serts/E+ via Getty Images

iShares Global Materials ETF (NYSEARCA:MXI) is an exchange-traded fund that provides investors with exposure to companies engaged in the production of raw materials, such as metals, chemicals, and forestry products. I last covered the fund in June 2022, in which I thought MXI was undervalued. Since then, it has appreciated by 9.93% against the S&P 500’s move of 11.31%, although relative performance is basically neutral after accounting for dividends.

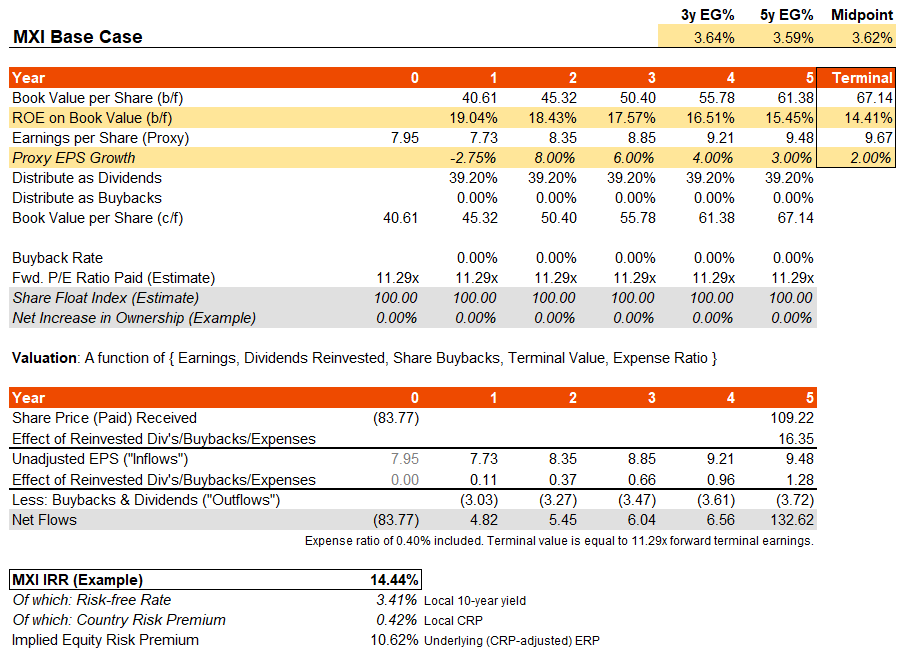

MXI’s benchmark index, which it seeks to replicate, is the S&P Global 1200 Materials Sector Index. Based on the most recent factsheet, the trailing and forward price/earnings ratios of MXI’s benchmark (a proxy for MXI’s portfolio itself) were 10.98x and 11.29x, respectively (as of January 31, 2023). This data implies negative earnings growth. Since my last article, earnings have under-whelmed, while forward earnings growth is expected to slip. However, we can probably assume that earnings will bounce into the next global business cycle. So, after a dip in earnings (as projected by the current consensus estimates), I am willing to assume 8% earnings growth in the following year, followed by a gradual drop to 2% in my terminal year (i.e., in six years’ time). I will also assume no forward buybacks, but keep dividends distributing at around 40% of underlying earnings (reinvested).

The net result of these assumptions, with a constant forward earnings multiple, is an IRR of over 14%. That actually implies a substantial undervaluation, as the geographically-weighted risk-free rate (10-year bond yield) is only 3.41% by my calculations, while the weighted country risk premium is only 0.42% (using data provided by Professor Damodaran).

Author’s Calculations

Upside on valuation alone, assuming a fair-value IRR of around 8-9%, would be well over 50%. If we now assume buybacks worth a third of earnings each year on a forward basis, such that the fund’s underlying return on equity is maintained at a high rate of around 19%, our IRR would boost further to about 15.2%. The forward earnings multiple is already low at just 11.29x, so I don’t think we need to adjust this lower to be conservative. In the longer run, it is probable that long-term yields will revert to more subdued levels, which should support earnings multiples generally.

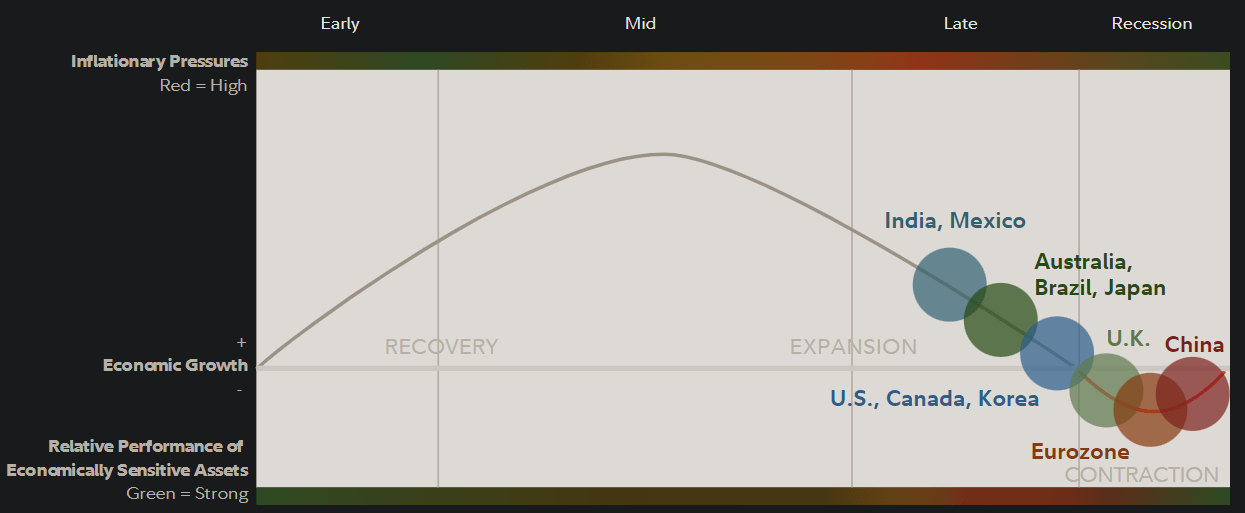

MXI is invested in a classically cyclical sector. Into the next business cycle, it is possible that MXI will out-perform as its already undervalued fund adjusts in line with potentially stronger-than-projected earnings. Fidelity, as illustrated below, currently suggest that the business cycle is in a near-term downturn. While this phase could be protracted, a new business cycle could send MXI earnings upward once again, possibly with some surprise upside.

Fidelity.com

Bear in mind that the current consensus three- to five-year average earnings growth rate that I can get from Morningstar suggests MXI’s portfolio earnings will grow at around 8% per year. My average as projected above is sub-4%. So, even with a fairly modest earnings outlook, MXI offers a headline IRR of possibly as much as 14%. The fund is also well-diversified within its sector, with 104 holdings, and offers a dividend yield of around 3%.

MXI might have struggled to materially out-perform benchmark equity indices given downturn and recessionary concerns. However, as the economy continues to hold up fairly well, it is possible the next business cycle will kick into gear without us ever seeing a serious recession. This could be a boon for stocks and even for commodity prices to which MXI is positively exposed.

Be the first to comment