Vertigo3d

Introduction

Following many tough years for the natural gas industry in the United States, it seems low prices are finally an issue of the past following the events in Eastern Europe in 2022 as the Russian army rolled into Ukraine and set off a chain of reactions leaving Europe short of natural gas. Despite this structural change, many companies in the industry are still scarred by excessive leverage after fighting for survival but not Natural Gas Services (NYSE:NGS), who is actually perfectly capitalized to take advantage of this rising tide.

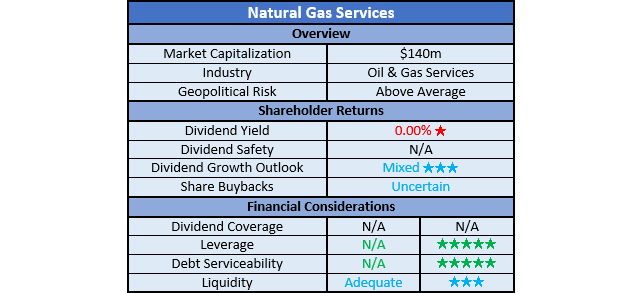

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

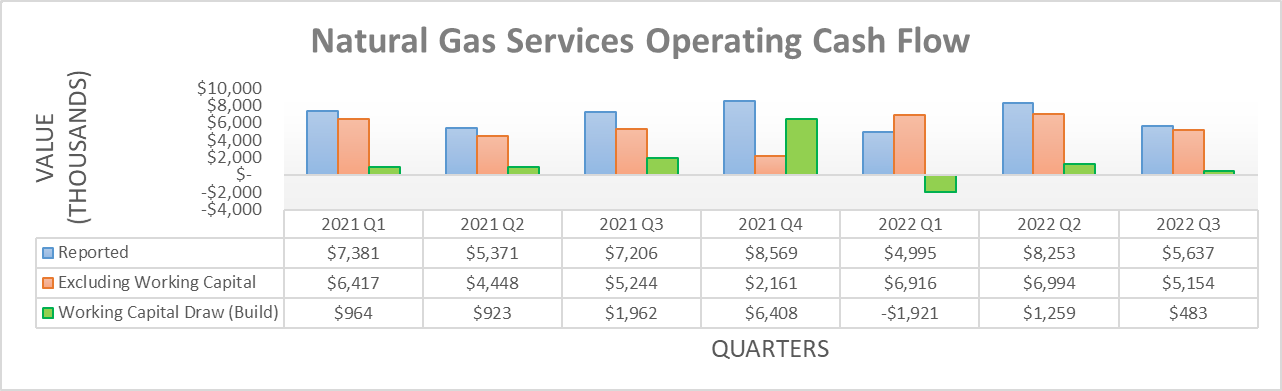

On the surface, their cash flow performance during their recent history does not appear too inspiring nor overly interesting with their operating cash flow fluctuating quite narrowly between a low of $28.5m and a high of $32.6m during 2019-2021. Subsequently, the first nine months of 2022 saw this continuing with their result of $18.9m down slightly year-on-year versus their previous result of $20m during the first nine months of 2021.

Author

If viewing their operating cash flow on a quarterly basis, it shows improvements during 2022 when excluding their working capital movements that make results more volatile on a quarter-to-quarter basis. To this point, the first and second quarters saw underlying results of $6.9m and $7m respectively, both of which are materially higher year-on-year versus their previous equivalent results of $6.4m and $4.4m during the first and second quarters of 2021, respectively. Whilst the third quarter of 2022 saw its underlying result of $5.2m effectively unchanged year-on-year, this was only due to severance expenses of $1.3m relating to the departure of their CEO. If not for this abnormally high expense, their underlying operating cash flow would have been $6.4m and thus once again materially higher year-on-year.

When all is said and done, thus far 2022 saw a strong start as natural gas prices surged but it would be prudent for investors to also remember there is an inherent lag between natural gas prices, drilling and then finally, demand for their compression and associated equipment. Since they are down the end of the production chain, it means their best days should still lay ahead, especially given the bullish medium to long-term backdrop for natural gas.

There are good reasons to expect natural gas production in the United States will continue growing in the coming years, thereby lifting demand down the production chain and thus as a result, their cash flow performance. To begin, they have been investing aggressively given their size, as observed by their capital expenditure during the first nine months of 2022 of $35.3m far outstripping their accompanying operating cash flow of $18.9m. This built upon 2021, when they deployed almost their entire operating cash flow of $28.5m into capital expenditure of $25.7m.

Even more importantly, the United States is well positioned for a surge in natural gas production during the coming years as Europe moves to source their vast supply outside of Russia following the invasion of Ukraine. Whilst this was initially driven by a wish to punish Russia economically, it is increasingly becoming a matter of necessity as Russia reduced their own exports, fighting back against other sanctions levied by Europe. Not to mention, the apparent sabotage of the Nord Stream pipelines a couple of months back further raises the stakes in this pivotal geopolitical moment in history. This is obviously a momentous task that will take many years, which the United States is well suited to help fill via LNG exports given their vast resources and business-friendly environment.

This is not to say natural gas prices can only go higher but in theory, it should enhance long-term demand and thus reduce both the severity and length of any downturns, thereby creating a bullish future backdrop for production. It remains too early to ascertain the magnitude of benefit the United States gas industry will see but suffice to say, a rising tide lifts all boats, plus at the company level, they are perfectly capitalized.

Author

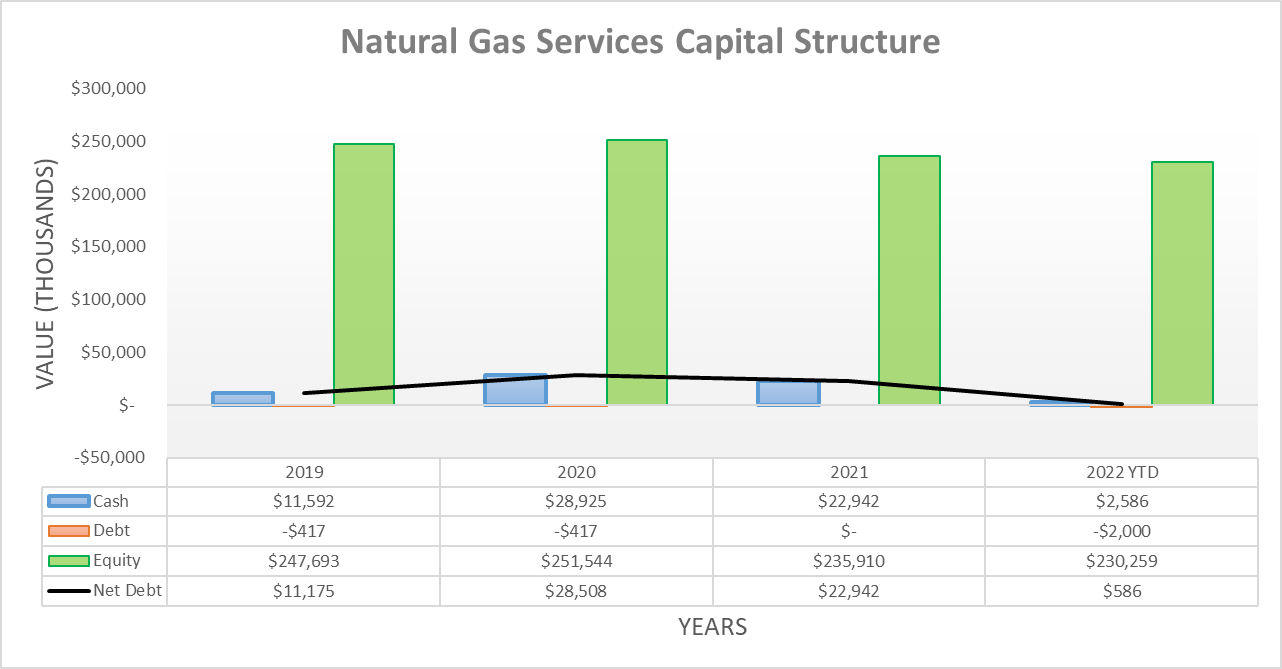

Even though their cash flow performance still needs to see further improvements, at least their capital structure sees them perfectly capitalized with their tiny $2m of debt being more than canceled out by their cash balance of $2.6m. Since this obviously leaves a net cash position of $0.6m, it would be pointless to assess their leverage or debt serviceability in detail, as it would be impossible for either to house any problems.

The absence of any net debt would normally create a strong outlook for dividend growth, although at the moment it remains mixed, largely dependent upon whether they scale their growth investments and thus capital expenditure higher with their financial performance. Interestingly, their balance sheet equity of $230.3m is significantly higher than their current market capitalization of approximately $140m, which effectively means that investors can buy their net assets for less than their accounting value. Admittedly, the accounting value of assets is not always perfect but at the same time, this is a rare opportunity for a company that sports zero leverage as normally companies trade with a premium over their balance sheet equity value. To provide an example, CSI Compressco (CCLP) whom I recently covered in my other article, carries a current market capitalization of approximately $190m but sees balance sheet equity of negative $20.3m, largely due to their very high leverage.

Author

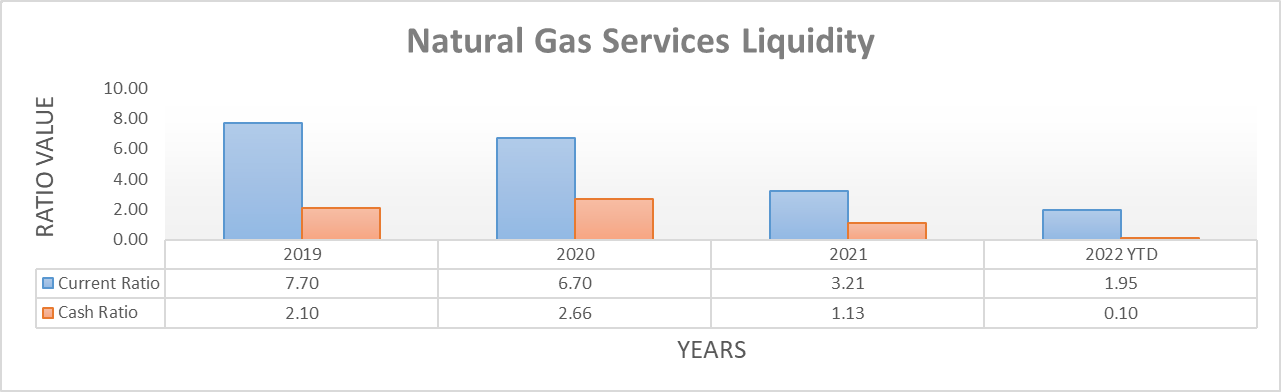

Quite unsurprisingly, their non-existent leverage is also matched by adequate liquidity, as primarily evidenced by their current ratio of 1.95 and cash ratio of 0.10. Whilst they obviously do not have to worry about debt maturities, their ability to access more capital is still important, especially as a very small company. As it stands right now, they only have $18m available from their $20m credit facility and thus going forwards, it will be important to monitor because they conducted $6.7m of share buybacks during the first nine months of 2022, despite their negative free cash flow.

Whilst their credit facility could have another $10m extended subject to collateral availability, this is still only fairly minor in the grand scheme, especially if they continue share buybacks. In theory, they should be able to access substantially more debt given their lack of leverage and ample balance sheet equity, although this will still need monitoring given the rapidly tightening monetary policy that is pulling liquidity from debt markets.

Conclusion

The future remains uncertain, although the outlook for natural gas demand in the United States has seldom been more bullish and thus by extension, the same can be said for production. Since they have zero leverage to address, they are perfectly capitalized to take advantage of this rising tide as their cash flow performance continues improving by either rewarding their shareholders or ramping up growth investments to capture market share. When combined with their balance sheet equity sitting significantly above their current market capitalization, there should be sizeable upside potential on the horizon and as such, it should not be surprising that I believe a buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Natural Gas Services’ SEC Filings, all calculated figures were performed by the author.

Be the first to comment