Ca-ssis

NanoString Technologies, Inc. (NASDAQ:NSTG), which develops, manufactures, and sells tools for scientific and clinical research in the fields of genomics and proteomics around the world, has soared since its last earnings report, jumping from its 52-week low of $4.37 per share on November 7, 2022, to a little over $13.00 per share on February 2, 2023.

That’s interesting, because the latest earnings report was disappointing with management downwardly revising its outlook for full-year 2022 after big misses with revenue and EPS.

While the company guided for an improvement in revenue from its CosMx systems for 2023, which is projected to jump from 40 percent to 50 percent for the full year, based upon prior orders from 2021 and 2022, I think it’s still going to struggle to maintain recent momentum because everything is already priced into the stock price, in my opinion.

There have been a couple of catalysts since the November 2022 earnings call that appear to have been part of the reason for the company’s share price to jump, but I think the major reason is swing traders took positions in the company, as it has moved in a stair-step pattern since the earnings report, which many times points to swing trader involvement in a stock. Swing traders don’t determine the initial move, but they can sustain it as they hold and/or add to their positions when a stock moves in this pattern.

In this article we’ll look at the recent performance of NSTG, some of the positive catalysts that appear to be driving the share price of the company up, and why I think it’s due for a correction; the depth of the correction will probably be determined by how the company performed in the fourth quarter of 2022.

Some of the numbers

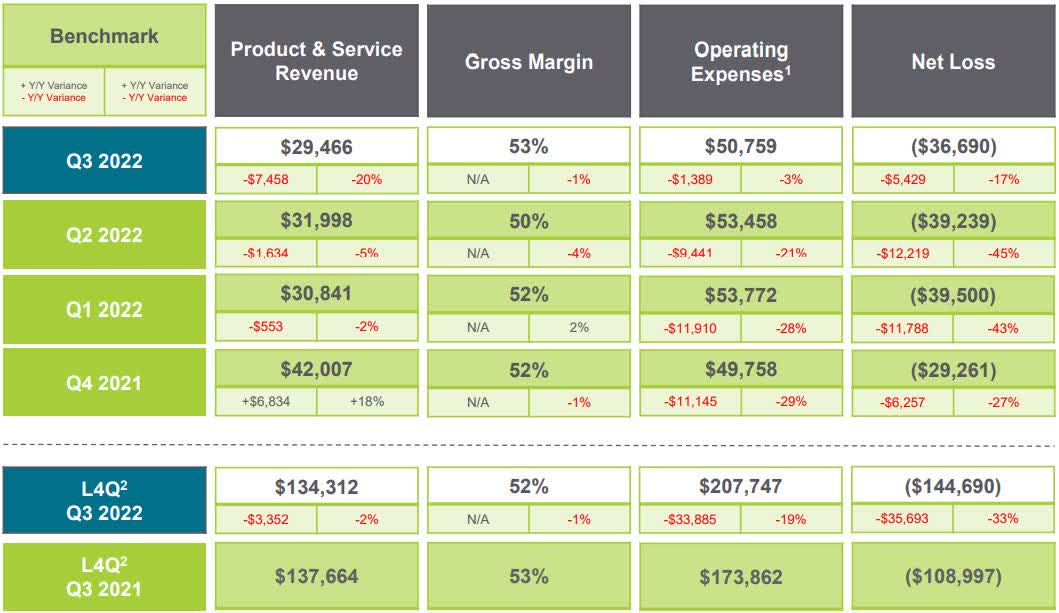

Revenue in the third quarter of 2022 came in at $29.54 million, compared to $37.1 million in the third quarter of 2021. Revenue in the first nine months of 2022 was $92.8 million, compared to revenue of $102.6 million in the first nine months of 2021.

Investor Presentation

Product revenue dropped from $32.5 million in the third quarter of 2021 to $24.6 million in the third quarter of 2022, while Service revenue climbed slightly from $4.4 million in the third quarter of 2021 to $4.9 million in the third quarter of 2022.

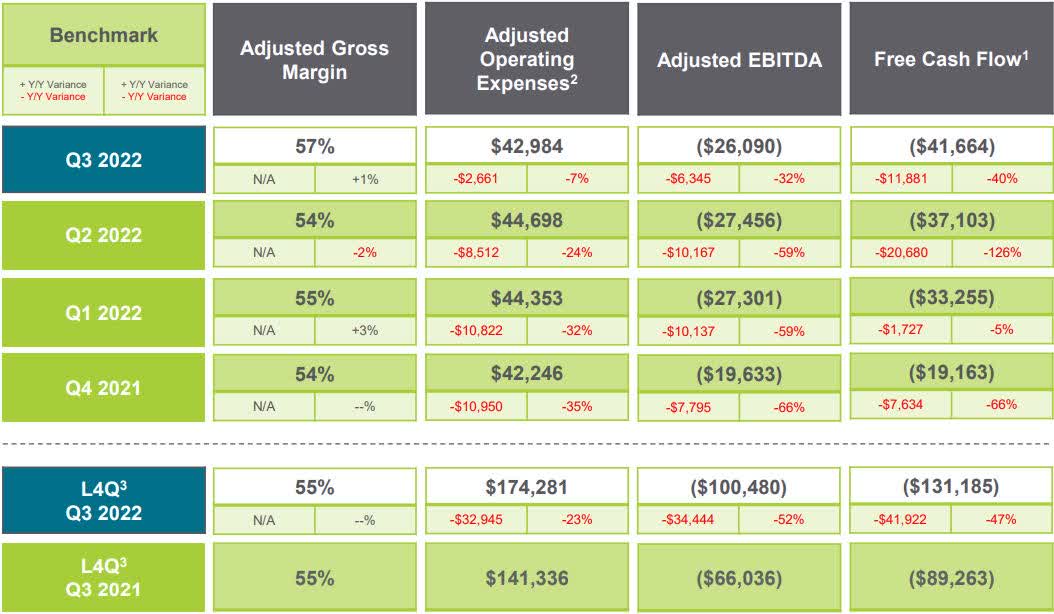

Adjusted EBITDA in the reporting period was -$(26.00) million, compared to adjusted EBITDA of -$(19.63) million in the fourth quarter of 2021. Adjusted gross margin in the third quarter of 2022 was 57 percent, compared to adjusted gross margin of 54 percent in the fourth quarter of 2021.

Net loss in the third quarter of 2022 was -$(36.7) million, or -$(0.79) per share, compared to a net loss of -$(31.3) million, or -$(0.69) per share in the third quarter of 2021. Net loss for the first nine months of 2022 was $115.4 million, or -$(2.49) per share, compared to a net loss of -$(86.00) million, or -$(1.90) per share in the first nine months of 2021.

Investor Presentation

Free cash flow in the reporting period was -$(41.7) million, compared to free cash flow of -$(19.2) million in the fourth quarter of 2021.

Cash and cash equivalents at the end of the third quarter of 2022 was $117 million, compared to cash and cash equivalents of $107 million at the end of calendar 2021.

The company had long-term debt of $225.3 million at the end of the reporting period, basically flat compared to long-term debt of $225.1 million at the end of calendar 2021.

NSTG guided for total revenue in the fourth quarter to be in a range of $33.00 million to $35.00 million.

In order to improve the bottom line, the company decided to eliminate 95 positions, while cutting back on spend in “non-personnel areas.”

Its share price pattern

As mentioned above, swing traders in particular are attracted to the stair-step share price pattern NSTG has been in since November 2022, and I think that’s probably the major reason it has found support, especially with the weak fundamentals of the company, combined with uncertainty as to how 2023 is going to play out.

First, the one thing that isn’t surprising is the bounce off its 52-week low of $4.37, which was inevitable in my opinion, as the stock was oversold at that price level. What is surprising is that it more than tripled from there when it hit approximately $13.19 per share on February 2, 2023. There are simply no visible catalysts to justify that type of move and depending on the numbers and management commentary and guidance in its next earnings report, I expect the company to correct to fairly significant levels from where it’s trading at this time, which is slightly above $12.00 per share as I write.

TradingView

It’s understandable that some investors have chosen to take a position in NSTG, as it has fallen from a 2-year high of about $81.50 per share on April 26, 2021, to the above-mentioned $4.37 per share. Yet, based upon its performance, that decline in its share price was in alignment with its performance.

More recently, I think traders are bidding up the price leading up to the next earnings report and are certain to take some profits before the numbers are released, primarily because there is little clarity on how the company is going to do in 2023.

Positive catalysts

Along with what I believe are swing traders taking a position in NSTG, there were also some positive catalysts that probably have driven up the share price since the third quarter earnings report, including top management acquiring shares in the company, a recent “Buy” rating on the company, and an announced expansion of its collaboration with Abcam (ABCM) immediately after the earnings release.

Per the Abcam collaboration, the two companies announced they’re going to “co-market Abcam antibodies for NanoString’s high-plex spatial multiomic solutions.”

It’ll be included as part of NanoString’s first 64-plex protein panel for its CosMx Spatial Molecular Imager (SMI).

While this is interesting, it remains to be seen how much it’ll add to the top and bottom lines of the company over time, as collaboration revenue is only a small part of the sales of the company, and it has been falling.

According to regulatory filings, on December 12, 2022, CEO Brad Gray acquired 67,600 shares of NSTG stock at $7.38 a share, with the total transaction being valued at $499,400. Gray now owns 270,000 share in the company.

Chief Financial Officer Thomas Bailey acquired 29,200 shares on December 13, 2022, at $8.05 per share, for the total cost of $234,700, bringing the total number of share he owns to 48,500.

The purpose of making these types of acquisitions is to show the market management has confidence in the future performance of a company, and immediately after the acquisitions the share price did get a temporary boost, although it did fall back not long after the initial positive response.

I find it doubtful the big jump in its share price is directly associated with the acquisitions, but possibly combined with the other factors mentioned in the article, it may be a small part of the upward move.

Last, on February 2, 2023, it was reported that UBS analyst John Sourbeer initiated coverage on NSTG, starting the company off with a “Buy” rating and a $15.00 price target for the next year.

Sourbeer said he believes the market isn’t taking into account the “bullish views” from management stated in a press release from early January 2023. He also said the company is “trading below its historical multiples and its peers.”

Nonetheless, after I looked over the press release, the company said revenue in the quarter is expected to come in at its guided range of $33.00 million to $35.00 million and is also expected to be in the guided range of $125.00 million to $127.00 million for full year 2022.

The point is, even after reporting some of the orders in the quarter, it doesn’t reflect any surprise to the upside for the fourth quarter, which suggests the company continues to perform at a very modest level. I don’t see why meeting guidance should be considered a positive catalyst for the company; that’s especially true since when guidance reflects a weaker performance than in the past.

Last, the CosMx spatial molecular imager has been gaining momentum, and has some promise as a generator of revenue growth if it is able to meet expectations. It was one of the few bright spots in the company’s latest report, and it needs to continue to do well if it has a chance of gaining some momentum in the quarters ahead. Based upon secured CosMx orders from 2021 and 2022, the company expects growth in 2023 to be in the range of 40 percent to 50 percent.

While all of these could be considered positive catalysts in general, other than the increase in collaboration with Abcam and the CosMx spatial molecular imager, they won’t have any impact on the actual performance of NSTG.

Conclusion

With NSTG stock trading at almost 3x its 52-week low in November 2022, and no significant catalysts to reinforce the soaring share price since that time, I see the company being set up for a potential deep correction.

There’s no doubt in my mind that shareholders will start taking profits, which should drive the share price down. That could be fairly deep if the fourth quarter numbers disappoint and guidance only remains in alignment with much of what we already know.

I don’t think the market has missed anything with the last earnings report or latest release, as they both reflect management guidance and expectations, and there’s nothing visible at this time that suggests any meaningful surprise to the upside.

The major thing to watch in my view is how its CosMx spatial molecular imager does going forward, and what the future pipeline looks like.

The company has plenty of cash on hand at this time, but it wouldn’t take long to burn through the $117 million if free cash flow continues to plunge, as it did by almost $42 million in the third quarter of 2022.

Until there’s confirmation of a turnaround, which appears far off to me, I think NSTG is going to struggle to gain any sustainable momentum. In the near term, I expect a sell-off, which could provide a good entry point for those that believe that over the long term the company will improve its performance.

Be the first to comment