Justin Sullivan/Getty Images News

What prompted this article?

Recently, my son wanted to buy a new car. I tried to convince him to get a full EV or a PHEV. He ignored my suggestion and bought a full Internal Combustion Engine, ICE, car, a Toyota Corolla Hatchback. His argument was simply: EVs are inconvenient because of charging and are too expensive. The wait time for receiving the car was about 5 months, and he is receiving it this January.

Recently, I read an article in Yahoo Finance talking about Toyota’s (NYSE:TM) president, Akio Toyoda, questioning whether the push for the auto industry to phase out gas-powered vehicles and go exclusively electric is the right decision at this stage. He provided a compelling argument founded on the fact that we do not have a clear vision to the path we should be taking for reaching the zero emissions for vehicles.

I was recently in Montreal, and noticed the large number of cars parked on the street overnight (compared to my neighbourhood in Toronto). This prompted me to think about how people who don’t have a garage and are parking on the street would be able to charge their electric vehicles overnight. I then thought about the grid infrastructure, the charging network and whether we are ready for the electrification of our roads or not.

On my way back from Montreal, I was in the car with a close friend of mine, an electrical engineer, and I asked him about EVs. His response was that it is not the right time for EVs. I asked him when the right time would be, and his response was “Until we harness nuclear fusion, the usage of full EVs as the only types of cars would not make sense; we will use fossil fuels to generate a major part of our electricity.” He was not joking about nuclear fusion, and he explained to me that we might be close to harnessing it.

These and other factors prompted me to research what the future is holding for us, whether it will be strictly full EVs, or PHEVs will have a prominent place in our future. I am sharing the results of my research in this article.

Article Thesis

This article provides the justification that we are not yet ready for conversion to full EVs, and that we may never be in generations to come.

The article starts by comparing the positions that Tesla (NASDAQ:TSLA) is taking together with other auto manufacturers against Toyota’s position regarding the transition from ICE to EVs. The article then addresses how PHEVs can be more environmentally friendly than full EVs for certain types of users, together with the challenges facing the rollout of EVs. Finally, the article shows that Tesla is a unique company and that it will have no choice but to succeed and to thrive despite the flawed vision of its leader. This is justified by the financial analysis that compares the financial projections of both companies.

What is Musk’s Position?

For over a decade, since the first Tesla car, the Roadster in 2008, Elon Musk has been an avid believer that the time is nigh for moving to full electric vehicles. When Musk started his narrative, many critics questioned this vision and outright called him a fraud. Actually, many still call him that but for different reasons.

Tesla committed all its resources to this vision, and have since been vindicated; many auto manufacturers have committed to moving all their production into EVs and all have committed to get into EV manufacturing. Following is the list of companies and their commitments to electrification:

|

Auto Manufacturer |

First Full EV |

Commitment |

|

Aston Martin (OTCPK:AMGDF) |

Due 2025 |

PHEV in 2023 95% EV by 2030 (5% for ICE race cars) |

|

Audi (OTCPK:VWAGY) |

2018 |

Full EV launches after 2026 Full EV only sales in 2030 but only in some markets |

|

Bentley (OTCPK:VWAGY) |

Due 2025 |

PHEVs already available Only PHEV and Full EV by 2026 Full EV only by 2030 |

|

BMW (OTCPK:BMWYY) |

2013 |

50% Full EV by 2030 Investing in hydrogen |

|

Buick (GM) |

Due 2024 |

Full EV only by 2030 |

|

Ferrari (RACE) |

Due 2025 |

No details other than PHEV due 2023 |

|

Fiat (STLA) |

Due 2027 |

Full EV by 2030 |

|

Ford (F) |

2011 |

Full EV in Europe by 2030 40% Full EV in North America by 2030 |

|

GM (GM) |

2013 |

Planning 30 new Full EVs by 2025 No indication as to when they are stopping ICE |

|

Honda (HMC) |

Due 2024 |

40% Full EV or Hydrogen by 2030 80% Full EV or Hydrogen by 2035 100% Full EV or Hydrogen by 2040 |

|

Hyundai (OTCPK:HYMLF) |

2009 |

Full EV in Europe by 2035 Full EV globally by 2040 |

|

Kia (OTCPK:HYMLF) |

Due 2026 |

Full EV in Europe by 2035 Full EV globally by 2040 |

|

Jaguar |

Due 2024 |

Full EV by 2025 |

|

Jeep (STLA) |

Due 2023 |

Planning 5 new Full EVs by 2025 No indication as to when they are stopping ICE |

|

Mercedes (OTCPK:MBGAF) |

2018 |

At least one EV in each segment by late 2022 Full EV by 2030 |

|

Porsche (OTCPK:POAHY) |

2019 |

Planning 2 new Full EVs by 2024 No indication as to when they are stopping ICE |

|

Rolls-Royce (OTCPK:BMWYY) |

Due 2023 |

Full EV by 2030 |

|

Volvo (OTCPK:VOLAF) |

2019 |

50% full EV by 2025 Full EV by 2030 |

Source: Prepared by Author from company Web Sites and Tom’s Guide, Which car companies are going electric and when

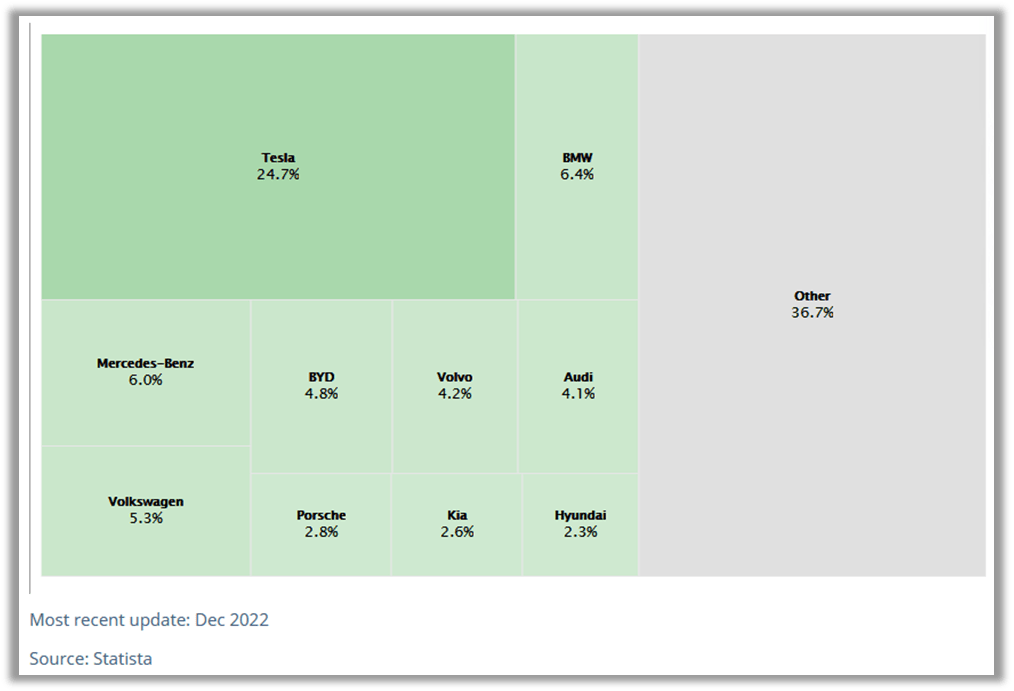

The list of cars above (excluding Toyota which will be discussed separately) represent the most well-known ICE auto manufacturers. There is another slew of companies that are 100% EVs. The following chart shows the dominion of Tesla in the full EV market with about 25% of the overall EV revenue worldwide.

EV Revenue Market Share (Statista)

Just to summarize: Musk’s position is that, despite the competition, the market for EVs is still too big; currently only 13% of the overall new car sales are for full EVs and only 18% of both full EVs and PHEVs. Musk strongly believes that there is no market for PHEVs and the whole world will eventually be only using full EVs. In July 2022, he upped his criticism by suggesting that PHEVs should be phased out.

Toyota Investing $50M in Tesla (Getty Images)

In 2010, Toyota invested $50M in Tesla and they jointly worked on creating the electric RAV-4. In 2016, Toyota created its own electric division. In 2017, Toyota sold its share in Tesla making approximately 10x profit on its investment.

What is Toyoda’s position?

Akio Toyoda, president of Toyota, the largest car manufacturer in the world, has been quite vocal that full EVs are not the only way to go and that different individuals will require different vehicle technologies. He agrees with the industry executives that there is no place for ICE-only cars in our future but is refusing to concede to the popular opinion that full EVs are the only way to go.

“People involved in the auto industry are largely a silent majority;” Mr. Toyoda said to reporters during a visit to the Toyota factories in Thailand. “That silent majority is wondering whether EVs are really OK to have as a single option. But they think it’s the trend so they can’t speak out loudly. Because the right answer is still unclear, we shouldn’t limit ourselves to just one option.”

As a result, Toyota is betting on different technologies including hydrogen and hybrids (both regular and plug-in), a technology it invented with the debut of the Toyota Prius in the 1990s, with a special focus on PHEVs.

And the market is also validating Toyoda’s position. The wait time for PHEVs is the longest for any type of cars, and can reach up to three years for the Toyota Rav-4 PHEV. Car buyers simply want PHEVs more than any other cars.

Still, Toyota is committed to electrifying its model lineup. It has a goal to produce 3.5 million electric vehicles by 2030, which would only be about a third of its current sales. To put this number in perspective, 3.5 million electric vehicles is about three times as much cars as Tesla produces.

What is the target market for PHEVs?

There is a distinct market for PHEV cars, and these buyers would have no incentive to get full EVs if PHEVs are available. Here are the characteristics of a typical car owner who would prefer a PHEV to a full EV:

- The average daily usage is less than 100 KM: With an average daily usage less than 100 KM, the ICE will hardly ever be used resulting in cost savings higher than those of full EVs.

- Cost conscious: PHEV prices are less than the equivalent full EVs because of their smaller battery, the component with the highest cost for EVs.

- Does not always have access to a charging station: Without access to charging station, for example during vacation, the driver can always use the ICE; this provides more flexibility to the driver.

- Time constrained: Filling up gas is much faster than charging a car, and the driver does not have to stop for extended periods for charging the battery during longer trips. We also need to consider the wait time for the charging station to be available. Moreover, charging a PHEV is faster than charging a full EV because of the smaller battery size.

- Environmentally conscious: In the next section, we will present a case for the environmental advantages of PHEVs compared to full EVs.

Individuals with these characteristics represent a good percentage of the market and they cannot be ignored as Musk is suggesting.

Toyota Plug-in Hybrid Car (Getty Images)

Is the PHEV more environmentally friendly than the full EV?

While controversial, I would argue that PHEVs are more environmentally friendly compared to full EVs for passenger cars. Here is the logic for this hypothesis, which applies to the PHEV client base described in the previous section:

Average length of daily trips: According to the US Department of Transportation, the annual average usage of cars is 13,476 miles annually, 37 miles daily, or 60 KM daily. This is significantly lower than the battery capacity of most PHEV cars, which means that the ICE will be rarely used for these cars; this alone makes them at least as environmentally friendly as full EVs.

Weight of the car: A PHEV car is usually much lighter than the equivalent extended range full EV. This extra weight consumes more energy making the EVs less efficient. In addition, EVs are more expensive as it must be equipped with more powerful brakes, suspension and structure. In addition, their tires have a shorter life. Based on the above reasons, PHEVs are more environmentally friendly than full EVs.

Battery recycling issues: There are many challenges associated with the recycling of EV batteries. The industry is still developing, and while recycling Lithium-Ion Batteries, LIBs will eventually be viable economically, we are not there yet. The EV battery reaches its end-of-life for EVs (75% capacity) after 8 years and the vast majority of EVs on the road have not yet hit this point. Unless new technology is developed, within a few years, we will face some significant issues related to EV battery recycling. Because PHEVs have smaller batteries than full EVs, they would require less recycling effort and are thereby more environmentally friendly. In addition, the end-of-life for PHEV cars can potentially be extended to be lower than the 75% capacity because of the ICE availability.

When can we practically completely stop using ICE?

Let me clarify here that I am not against EVs. I am just stating the facts that there are a lot of conditions that need to be fulfilled first before the full electrification of our roads.

Making the assumption that we will be 100% free of gasoline cars in the near future is a statement that does not have solid foundations.

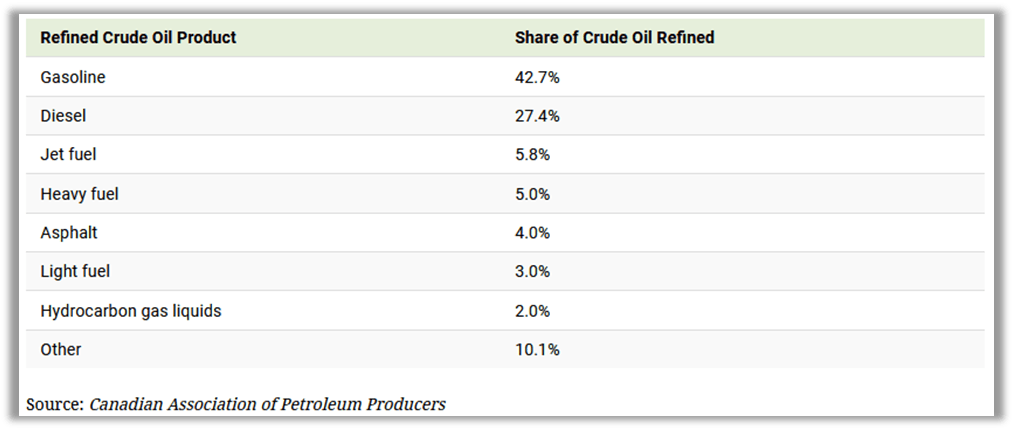

Out of the components of crude oil, only 43% is refined into gasoline, the remaining 57% being refined into other products that range from jet fuel to asphalt to cosmetics. As we continue refining oil, gasoline will always be produced and the gasoline price will drop significantly with the continued electrification of our roads. This will challenge the value proposition of EVs and the transition would not be as rapid as some are leading us to believe.

Products from Refining Oil (Visual Capitalist)

Before the full electrification of our roads, we need to consider the rollout of the charging stations. There is currently no infrastructure that would allow charging cars that are parked overnight on city streets. For big garages (like in apartment building garages), we would need a charging station for every overnight parking spot, which is a huge capital expenditure for these private garages. The overnight charging infrastructure is simply not there, and having it in place will be a long and an expensive endeavour.

Tesla Charging Stations (Getty Images)

Electrifying our streets would require a major overhaul of the grid to support the charging stations. Despite their commitment to build charging stations, I am not sure governments are willing to expedite the building of charging stations given the abnormally high deficits we are currently experiencing. Moreover, these charging stations require an upgrade to the electric grids before their construction, and this dependency would further delay the rollout.

As per the Washington Post, the current electric grid is not ready for the electrification of our roads. The article pegs the cost of the grid upgrade at $125B, which dwarfs the $900M that Biden allocated for building 500,000 charging stations. While the blackouts in California were not directly caused by the EV charging stations, they demonstrate the fragility of our grid and how it may collapse with a perfect storm of high heat, reduced renewable energy supply and increased EV utilization during vacations.

Not all experts agree that the grid is not ready. Some reports indicate that the grid is ready for the rollout of EVs. Here are some of these reports:

I do not agree with the conclusions of these reports and strongly believe that the grid needs to be upgraded.

Sunset of the Power Grid (Getty Images)

Why will Tesla win?

Despite the above challenges that EV rollout faces and the rise of the PHEVs, I still believe that Tesla will thrive and will continue growing more than any other auto company. Tesla is operating in a market that is still in its infancy, and the market for full EVs is huge and growing by the day. Tesla is the clear leader in this market. Tesla is at least five years ahead of any competitor in the following areas:

- Efficiency of the Electric Power Train

- Innovative Batteries

- Usage of AI in Self Driving

- Manufacturing Automation

- Distribution Network

- Support and Maintenance

- Insurance

- Power Storage

- Solar Power Generation

- Integrated Circuit Optimization and Design

These are core competencies that none of the Tesla competitors has come even close to what Tesla has achieved. Elon Musk indicated that Tesla is worth as much as Apple and Saudi Aramco combined and many analysts ridiculed Musk’s statement. However, based on the above core competencies, I believe he was conservative in his estimate.

In October 2021, I wrote an article where I indicated that Tesla is a $3B company. I still believe that the company is worth at least as much despite the current rout that dropped the Tesla stock price by 60% since I published the article. I will not reiterate the justification for my valuation, and I still stand by it.

Do the financials justify Tesla winning?

Based on my analysis, the upside for Tesla is much higher than that of Toyota and this section justifies the reasoning behind this statement that Tesla will be winning.

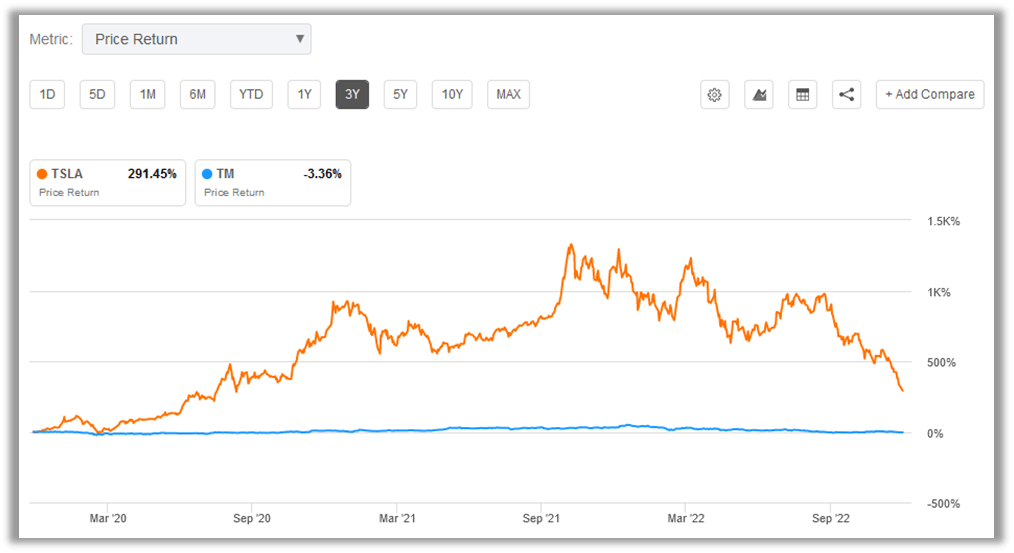

Tesla versus Toyota Share Price Comparison as of 2022/12/27 (Seeking Alpha)

Toyota, over the years, has been a very stable investment, distributing a dividend of 2.9%. Tesla, on the other hand, has given its investors a wild ride as shown in the above chart. The following table shows the comparison between both companies for some key financial performance indicators:

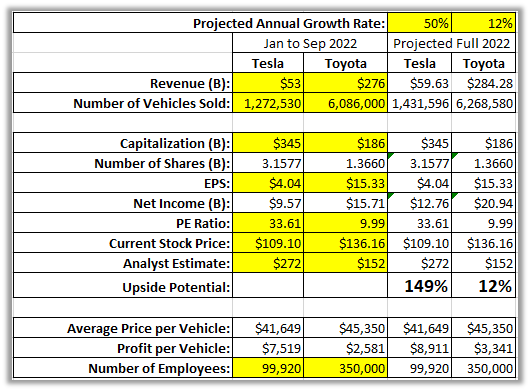

Key Financial Comparison as of 2022/12/27 (Author)

Source: Prepared by Author as of 2022/12/27; Cells in yellow can be modified in the downloadable spreadsheet to provide personalized estimates.

Here is how the data in the above table was derived:

Projected Annual Growth Rate: Tesla projected a 50% compounded annual growth rate. Toyota has been growing at an annualized rate of 12% quarterly over the past three quarters.

Revenue: I took the revenue for each company from January to September 2022, and projected it based on the above growth rate; the year-end for both companies is different and that was the normalized method of comparison.

Number of Vehicles Sold: Projected from the number of vehicles sold for each company from January to September 2022.

Capitalization, Number of Shares, EPS, P/E Ratio: Last Quarterly Reporting per company; no projections.

Current Stock Price: As of 2022/12/27.

Net Income: Annualized based on the last three quarters without applying the growth rate.

Analyst Estimates: Based on the estimates from TD Waterhouse portal as of 2022/12/27; This gives an upside potential of 149% for Tesla and only 12% for Toyota. My analysis next shows that the upside for both companies is remarkably higher than that of the analysts’ estimates.

I did not include the comparison for the price per vehicle, because I believe that the full-year projection is not correct. In the third quarter, Tesla reported $3.29 billion in net profit compared to Toyota earning $3.15 billion with Toyota delivering almost eight times more cars than Tesla during the same time. Tesla’s margin on cars being 8 times as much as Toyota is quite a remarkable achievement and gives them a huge buffer to compete on price if choose to do that. The full year projection puts Tesla at a 3-times the margin per car compared to Toyota, although the average price per vehicle is comparable.

The comparison for the number of employees is not valid either (99K for Tesla and 350K for Toyota) and would need to be adjusted to take into consideration that Tesla has massive vertical integration that Toyota does not have. For example, Tesla manufactures much of its items itself while Toyota outsources the equivalent manufacturing. In addition, Tesla does not have dealers, and all sales and maintenance outlets are Tesla employees, whereas Toyota fully depends on dealerships in its operations.

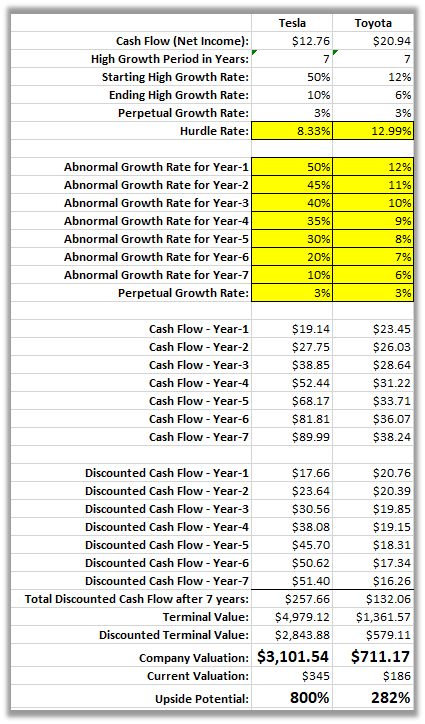

Based on the above numbers, I came up with my own projections and valuations according to the following assumptions:

- Toyota will no longer distribute dividends (its dividend yield is currently 2.91%).

- The free cash flow for both companies is represented by their net income.

- The hurdle rate is two times the current bank rate of 4.33% (8.33%) for Tesla, and three times the hurdle rate for Toyota (12.99%). The difference is because of Toyota’s much higher debt to asset ratio of almost 100% compared to Tesla’s 20%.

- The abnormal growth rate for both companies will continue for 7 years with different rates for each company. I started the abnormal growth rate for Tesla at 50%, Tesla’s projection, versus 12% for Toyota, which is the approximate annual average growth for the last three quarters. Both companies ended up with 3% perpetual growth rate, lower than the 3.4% average worldwide GDP growth rate.

The following table, derived from the spreadsheet that you can download and personalize, shows the parameters for both companies together with the valuations showing that Tesla will be valued at $3B in 7 years whereas Toyota will be valued at around $700M.

Valuation Comparison in Billions as of 2022/12/27 (Author)

Source: Prepared by Author; Cells in yellow can be updated on this spreadsheet to drive the valuation.

Based on the above analysis, Tesla’s valuation will end up being over four times the valuation of Toyota in 7 years, whereas it is currently only 1.9 times the valuation. I believe that both companies have a huge upside for them, and I would be bullish on both of them. However, I expect the ride of Tesla to $3T will be a wild one whereas Toyota will rise quietly but surely to the $700B.

Conclusion

Akio Toyoda, president of Toyota and Elon Musk, Technoking of Tesla have opinions on the future of our transportation are on diametrically opposing each other. Musk believes that full EVs are the only way to go, while Toyoda believes that other technologies like Hydrogen and PHEVs will have a place beside full EVs in the future.

I believe that Toyoda is right and that Musk is wrong about the future of electrification of our roads; there is a market for PHEVs which will always prefer them to full EVs; they are less expensive, more environmentally friendly, save time and provide more flexibility. In addition, we will continue producing gasoline because of the other usages of oil.

While I strongly believe that there is a very strong market for PHEVs and that they will not be phased out as Musk is advocating, I still believe that Tesla has core competencies that are unmatched in the industry; I believe it will eventually be the largest car manufacturer in the world, at least, in terms of net income. My analysis indicates that it will be worth $3T within 7 years. If Musk can pull a magic trick to get the company to sustain its 50% growth longer than my projections, he might be right that “Tesla will eventually be worth more than Apple and Saudi Aramco combined.”

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment