metamorworks/iStock via Getty Images

Summary

There is high demand for IT service providers like Nagarro SE (OTCPK:NGRRF) due to the increasing digitization of business processes and the need for businesses to adapt to digital disruption. NGRRF is particularly appealing because they can efficiently source, train, and deploy skilled personnel. The outlook for the company is positive, but the current stock price has already taken this into account, and it may be wise to wait for a lower price before investing.

Company overview

Nagarro SE is a multinational digital engineering company headquartered in Germany. It offers a comprehensive set of services, including digital product engineering, digital commerce and customer experience, enterprise resource planning [ERP] consulting, managed services, and independent testing.

Homepage

Transformation is the constant

The widespread digitalization of business processes and product lines is having a profoundly disruptive effect on companies of all stripes. This shift has implications for how companies interact with their clients and workers, as well as for the ways in which they can streamline their operations. Customers today anticipate a seamless, timely, contextual, intelligent, and unrestricted experience across all touchpoints in the digital ecosystem, regardless of their location or time of day. Worse yet, the pandemic has hastened this development.

Therefore, there is a lasting shift in the IT services market away from the provision of basic services. Service providers who target this sizable and quickly expanding market segment stand to benefit from the widespread adoption, adaptation, and response to new digital opportunities by businesses of all stripes.

To put this in perspective, Spherical Insights predicts that by 2023, the worldwide IT services market will be worth $2.5 trillion, expanding at a CAGR of 5.8% from $2021. Market sizes vary from source to source, but they all point in the same direction.

3 key drivers driving growth in the industry

I believe there are 3 key drivers here: digitization, agility, and talent shortage.

As society continues to go digital and businesses compete more and more through software, digital transformation remains a challenge and an opportunity for many businesses. Among the difficulties is the ever-increasing competition and the constant burden to push digital tools to end-customers. These shifts will affect every facet of business, from customer service to product design to sales strategies to company structure. Because of the complexity of this transition, businesses are increasingly relying on third-parties to take the lead in their digitalization initiatives. Hence, employing reliable IT service providers can be beneficial for businesses.

There is a growing urgency for businesses to adapt rapidly to shifting competitive landscape. Optimizing DevOps and agile development approaches are becoming increasingly important as businesses strive to meet the rising time-to-market expectations for digital investments. As a result, companies are looking for service providers who can meet their complex needs and assist them to cut costs and speed up their time to market.

In addition, the fast-changing nature of technology has resulted in a shortage of skilled personnel with the advanced IT skills needed for digital transformation, making it challenging for many businesses to attract and retain top talent in this area. This makes global service providers, who can efficiently and effectively find, train, and deploy professionals from various locations, more appealing to companies seeking to undergo digital transformation.

Nagarro is a collection of digital engineers

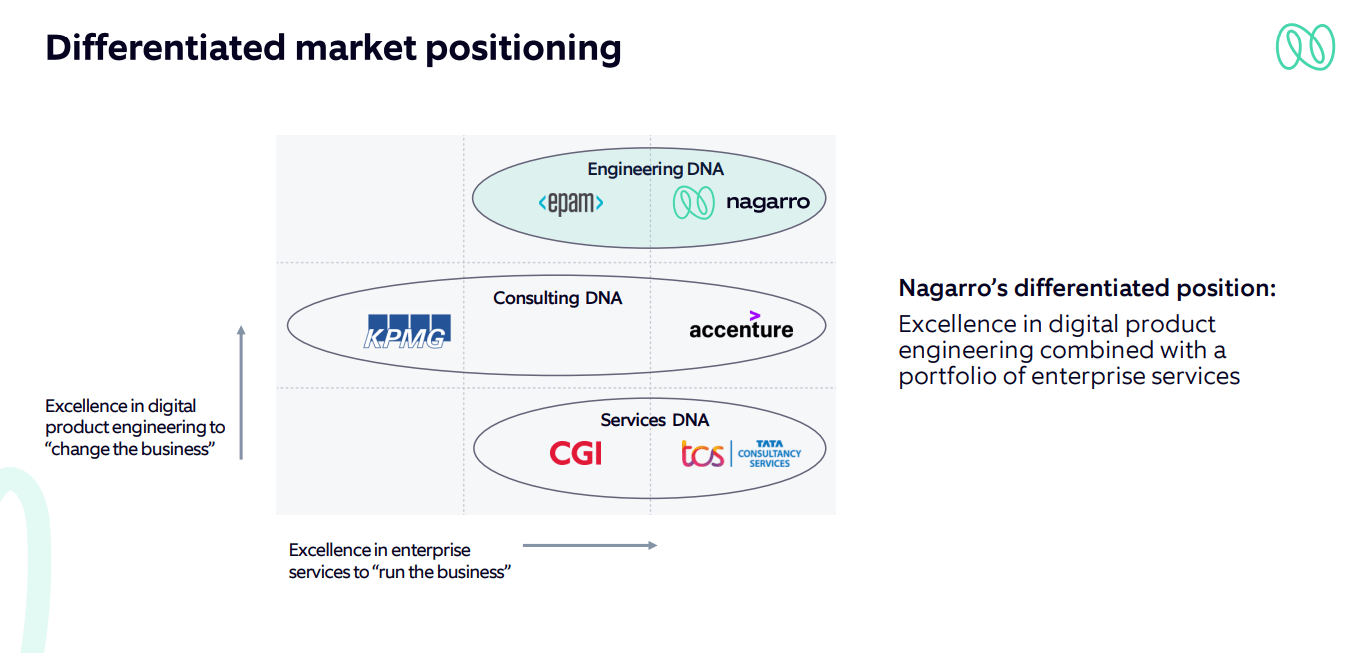

From what I can tell, more than 90% of NGRRF’s staff are engineers, making it a veritable hive of engineering talent. Nagarro SE has clearly proven that it knows its way around the industry and can adapt to the specific needs of its customers from its year of experience and base of clients (Refer below). Also distinguishing NGRRF from its rivals is the breadth of its digital consulting and business enterprise offerings.

Nov 22 investor presentation

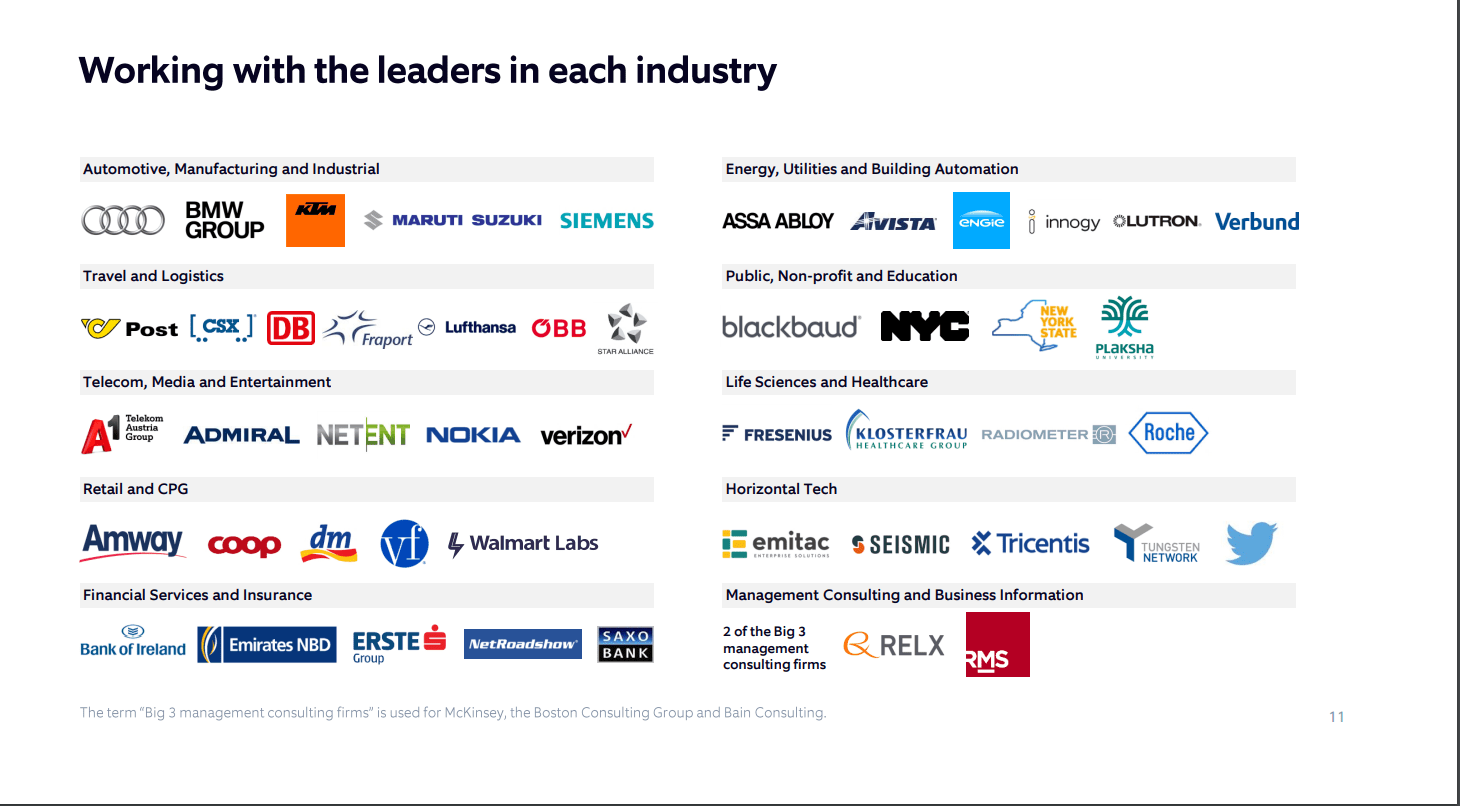

Large base of key clients

Looking at a company’s clientele is the best indicator of the quality of its services. That’s because only reliable and effective products would be used by such prestigious firms. In my opinion, one of NGRRF’s main advantages over the competition is the extensive collection of case studies and glowing recommendations from prominent businesses across a wide range of industries. NGRRF works with both well-known multinationals and market pioneers.

Nov 22 investor presentation

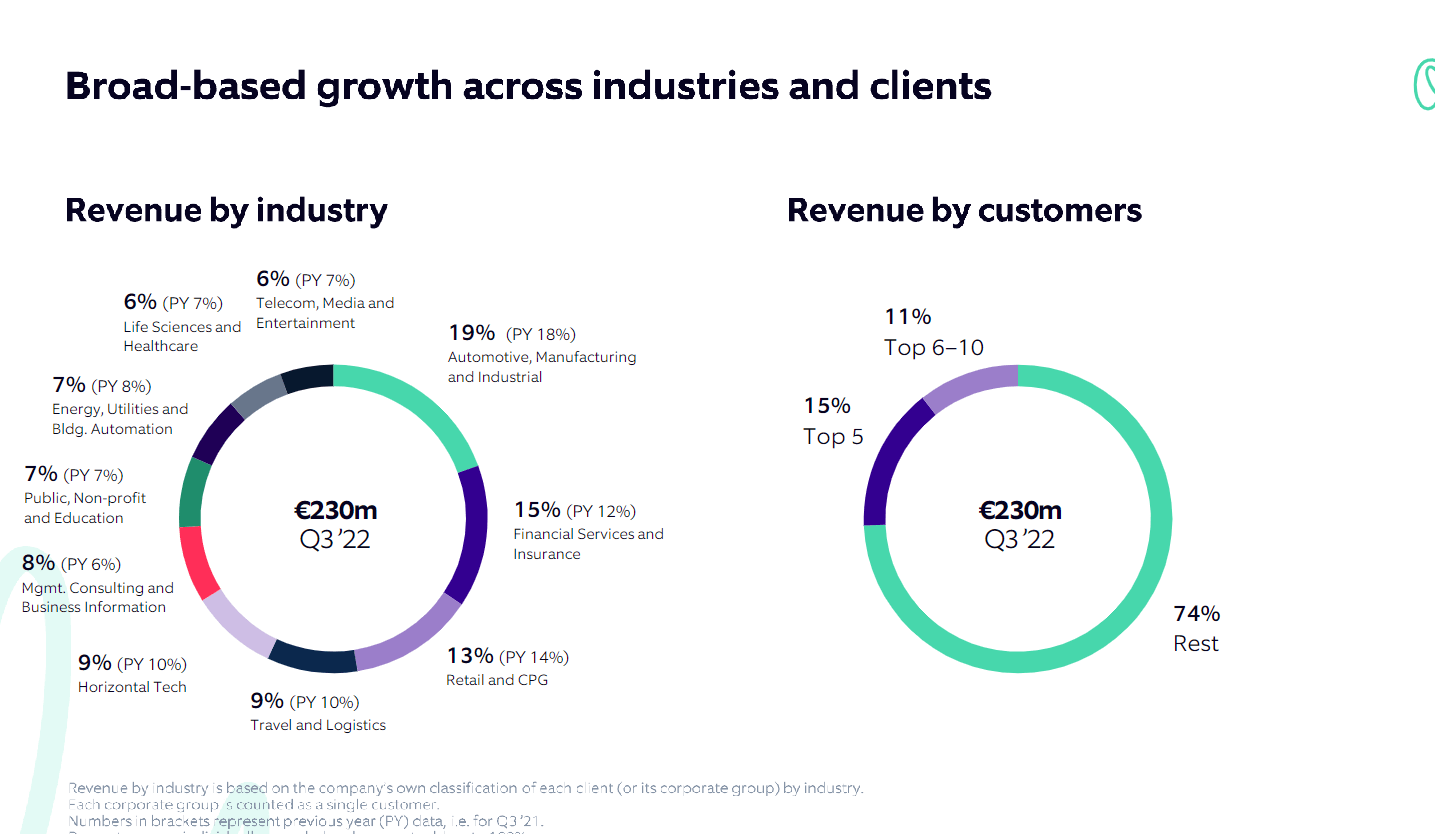

NGRRF’s ability to both foster its younger, more nascent client relationships and expand its larger, more established ones, in my opinion, is crucial to the company’s long-term growth rates. And NGRRF has certainly pulled this off. Since 2017, NGRRF has seen a dramatic increase in the number of its client accounts that generate over €1 million in annual revenue. They were also able to increase earnings from the top ten customers during the same time frame. The clientele of NGRRF, on the other hand, comes from a wide variety of fields, and the firm does not rely heavily on any one industry.

Nov 22 investor presentation

Unique culture

Investors often fail to recognize the value of a company’s unique culture in creating value. Why? Because it’s not obvious to spot in the books, that’s why. This is not to say, however, that it is of no significance. The bottom line would benefit in the long run from a company with a robust culture because of the increased efficiency in execution and the lower attrition rate.

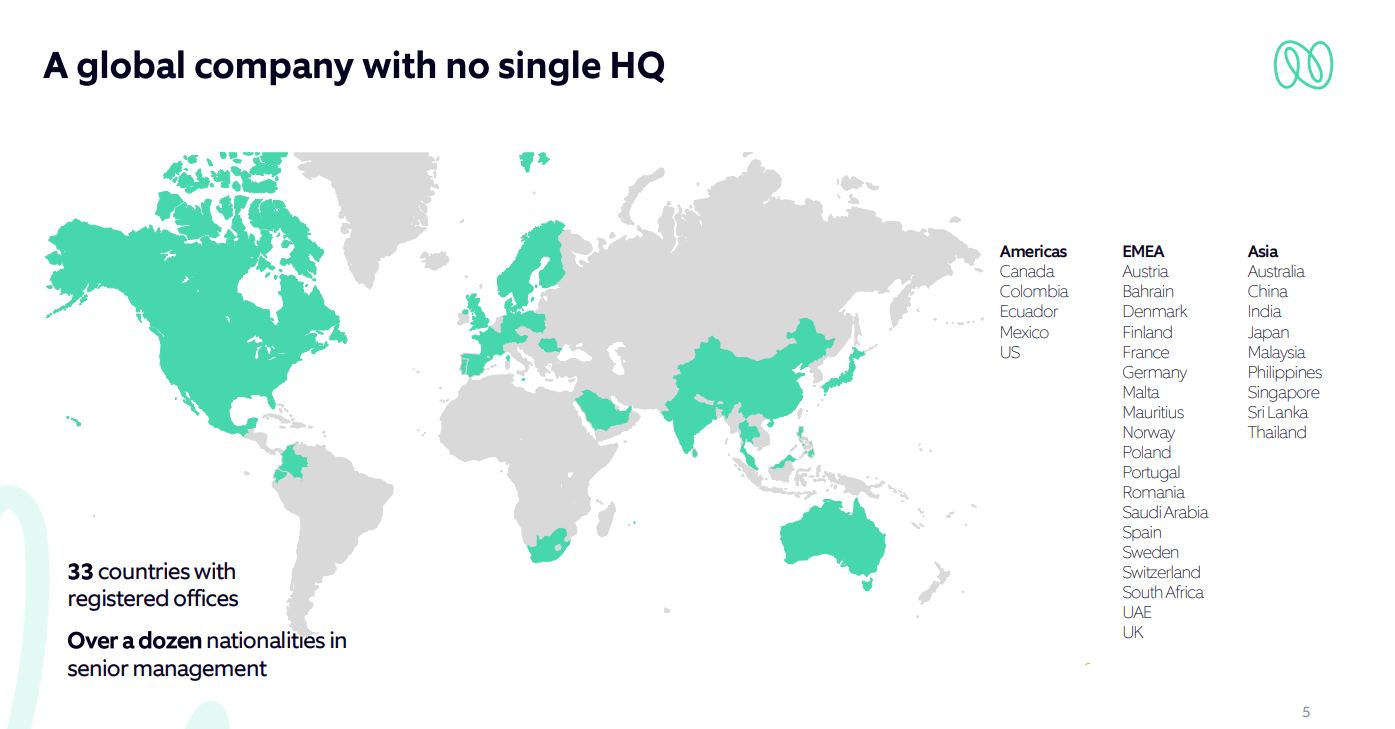

The unique structure and culture of NGRRF, in my opinion, set it apart from many rivals. For instance, NGRRF does not have a central headquarters, despite having locations in 33 countries and employing over 10,000 people to serve clients in local markets.

To me, the emphasis on discretion rather than centralized authority is what makes this non-authoritarian method so effective at addressing the challenges and seizing the benefits of entrepreneurial growth. Because of this, teamwork and individual accountability are encouraged at all levels of the company.

Nov 22 investor presentation

Raised guidance is music to investors ears

Despite the current macroeconomic environment, demand remained robust in the third quarter, leading to the fourth guidance increase of the year. The combination of a robust U.S. dollar and efficient management of available resources resulted in a 63% rise in revenue, to 230 million euros. North American sales increased by 86%, while international sales increased by 97%. Furthermore, growth is showing no signs of slowing down in any industry (all growing mid- to high-double-digit).

What gives this print the most hope is the margin, which has grown for the past two runs. This is due to 2 reasons:

- Nagarro’s primary sourcing market in India has experienced a decline in wage inflation towards pre-COVID levels.

- Increasing project prices which demonstrates the company pricing power.

Adjusted EBITDA rose 123% to €48.4m, while EBIT rose 192% to €39.2m, for a better margin of 21.1%. If this holds true, then the results for 4Q22e would suggest a deceleration in both revenue and profit growth from the previous quarter, as the holiday season and fewer working days would be the primary causes.

The best news is the guidance. Management has revised its revenue forecast for October to €850 million, up from the previous estimate of €830 million. The gross margin is expected to be 28%, an increase from the previous forecast of 27%, and the adjusted EBITDA margin is now anticipated to be 16%, higher than the previous estimate of 15%. This revised guidance implies an adjusted EBITDA target of €136 million, which is 6% higher than what was previously expected and 39% higher than the initial forecast made in January. The higher margin forecast is seen as a sign that the company is confident in its ability to maintain pricing despite inflationary pressures. Despite economic uncertainty, the management team has cited strong demand from clients and expressed optimism for the coming year. In addition to additional acquisitions, they believe that growth of 20% is possible.

Valuation

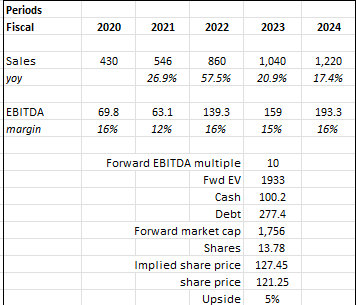

My model points indicate that NGRRF is worth $127.45 in FY23, so I believe it is fairly valued at this time. This is approximately 5% higher than the current share price. My model assumption is based on my belief that the NGRRF will benefit from the strong trend of digitization in all industries.

Where I see potential for further upside is in valuation; NGRRF is currently trading at 10x forward EBITDA, which seems a little low given its historical valuation rage. Assuming NGRRF continues to demonstrate its ability to expand margins and address wage issues, I believe there is a chance for valuation to re-rate higher based on the positive narrative. To be on the safe side, I’m assuming no change in multiples.

Own calculations

Risks

FX exposure

Nagarro SE is especially susceptible to currency fluctuations, which have been a major disruption in many international companies recently due to the rising dollar, because it operates and earns in multiple countries. The short-term stability of NGRRF results may be affected by the continued turbulence of currency exchange rates.

Competition

As a result of the low barriers to entry, I expect the already competitive market for NGRRF services and products to remain so. To put things into context, employees at NGRRF would essentially be able to quit and start their own business to compete against NGRRF.

In addition, customers often hire several different IT service providers instead of using just one, which can put a dent in NGRRF ability to rise prices.

Wage inflation

The people who work for and with Nagarro are its greatest assets. Therefore, future wage increases may cut into Nagarro’s margins if not balanced by higher project pricing. If it’s difficult to recruit, retain, and inspire the best people, it could have a negative impact on client satisfaction and productivity.

Conclusion

The increasing digitization of business processes and the need for businesses to adapt quickly to digital disruption are driving demand for IT service providers who can provide complex product engineering services and help companies speed up their time to market. In addition, the shortage of skilled personnel with advanced IT skills required for digital transformation makes global service providers like NGRRF, who can efficiently source, train, and deploy highly skilled personnel, more appealing to companies seeking to undergo digital transformation.

I am optimistic about Nagarro SE, but I am concerned about the stock price, which has already factored in the positive outlook. I would recommend waiting for the share price to fall further before investing.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment