RHJ/iStock via Getty Images

A few months ago, I wrote an initiation article on NexGen Energy Ltd (NYSE:NXE). Although I believe NexGen’s Arrow uranium deposit is a tier 1 development project, it is now stuck in development limbo with not much in terms of catalysts to get speculators excited in the near-term.

One big risk to NexGen is a recent spate of mining/infrastructure capex blowouts, which suggests capital costs could be significantly higher at Arrow. NexGen is currently trading at 0.85x P/NAV, which appears rich relative to the capex risks. I would wait for a pullback for a good entry point in this tier 1 asset.

Brief Company Overview

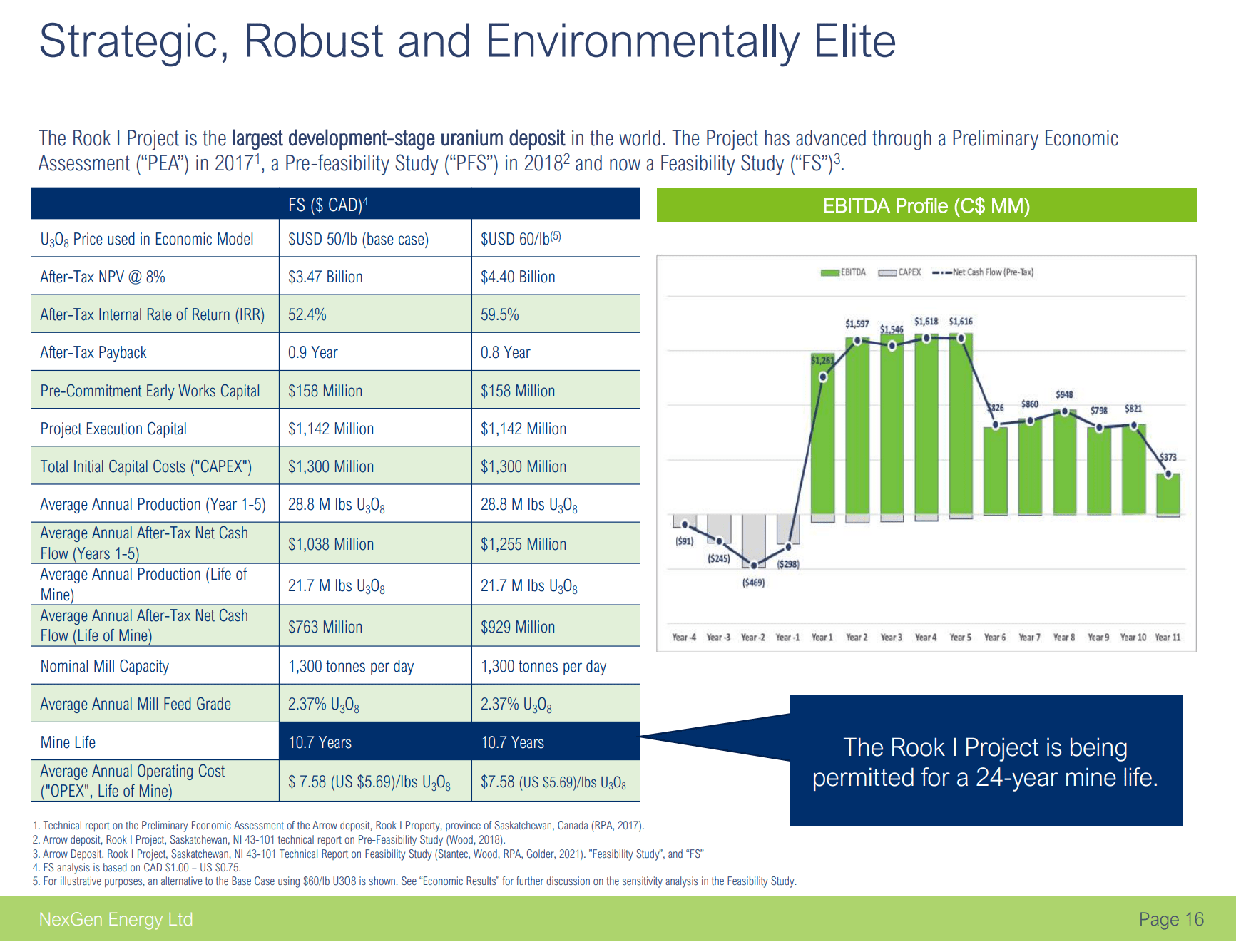

NexGen Energy is a uranium exploration and development company advancing the ‘Rook I Project/Arrow Deposit’ (“Arrow”) in Southwestern Saskatchewan. According to a 2021 Feasibility Study (“FS”), Arrow can generate over C$750 million in average annual after-tax cash flows at US$50/lb U3O8. With C$1.3 billion in capex, Arrow has a C$3.5 billion project NPV and 52% IRR (Figure 1).

Figure 1 – Arrow has robust economics (NXE investor presentation)

Bull Case Scenario Suggests Large Upside

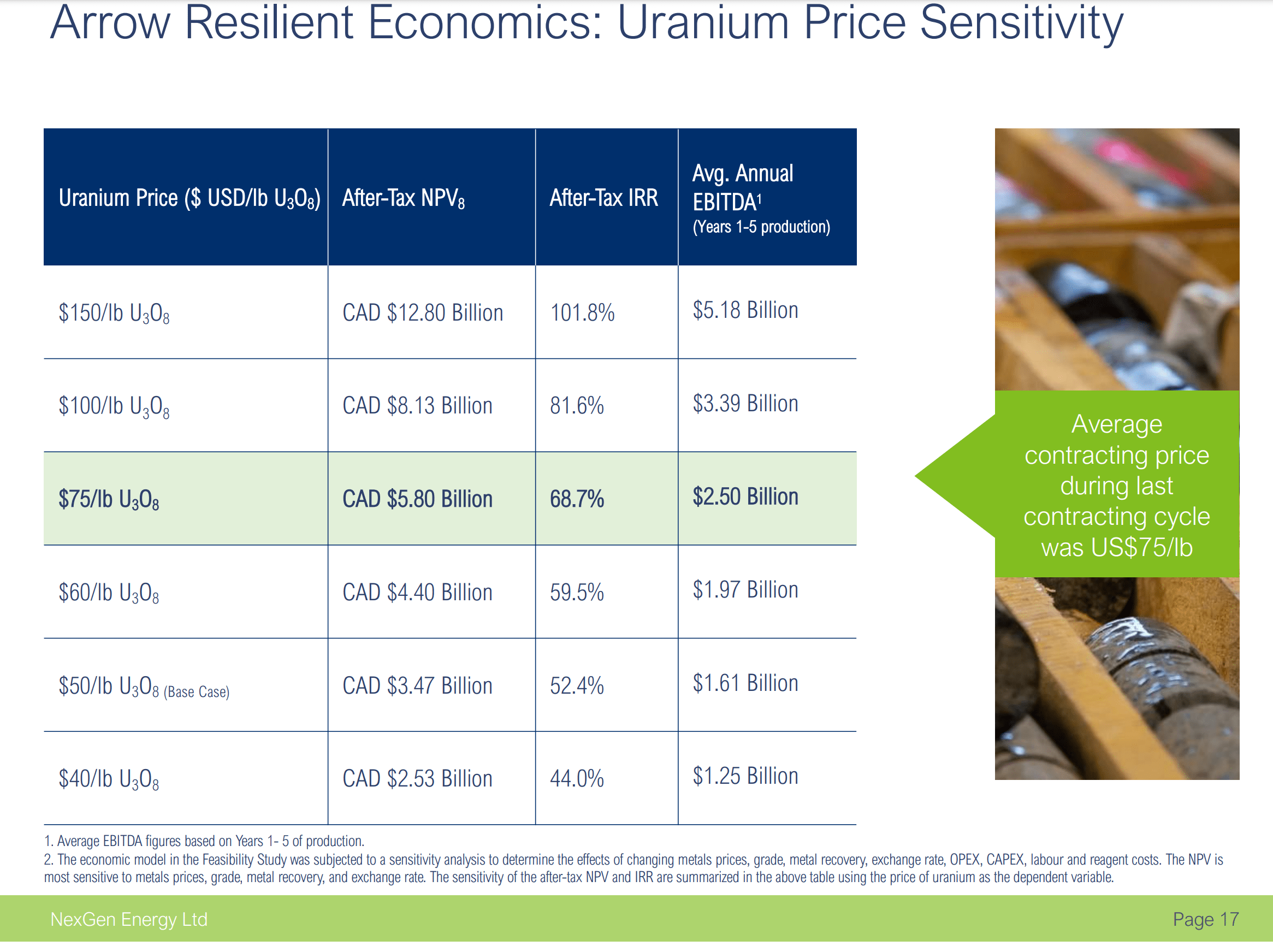

At spot U3O8 prices of ~$50 / lb, Arrow is already a tier 1 project with eye-popping economics. However, what is truly outstanding about Arrow is the project’s sensitivity to higher uranium prices. In a bull-case scenario with sustained $100 / lb U3O8, Arrow’s NPV more than doubles to C$8.1 billion (Figure 2).

Figure 2 – Arrow NPV sensitivity (NXE investor presentation)

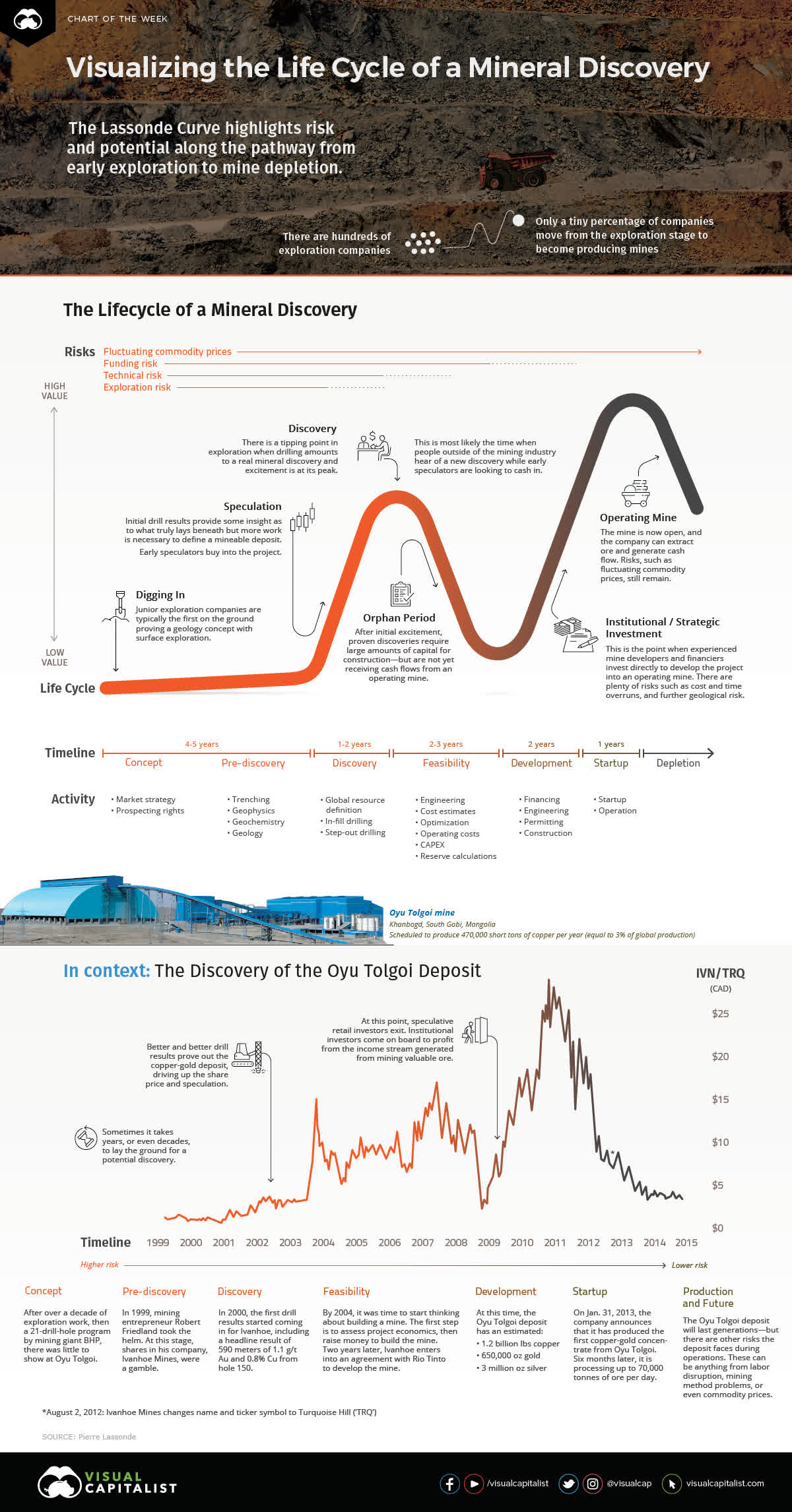

Development Phase Is When Projects Get Delayed

In my prior article, my main concern with NexGen is that it is now entering the long and arduous development phase of any mining project (Figure 3). Typically, the development phase is when mining projects hit engineering and regulatory snags.

Figure 3 – Illustrative Lassonde Curve (visualcapitalist)

For example, Cameco’s (CCJ) Cigar Lake uranium mine initially filed its Environmental Impact Statement (“EIS”) in 1995 and expected first production in 2003. However, construction delays and flooding events delayed first production until 2014, a full decade later than initially expected.

Draft EIS Turnaround Surprisingly Fast For Arrow

Coming back to NexGen and the Arrow project, I was pleasantly surprised to see NexGen announced on December 1st, 2022 that it has received Federal technical and public review comments and Provincial technical review comments on the draft EIS it submitted on July 15, 2022.

The next steps for NexGen is to review the comments and prepare the final EIS for submission to the Saskatchewan Ministry of Environment (“ENV”) and the Canadian Nuclear Safety Commission (“CNSC”) sometime in Q1/2023.

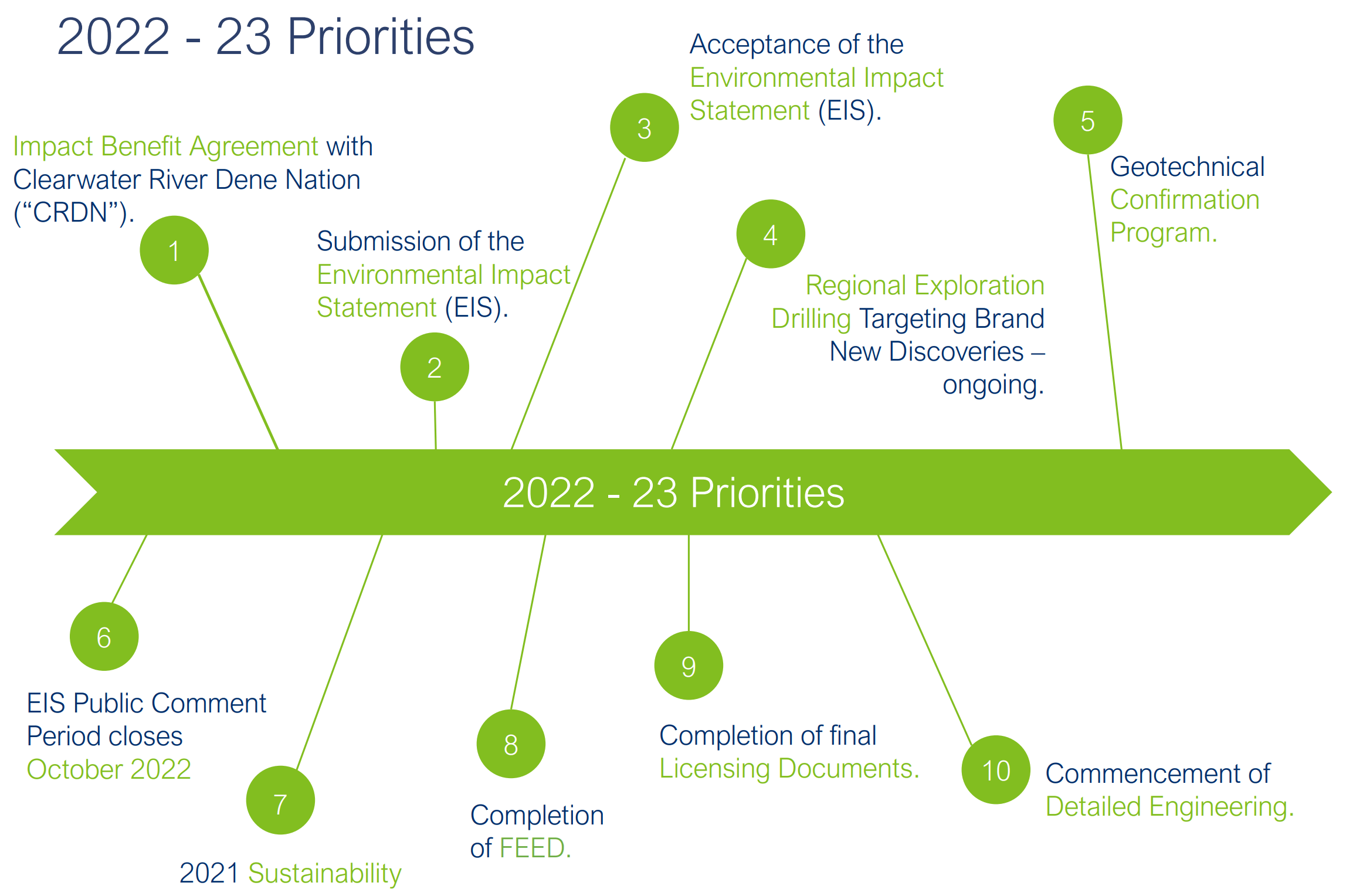

However, investors should note that submission of the final EIS is only one step of many that NexGen will still have to go through in the next year or two before it can begin the actual construction of the Arrow project (Figure 4).

Figure 4 – NXE catalyst timeline (NXE investor presentation)

What Will Actual Capex Be When Arrow Breaks Ground?

Another risk to NexGen is the possibility of a capex blowout, given the soaring cost of labour and materials in the past few years. In recent months, we have seen numerous instances of soaring capital expenditure blowouts for large mining and infrastructure projects in Canada, such as the cost blowout at TC Energy’s (TRP) Coastal GasLink or IAMGOLD’s (IAG) Cote project.

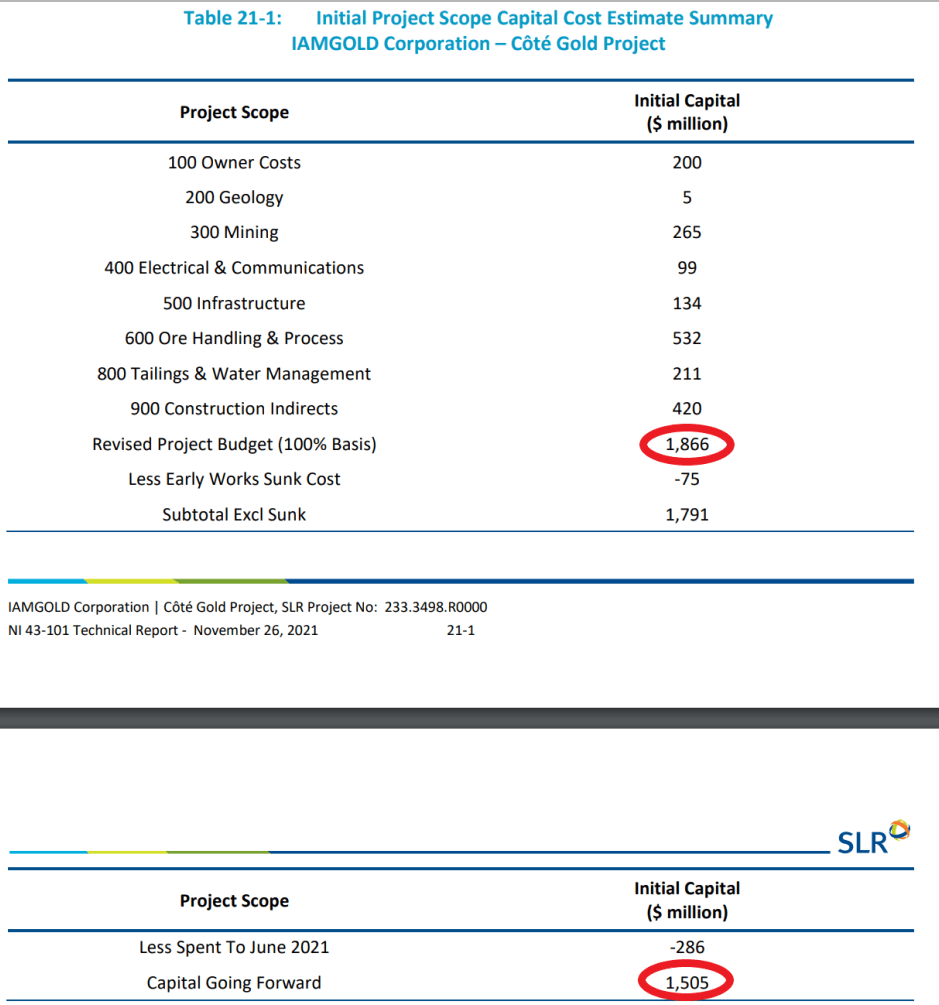

In fact, the Cote project cost blowout may be illustrative of the rise in capex costs experienced in the past few years. Cote is a large-scale gold mining project located in Ontario, Canada. According to IAMGOLD’s November 2021 technical report on Cote, the cost to complete the project was estimated at $1.5 billion, inclusive of $286 million already spent (Figure 5).

Figure 5 – Cote project capex (IAG November 2021 Technical Report)

However, less than 1 year later, in an updated August 2022 technical report, the remaining costs to complete the Cote project had ballooned to $1.9 billion, after $982 million had already been spent (Figure 6).

Figure 6 – Cote project updated capex (IAG August 2022 Technical Report)

Altogether, the Cote project’s budget had been revised from an original $1.9 billion to $3.0 billion, or 58% higher!

While I am not suggesting the Arrow project’s capex will be 50% higher than in the 2021 feasibility study, the analysis above does highlight the significant capex risks in an inflationary environment (Figure 7). Furthermore, the Arrow project is not expected to break ground for at least a few more years, so the actual costs when Arrow is built could be even higher.

Figure 7 – Arrow project capex (NXE Feasibility Study, March 2021)

Current Valuation Is Rich

NexGen currently has a C$3.0 billion market cap, which is approximately 0.85x the C$3.5 billion NPV of the Arrow project, using US$50 U3O8 price. I believe this valuation is rich, given the risks to capex highlighted above, which could reduce the project’s NPV.

The company seems to agree with my assessment, as it recently began an ‘at-the-market’ equity issuance program to raise up to C$250 million in equity.

Risks To My Cautious Call

The biggest risk to my cautious call is that Arrow is such an attractive project that any major mining company would love to have it in their portfolio. Therefore, if equity markets were to weaken significantly or if NexGen de-risks the project to actual construction, I would not be surprised if BHP (BHP) or Rio Tinto (RIO) swoops in and acquires the company.

Conclusion

NexGen owns the tier 1 Arrow project, with eye-popping economics based on its 2021 feasibility report. The company is currently stuck in development limbo as it has to grind through multiple regulatory / development milestones before construction can actually begin on the Arrow project. One big risk to Arrow is a recent spate of mining/infrastructure capex blowouts, which suggests capital costs could be significantly higher for Arrow. Trading at 0.85x P/NAV, NexGen’s valuation appears rich and I would wait for a pullback for a good entry point.

Be the first to comment