BlackSalmon/iStock via Getty Images

Neuronetics (NASDAQ:STIM) is a company with solid growth potential that is valued below its industry. The company is likely to see strong demand for its products from the high prevalence of major depressive disorder [MDD]. Although STIM is not yet profitable, annual losses are expected to decrease over the next few years. In the meantime, Neuronetics is growing revenue at a strong double-digit pace.

Neuronetics produces the NeuroStar Advanced Therapy System for treating those with MDD. NeuroStar is a non-invasive, in-office therapy that treats adult patients with MDD. NeuroStar uses an MRI-strength magnetic field to stimulate specific areas of the brain that are associated with mood.

The company makes its revenue from the sales of the NeuroStar system, sales from recurring treatment sessions, from service and repair, and from extended warranty contracts.

Why NeuroStar is a Needed Therapy for MDD

There is a high prevalence of MDD in the United States. It is estimated that 21 million adults in the United States had at least one major depressive disorder in 2020. A major depressive episode is defined as a period of at least 2 weeks where a person is in a depressed mood or experiences loss of interest or pleasure in daily activities. MDD is associated with symptoms such as negative changes in sleeping, eating, self-worth, concentration, and energy.

MDD is typically treated with counseling and medication. However, for many MDD patients, this falls short on effectiveness. There are those who have treatment resistant depression. This occurs when standard treatments are not enough. That is where NeuroStar therapy can fill the void.

Studies have demonstrated that 83% of patients responded to an acute course of NeuroStar and 62% achieved remission. NeuroStar also has a low discontinuation rate of about 5% from adverse events. The company stated that of the 21 million with MDD, 6.4 million are underserved for treatment due to negative side effects of medications, lack of efficacy, and the increased need for solutions post-COVID. Also, 67% of patients with MDD are unhappy with their current treatment. STIM spent $14.5 million on marketing to bring awareness about the benefits of NeuroStar and how it can help those who need it.

Recent and Future Developments

NeuroStar has been cleared by the FDA for two new indications in 2022:

1. For anxiety in people with depression.

3. For those with obsessive compulsive disorder [OCD].

These new indications can help drive revenue growth going forward. Nearly half of those who suffer from major depression also have severe and persistent anxiety. About 1.2% of adults (about 2.5 million people) in the U.S. have OCD.

Neuronetics also has clinical trials underway for NeuroStar to address anxiety, bipolar disorder, pain, PTSD, addiction, schizophrenia, tinnitus, and others. If these are approved for NeuroStar treatment, then STIM is likely to have an ongoing source of new revenue.

Valuation & Growth

Since Neuronetics is not yet profitable, it makes sense to use the price/sales ratio to evaluate the stock’s valuation. Neuronetics is currently trading with a trailing price/sales ratio of 2.36 and a forward price/sales of 1.92. The forward price/sales is based on expected revenue of $73.59 million for 2023. That revenue target would equate to about 15.7% annual growth over 2022.

Neuronetics is trading attractively 43% below the Diagnostics & Research industry’s trailing price/sales ratio of 4.17. So, I see STIM trading at an attractive valuation which leaves room to the upside for the stock.

EPS losses are expected to decrease annually at a double-digit annual percentage pace. So, the company should be able to achieve profitability a few years down the road – probably sometime in the second half of the decade. In the meantime, the stock is likely to respond to sales growth and widening gross profit margins.

stockcharts.com

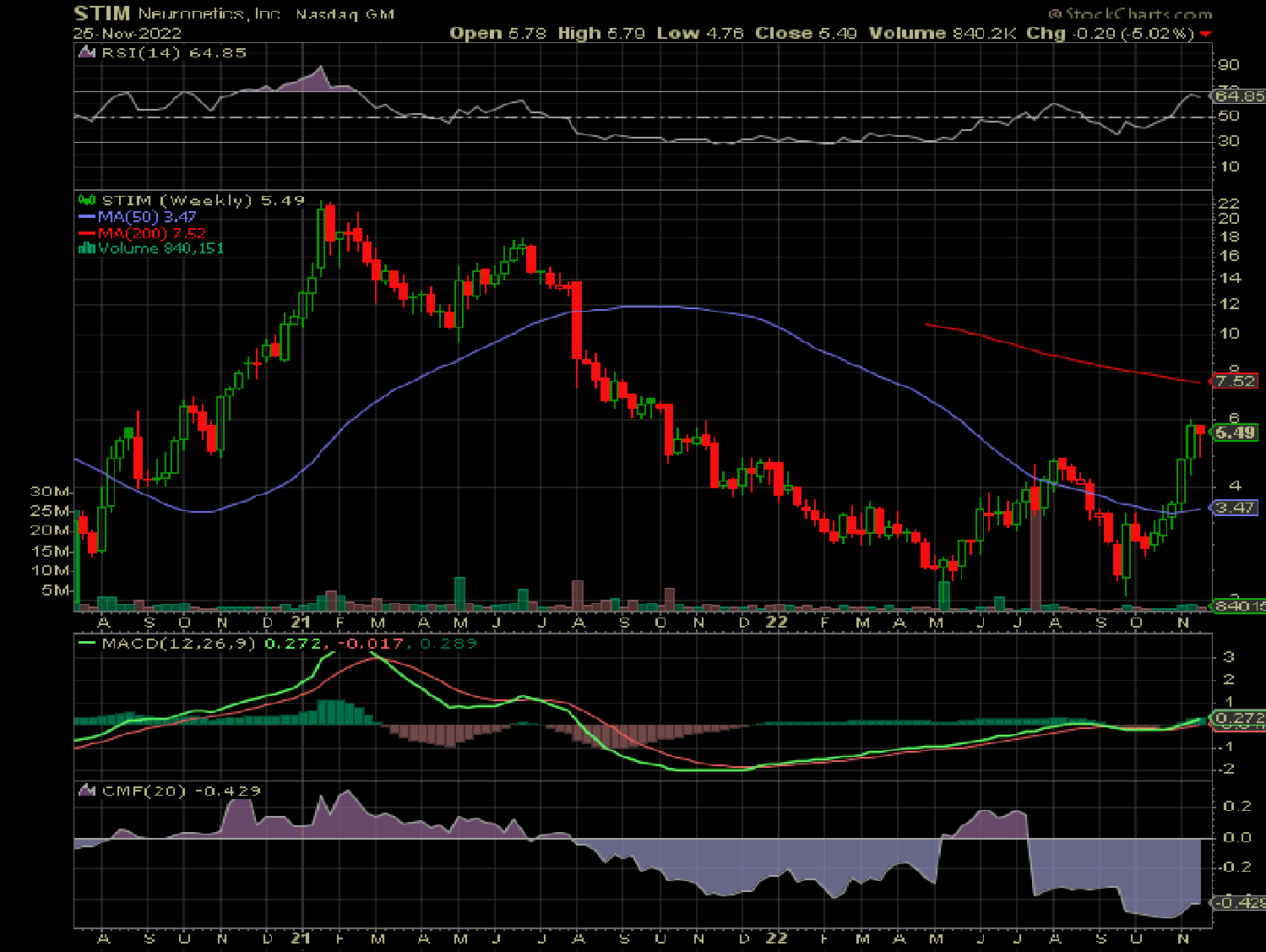

STIM’s weekly chart above shows the stock price making one higher low and two higher highs from a previous oversold condition. The RSI moved above 50, and remains below the overbought territory of 70 or higher. The green MACD line rose above the red signal line and the zero line, indicating that the trend is positive. The money flow [CMF] increased slightly from a low point, leaving more possible room to the upside. Overall, the trend looks positive. The positive trends on the weekly chart indicate that a long-term rally could occur over the next few months.

Patient & Geographic Growth Potential

Neuronetics plans on increasing the amount of patients at each NeuroStar site. Currently, there are about 2.5 patients per site per day. The company plans on increasing this to 4 or 5 patients per day per site. However, the company didn’t mention the time frame to reach that goal. I would just consider it a long-term, multi-year goal at this point.

Increasing the amount of NeuroStar treatment sites is another avenue for growth. Neuronetics currently operates in the United States and Japan. There are opportunities for the company to continue to increase the amount of offices that offer NeuroStar treatments in these countries. Of course, efforts can be made to expand into new countries for ongoing long-term growth. That would involve regulatory approvals for each region. Overall, these efforts have the potential to provide many years of growth for Neuronetics.

Balance Sheet

Neuronetics has a strong balance sheet with $73.7 million in total cash and $39.7 million in total debt. Having more total cash than debt gives STIM financial stability. There are 4x more current assets than current liabilities and 2x more total assets than total liabilities for a total equity of $63 million.

The strong balance sheet should enable the company to weather any unexpected storms that may come its way. It also puts the company in a great financial position as it strives to achieve profitability over the long term.

Neuronetics – Long-Term Outlook

Neuronetics has positive momentum with its business, with a likely path for ongoing growth. The company has a good chance to achieve double-digit revenue growth for multiple years. This can occur through increased patients in existing NeuroStar locations, increased locations in existing and new regions, and with new indication approvals.

One key risk for the company is that a possible recession could lead clients to halt spending on NeuroStar equipment. However, mental health patients are likely to seek treatment regardless of the economic situation. If more people start losing their jobs as part of a recession, then there might be more mental health patients demanding treatment.

The stock is valued below its industry average, leaving more room to the upside. Analysts have a one-year price target of $10 for the stock, which represents an 82% gain from the current price. This can be driven by strong revenue growth from a low valuation and from new milestones as new indications become approved.

Be the first to comment