Georgijevic Singular Research

Company Description

NexTech AR Solutions (OTCQX:NEXCF) engages in the acquisition and development of augmented reality [AR] technology. The Company started as an eCommerce franchise but is now essentially focused on commercializing AR technology. NexTech was incorporated in 2018 and is based in Toronto, Canada.

Investment Thesis

NexTech is positioning itself as the first publicly traded company that is exclusively focused on the Augmented Reality [AR] niche of eCommerce. eCommerce, an over $5 trillion/year market, needs new offerings to enhance customer experience. AR and Metaverse offerings have become key for the next leg of growth. The Company enjoys a competitive advantage in this space, as its offerings are Artificial Intelligence based and hence are not only better priced than its competitors but also scalable and more versatile. We believe NexTech has the wherewithal to dominate the AR experience and 3D model services space. With the acquisition of Amazon as a customer, arguably the holy grail of eCommerce, the Company seems to be on a path to deliver on its corporate strategy.

At this time, we are not making any changes to our estimates as we await execution. We reiterate our Buy-Venture rating and a $1.50 price target, 9.50 times EV/2023 Revenue (implying a capital appreciation potential of 150%).

Toggle3D: A New Offshoot

- NEXCF plans to pursue a spinout of its Toggle3D design studio SaaS (Software as a Service) platform. Though final tax and legal structuring await, we estimate that current NEXCF shareholders will receive about 50% of Toggle3D (Spinco) shares. We note that ARWay (OTCPK:ARWYF, ARWY/CSE), which was spun off in a similar fashion in October 2022, has attained a market cap of $25 million.

- Meticulously nurtured by NEXCF, the Toggle-3D platform enables the conversion of CAD (Computer Aided Design) files into 3D/AR models at scale. Modeled as SaaS, Toggle-3D’s offerings will enjoy high operating margins.

- To be marked as “A Web-Based 3D Design Studio for Anyone,” Toggle-3D intends to disrupt the CGI (Computer-Generated Imagery) market, which NEXCF estimates to be $160 billion per year (6% CAGR), by its easy, scalable, affordable and accessible offerings.

Primary Risks

- Though AR is gaining momentum, its usage is still with the early adopters, which represent only a small proportion of the total eCommerce accessible market.

- The disappearance of pandemic-related tailwinds has adversely affected eCommerce companies’ top-line momentum and compressed their valuations.

Valuation

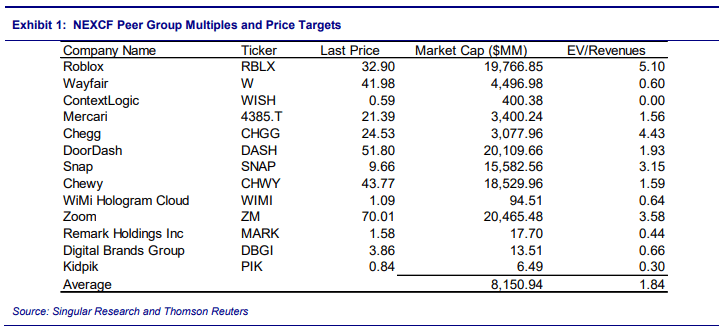

We value NexTech using a revenue multiple analysis method. All NexTech’s direct competitors in the AR space are private companies. Therefore, for the sake of valuation, we have assembled a group of public companies that are either involved in AR or have exposure to Metaverse technology. Most of these companies utilize AR/metaverse technology to serve Internet Retail end markets, but some also serve Conferencing and Electronic Gaming industries. As shown below, the multiples of most of the peer group are depressed partly due to the current interest rate/macro-economic environment and partly due to revenue headwinds (and difficult comps) these companies are facing from the post-pandemic stimulated revenue surge. Nevertheless, NexTech’s case is different as the Company is exiting the eCommerce product-based business and entering the service-only and differentiated AR and Metaverse space. As shown in the Revenue and COGS Exhibit, we project the Company’s Renewable Software Licenses segment to grow by almost 400% in 2023 and essentially account for almost 100% of NexTech’s revenues. Most of the comparable companies are not experiencing such a surge in top and bottom-line growth. Moreover, the Company has spun off ARWay as a separately publicly traded company, which could be substantially value accretive for NexTech. Similarly, Toggle3D’s proposed IPO/Spin-off could be considerably value accretive. Therefore, we ascribe NexTech an EV/Revenue multiple of 9.50x (its 2023 revenues), over a 400% premium to the 1.84x average for the group of companies, as shown below. Based on a 9.50x EV/Revenue multiple, we value NexTech at $1.50 per share, which represents a 150% appreciation potential to the stock’s current price.

Singular Research and Thomson Reuters

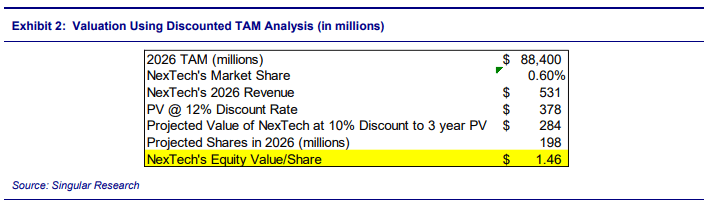

As an alternative valuation methodology, we attempted to value NexTech using a total addressable market analysis [TAM]. According to Markets & Markets Research Pvt Ltd, 1, the Augmented Reality Market was valued at U.S.$23 billion in 2021 and is expected to reach U.S.$88 billion by 2026, witnessing a CAGR of 31%. We project NexTech to be just 0.05% of this market in 2023. However, we project NexTech to grow much faster than the market from 2023 onwards. If we assume the Company attains a modest 0.6% share of the TAM in 2026, its revenues will amount to $531 million. Discounting this figure back to 2023 (3 years), with a 12% WACC, we project that the present value of NexTech’s potential 2026 revenue to be $378 million. Discounting this value at 10% to reflect NexTech’s challenging odds of realizing this level of revenues provides a projected value for the Company of $284 million. Dividing this figure by our projected outstanding shares at the end of FY:26 yields a per-share value today of $1.46 per share. We believe using FY:26 projected yearend shares outstanding is a conservative valuation approach that accounts for the expected growth in outstanding shares.

Singular Research

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment