Serenethos

As the title already suggested, Blink Charging (NASDAQ:BLNK), which manufactures and distributes charging stations for all-electric and hybrid vehicles, has multiple positive catalysts as it heads into 2023 and beyond.

These are divided into 2 groups, industry-wide and company-specific. The former may affect most companies operating in the sector while company specific factors benefit Blink Charging specifically, where they may be the largest beneficiary or have an outright advantage over competitors.

Since there are multiple companies, which we’ll use for peer comparison later in the article, it’s important to paint a somewhat detailed picture of the how each company is faring when it comes to the various factors affecting sales and income. While the industry still has much room to grow and as a result many companies may do well, we’re here to beat the market, after all.

Industry-Wide Catalysts: Investments, Improvements & Spending Fueling Industry

There are several factors which are affecting the industry overall. The number one factor though is, simply put, the need for charging infrastructure. Now, duh, right? It’s not just that you need more chargers because more all-electric vehicles are on the road now – we need more charging stations FOR more vehicles to make it on the road.

The number one hurdle to a full all-electric of plug-in hybrid adoption, at least in the United States, is that with the limited 300-mile range of most all-electric vehicles, they may be perfect for set-distance commuters but it’s far from ideal if you live anywhere outside a big city and either have long commutes or want to use your car for road trips, long work stints and the likes.

Therefore, all levels of government and private industry are investing heavily in deploying as many charging stations as possible.

On the private sector side, buildings both commercial and residential are covering the costs of installing these chargers so they can lure in customers and potential residents who own all-electric vehicles. There has been a trend in recent years to visit the local grocery store just to charge your election vehicle. These deployments follow 2 models: the first is the charging station company will sell the stations to the properties and the property provides free charging and the other is that the company would cover the cost of the station and have a revenue sharing agreement for payments made to charge the cars.

On the public sector side, governments are including funding in various infrastructure and transportation bills to expand the charging networks to encourage electric vehicle adaptation. In the United States, the industry’s fastest growing region, the Biden administration and Congress passed a $5 billion fund to help states expand their electric vehicle charging stations over the course of 5 years through Department of Transportation and Department of Energy grants.

An Industry Supporting An Industry

The electric vehicle market is expected to report a compound annual growth rate of 17.02% over the next 4 years, through 2027, and reach over $450 billion in revenues. Unit sales are projected to reach nearly 16M units by then, up from an estimated 8.4M units currently on the roads.

The charging station market though, is projected to report a compound annual growth rate of almost triple the electric vehicle market over the same 4 year period and reach over $8 billion in revenues by 2027. Unit sales are projected to double, from roughly 1.4M units to 2.8M units deployed.

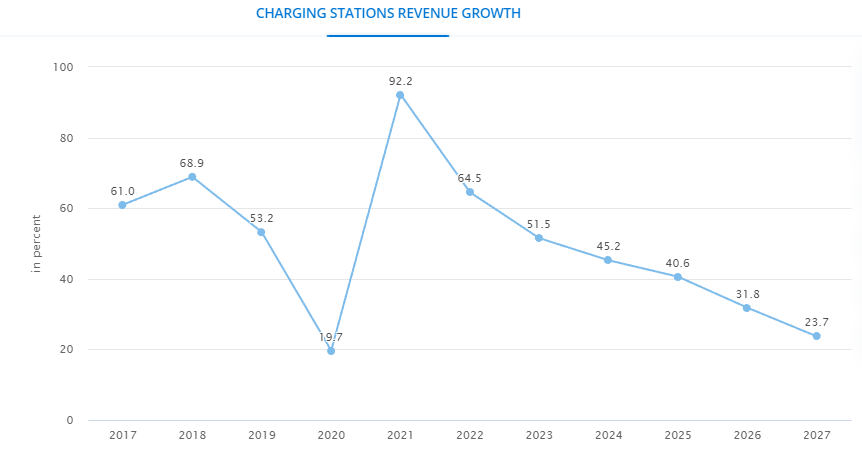

While the growth rates in the charging station and electric vehicle markets are set to pair up by 2027, both growing at just over 20% annually, the charging station revenue is expected to easily outpace that of the electric vehicle one.

Charging Station Revenue Growth (Statista)

The United States is projected to be the fastest growing region at over 22%, followed by Europe (which includes the United Kingdom) at 17% and then Asia with a compound annual growth rate of just under 15%. This is mostly due to the fact that China, the region’s largest electric vehicle market, has already deployed more than 1.15M charging stations while there are around 50,000 in the United States, according to the US Department of Energy. The United States has a long way to go, as well as Europe and the rest of the Asia-Pacific region, which is why the company is making strategic moves in those regions.

Company-Specific Catalysts: Pricing Policy, Partnerships & Earnings Potential

The number one long term catalyst I see is that Blink Charging is currently one of the cheapest options for public charging per kWh or per minute of charging, when compared to its closest competitors like ChargePoint (CHPT) and Tesla (TSLA). While Volta (VLTA) is mostly free with no membership required, the company’s reliance on ads to generate revenue can be volatile and dangerous for a long term investment.

This has 2 distinct implications:

Partnership Potential

Due to the company’s lower overall pricing per kWh (or minute), they have been able to attract more partnerships. There are far too many, albeit smaller, ones to mention here, you can find them in the company’s Seeking Alpha news segment, but the bottom line is that while most companies are similar when it comes to their technology of charging speed and ease of deployment, the cost of charging is set by the company at stations where they purchase the power and then sell it to the consumer.

This gets Blink Charging ‘in the door’, where commercial properties like supermarkets, dealerships, and others look to increase the value to their customers, with an increasing number of them owning electric vehicles, they’ll go for the cheaper option. That’s where the company’s other long term catalyst comes in.

Earnings Potential

Right now, revenue for the company is increasing at a slightly faster rate than competitors given their partnerships agreements whereas their competitors are somewhat more focused on deploying public charging stations. These new partnerships are increasing sales and allowing the company to count on future revenues and deploy public charging stations at various properties in order to generate longer term revenues from charging fees.

This has 2 distinct long term earnings potential implications: The first is that when properties decide which stations to install they are going with Blink due to their lower pricing and the second is that individuals are registering with the company’s app as they’re attracted by the lower pricing.

Since most other companies have either some form of monthly payment or per-session fees, they add up to around $0.25 per minute of charging, or the equivalent per-kWh, while Blink charges around $0.05 per minute of charging.

While there are other factors to consider, this means that Blink can easily double the price of charging later down the line and thus have a stronger long term earnings potential than most of its peers. They can also explore various other plans like monthly subscriptions beyond the ones they currently offer, to enable a steady income stream as more companies enter the market.

Acquisitions Sustaining Long Term Growth

Blink Charging isn’t just projected to grow at a slightly faster rate than its competitors, it’s also in a good financial health position as most companies remain unprofitable and in constant need of cash to deploy new stations.

The company makes about half of its revenues from international markets and has a rather diverse portfolio of partnerships. In just some of the recent news, the company has made 2 main acquisitions in the past year in order to help them penetrate international markets in Europe (the UK) and North America.

They first spent $23.4 million to buy EB Charging, which allows them to operate charging stations in the United Kingdom and potentially other countries across Europe. Early in 2022, the United Kingdom government announced a $2 billion plan to expand the EV infrastructure in the country and increase the number of charging stations to 300,000 over the next 7 years. This is set to drive growth in the industry and region, which Blink can now fully take advantage of due to the country’s rules around international operators.

They then most recently spent around $200 million to acquire SemaConnect, which adds more than 150,000 registered EV users, 13,000 chargers and 3,800 host sites. Given that North America is set to be the industry’s leading growth source over the next few years, this acquisition will add value to the company’s long term prospects.

Beyond the company’s acquisitions, they have partnered with companies like General Motors (GM) to deploy charging stations in the back and front end of their dealerships across North America, which sets forth a long term partnership, meaning that as General Motors grows its EV presence in the North American region, so will Blink Charging’s long term growth.

I believe that these partnerships and acquisitions will continue and that the company will continue to look for strategic moves that may cost them in cash and share dilution in the short run but generate meaningful long term growth.

Financial Health Is Mixed But Good

When it comes to the company’s headline figures, they’ve been seeing some fluctuating and increasing net loss per share. Due to their acquisitions, the company’s headcount went from 91 to 195, which increased compensation expenses as well as stock based compensation in the most recent year totaling more than $19 million, which contributed heavily to their increased net losses.

They currently hold around $57 million in cash and equivalents, after issuing around $230 million in common stock to mostly fund their acquisition of SemaConnect but also to add cash and sustain operations. The positive thing is that the company has stopped issuing more stock to fund these operations since, something which is encouraging as the partnerships begin bringing in more and more revenues.

The company has more than $24 million in inventories which are set to be deployed and delivered over the next few years, which is why analysts currently project a sharp rise in revenues over the next few years, which leads me to the question of the company’s current, fair and future valuation.

Fair Value Provides Potential Upside

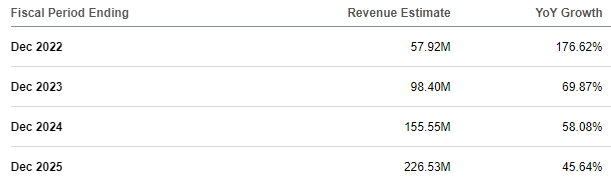

Currently, analysts are projecting that the company will report a 176% growth rate in the coming years revenue, to around $58 million. This is well over the company’s closest competitors, ChargePoint and Volta, which are projected to report growth rates of 98% and 77%, respectively, for the coming year.

Blink Charging Revenue Projections (Seeking Alpha Aggregator)

This points to some near term market share gain, as most companies are projected to currently reach sub-50% annual revenue growth rates by 2025, which is when the market should begin to see most investments already done.

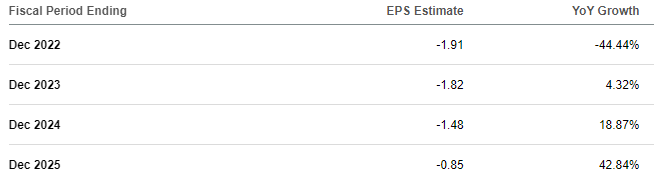

When it comes to profitability, Blink Charging is projected to report some short term headwinds but accelerating growth thereafter. This is mostly due to the aforementioned expenses related to their acquisitions and higher headcounts.

Volta, which uses ads to make their money, are projected to report declining EPS growth rates over the same period that Blink’s is projected to accelerate, even if they are starting out stronger. Volta is not expected to be profitable.

ChargePoint is projected to grow EPS at a higher rate than Blink due to its current subscription based model and their massive number of existing infrastructure. Due to Blink’s potential for raising the price of charging per minute or kWh however, I believe that they have far more flexibility to grow their net income in the long run.

Blink Charging EPS Projections (Seeking Alpha Aggregator)

While all companies remain unprofitable, I like to judge fair value by sales multiples. Comparing to ChargePoint, which generates revenues from the same sources as Blink, the company is expected to grow sales at nearly double the rate but trade at roughly the same multiple.

ChargePoint is projected to grow sales at around 30% in 2025, and is trading at a forward price to sales multiple of 2.06x.

Blink Charging is projected to grow sales at around 46% in 2025, and is trading at a forward price to sales multiple of 2.53x.

If we more or less equalize the price to multiple rations, Blink is projected to grow their sales at 150% times the rate of ChargePoint, which projects a fair value at a 3x price to sales multiple – meaning the company is undervalued by as much as 20% at current levels.

Conclusion: Short Term Growth, Long Term Value, Especially Relative To Peers

One of the most encouraging things we’re seeing right now to support my thesis is that while the company continued to underwhelm when it comes to profitability, they are outperforming expectations when it comes to revenues on behalf of acquisitions and partnerships.

Since the market is currently looking at profits more than growth in the sector, it’s encouraging that the company’s faster revenue growth means that they’re gaining market share at a faster rate than others, which will provide for longer term value as the industry sees the implementation of higher overall spending.

Given the aforementioned factors, I believe that Blink Charging is currently the best choice in the EV charging station industry as it grows revenues at a faster rate than its peers and has better long term earnings growth potential due to their pricing models.

With them being undervalued by as much as 20% at current levels and projected to grow at mid-double-digit rates over the next 5 years, I believe that the company will easily outperform the broader market and is likely to outperform peers.

I remain increasingly bullish on the company’s long term prospects and will be adding to my long term position throughout the coming week.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment