Jorisvo/iStock Editorial via Getty Images

Masolino and Masaccio

Six years were enough for Masaccio (1401-1428) to revolutionize Western painting. His real name was Tommaso Cassai, but because he was apparently neglectful in dress and living, he was given the nickname “Masaccio” (the suffix –accio in Italian is used to form nouns and adjectives with a pejorative value).

In 1425 he worked in Florence, in a church in the San Frediano district, that portion of the city called Oltrarno (“Beyond river Arno”), where he was commissioned to fresco the Brancacci Chapel with his master, Masolino.

Masolino was a late Gothic painter anchored in courtly manners, whose art was expressed in figures with kind faces and neat clothes, with static poses and expressive fixity. He conjured a sweetened vision, even of the relationship with God, which Masaccio distorted by breaking all ties with the artistic culture of the generation of which Masolino is an expression.

Indeed, Masaccio firmly nails his figures in reality through robust compositional dynamism, sculptural roundness, and powerful drama. His frescoes are characterized by a confident spatiality and figures of a severe and synthetic realism, through which the artist expresses a message of great moral vigor.

The disruptive force of his painting is expressed in the austere and solemn poses of his figures. It is Humanism, which restores dignity to human beings even in their relationship with God. Adam and Eve, banished from the Earthly Paradise, communicate in an unprecedented and lacerating way the heartbreak of remorse and the consciousness of modesty. Suffering faces betray the weight of sin.

The absolute summit of the fresco cycle is the Payment of the Tribute, one of the highest creations of Italian painting and the cultural watershed between Gothic and Renaissance painting, as well as a veritable training school for generations of artists in the centuries to follow. Any visitor to Florence cannot fail to admire this masterpiece, which represents a synthesis of the values expressed by the entire Western civilization.

Why Masaccio?

In my previous article, I talked about the genius next door: Harry Beck, Rinus Michels, Dick Fosbury. After them, there can be no going back to thinking or acting as before, and this can happen in a wide variety of human activities. Most importantly, it happens thanks to normal people like the next-door neighbor, the “scruffy” Masaccio.

When, many years ago, I approached art history (an inevitable step for those born in Florence), my father suggested that I start with the Brancacci Chapel to get an idea of the grandeur of 15th-century Florence.

This is one of the reasons why, so many years later, I wanted to name one of my portfolios after Masaccio, the painter who started the Renaissance. A portfolio that contains a heterogeneous set of titles, both in terms of strategy and type, which can change from time to time in response to any needs that may arise. A “portfoliaccio,” as unruly as the artist who inspired it.

The Wild Bunch

As you may know, my investments are in fact divided into three different portfolios; Cupolone, my primary CEF portfolio; Giotto, my ETF portfolio; and indeed, Masaccio.

Cupolone Income Portfolio (named after Brunelleschi’s Florentine dome) is my strategic, primary investment portfolio, the backbone of my overall portfolio. Its solid, structured foundation is based on the following sixteen CEFs:

- BlackRock Science And Technology Trust (BST)

- Calamos Dynamic Convertible and Income (CCD)

- Calamos Global Total Return (CGO)

- Eaton Vance Enhanced Equity Income II (EOS)

- Eaton Vance Tax-Adv. Global Dividend Opps (ETO)

- Eaton Vance Tax-Adv. Dividend Income (EVT)

- Guggenheim Strategic Opp (GOF)

- John Hancock Tax-Adv. Dividend Income (HTD)

- PIMCO Corporate & Income Strategy (PCN)

- PIMCO Dynamic Income (PDI)

- John Hancock Premium Dividend (PDT)

- PIMCO Corporate & Income Opportunities (PTY)

- Cohen & Steers Quality Income Realty (RQI)

- Special Opportunities Fund (SPE)

- Cohen & Steers Infrastructure (UTF)

- Reaves Utility Income (UTG)

Giotto Income Portfolio (named after the fourteenth-century Florentine painter and architect) includes five ETFs that adopt a covered-call strategy. A slender portfolio, like Florence’s cathedral bell tower that bears his name.

- JPMorgan Equity Premium Income (JEPI)

- JPMorgan Nasdaq Equity Premium Income (JEPQ)

- Global X NASDAQ 100 Covered Call (QYLD)

- Global X Russell 2000 Covered Call (RYLD)

- Global X S&P 500 Covered Call (XYLD)

Masaccio Income Portfolio is my third, “tactical” portfolio, which contains these five titles:

- Ares Capital (ARCC)

- Crescent Capital (CCAP)

- Royce Value Trust (RVT)

- Credit Suisse Crude Oil Shares Covered Call ETN (USOI)

- XAI Octagon FR & Alt Income Term Trust (XFLT)

There are 26 titles in total. They all offer monthly distribution with the exception of ARCC, CCAP, and RVT, which have quarterly distributions.

Right now, the portfolio as a whole is losing a few percentage points, which is, all in all, an acceptable situation given the markets’ performance during 2022. Several CEFs are still making gains relative to their load price (ETO, EVT, HTD, PDT, RQI, UTF), but most of the positions built during the year are now in the red. Patience is needed: portfolios of this type offer the desired results only in the long run. Also, thanks to the reinvestment (in full or in part) of dividends, a broad view should always be taken in their creation and management.

Check Up of My Portfolio

Let us briefly look at the criteria behind my choices and my reasons for keeping these titles in my portfolio, starting with the sixteen CEFs that make up Cupolone, then examining the Giotto ETFs and finally the Masaccio securities.

Cupolone Income Portfolio

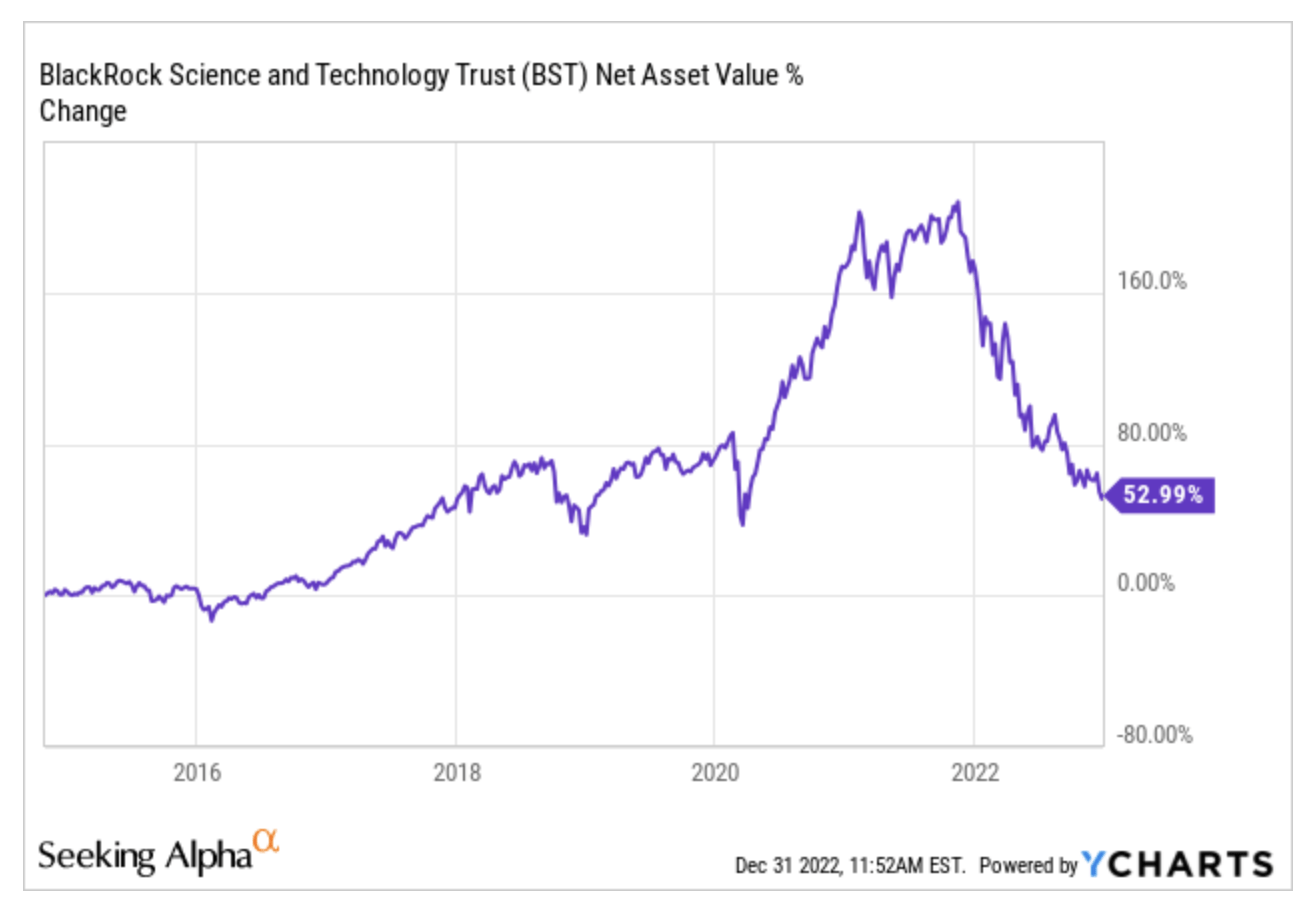

BST is a fund launched by BlackRock in late 2014 and has grown dramatically for a full seven years. Its decline began in late 2021, parallel to the trend of the technology sector it refers to. Unfortunately, my load price is much higher than the current market price, but I see no reason to reduce or, much less, close my position.

YCharts

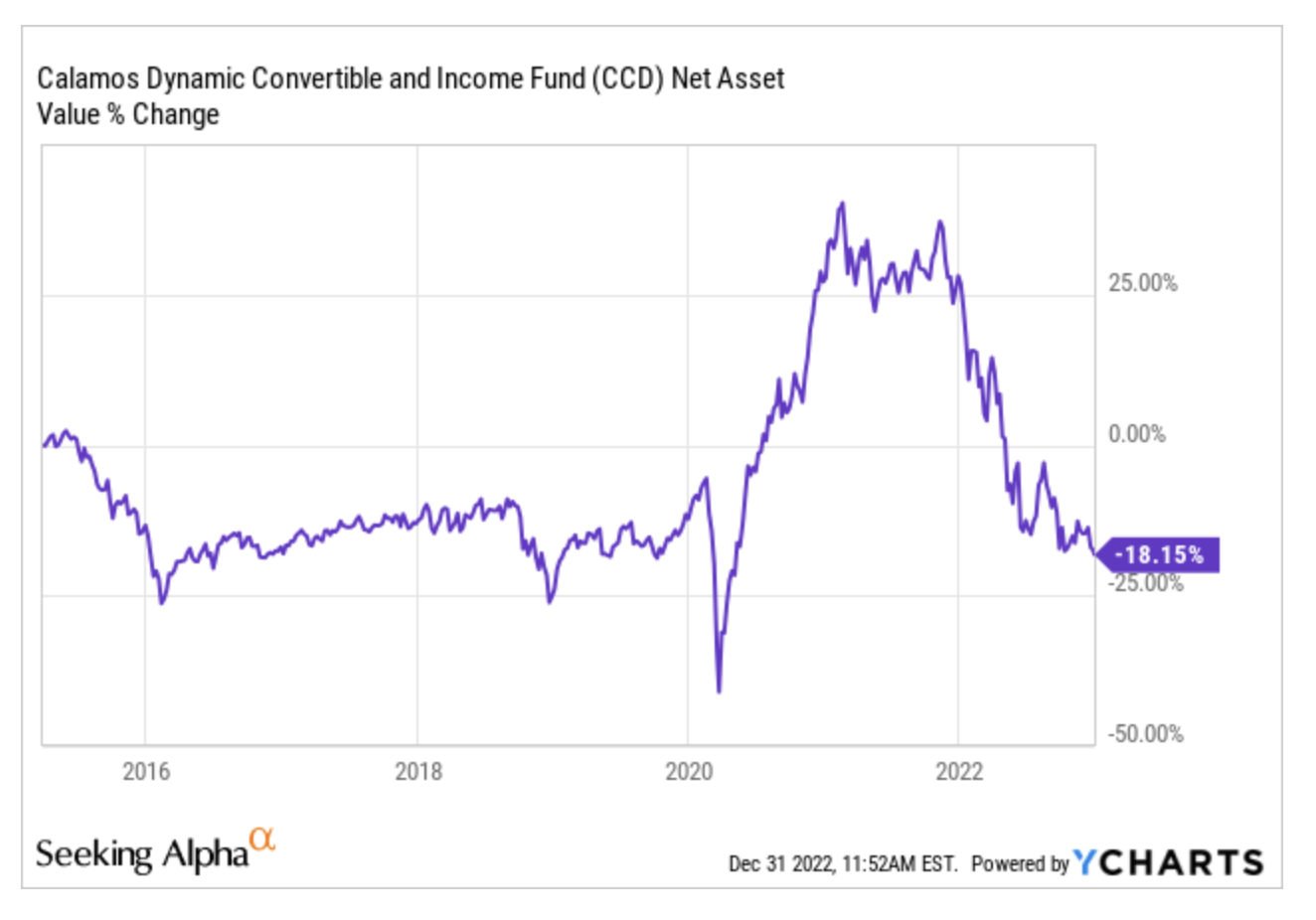

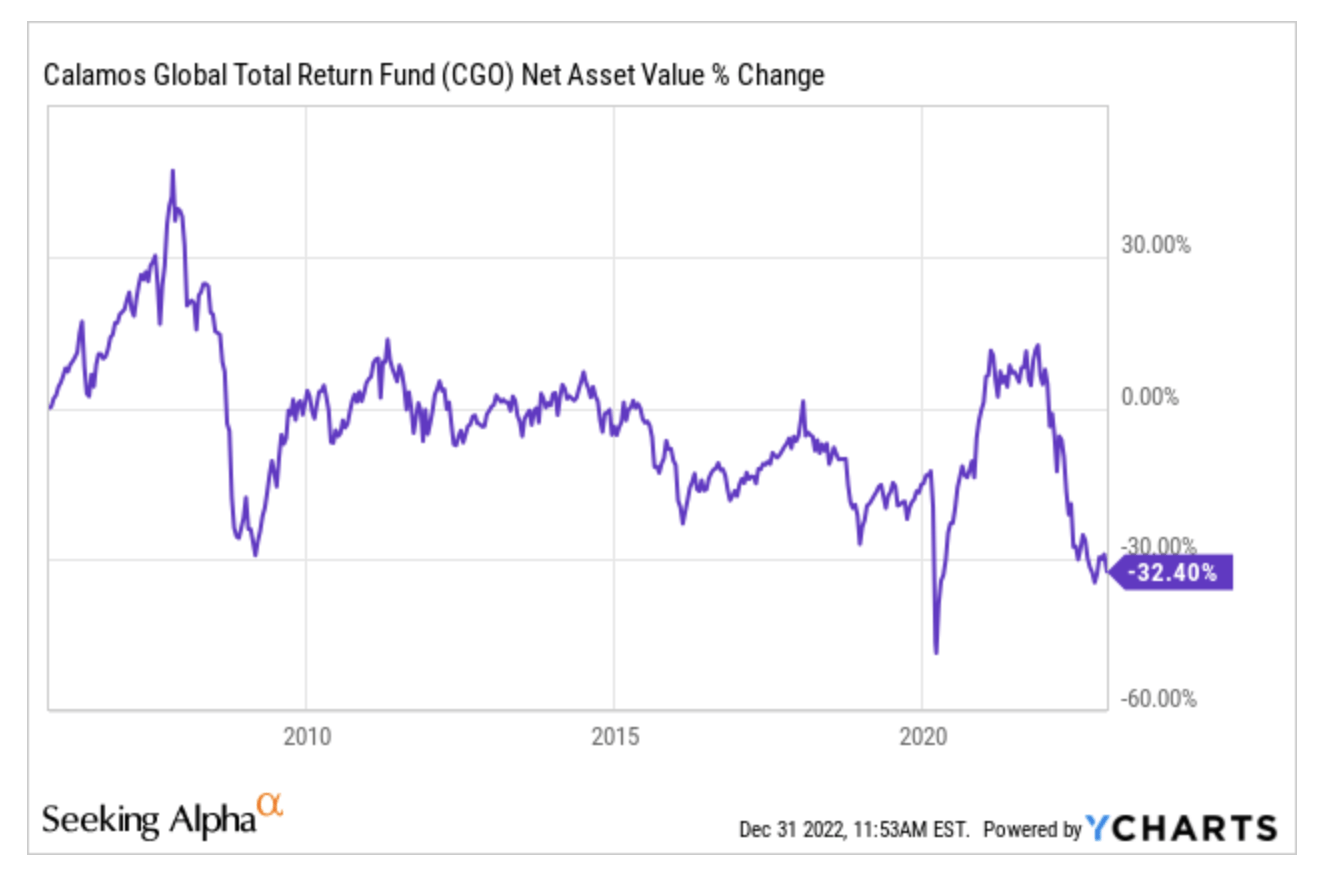

CCD and CGO are two Calamos funds, the former invested mainly in convertible bonds while the latter is a fairly diversified Global Allocation equity. CCD has lost a lot since its recent highs but its NAV performance shows no particular signs of weakness compared to the average of the last few years, while CGO’s performance has been steadily declining, which recently prompted me to revise my views on this fund and reduce my exposure to it somewhat.

YCharts YCharts

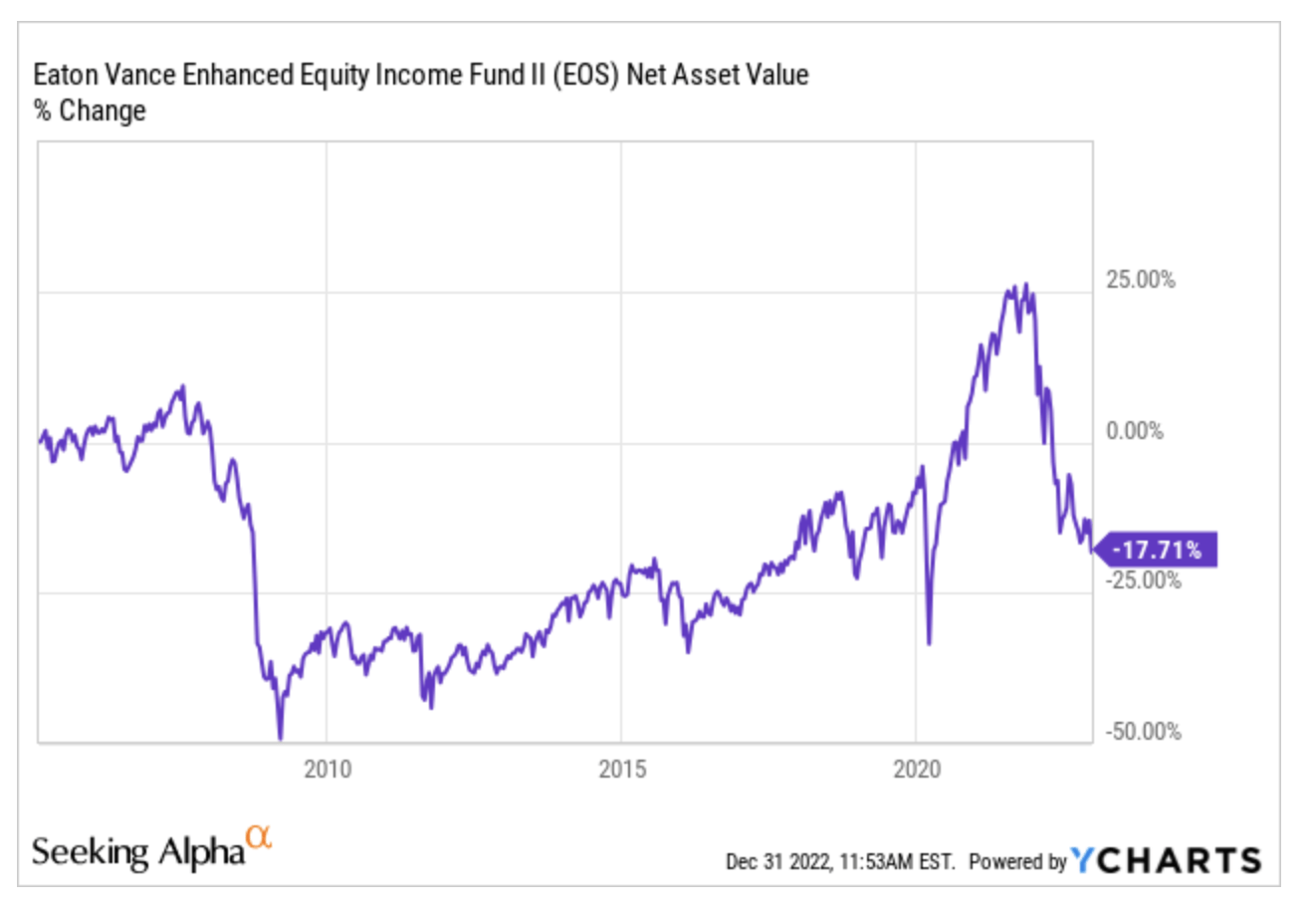

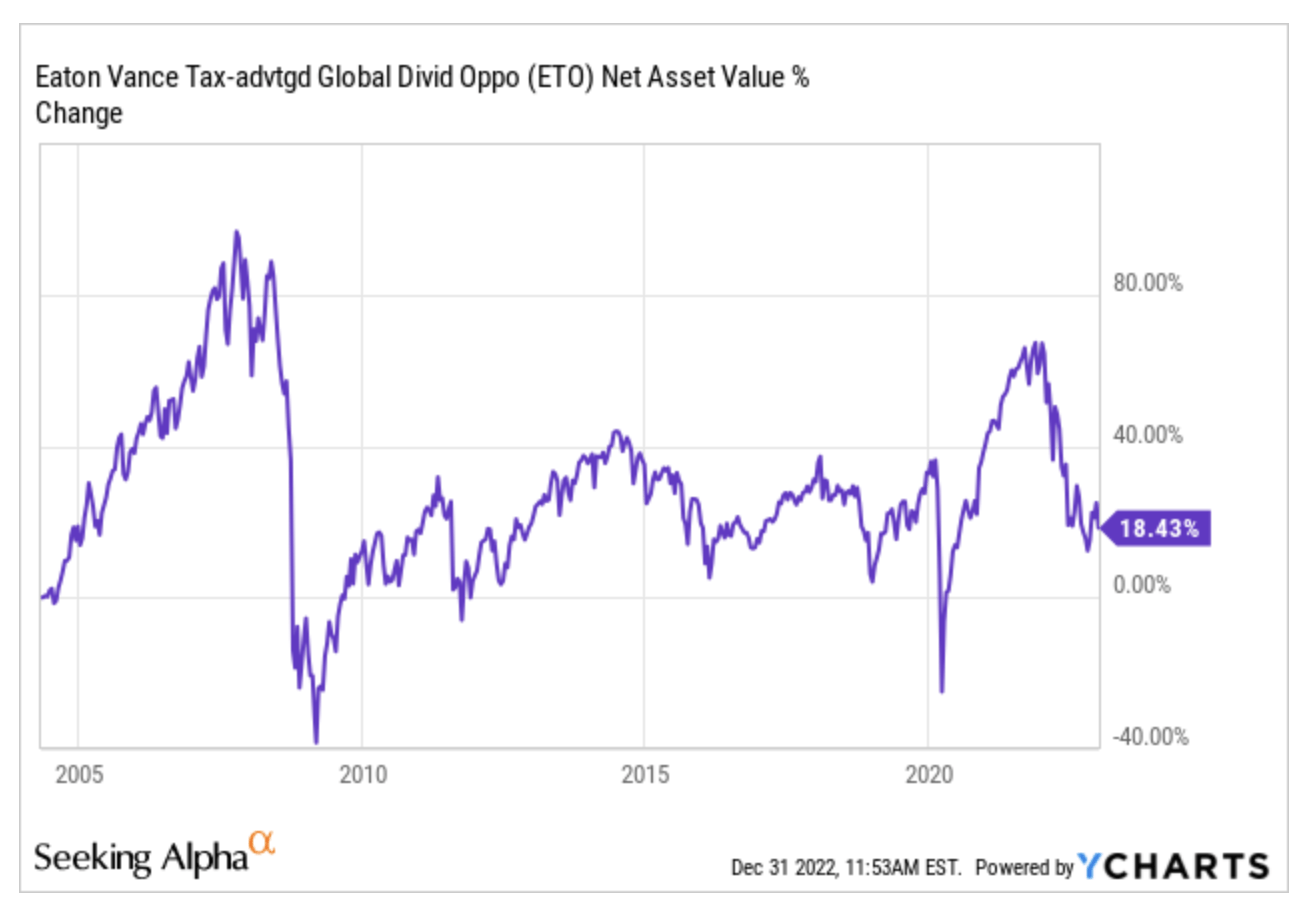

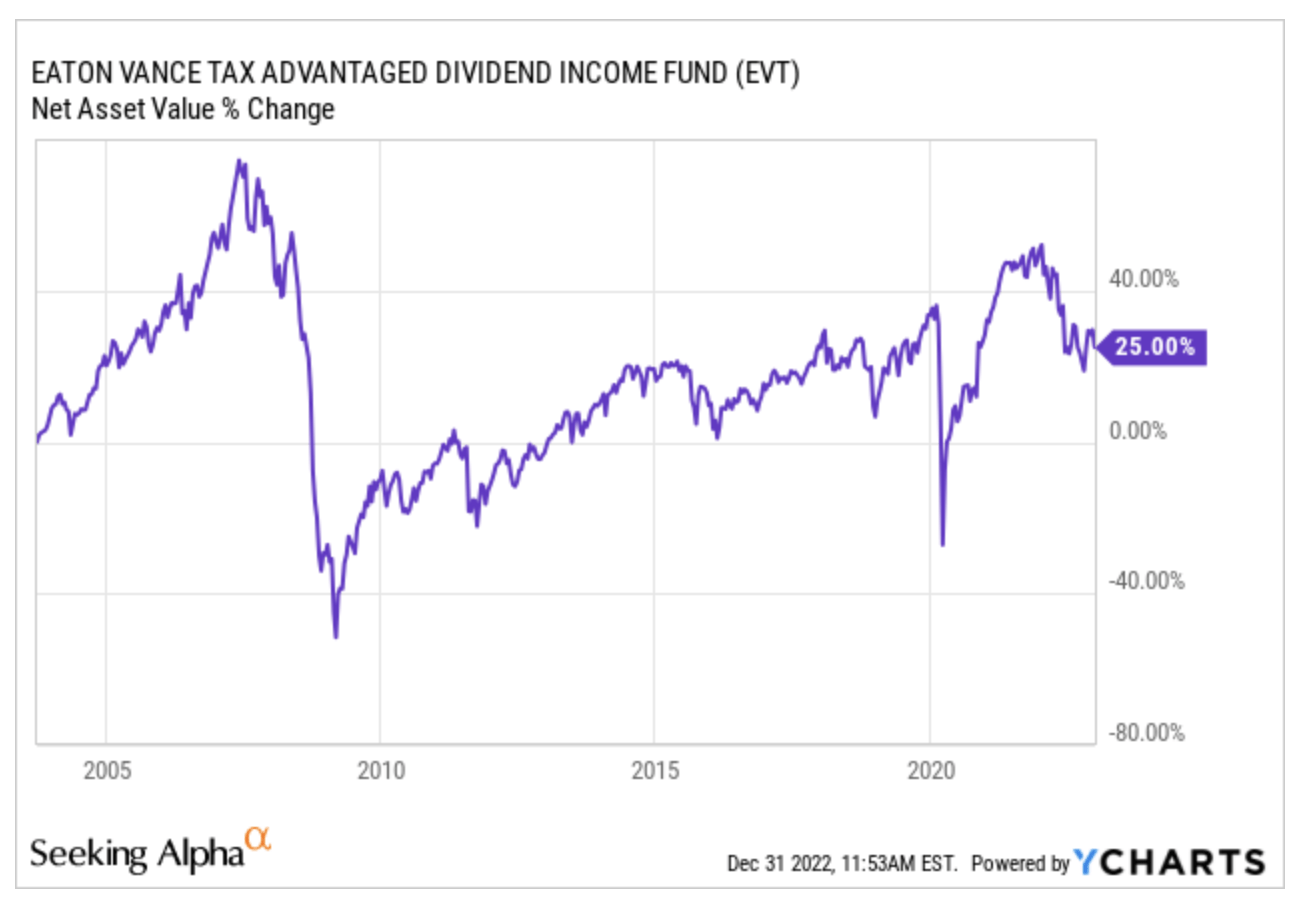

Of the three Eaton Vance funds (EOS, ETO, EVT), the first is an inclusion from 2022, while the other two have been in my portfolio since 2020. EOS invests in growth stocks among diversified sectors and also generates its earnings from selling call options; ETO is a Global Allocation equity rather diversified in both sectors and countries; EVT is a 70-85% equity fund that invests mainly in the U.S. market. All three of these funds have lost a lot during 2022, but as far as I am concerned, the performance of their NAVs is of no particular concern, although EOS appears to be the weakest of the three.

YCharts YCharts YCharts

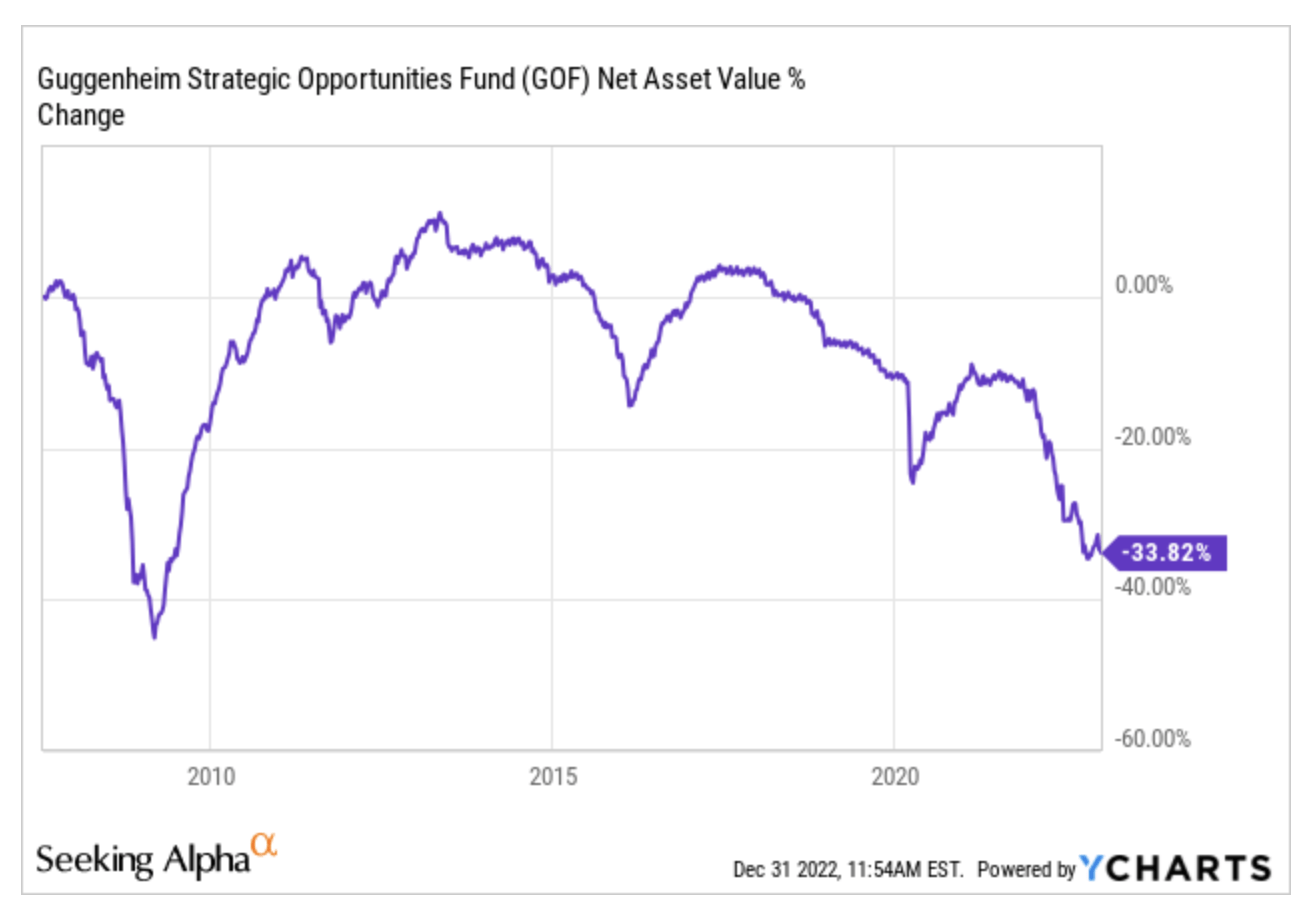

GOF is a multi-sector fixed income fund from Guggenheim, about which I continue to have strong doubts, summarized by the performance of its NAV, which has been steadily declining for years. After reading articles by people far more knowledgeable than I am on SA, I see that opinions differ widely. But for my part, over the course of 2022 I have reduced my exposure to this fund.

YCharts

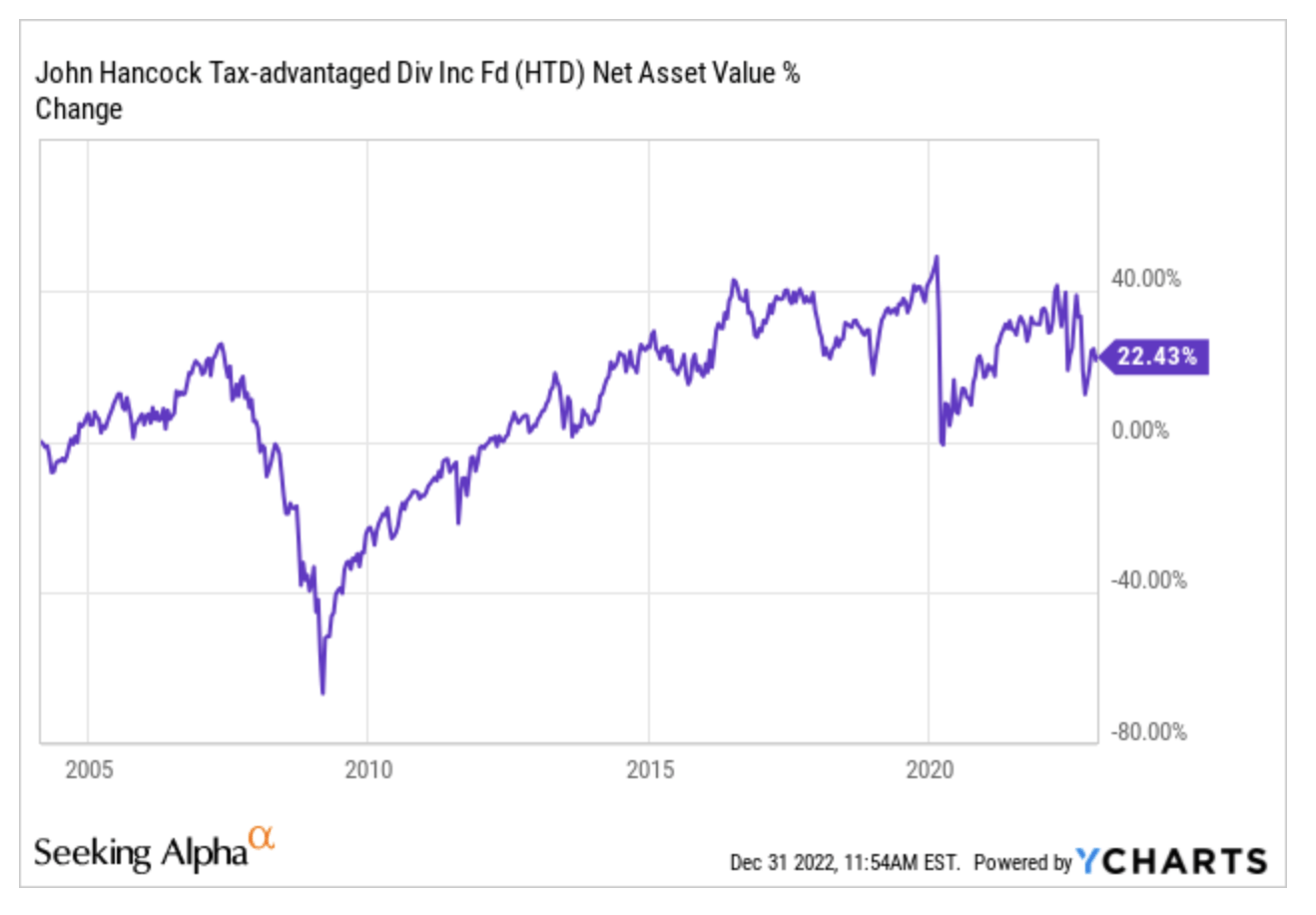

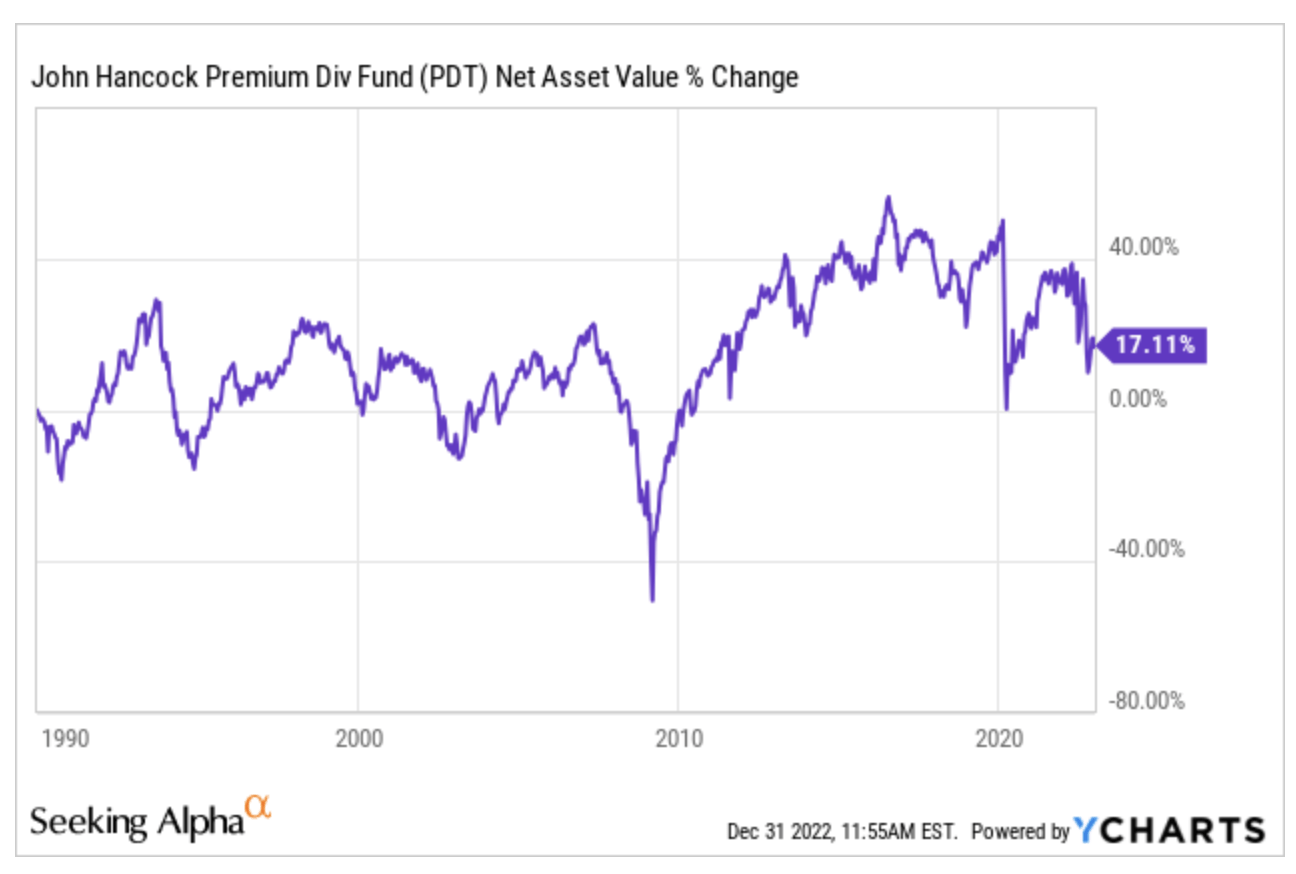

HTD and PDT are twin funds of John Hancock, both with 50-75% equity allocation mainly in the utilities sector, with a preferred stock component, which is more relevant in PDT. I have a slight preference for HTD, but I consider them both to be excellent funds, which I intend to continue maintaining in my portfolio.

YCharts YCharts

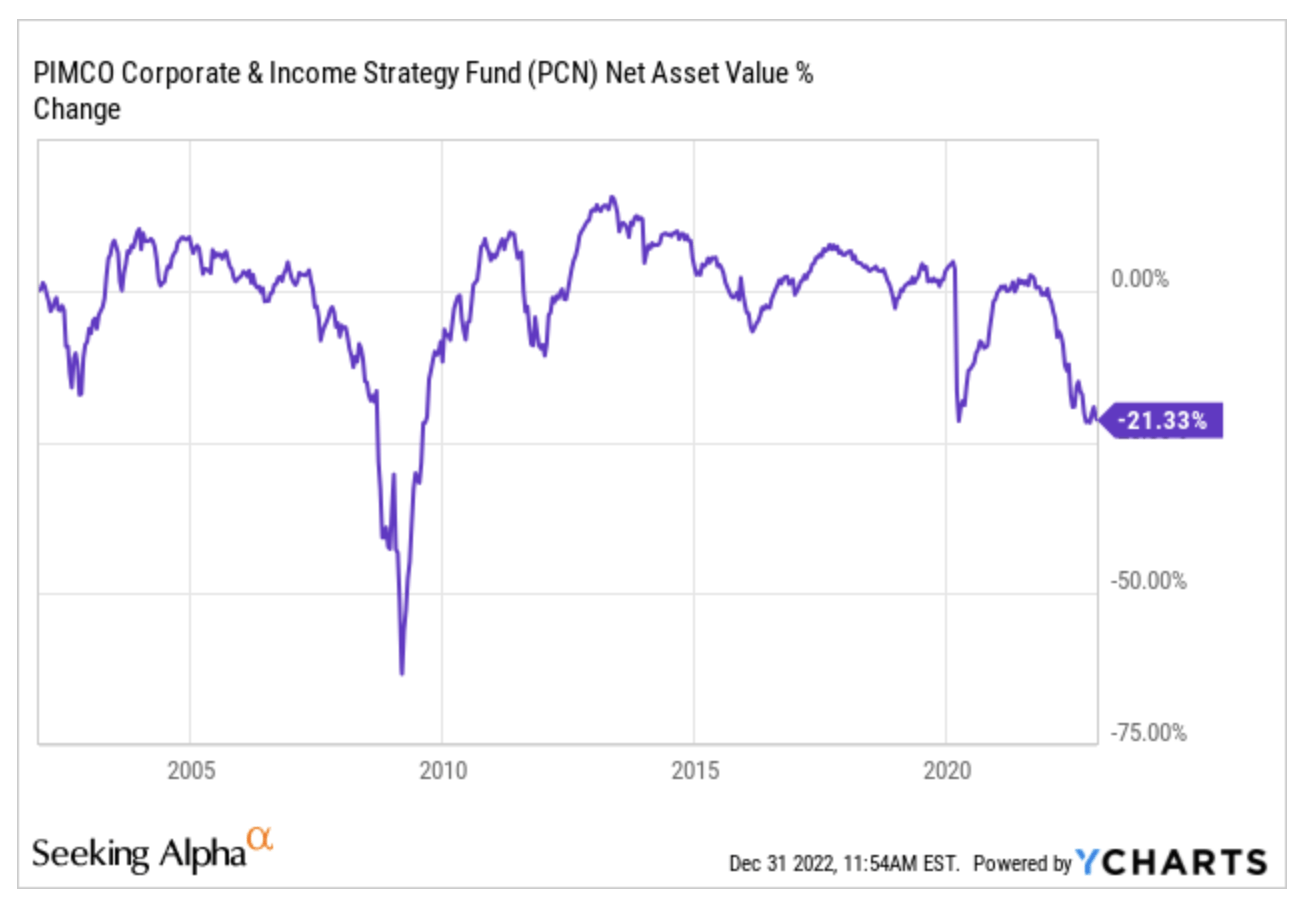

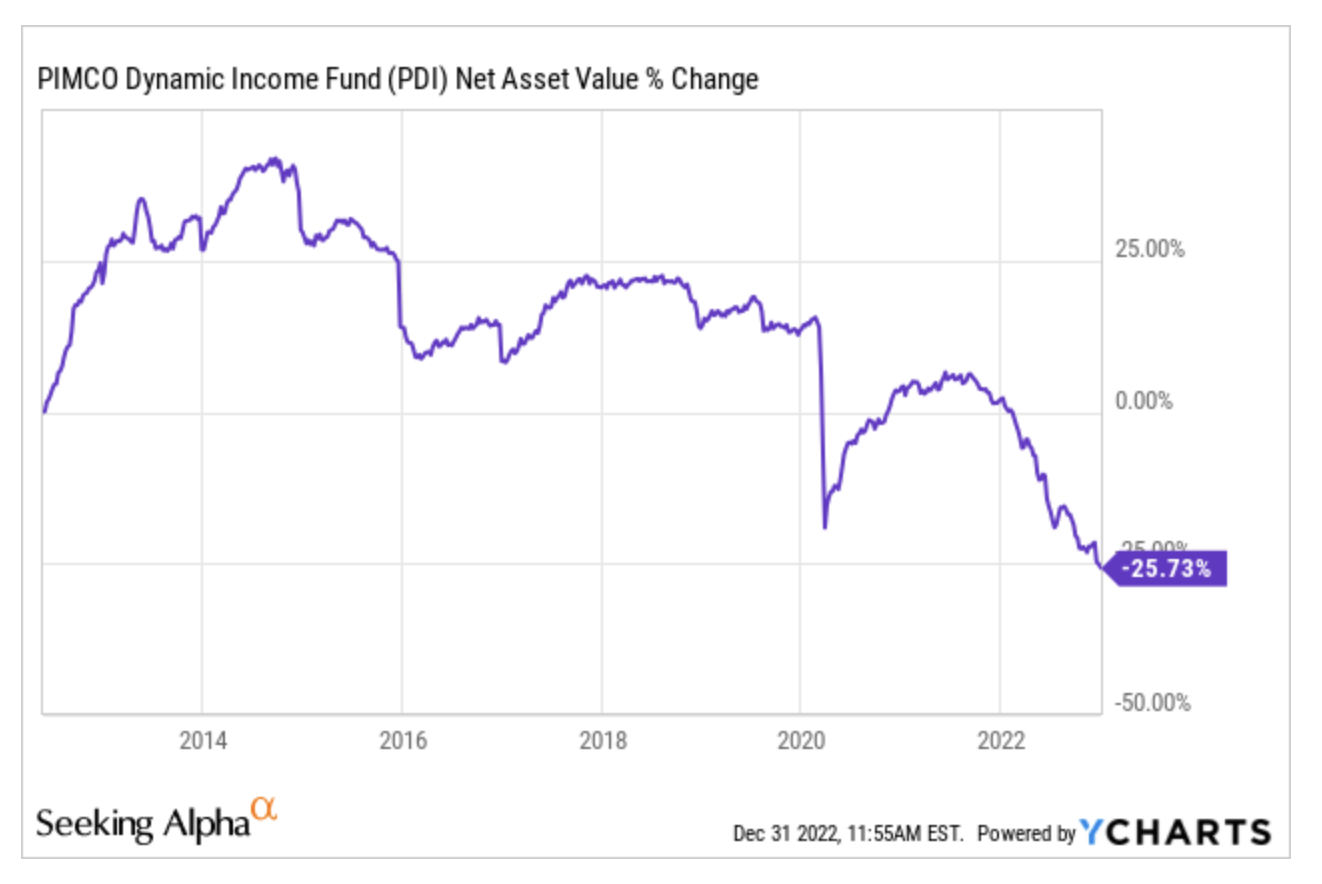

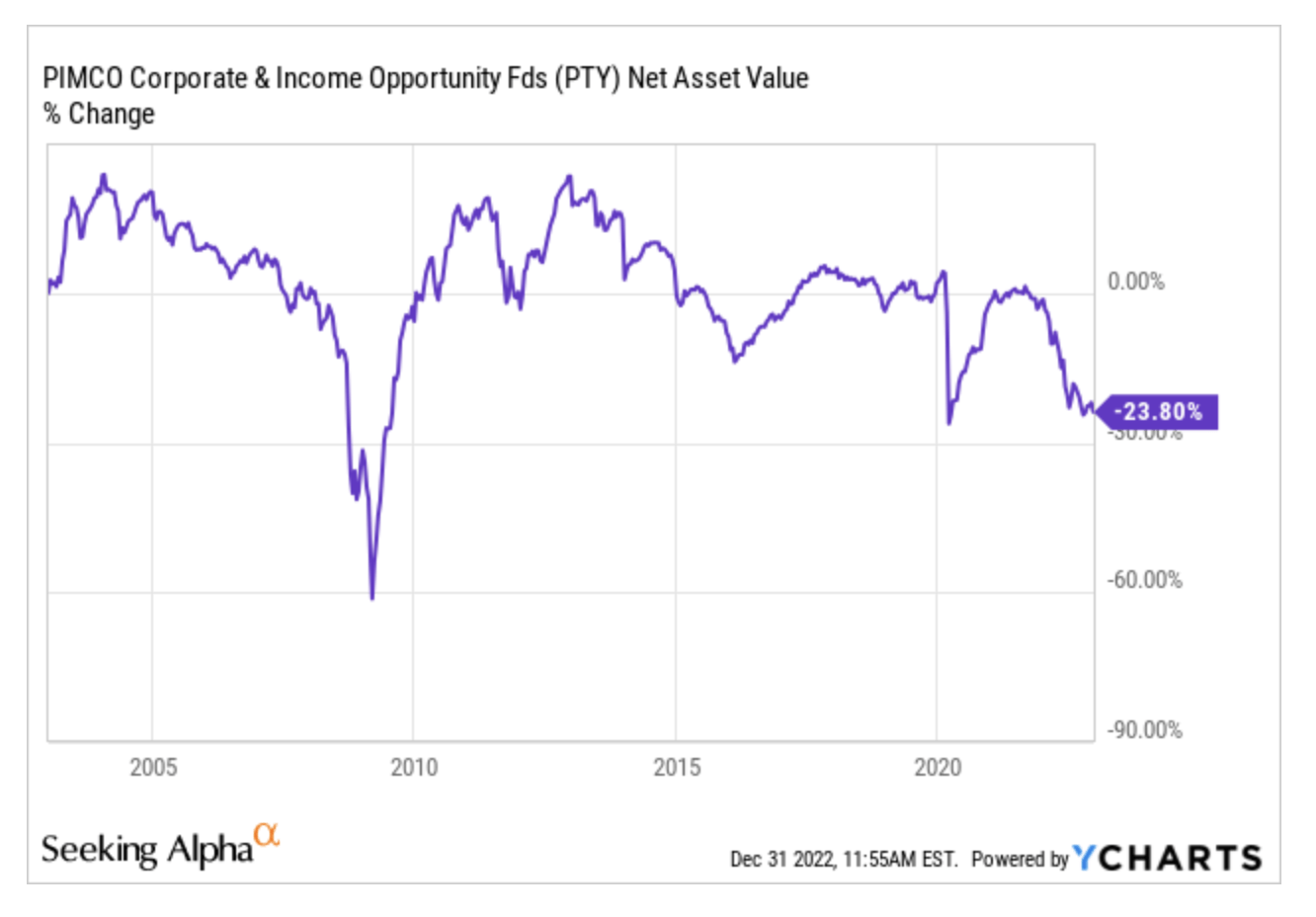

And here we come to Pimco’s three multi-sector fixed income funds (PCN, PDI, PTY), workhorses of many high-yield portfolios, mainly because of the fame attached to their managers’ names. With dissenting opinions among SA authors on the quality of these stocks as well, I personally continue to hold these in my portfolio despite the negative trend of their NAVs. I have a slight preference for PCN, but increased perplexity about PDI. PDI, in fact, has shown a steady descent for some years now that is difficult to attribute simply to the recent decline in the bond market.

YCharts YCharts YCharts

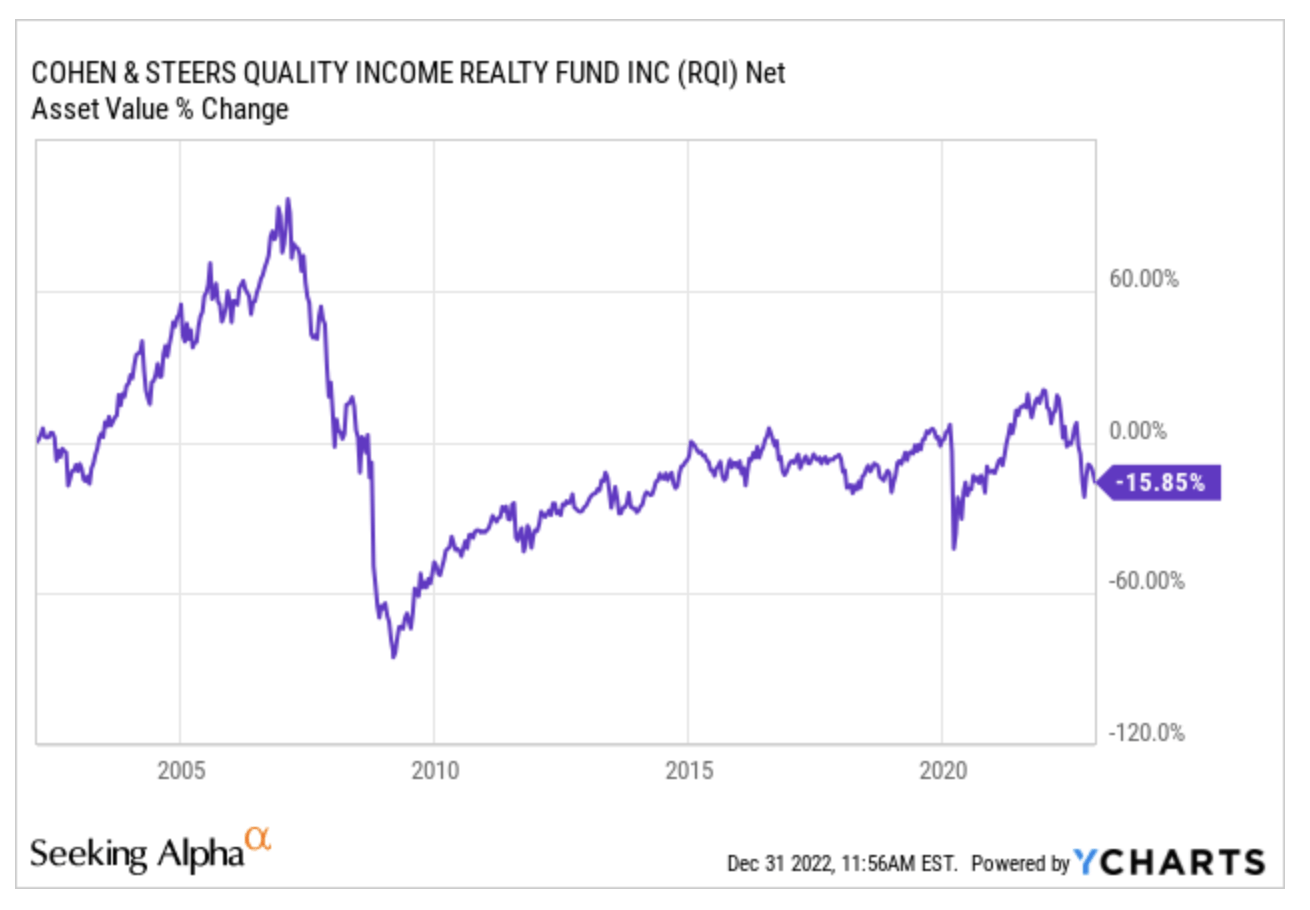

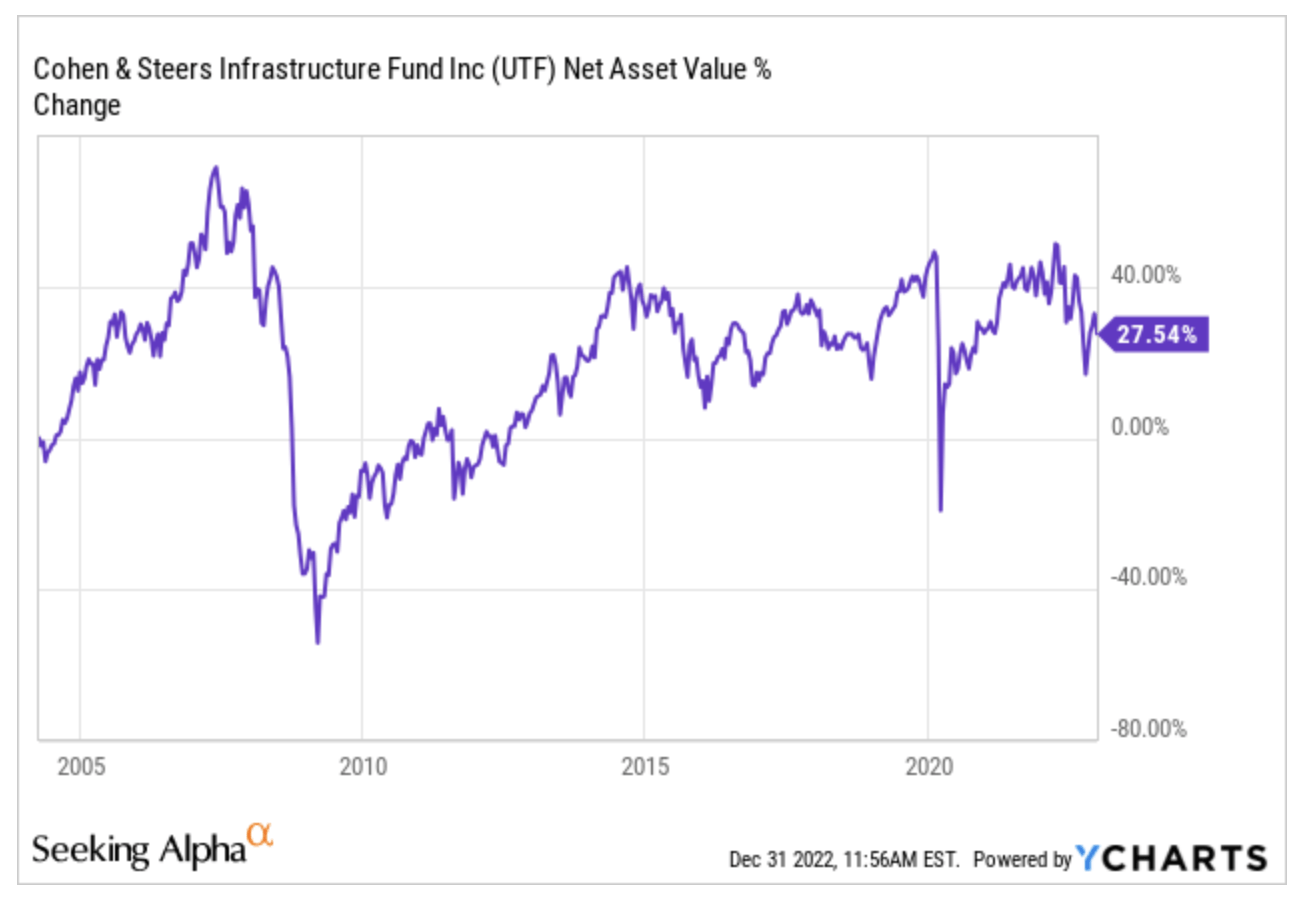

RQI and UTF are two Cohen & Steers funds that I consider among the best in my portfolio. The former is a Real Estate CEF, while the latter invests in infrastructures and utilities. A sideways trend for years for RQI’s NAV, while UTF showed steady growth for a decade.

YCharts YCharts

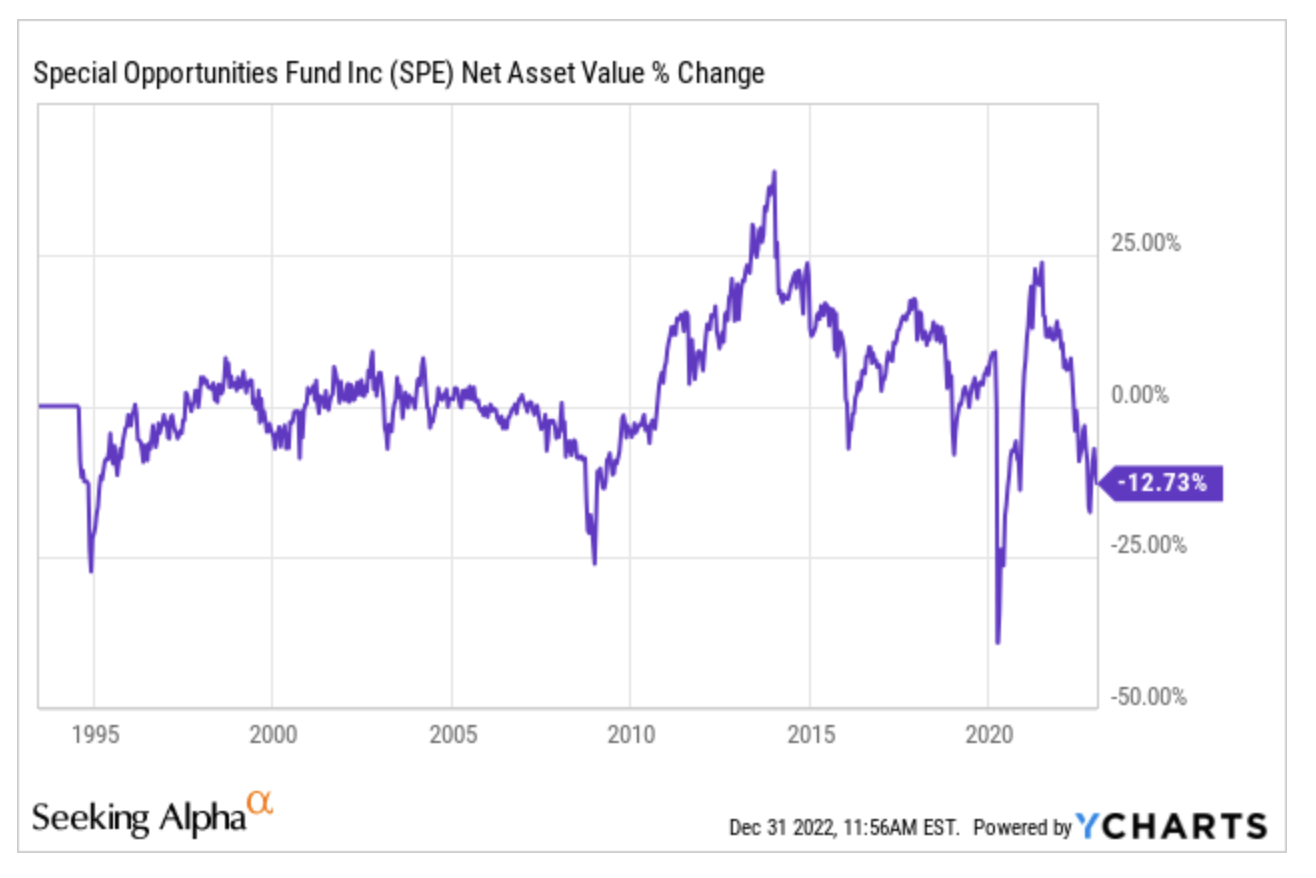

SPE is a CEF from Bulldog Investors classified as Tactical Allocation, a definition that implies a diversified blend of equity, bond, BDC and SPAC investments. Notable volatility has characterized this fund as well, whose retention in the portfolio, however, does not cause me particular concern.

YCharts

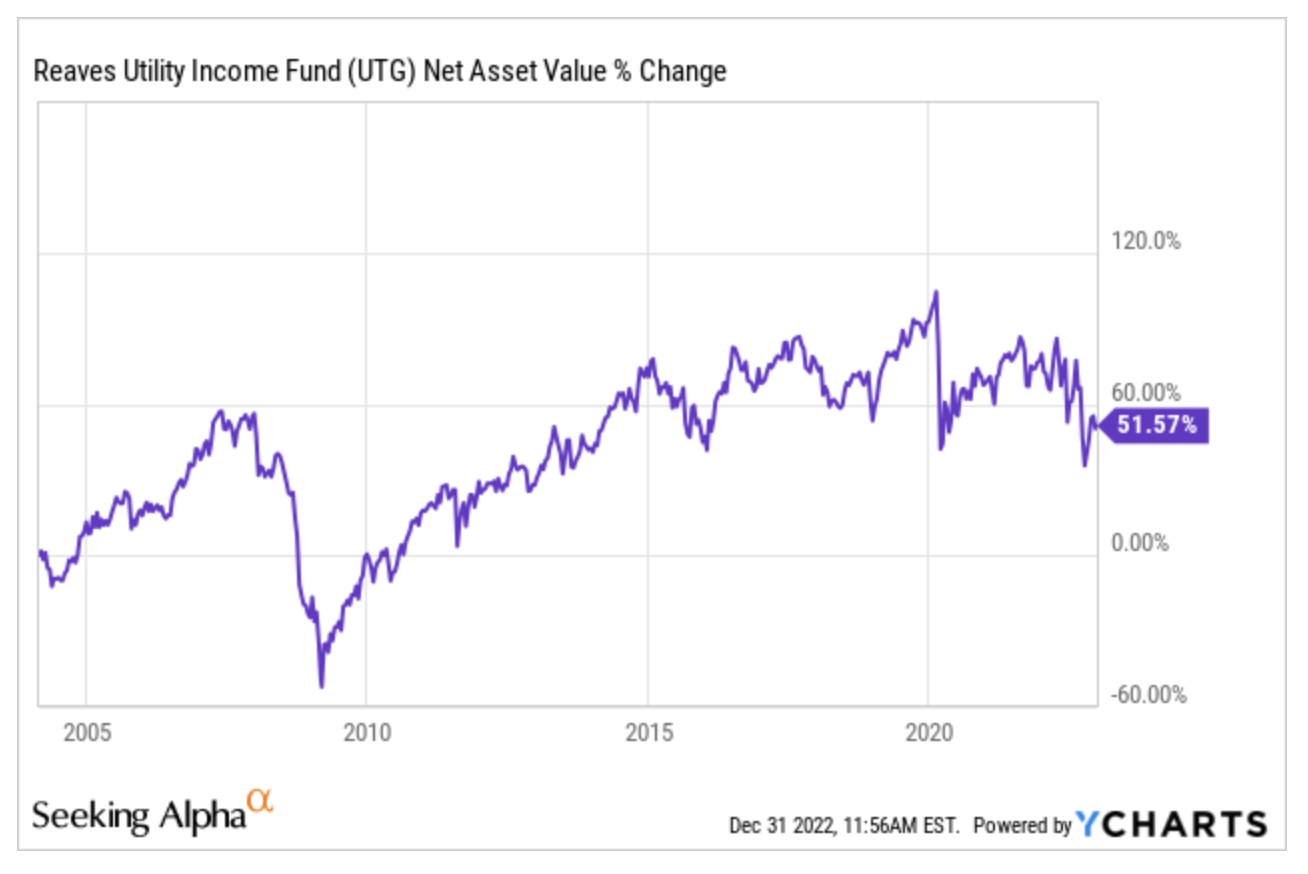

UTG, finally, is a Reaves fund that invests in utilities, among the best and most stable in my entire portfolio. A steady upward trend for more than a decade, with obvious swings starting in 2020.

YCharts

Giotto Income Portfolio

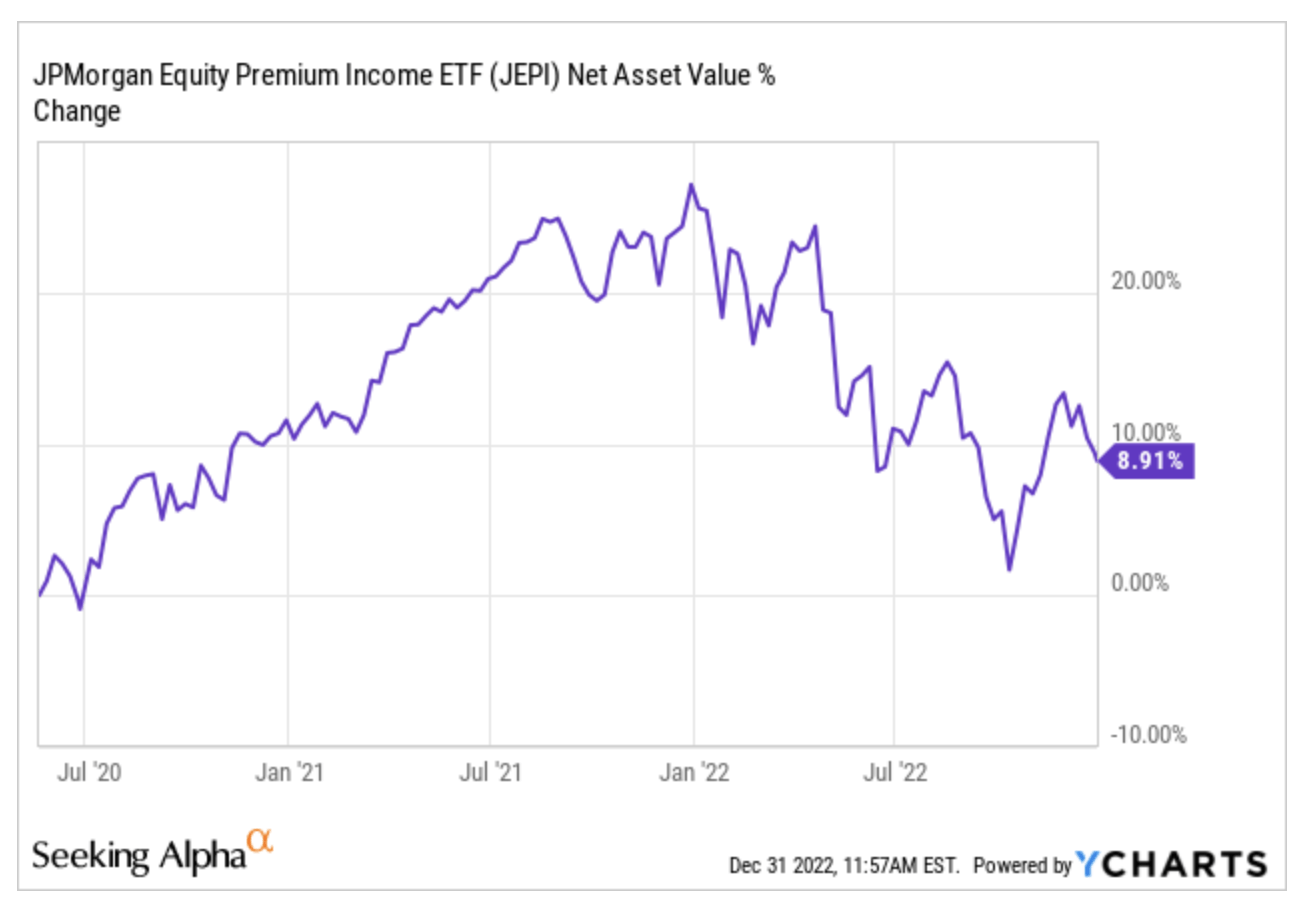

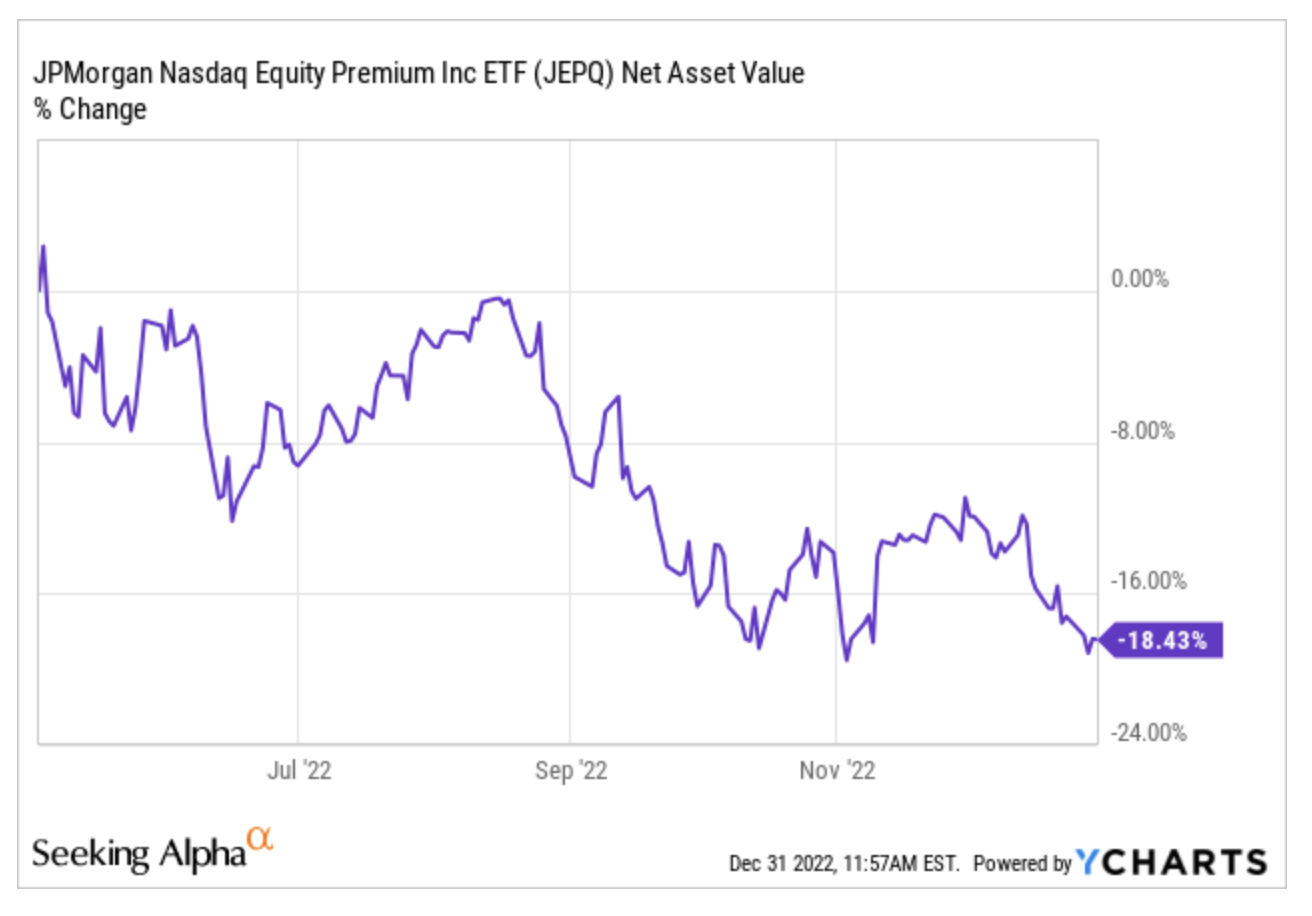

JEPI and JEPQ are two JP Morgan covered call ETFs, the former launched in 2020, the latter in 2022 and recently joined my stable. JEPI trades on the S&P 500 with derivatives while its younger brother, JEPQ, adopts the same strategy on the NASDAQ. JEPI’s behavior is excellent, while JEPQ’s NAV has suffered more, as did its sector.

YCharts YCharts

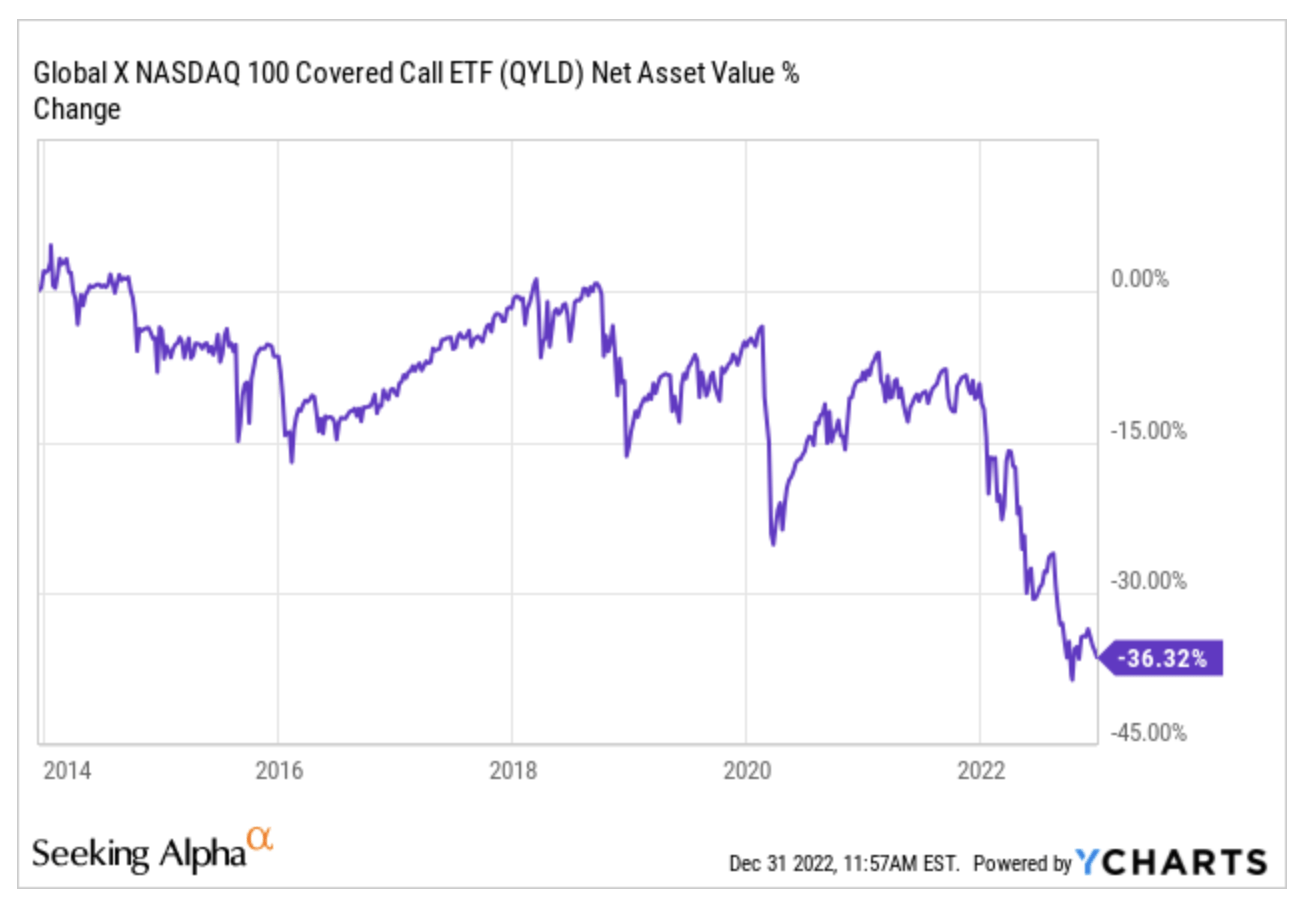

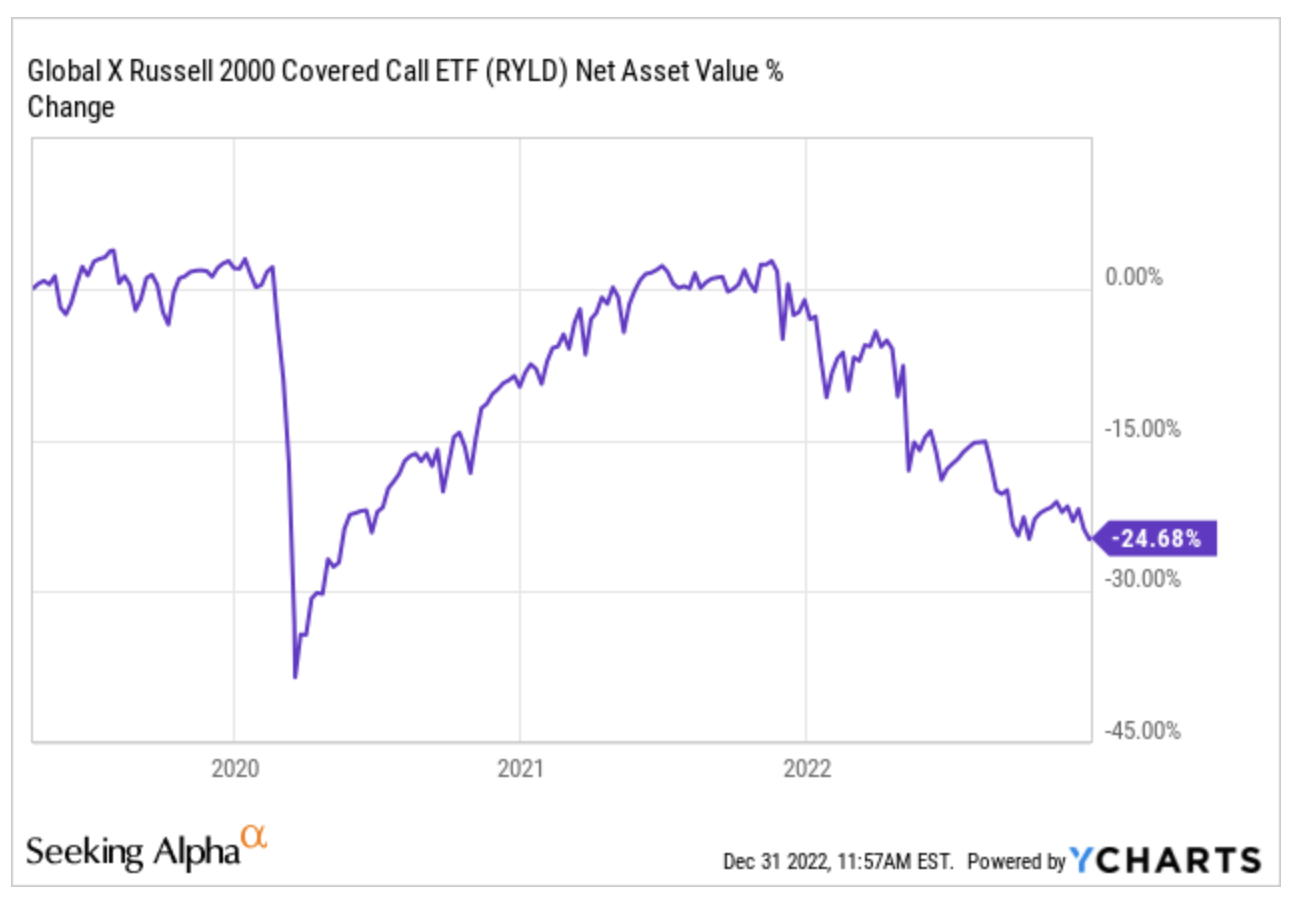

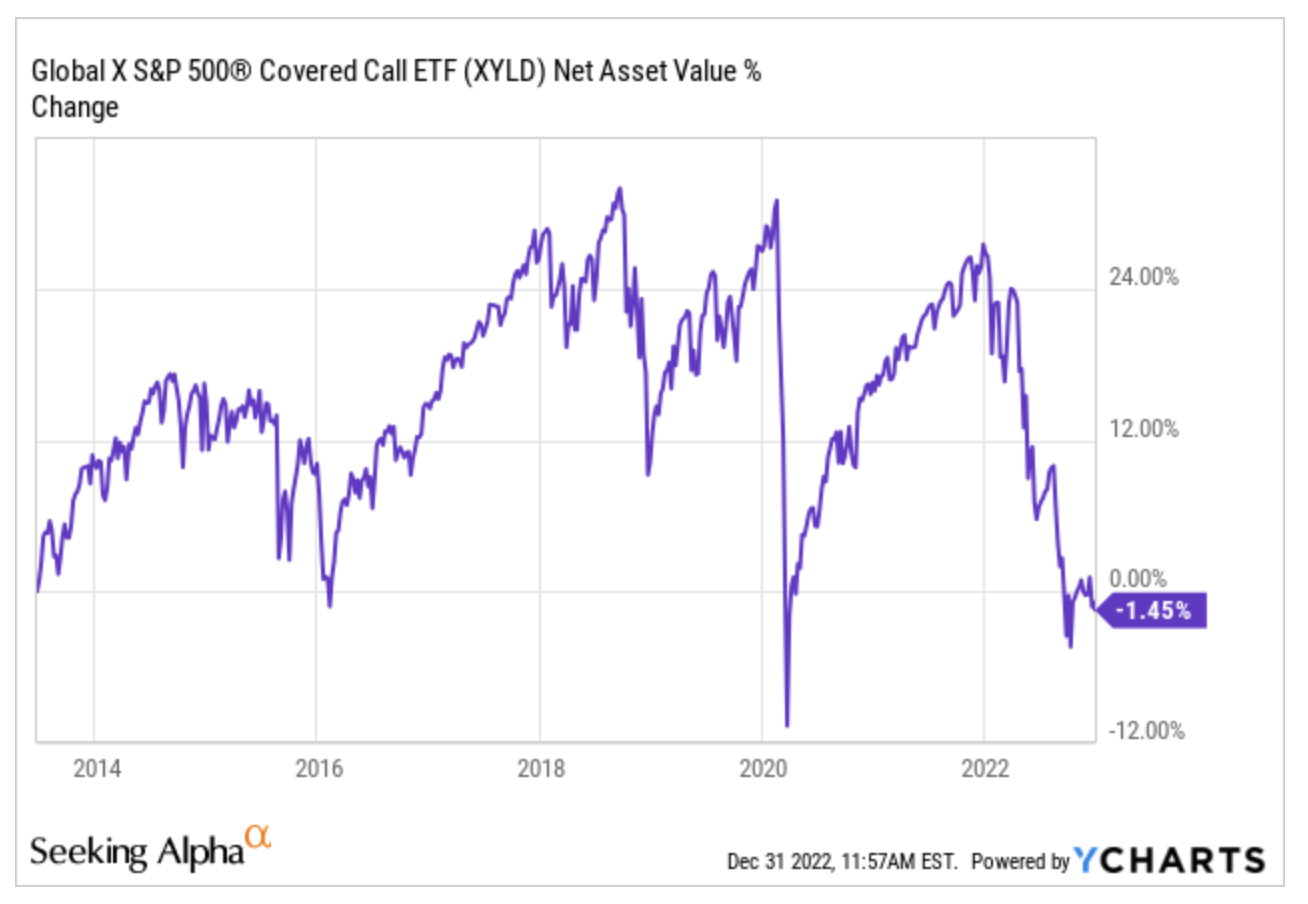

QYLD, RYLD and XYLD are three Global X covered call ETFs that invest in the NASDAQ, Russell 2000, and S&P 500, respectively. NAVs are down sharply since launch for the first two, with QYLD trending more negatively, while XYLD is sailing around parity after years of ups and downs. I remain confident in all three of these ETFs, although I have a stronger belief in XYLD. So, over the course of 2022, I lightened my positions in QYLD and RYLD in favor of XYLD.

YCharts YCharts YCharts

Masaccio Income Portfolio

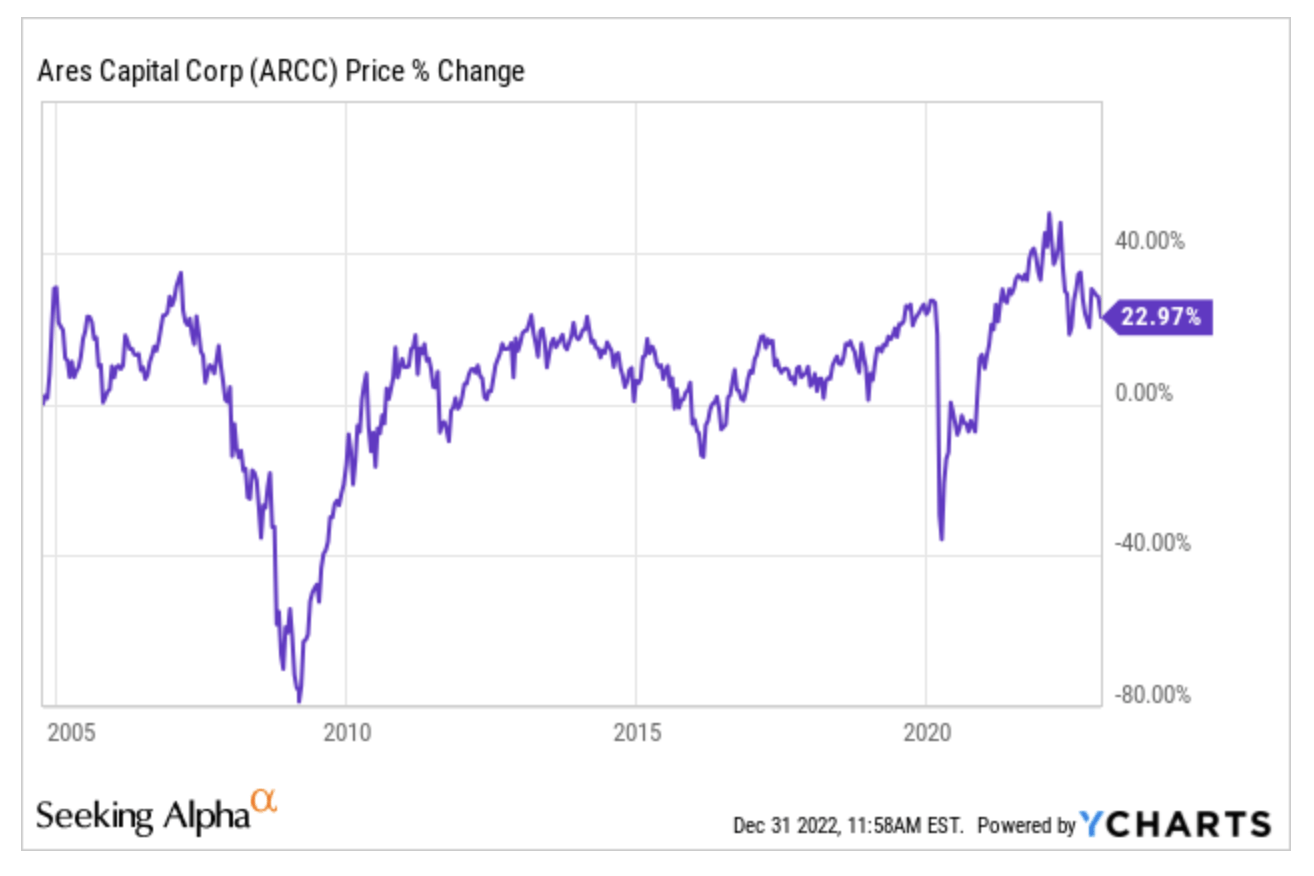

ARCC is one of the best Business Development Companies (BDC) on the market, included in my portfolio because of its quality, also revealed by its share price performance. After selling it last summer, I bought it back in the fall despite the fact that it is tax inefficient for me because of how its dividends are taxed in Italy.

YCharts

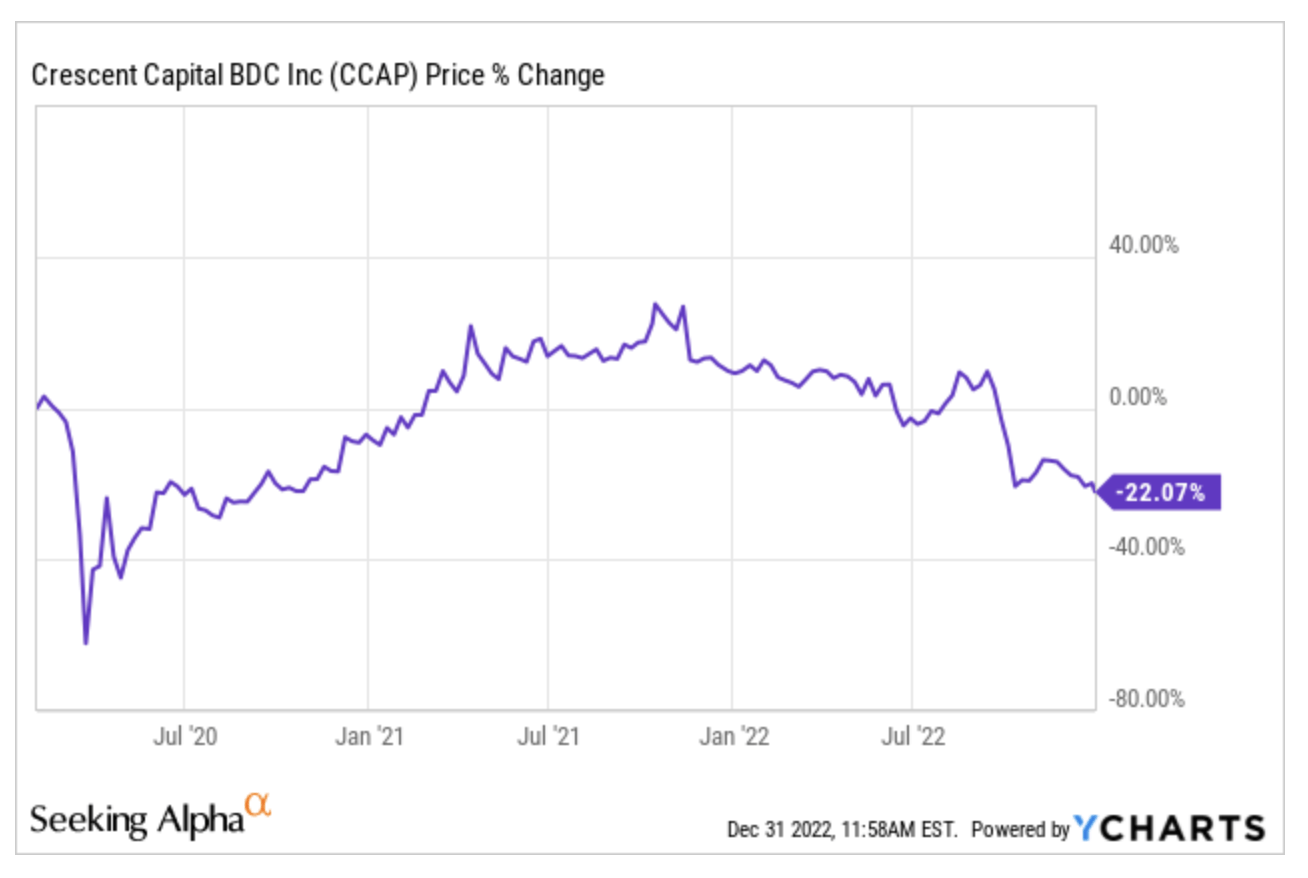

The same holds for CCAP from the tax point of view, but I also decided to put this BDC back into my portfolio because of its prospects, highlighted by various authors here on SA, including Steven Bavaria, a person I hold in high esteem.

YCharts

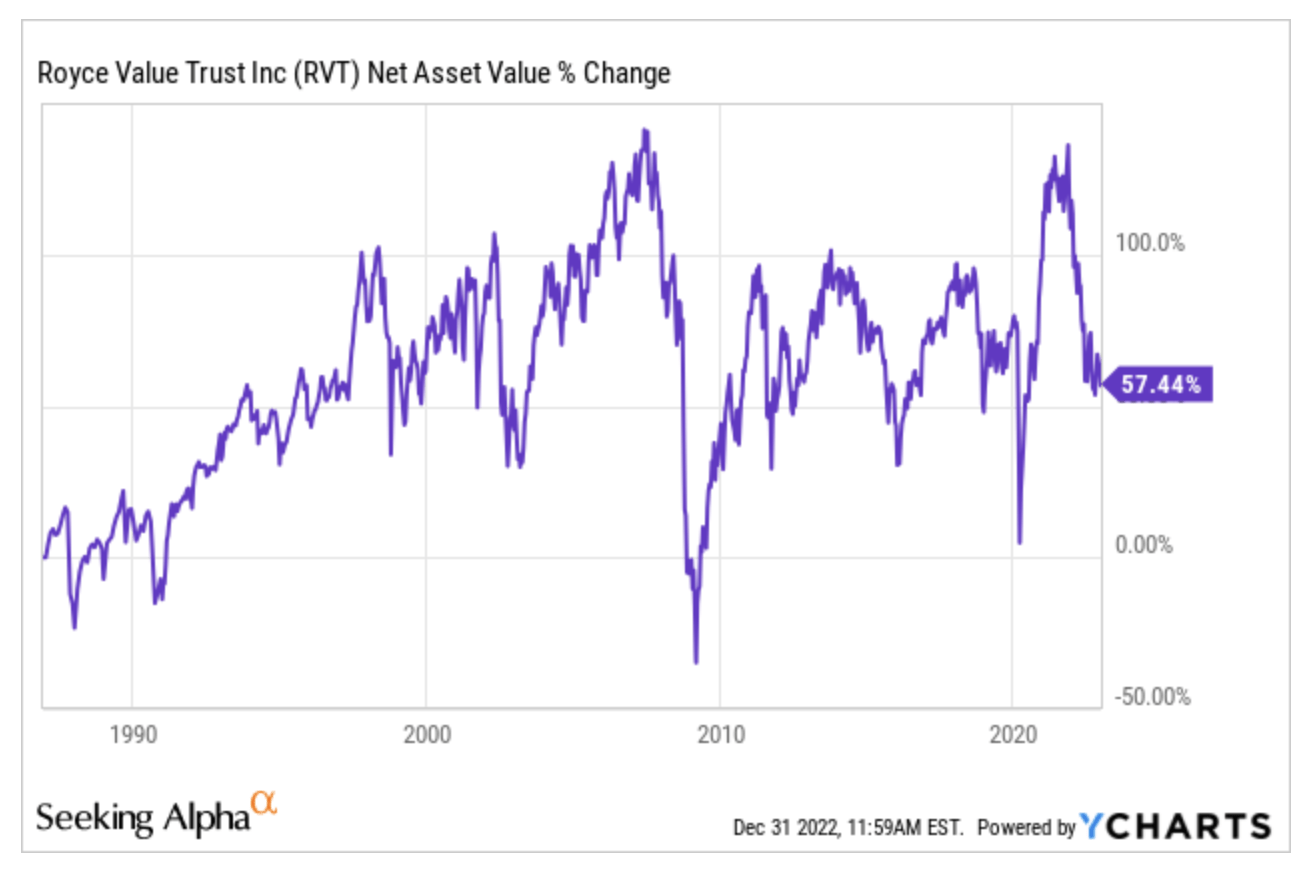

RVT is a small-cap focused CEF that has been in the market for several decades, whose NAV shows a fluctuating but growing trend, which makes me comfortable about its presence in my portfolio.

YCharts

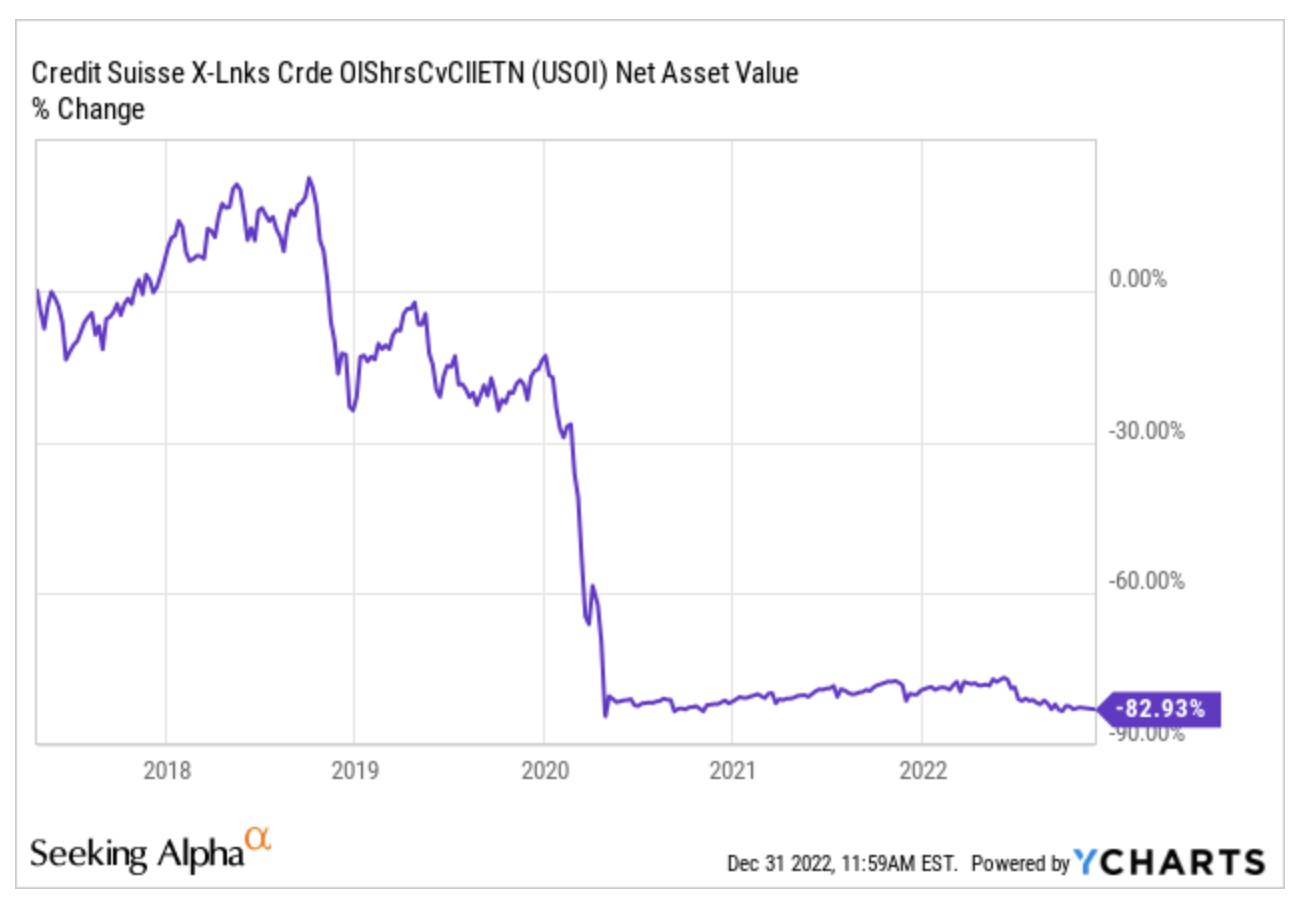

USOI is a Credit Suisse covered call ETN, which is in my portfolio because of its peculiar dividend feature for me as an Italian, being able to offset with it my past losses. My repurchase after the summer sale has this sole purpose, in the hope that its value will not fall further. It is, however, a risk I have decided to take, while not exposing myself too much.

YCharts

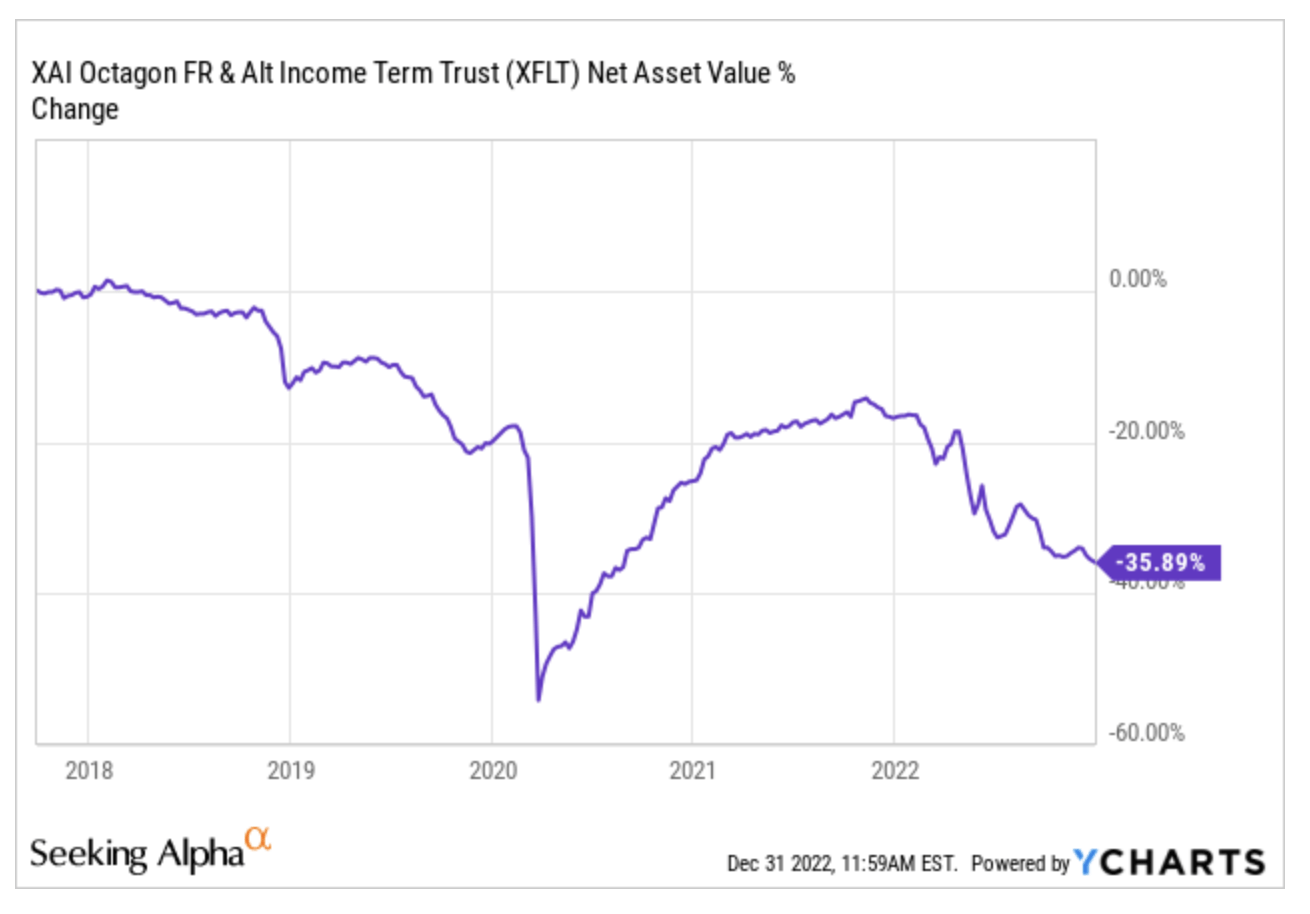

Finally, XFLT is a CEF that invests in Collateralized Loan Obligations (CLOs) and has a good reputation among some SA authors (including Steven Bavaria) especially for the quality of management. The NAV performance is not the most exciting, but I want to give it confidence.

YCharts

The Knight Move

I guess few people expected it (certainly not me), but in a year like 2022, Pimco’s managers have taken many of us aback with a nice, special distribution under the tree to end the year with a bang. It is true that special distributions have a different origin than ordinary ones, but in the case of many Pimco funds, the problem of sustainability remains given their very high yields in a suffering market like the current one. Nonetheless, we shall see how the situation evolves, without undue anxiety.

Indeed, it is curious how we all scramble to pose and solve other people’s problems: there is in all of us an irresistible tendency to mimic others, to anticipate their thoughts, their will, their moves. Then reality presents itself, and it is almost always different from what we imagined, so the scenario changes and we have to revise our beliefs or adjust our expectations. So much useless effort along the way!

One day, Giulio Andreotti, a politician of Italy’s so-called “First Republic,” amused himself by expounding a kind of homemade “phenomenology of problems.” According to him, 25 percent of problems vanish 48 hours after they are declared fundamental, another 25 percent solve themselves or others solve them, and 25 percent belong to the category of unsolvable problems. Thus, three out of four problems are not worth dealing with, or in any case dealing with them head-on only serves to do harm. That leaves only the last “quarter,” that 25 percent of issues that need to be taken care of, followed up and solved.

Frankly, I wouldn’t know in which category to classify the “problem” of Pimco distributions, but for now I’m enjoying their “Christmas gift” and trying to look serenely ahead to a 2023 that promises to be anything but easy.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment