Stephen Chernin

The tech sector has fallen out of favor in a big way of late, with the Nasdaq 100 falling by over a third since its 2021 peak. The last article I wrote on the NDX was back in January 2021, where I argued that the growth outlook was turning negative, and since then the index has fallen over 10% even in total return terms. While valuations may have fallen, they remain expensive in the context of weaker future growth, and free cash flows are painting a much more negative picture of earnings. The path of least resistance remains lower for the NDX, but I have covered my short positions, favoring long positions in bonds to hedge against a decline in my long equity positions.

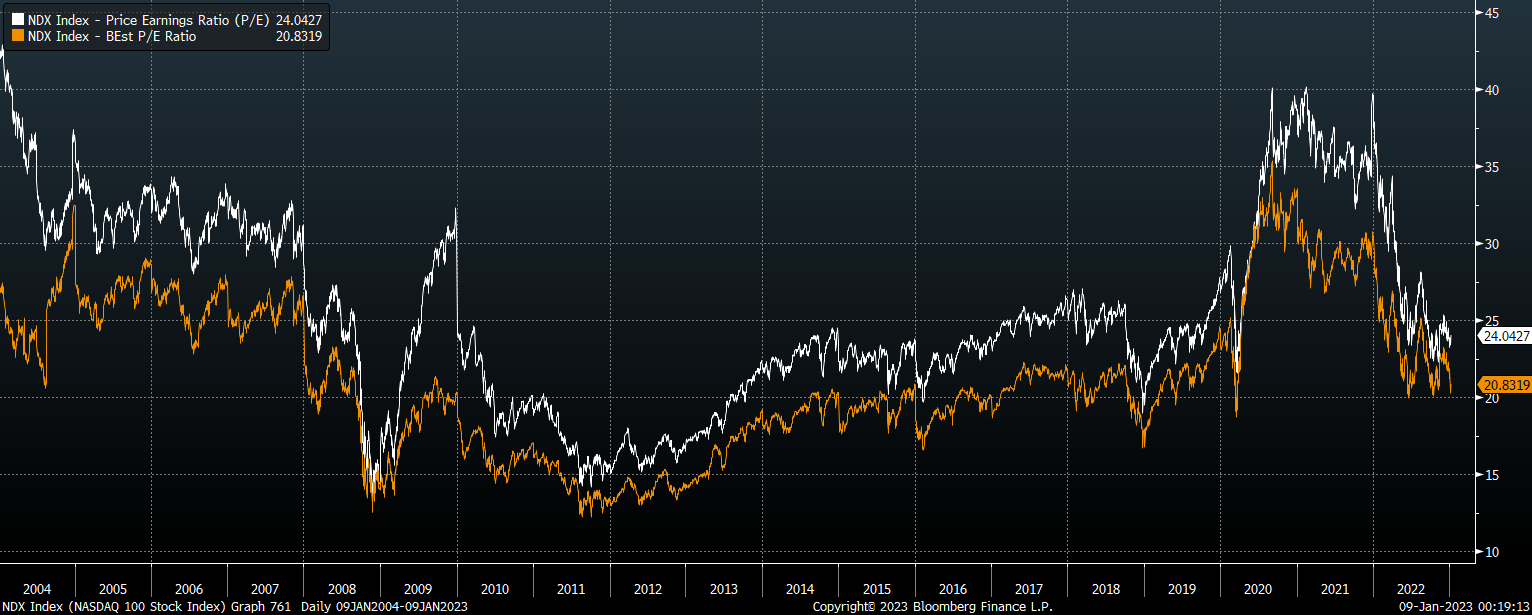

Price-To-Earnings Ratios Have Come Down Significantly But Remain High

From a peak of over 40x the trailing PE ratio on the NDX has now fallen to 24.8x, while the forward PE has fallen from 35.0x to 20.8x. However, discounted does not always mean cheap, and while these kinds of valuations represented a screaming buy for the NDX a decade ago, the growth outlook is significantly worse now.

NDX: Trailing And Forward PE Ratios (Bloomberg)

NDX earnings have almost tripled over the past 10 years, fueled by collapsing US savings rates and a growing market share in many companies that are now market leaders. As I argued in ‘NDX: Big Tech’s Growing Pains And The Risk Of The Repeat Of 2000-2002 Decline‘, these two forces suggests that growth will be significantly slower over the coming years, much more closely in line with nominal GDP. With 10-year breakeven inflation expectations at just 2.2% and structural real GDP growth declining, this is likely to be no higher than 3% annually. In order for investors to achieve historically-average returns of 10% going forward, the dividend yield would need to rise to around 7% from the current 1%. Even a move to half of this level would require a decline in the NDX of over 70%, all else equal.

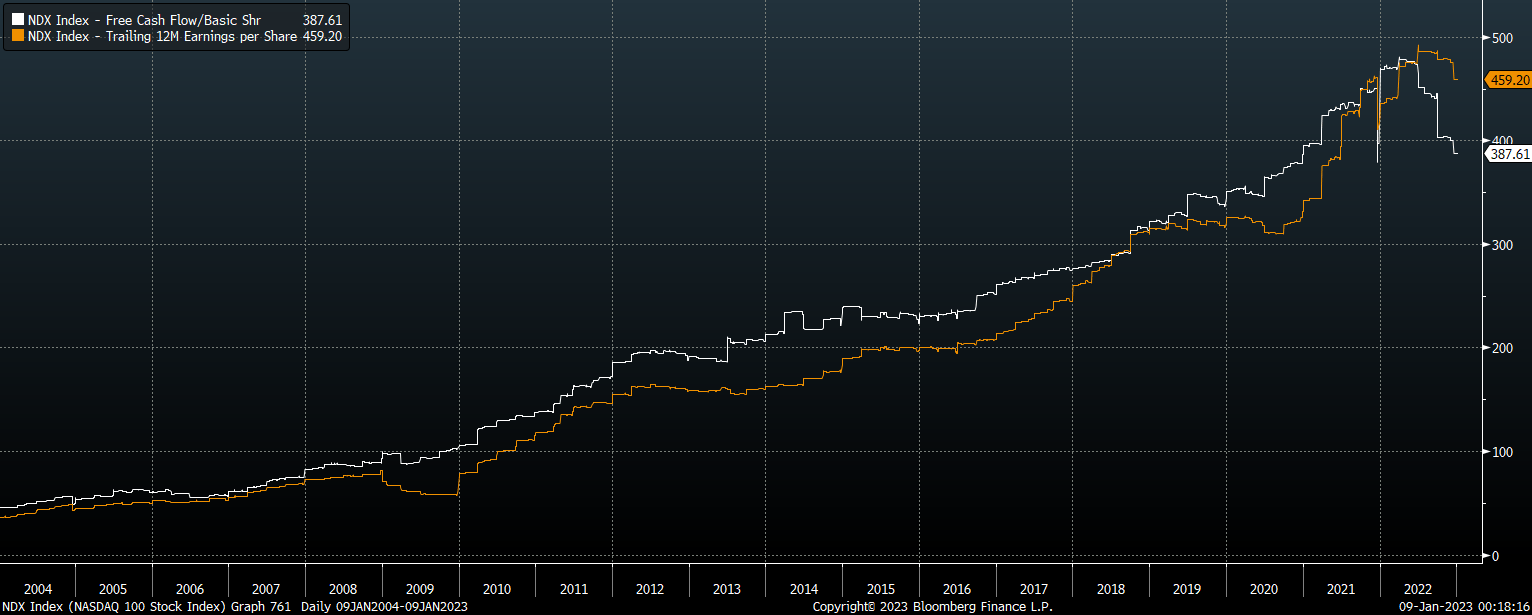

Free Cash Flows Paint A Bearish Picture

While such a decline seemed unthinkable just a year ago, this collapse in free cash flows across the tech sector reminds us that no company or sector is immune from economic weakness. Free cash flows have fallen by 20% since last year’s peak, largely thanks to rising capex costs. I noted last year that elevated accounting earnings partly reflected the temporary positive impact of artificially low depreciation costs on earnings, arguing that free cash flow was a better indicator of true earnings.

NDX: Free Cash Flow Vs Earnings (Bloomberg)

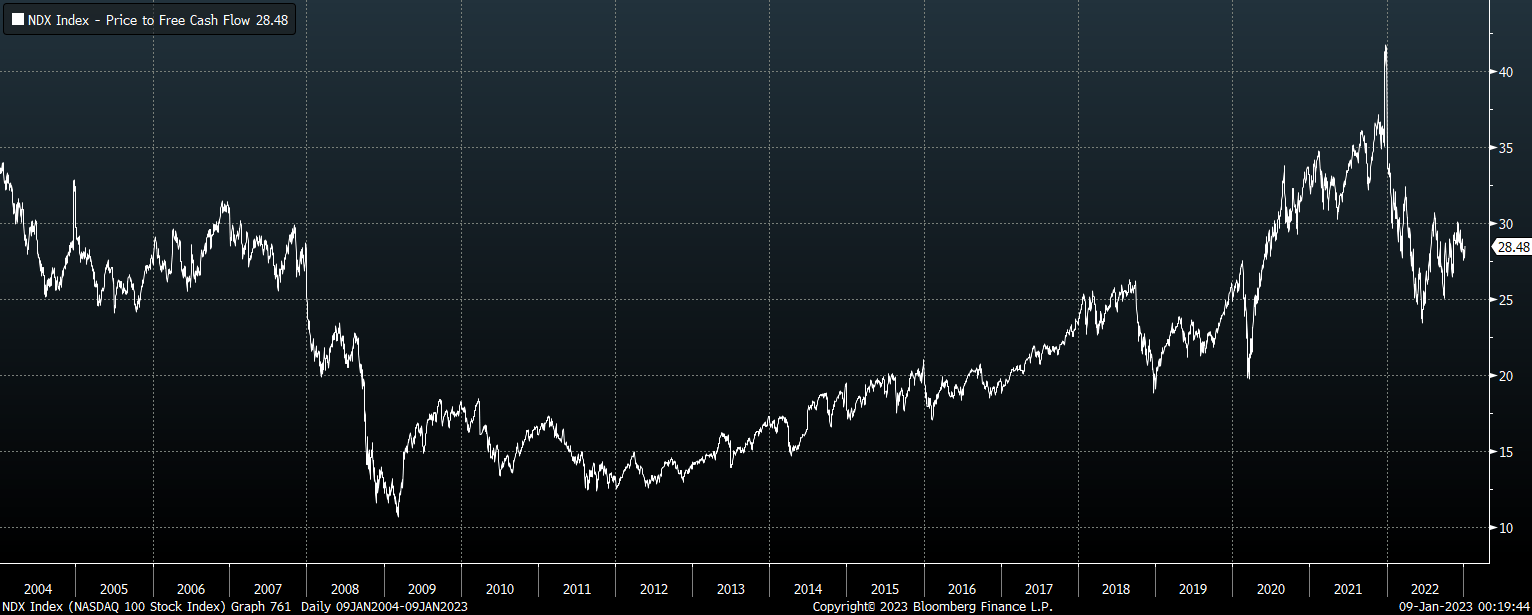

On this metric the PE ratio rises to 28.5x, significantly higher than the official PE ratio. The decline in free cash flows appears to be at least partly structural as sales slow in response to market saturation and margins decline amid rising labor costs and a narrowed fiscal deficit. However, it also reflects the slowdown in the economy, showing that the Tech sector is not immune from economic weakness. A deep recession or another credit crunch could easily see the NDX fall by another third in 2023 as free cash flows and valuation multiples head lower. Just as accelerating earnings allowed investors’ greed to drive up valuations in anticipation of perpetual rapid growth, falling earnings are likely to drive them down due to fear of continued weakness.

NDX: Price To Free Cash Flow (Bloomberg)

Despite The Negative Outlook, I Am No Longer Short

While I continue to see further losses in the NDX I am no longer net short the tech sector. I was aggressively short tech stocks during much of the 2021-2022 period as not only were they extremely expensive, but there was also no easy way to hedge long positions, predominantly in international and commodity related stocks. However, with equity valuations falling and bond yields rising, the opportunity cost of shorting has increased and I favor long positions in bonds to hedge against a decline in my long equity positions.

Be the first to comment