jetcityimage

Investment Thesis

BorgWarner (NYSE:BWA) should see higher stock prices due to its consistent technology innovation and expanding product line. BWA provides substantial product differentiation, performance, weight reduction, enhanced safety, and reduced cost. Their worldwide factories provide a competitive advantage since they offer local production. BWA can provide an excellent return from the covered call premium and dividends even if the stock price does not move much.

Borg Warner

BorgWarner provides technology solutions for combustion, hybrid and electric vehicles. The Company’s Air Management segment (49.2% of sales) offers technology, such as turbochargers, eBoosters, eTurbos, timing systems, emissions systems, gasoline ignition technology, smart remote actuators, powertrain sensors, cabin heaters, battery heaters, and battery charging.

The e-Propulsion & Drivetrain segment (36.2% of sales) offers technologies such as rotating electrical components, power electronics, control modules, software, friction, and mechanical products for automatic transmissions.

The Fuel Injection segment (12.3% of sales) develops and manufactures gasoline and diesel fuel injection components and systems. The Aftermarket segment (2.3% of sales) offers various solutions covering the fuel injection, electronics and engine management, maintenance and test equipment, and vehicle diagnostics categories.

The company’s largest three customers are Ford at 10%, Volkswagen at 9%, and then Hyundai at about 6% totaling 25% of 2021 revenue. Sales were split about 76% light vehicles, 11% commercial vehicles, 4% off-highway vehicles, and 9% aftermarket auto parts suppliers. Geographically, Europe accounted for 35% of 2021 revenue, Asia 35%, and North America 29%.

BWA had 93 manufacturing, assembly, and technical locations worldwide as of January 2022, providing a competitive advantage to multi-national vehicle manufacturers who want fewer product differences between countries. Borg Warner’s revenue continued to grow in the last ten years even though U.S. light-vehicle sales units did not.

BWA secures at least one-year contracts from its customers, and vehicle programs, once announced, often have a 5 to 10-year life cycle. Powertrains can have a 10 to 15-year life cycle.

BWA has annual sales of $15.3B with 49K employees. On January 28, 2020, BWA announced plans to acquire Delphi Technologies for $3.3B in an all-stock transaction. Roughly 19K employees were added due to this acquisition. Delphi was a leading manufacturer of propulsion technologies and services with a specialty in power electronics which BWA needed to expand its EV presence.

They are 97.1% owned by institutions, with only 3% short interest. Their return on equity is 12.1%, and they have an 8.4% return on invested capital. The free cash flow yield per share is 5.5%, and their buyback yield per share is 2.5%. Their Piotroski F-score is seven, indicating strength. BWA’s S&P credit rating is BBB. Only 26.9% of total assets are considered intangible hard-to-value, non-physical assets. Their net debt to EBITDA ratio is only 1.6. They have a price-to-book ratio of 1.4.

Potential Positive Impacts

- BorgWarner intends to spin off its fuel systems and aftermarket businesses to shareholders by the end of 2023.

- Light vehicle sales should pick up post Covid as the supply chain and chip problems dissipate.

- BWA continues to prove they can outperform the light vehicle sales trend.

- The company provides product differentiation and enjoys high customer switching costs plus cost advantages with a substantial global manufacturing presence and pricing power from their technologies.

- BWA provides some of the best answers to global clean air legislation.

Potential Negative Impacts

- A recession may temporarily reduce new vehicle purchases.

- BWA is capital-intensive with high fixed costs, so a sudden decline in volume could cause another earnings trough similar to 2020.

- Raw material costs could continue to rise under inflationary conditions, and their highly engineered products require the company to pay the going rate for personnel with expertise in software and engineering.

- FX continues to be a headwind.

- BWA is exposed to risk from potential vehicle recalls.

Q3 Quarterly Results

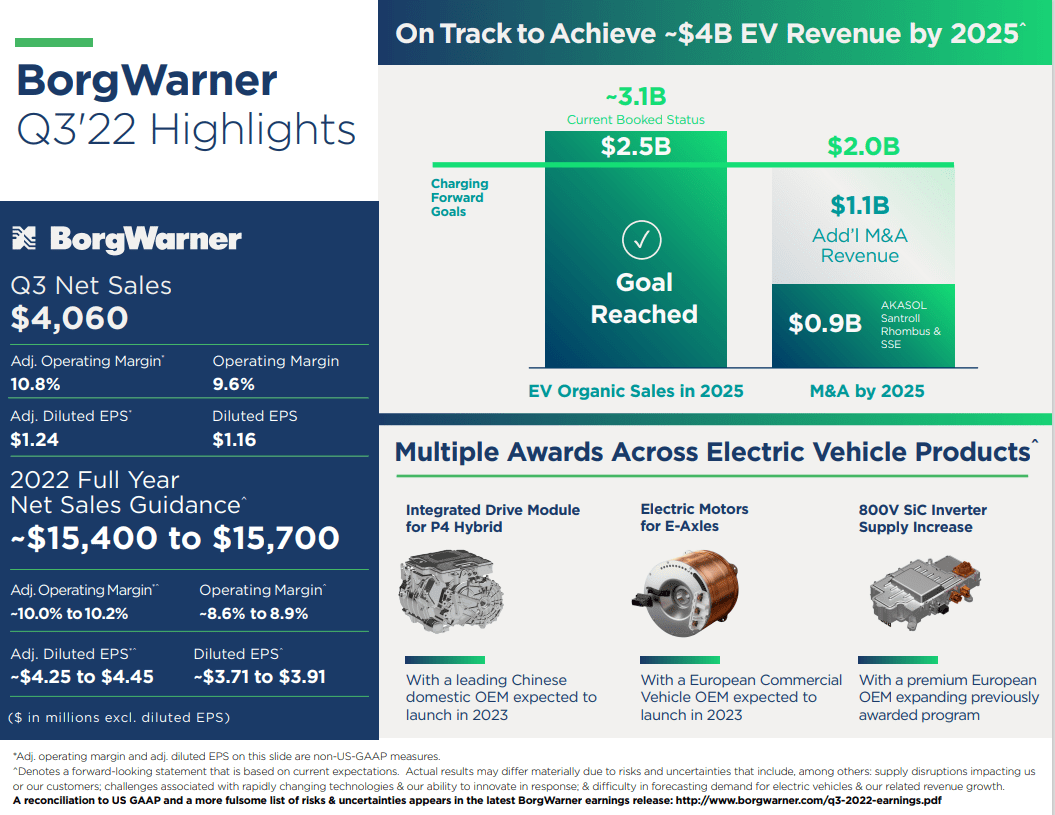

BorgWarner announced Q3 earnings in their October 27th press release with the following highlights:

• On track to achieve approximately $4 billion in electric vehicle revenue by 2025. The Company expects its 2022 electric vehicle revenue to grow to roughly $850 million, which is more than double what it was in 2021.

• BorgWarner has agreed to acquire the charging business of Hubei Surpass Sun Electric (SSE). The acquisition complements BorgWarner’s existing European and North American charging footprints by adding a China presence. The Company expects DC’s fast-charging related revenue to be $225 million to $275 million by 2025.

• BorgWarner has been granted a production increase to supply its 800V silicon carbide (SIC) inverters to a premium European OEM. The initial order has now been significantly increased, with production for this program set to begin in 2024.

• BorgWarner will supply electric motors for the E-Axles of a European commercial vehicle OEM. This e-axle is designed to equip new electric light commercial trucks with up to 7.5 tons, and production is expected to begin in early 2023.

• U.S. GAAP Q3 net sales of $4,060 million, an increase of 19% compared with the third quarter of 2021. Excluding the impact of foreign currencies, the 2022 acquisitions of Santroll’s light vehicle eMotor business and Rhombus Energy Solutions, and the 2021 divestiture of the Water Valley, Mississippi business, organic sales were up 29% compared with the third quarter of 2021.

• U.S. GAAP Q3 net earnings of $1.16 per diluted share, and adjusted net earnings were $1.24 per diluted share.

• U.S. GAAP Q3 operating income of $389 million, or 9.6% of net sales.

• Q3 Net cash provided by operating activities of $347 million. Free cash flow was $167 million.

www.borgwarner.com/investors

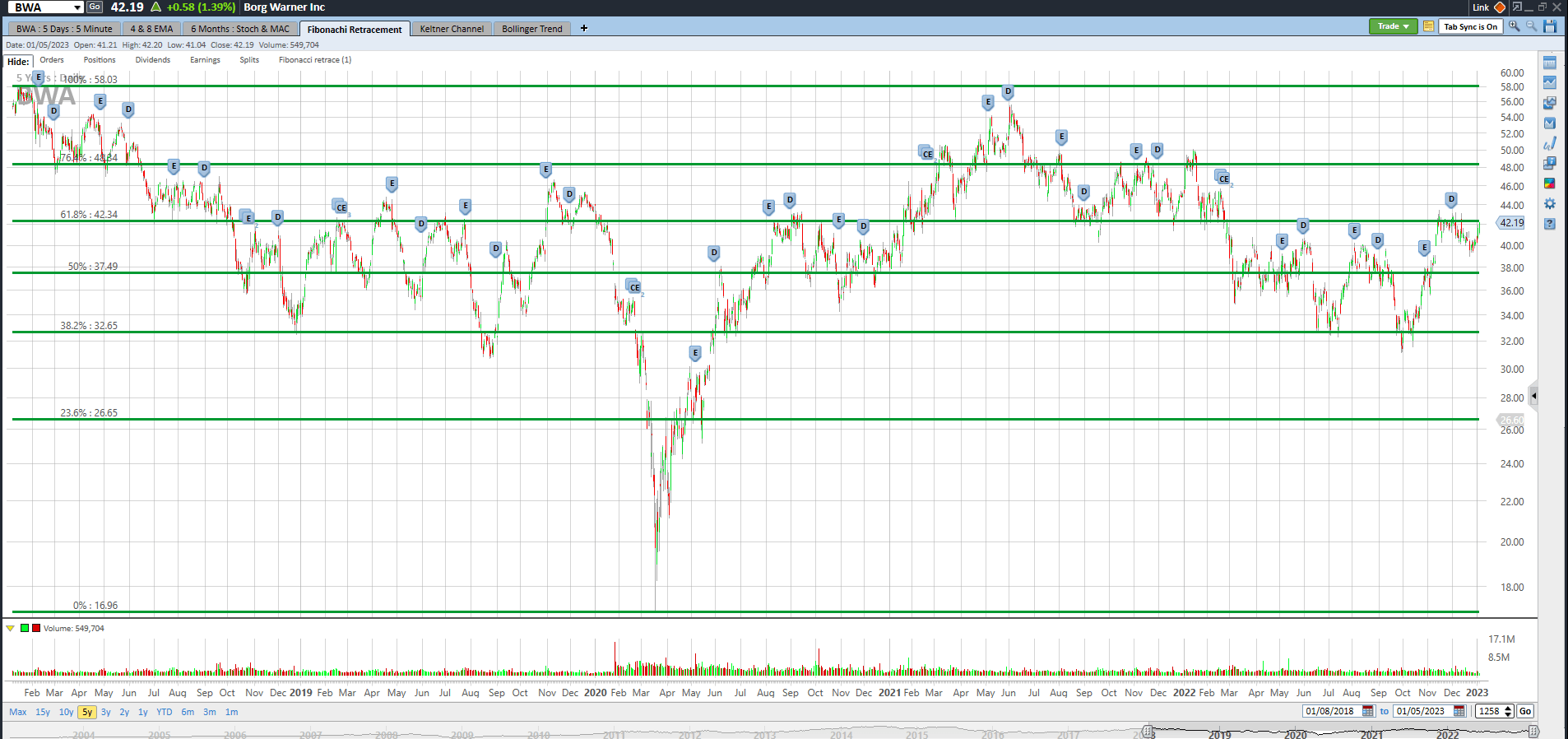

Good Technical Entry Point

The share price of BWA traded at $42.00 on January 5th. I’ve added the green Fibonacci lines, using BWA’s high and low for the past five years. It’s interesting to note how the market pauses or bounces off these Fibonacci lines, and they can be one clue as to where the stock price may be headed. BWA is at the 61.8% Fibonacci retracement level but could go lower. However, I believe that BWA will trade above $42.50 by July for the reasons in this article.

Schwab StreetSmart Edge

The four most accurate analysts have an average one-year price target of $55.50, indicating a 32.1% potential upside from the January 5th trading price of $42.00 if they are correct. Their ratings are three buys, one hold, and no sells. Analysts are just one of my indicators, and they are not perfect, but they are usually in the ballpark with estimates or at least headed in the right direction. They often seem a bit optimistic, so I suspect prices may end up lower than their one-year targets to be on the safe side.

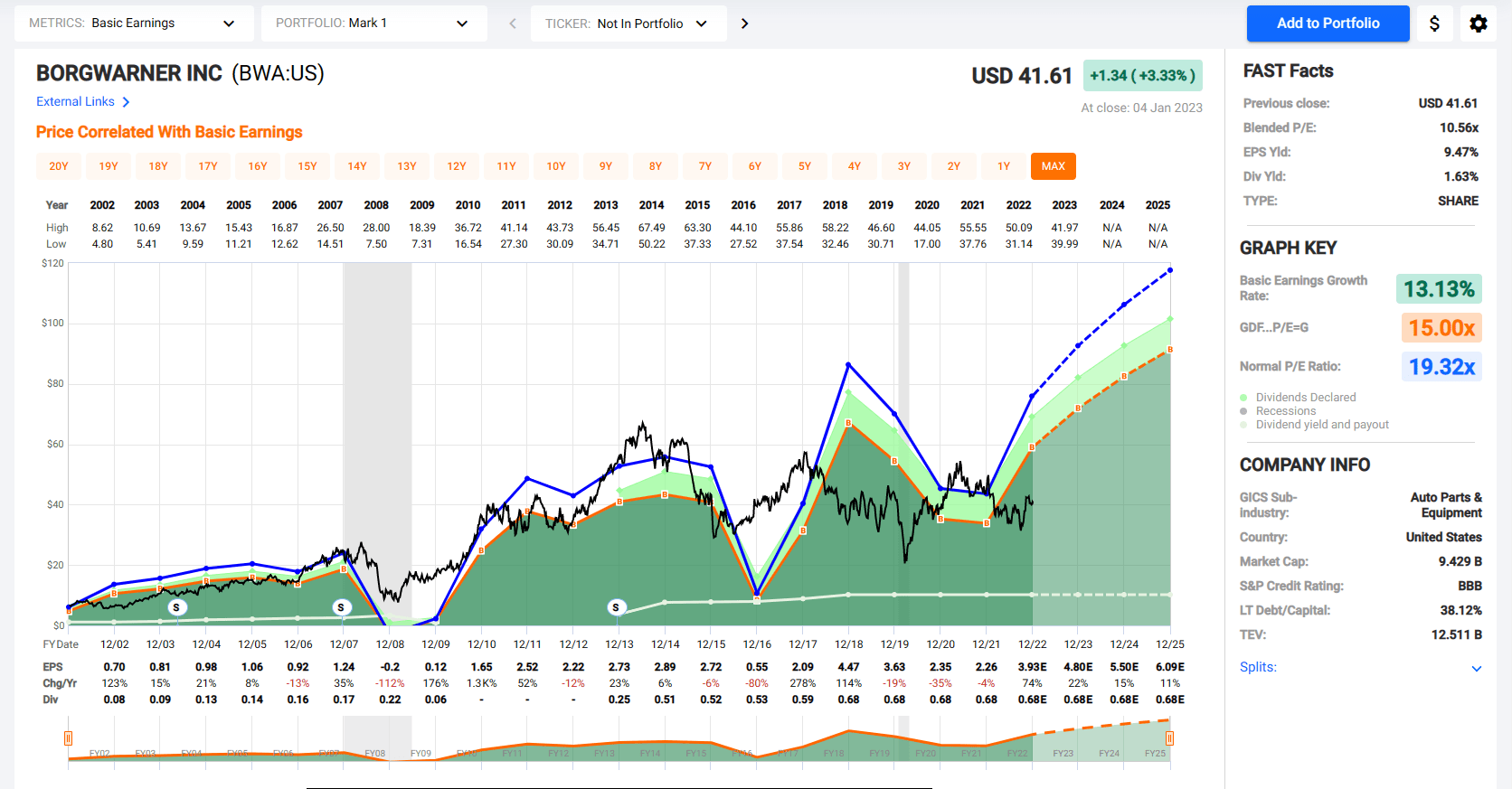

Trends In Earnings Per Share and P/E Ratio

The black line shows BWA’s stock price for the past twenty years. Look at the chart of numbers below the graph to see that BWA’s earnings were $3.63 in 2019, $2.35 in 2020, and $2.26 in 2021. They are projected to earn $3.93 in 2022, $4.80 in 2023, and $5.50 in 2024.

The P/E ratio for BWA is currently at 11, but the average ratio over the past ten years is 16. I don’t think the P/E will rally back to 16 anytime soon. If BWA earns $4.80 in 2023, the stock could trade at $52.80 if the market assigns an 11 P/E ratio.

FastGraphs.com

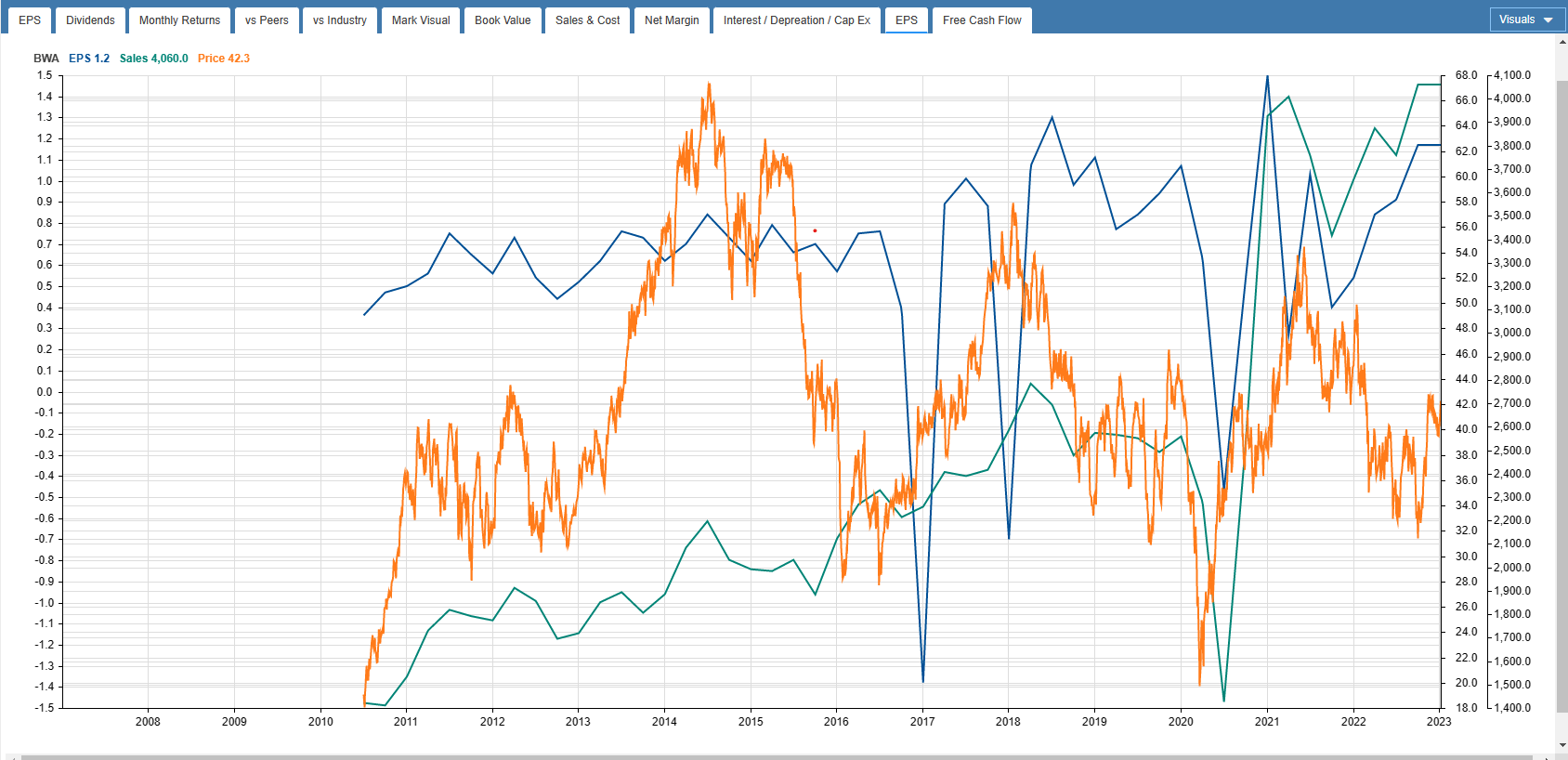

The stock price has not yet caught up with the increasing sales and EPS.

StockRover.com

Sell Covered Calls

My answer to uncertainty is to sell covered calls on BWA six months out. BorgWarner traded at $42.00 on January 5th, and July’s $42.50 covered calls are at or near $4.30. One covered call requires 100 shares of stock to be purchased. The stock will be called away if it trades above $42.50 on July 17th. It may even be called away sooner if the price exceeds $42.50, but that’s fine since capital is returned sooner.

The investor can earn $430 from call premium and $50 from stock price appreciation plus $34 in dividends. This totals $514 in estimated profit on a $4,200 investment, a 23.1% annualized return since the period is 193 days.

If the stock is below $42.00 on July 17th, investors will still make a profit on this trade down to the net stock price of $37.36. Dividends and selling covered calls reduce your risk.

Takeaway

BWA should see higher stock prices due to its consistent technology innovation and expanding product line. Even if BWA’s stock price only moves from $42.00 to $42.50 by July 17th, a 23.1% potential annualized return is possible, including dividends and the covered call premium.

Be the first to comment