sykono/iStock via Getty Images

Mueller Industries (NYSE:MLI) is the second-largest metal fabrication company in the world. It has a long history and is a serial acquirer that currently has 21 separate subsidiaries.

The categories of industry are piping systems, industrial metals, and climate products. Residential and infrastructure construction are the main industries that consume what MLI produces. Recently, it has cleaned up its balance sheet by selling off some assets and paying down most of its debt.

|

Company |

10-Year Median ROE |

10-Year Median ROIC |

10-Year EPS CAGR |

|

MLI |

14.9% |

9.6% |

22% |

|

-2.6% |

-0.8% |

n/a |

|

|

3.1% |

2.8% |

n/a |

|

|

12.9% |

7.8% |

0.6% |

One of the most impressive aspects of this company is the incremental returns on capital. The payout ratio averages around 10%, which means around 90% of earnings are reinvested at incrementally high rates of return. These returns have been improving over time, so there is a potential for a period of sustainable high returns ahead. Mean reversion should bring these back down eventually, but for the time being, MLI is putting up solid returns on capital

MLI has been paying a dividend since 2004, and buybacks have been minimal and irregular. The industry is inherently capital intensive, but the company has commendably not loaded up with excessive debt. They are in a very healthy position financially to make more acquisitions without over-levering.

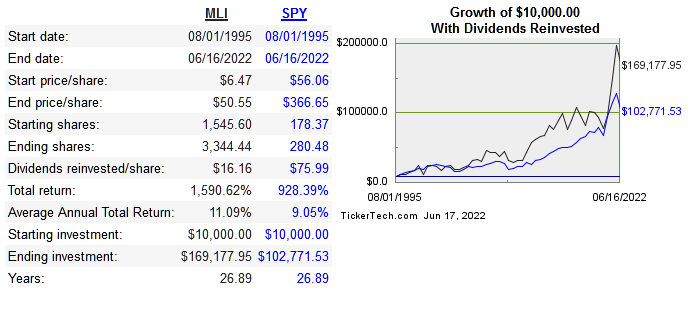

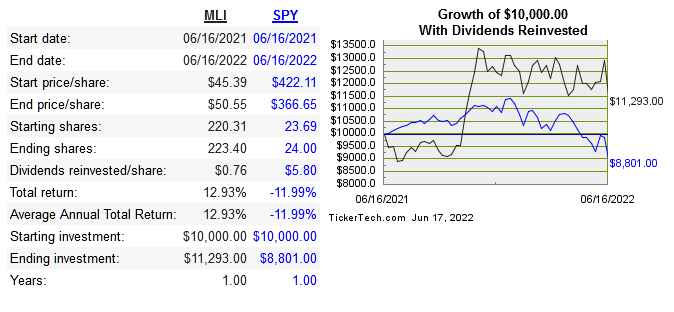

MLI hasn’t had a major correction like so many other stocks, and the industry obviously doesn’t correlate with many others. In spite of the lack of big drawdown compared to so many other names, the company is priced low on a multiples basis, as we will see later.

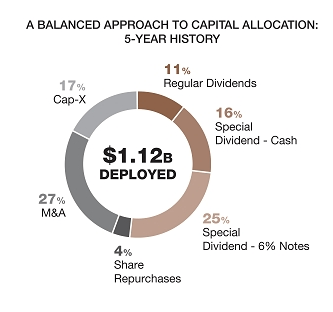

Capital Allocation

Overall, I like the capital allocation decisions and think the more recent strategy sets the company up for success. Selling off some assets, reducing debt, and still making new acquisitions is something.

proxy filing

My preference for returning capital to shareholders is the use of buybacks, but I’m okay with the current dividend policy since they keep a pretty low payout ratio. In spite of some assets being sold off, you can’t say that they have a poor track record of acquisitions. It has been a key driver of value, and it shouldn’t be expected to stop, but most likely will slow down due to size constraints.

Revenue hit an all-time high of 3.76 billion last year, so at this size, I would personally prefer to see a moderately sized buyback plan implemented. Repurchases are only one lever that can be pulled, but right now would be an ideal time, with the P/E ratio sitting in the mid single digits.

Valuation

Whether you use multiples or a DCF, MLI is clearly undervalued.

|

Company |

EV/Sales |

EV/EBIDTA |

EV/FCF |

P/B |

|

MLI |

0.7 |

3.8 |

7.7 |

2.2 |

|

VMI |

1.6 |

14.4 |

-81.2 |

3.3 |

|

ATI |

1.5 |

14 |

-16.5 |

3.8 |

|

ARNC |

0.6 |

7 |

-7 |

2 |

Why should a company with superior operating margins, and returns on capital be rated lower than its peers? The net margin is only this high due to recent asset sales, and should return to normal levels in the 4% range.

|

Company |

Gross Margin |

Operating Margin |

Net Margin |

|

MLI |

23.9% |

19.6% |

14.2% |

|

VMI |

25% |

8.2% |

5.5% |

|

ATI |

14.2% |

5.7% |

0% |

|

ARNC |

11.5% |

-3.9% |

-5.1% |

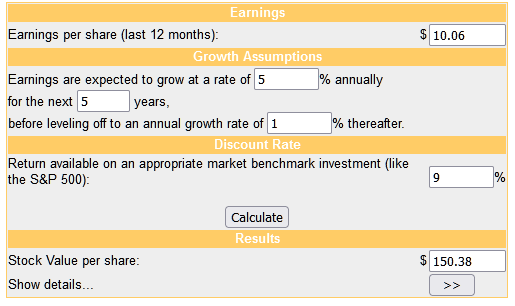

Using what I consider a very conservative DCF (as far as growth estimates), shares are also substantially undervalued.

moneychimp

With a debt/equity ratio of 0.4, there isn’t much risk at all as far as their leverage goes. The biggest risk overall is that their returns on capital will mean revert, while revenue growth slows.

Conclusion

There’s no doubt that MLI is one of, if not, the top companies in its space. They are well diversified within their industry and have been overall successful as a serial acquirer. Net income is temporarily boosted right now, but even as it normalizes, the quality of this business is still high enough to consider owning as a longer-term compounder. Current prices make it quite compelling. I really think the quality of earnings here isn’t being recognized.

Be the first to comment