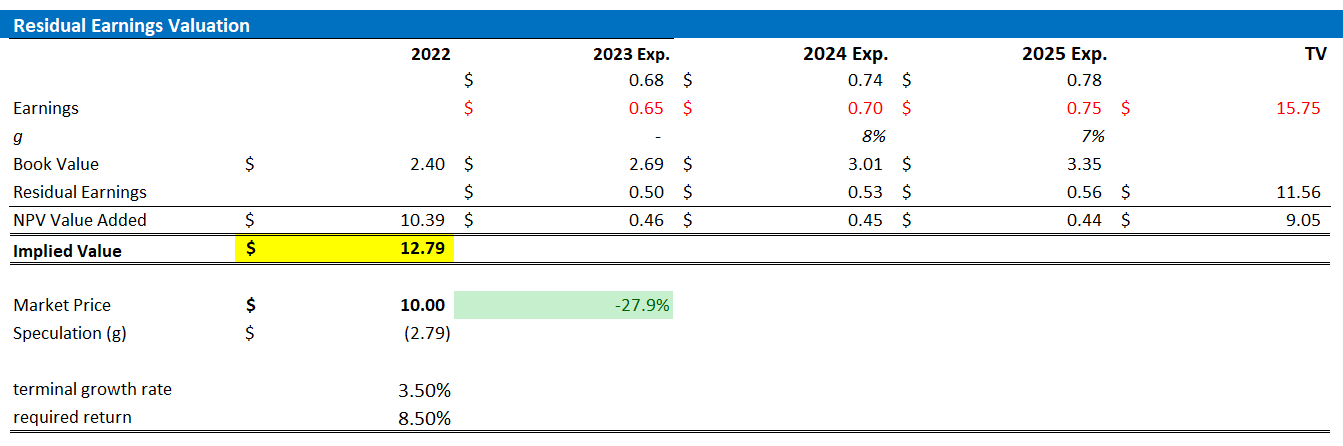

Target Price: Lower To $12.79

Reflecting on more cost discipline in 2023 vs 2022, I estimate that NTDOY’s EPS in 2023 will likely fall somewhere between $0.6 and $0.7. Moreover, I also slightly lower my EPS expectations for 2024 and 2025, to $0.7 and 0.75, respectively.

I continue to anchor on a 3.5% terminal growth rate (one percentage point higher than estimated nominal global GDP growth), but I raise my cost of equity requirement by 50 basis points, to 8.5% (to reflect structurally higher risk premia for equity investments across the world).

Given the EPS updates as highlighted below, I now calculate a fair implied share price of $12.79, as compared to $14.45/share prior.

Author’s EPS Estimates & Calculation

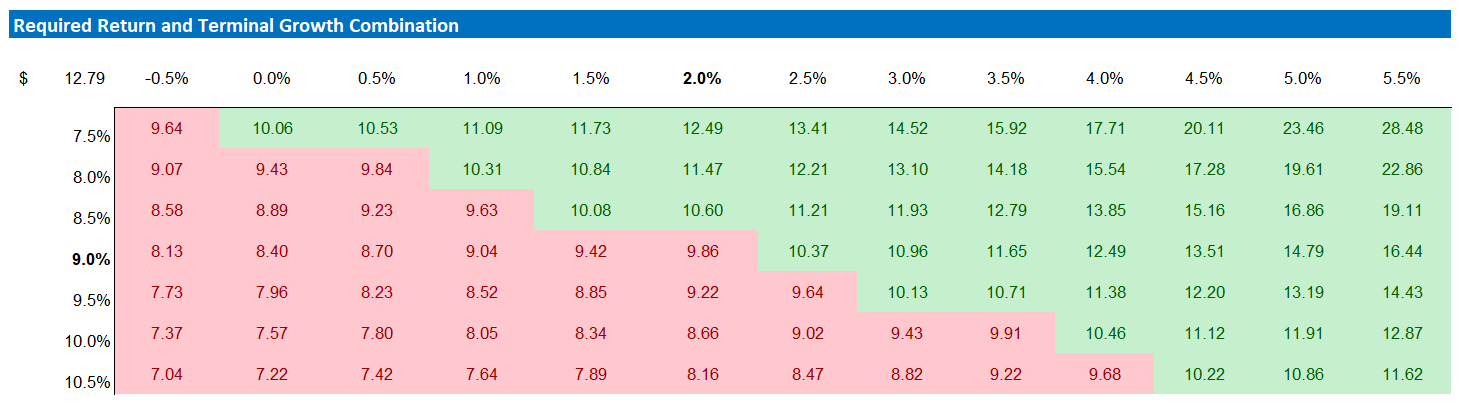

Below is also the updated sensitivity table.

Author’s EPS Estimates & Calculation

Risks

As I see it, there has been no major risk-updated since I have last covered NTDOY stock. Thus, I would like to highlight what I have written before:

First, a worsening macro-environment could negatively impact Nintendo’s business operations. On the demand side: including inflation, rising interest rates and falling asset prices might negatively impact consumer sentiment and entertainment spending. On the supply side: supply-chain challenges such as semiconductor shortage could slow Nintendo’s production output. If challenges-both on the demand and supply side-turn out to be more severe and/or last longer than expected, the company’s financial outlook should be adjusted accordingly.

Second, while high brand-equity company’s such as Nintendo see relatively little impact from direct price competition or competitive cannibalism, Nintendo’s competitive positioning and future success is deeply intertwined with the company’s ability to successfully innovate and market new products. Nintendo’s ability to innovate and launch industry-leading entertainment solutions must further be analyzed in a relative context versus competitors such as Sony and Microsoft.

Conclusion

Despite a somewhat softer than expected performance in the 2022 holiday period, as well as a lowered profit outlook in FY 2023 on the backdrop of the Nintendo Switch entering its late-life cycle, I maintain my ‘Buy’ rating on Nintendo. Personally, I continue to like the company’s strong brand and favorable valuation relative to fundamentals. Taking into consideration the recent EPS updates with a downward revision through 2025, I now estimate a fair share price for NTDOY to be $12.79/share.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment