lucky-photographer/iStock Editorial via Getty Images

Introduction

The market is down roughly 20% year to date while I’m writing this. Nasdaq Inc. (NASDAQ:NDAQ) is down 26% as it was one of the biggest beneficiaries of the stock price rally that occurred after the pandemic sell-off in 2020. However, Nasdaq is different. The company is a high-quality growth stock with a fantastic business model, high growth rates, a decent dividend yield, high dividend growth, and a valuation that makes investments at current prices attractive. In this article, I will explain why dividend growth is so important, why sell-offs offer great opportunities, and why Nasdaq is one of my all-time favorite dividend stocks.

So, bear with me!

Prioritizing Dividend Growth

I’m afraid that this is going to be one of these articles that loses a lot of high-yield-oriented readers right from the beginning. After all, we’re dealing with one of the best examples of dividend growth instead of a company that makes it possible for retirees to cover costs.

Nasdaq pays a quarterly dividend of $0.60. That’s $2.40 per share per year. Based on its $155 stock price, we’re dealing with a 1.5% dividend yield. That’s just 10 basis points below the S&P 500 yield of 1.60%. However, it’s well below the yield of the Vanguard High Yield Dividend ETF (VYM), which is currently yielding 3.1%.

While there are good reasons to buy (quality!) high-yield investments, I’m going to focus on dividend growth in this article.

With that said, and before I show you any numbers, I believe that dividend growth stocks make sense for every investor with at least 10 years until retirement. This allows dividend growth stock to either build an attractive yield on cost or to accumulate enough capital gains through outperformance that retirees can sell dividend growth and move money into higher-yielding investments.

With that said, I dug into the “scientific” research that I usually use and added a new piece of evidence that builds the case for long-term dividend growth investments.

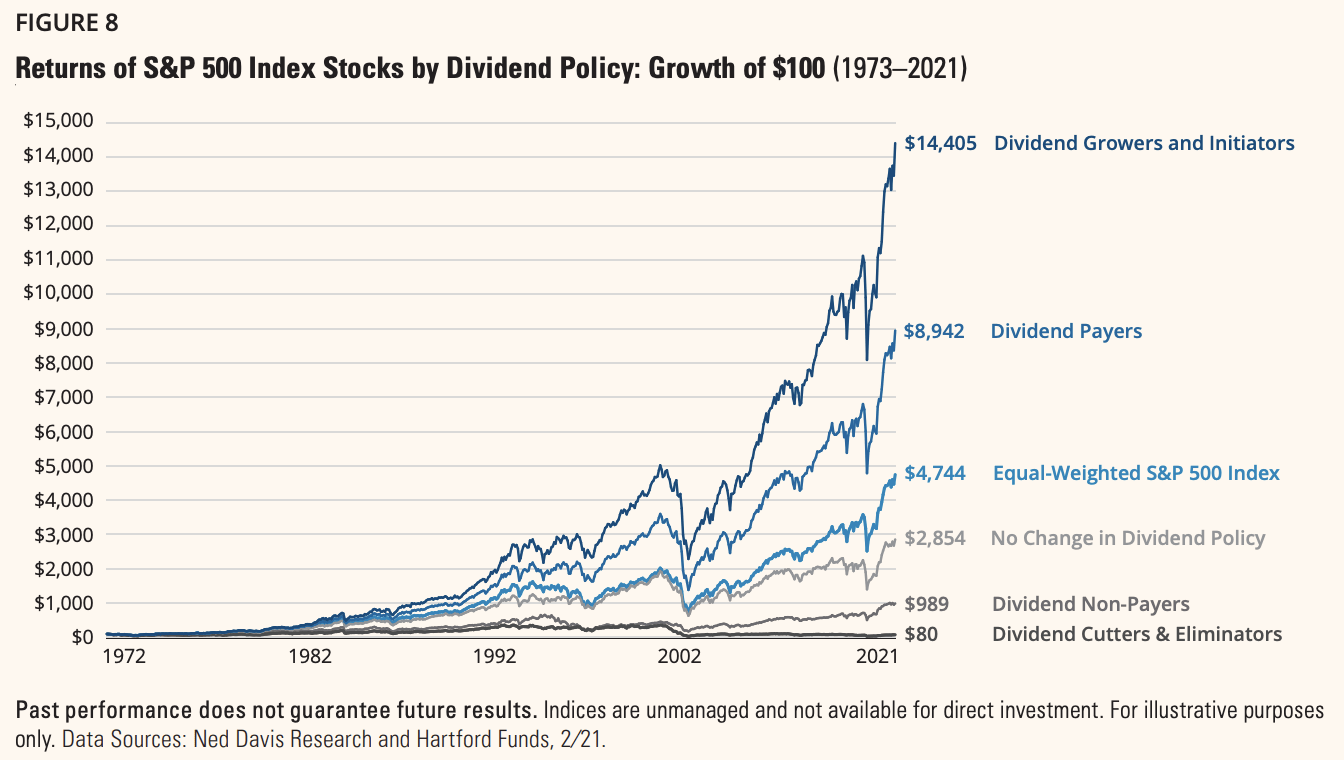

The chart below, for example, has been featured in multiple articles of mine this year. It shows the long-term performance of various dividend categories between 1973 and 2021. What we see is that an equal-weighted S&P 500 investment would have resulted in a $4,655 profit on a $100 investment in 1973. That’s 8.2% per year.

Dividend growers and initiators rose by 10.7% per year. That’s a 250 basis points difference per year, resulting in $10,000 more in profits. On a side note, dividend payers, in general, outperformed the market.

Hartford Funds

Why do dividend stocks do so well?

One reason is quality. A dividend is somewhat of a stamp of approval. According to a recent S&P Global report:

Dividend growth stocks tend to be of higher quality than those of the broader market in terms of earnings quality and leverage. Quite simply, when a company is reliably able to boost its dividend for years or even decades, this may suggest it has a certain amount of financial strength and discipline.

The other reason is low volatility, which is connected to quality. According to the same report:

Dividend growth stocks could be attractive to market participants looking for disciplined companies that can endure difficult market and economic environments relatively well.

[…]

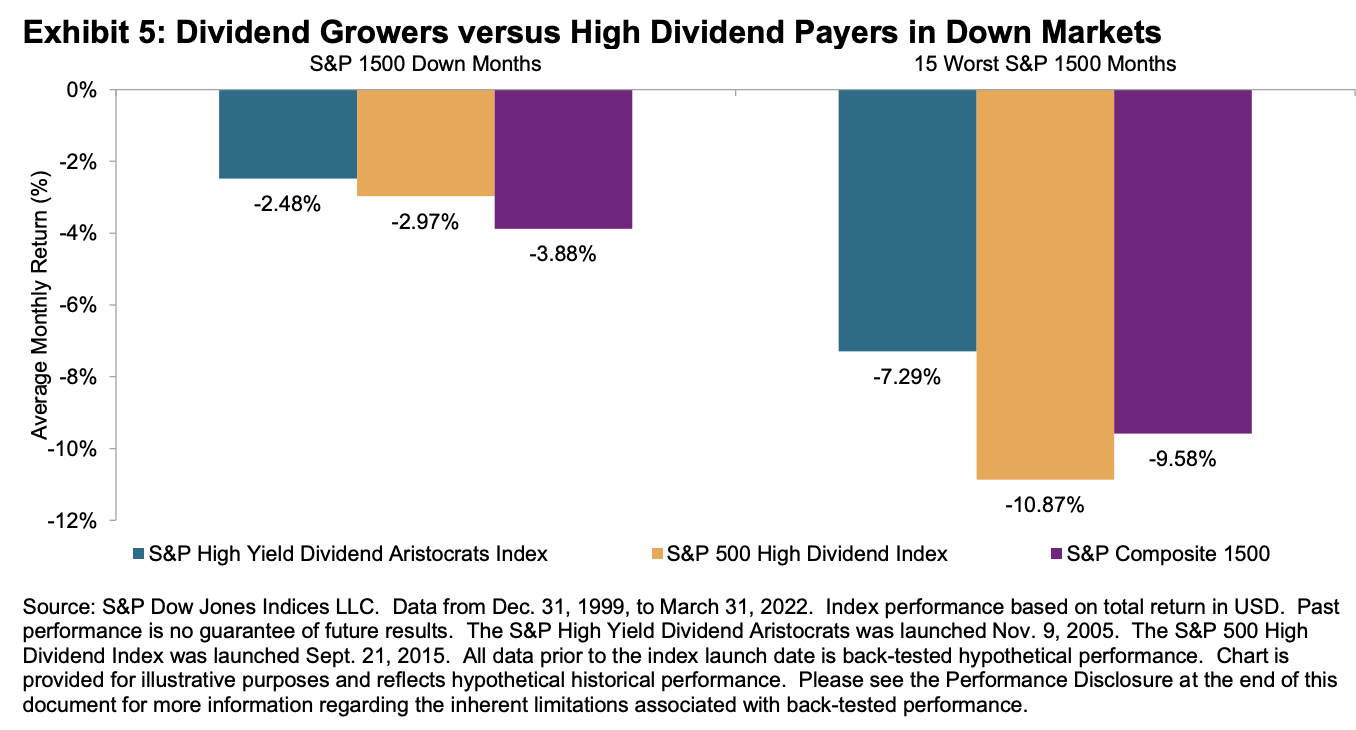

When we focus on the 15 worst-performing months for the S&P 1500 during the same period, the protection provided by the S&P High Yield Dividend Aristocrats was prominent. Its monthly outperformance was 229 bps and 358 bps against the S&P 1500 and S&P 500 High Dividend Index, respectively (see Exhibit 5).

S&P Global

Low volatility is extremely important and often underestimated by investors. While low volatility is always a good thing to have, it’s a blessing during bear markets.

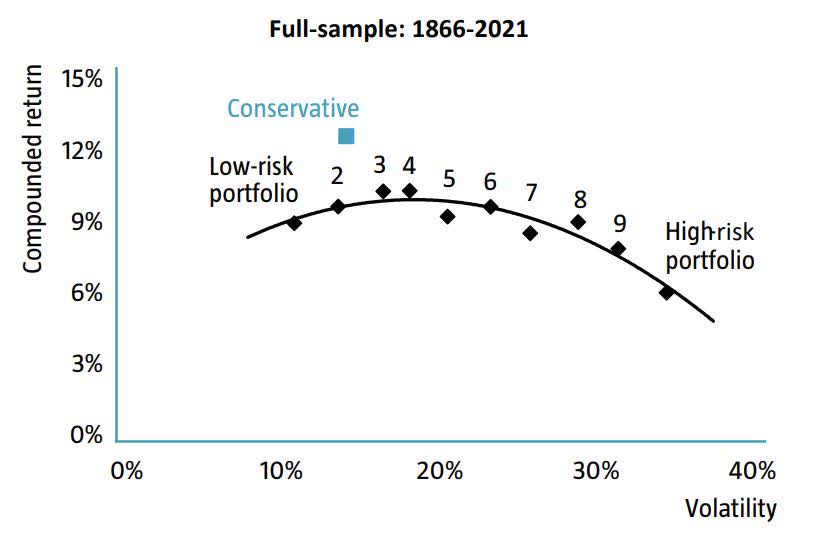

A recent report written by ROBECO shows that the higher the average volatility, the lower the compounded return.

ROBECO

So, why is that? In general, it can be said that low volatility stocks perform better during bear markets. I presented that evidence in this article. When it comes to long-term investing, protecting the downside is key.

Nasdaq confirmed this in its own research, showing that low volatility stocks “crushed” high volatility stocks since 2001.

Nasdaq Inc.

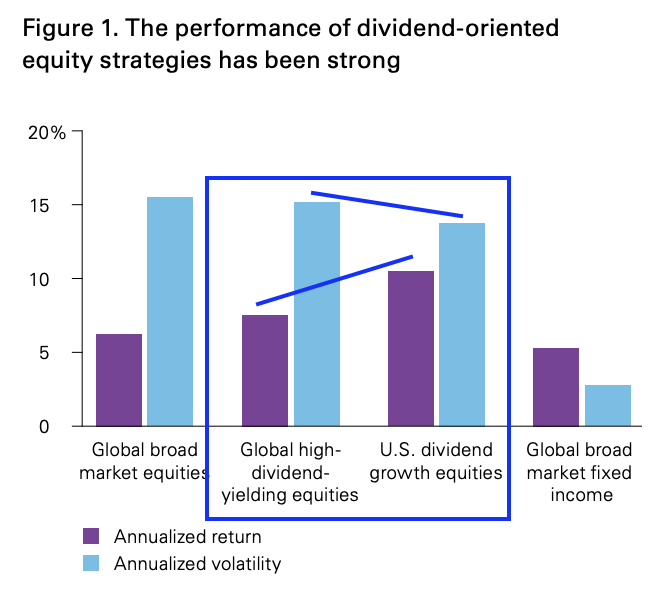

To put all things together, I found the chart below (and modified it a bit). Vanguard found that between 1997 and 2016, both high yield and dividend growth stocks outperformed global equities. Moreover, dividend growth outperformed high yield. And, on top of that, dividend growth stocks did it with lower volatility.

Vanguard

In other words, there’s a very strong case for dividend growth stocks, even if the yield is low and somewhat “unattractive” to some.

Why I Love Nasdaq

With a market cap of $26.0 billion, Nasdaq is one of the largest players in the financial data & stock exchanges industry. I’m a big fan of this industry as I own one of its peers CME Group (CME) and because I’m about to add Intercontinental Exchange (ICE) as well.

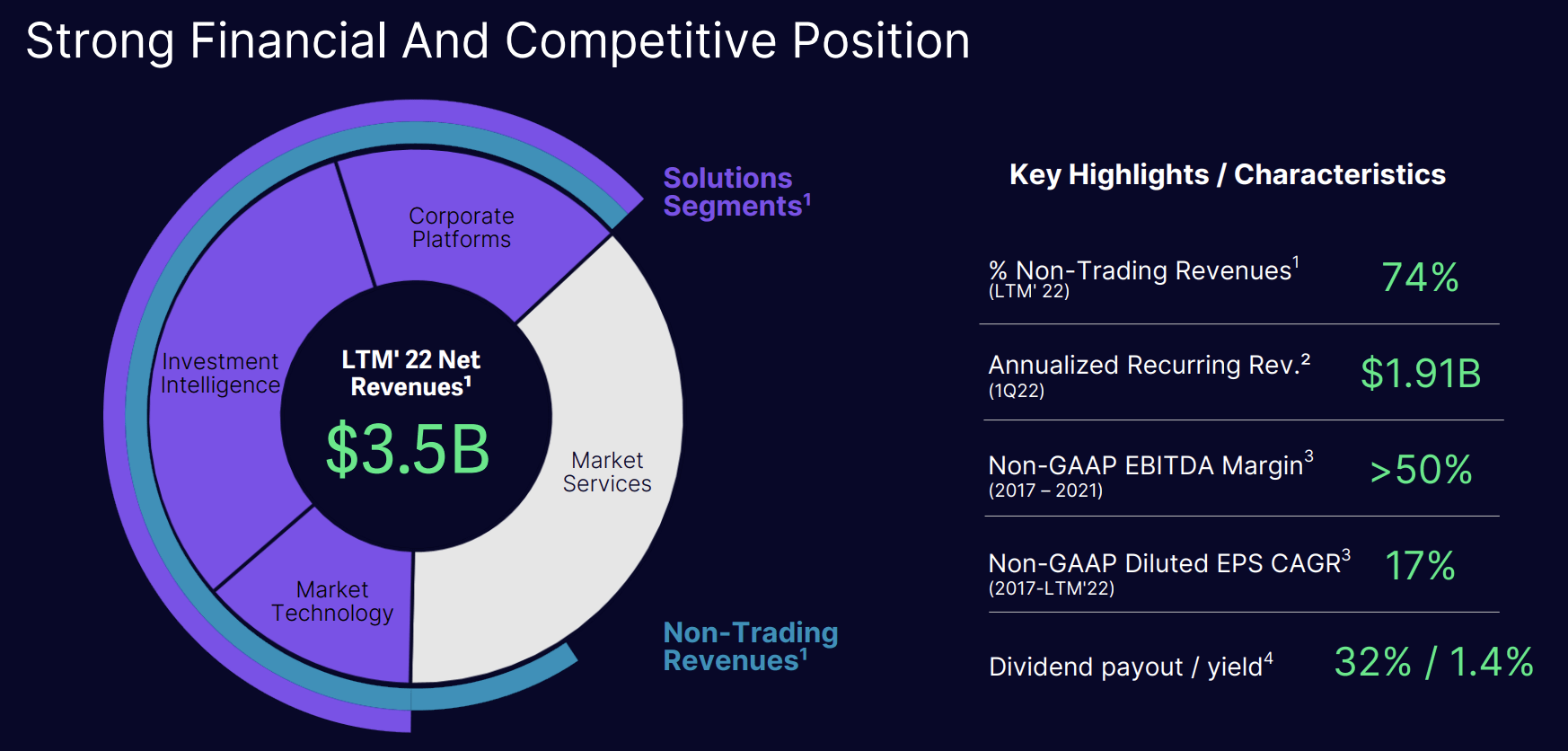

The beauty of owning companies in this industry is that it’s a breeding ground for new services and recurring revenue. Nasdaq, being the owner of major markets like Nasdaq and Nordic (Nasdaq) markets not only benefits from new listings, re-listings, and trading volume, but it also has access to a load of data it can use to create new products.

Hence, 74% of its revenues are from non-trading activities.

Nasdaq Inc.

Between its four business segments, the company owns the biggest US equities venue (Nasdaq), Nordic equities, derivatives like stock options, and futures as well as a corporate platform covering more than 10,000 corporate platforms clients and more than 5,000 listed corporate issuers (excluding ETPs – exchange-traded products).

The company’s market technology and investment intelligence platforms service 2,100 asset managers, more than 1,000 asset owners and consultants, market data clients, and index clients, as well as 2,000 banks and credit unions and more than 170 sell- and buy-side firms.

The strategic pivot to non-trading services (the solutions segment, see the graph above) has resulted in 2x higher organic revenue growth. The average annual organic revenue growth rate was 10% between 2018 and 2018, which is up from 4% in the two years prior to that.

The market technology segment alone is expected to have a total addressable market of $26 billion. On an LTM basis ending 1Q22, the company did $486 million in sales in this segment. A focus on anti-money laundering and fraud solutions, trade surveillance, and complete marketplace solutions is expected to fuel above-average growth.

Between 4Q16 and 1Q22, total annualized SaaS (software as a service) revenues grew by 21% per year. In 1Q22, these sales accounted for 34% of annual recurring revenue. The goal is to get this number to at least 40% by 2025.

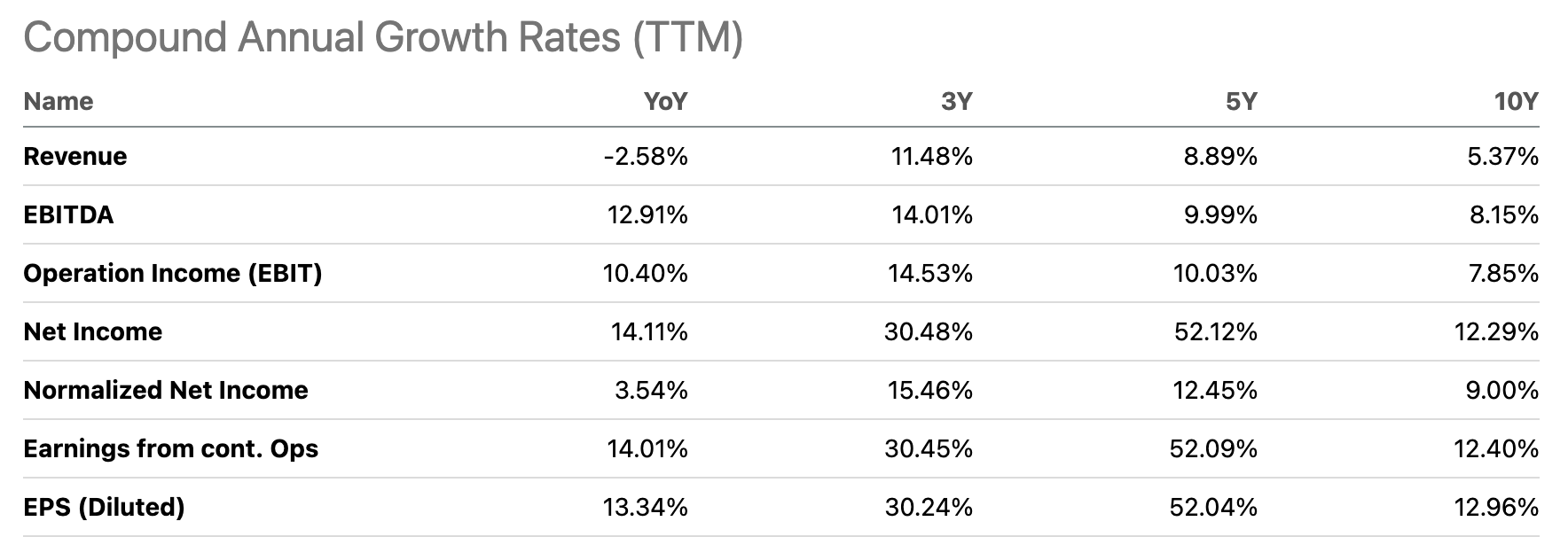

Over the past three years, revenue has grown by 11.5% per year. EBITDA has added 14.0% per year.

Seeking Alpha

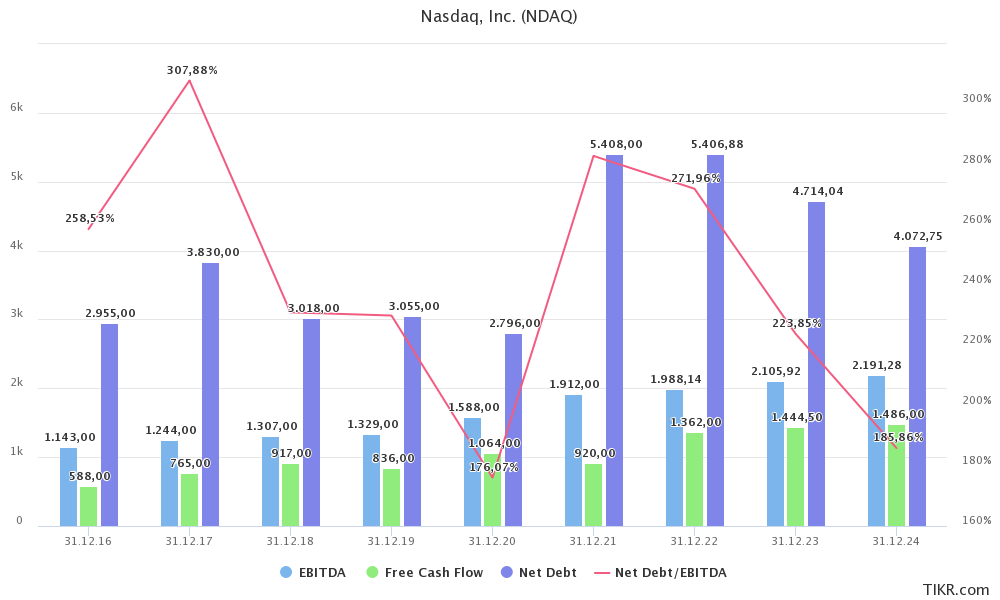

The best thing is that free cash flow generation is extremely high. Free cash flow is cash from operations minus capital expenditures. It’s cash a company can spend on dividends and buybacks – or to reduce debt.

TIKR.com

As the company’s net debt is expected to fall to 2.2x EBITDA in 2023, there is a lot of room to spend money on shareholders.

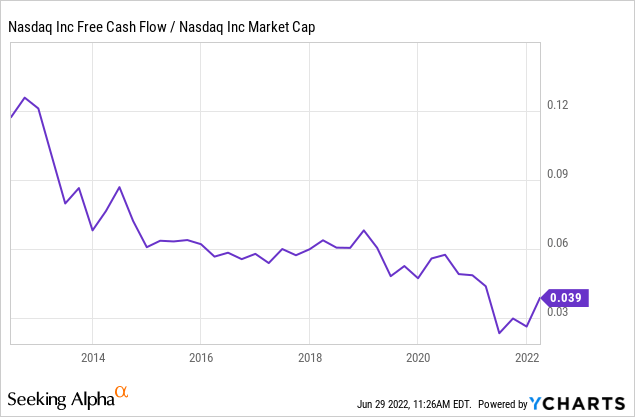

Even better, free cash flow is high. If we use 2023 FCF estimates, we’re dealing with a 5.5% free cash flow yield. This is roughly in line with pre-pandemic results close to 6% of the company’s market cap.

Between 2018 and LTM ending 1Q22, free cash flow grew by 14% per year. The free cash flow conversion is 104% of net income, indicating high-quality earnings.

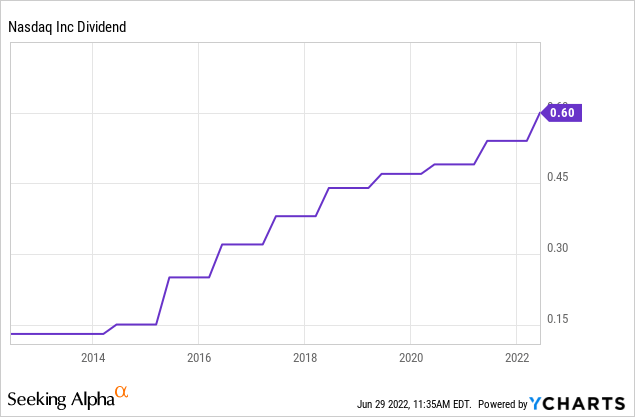

Thanks to these numbers and business model, the company has a fantastic dividend scorecard – except for its yield. In this case, the scores are relative to the financials sector. This makes the dividend yield comparison even tougher as the stock is up against large regional and money center banks. These banks tend to have high yields.

Seeking Alpha

The good news is that Nasdaq is indeed using free cash flow to boost its dividends.

Nasdaq has a clear and transparent capital plan. First of all, it invests in growth, with is already included in free cash flow. It then maintains a 32% dividend payout ratio, which means dividend growth and earnings growth should be fairly in line. Buybacks are also used but they are NOT resulting in a lower share count. The company buys back shares to offset dilution caused by i.e., stock-based compensation.

With that said, dividend growth has averaged 10.6% per year over the past 5 years. These are the “most recent” hikes:

April 20, 2022: 11.1%

April 21, 2021: 10.2%

April 22, 2020: 4.3%

April 24, 2019: 6.8%

The valuation isn’t bad either. Using the company’s $26.0 billion market cap, $4.7 billion in expected 2023 net debt, and $2.1 billion in expected 2023 EBITDA give the company an enterprise value of $30.7 billion. That’s 14.6x expected EBITDA.

This valuation is fair. It’s roughly what the company was valued at prior to the pandemic when investors incorporated higher growth from its service/SaaS business.

TIKR.com

Moreover, with NDAQ being down 26% year to date, I think it’s a good point to either start a position or add to an existing one.

Takeaway

Stock market turmoil isn’t fun, but it opens up new opportunities to buy high-quality stocks. In this case, I’m mainly buying dividend growth stocks as I believe that it’s the best way to achieve long-term outperformance.

In this case, Nasdaq is one of my favorites. The company has a major footprint in financial services with high growth rates in its SaaS-focused segments.

The 26% year-to-date sell-off is providing investors with a somewhat decent yield, which makes high (expected) dividend growth even more attractive.

While nobody knows when or where the market will bottom, I believe that gradually adding to NDAQ is a great way to build long-term wealth. For example, buying 25% now and adding over time allows investors to average down if the market keeps falling. If the stock suddenly takes off, investors have a foot in the door.

This is how I’m dealing with all of my investments at the moment.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment