M. Suhail

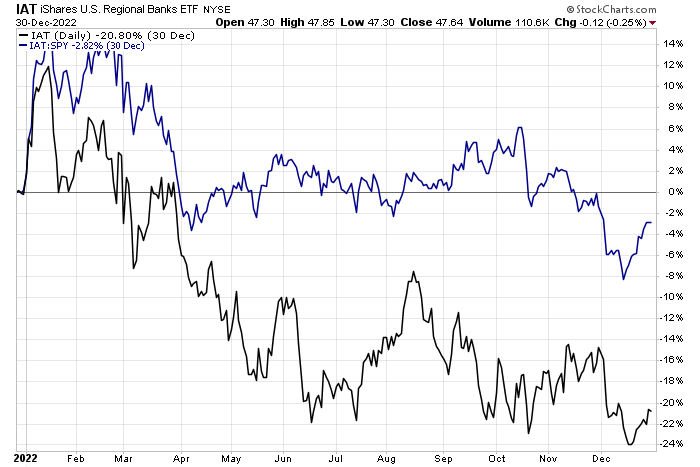

Regional banks had a topsy-turvy 2022. The relative performance of the iShares U.S. Regional Banks ETF (IAT) was hot during the first two months, but then the economically sensitive group underperformed the broad market from late February through mid-December. A rise in rates during the back half of last month helped IAT.

One of its components, M&T Bank, was volatile on its own with very poor performance in the final quarter of 2022. Is the stock a value now ahead of earnings mid-month? Let’s check it out.

Regional Banks Pop & Drop In 2022

Stockcharts.com

According to Bank of America Global Research, M&T Bank Corporation (NYSE:MTB) is based in Buffalo, NY, with $200 billion in total assets and a branch network that spans the Mid-Atlantic. The company’s lending portfolio focuses primarily on Commercial RE, residential real estate, and C&I.

The $25.0 billion market cap Banks industry company within the Financials sector trades at a somewhat low 13.7 trailing 12-month GAAP price-to-earnings ratio and pays an above-market dividend yield of 3.3%, according to The Wall Street Journal.

Back in October, MTB issued a significant earnings miss while revenues also fell short of analysts’ expectations. The stock traded down after that report. After the tough quarter, M&T tapped an executive at rival Truist to be its next CFO to hopefully right the ship. Also, perhaps helping to lift shares off recent lows, the firm sold its Collective Investment Trust to Madison Dearborn as a divestiture. M&T has strong cash levels going into 2023 which should help its net interest margin performance, but that also means the stock could be tied to how the yield curve changes. Its commercial real estate portfolio is a possible risk this year, too.

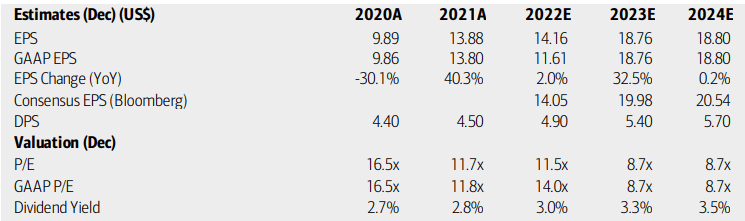

On valuation, analysts at BofA see earnings having risen just 2% in 2022 but then surging more than 30% this year with stagnant per-share profit changes seen in 2024. The Bloomberg consensus outlook is actually a bit more upbeat than what BofA expects. Dividends, meanwhile, are forecast to rise commensurate with EPS. Both MTB’s operating and GAAP P/Es should retreat to the high single digits should the stock price hang where it is. Overall, I like the valuation outlook given the growth in the coming quarters, but there are macro risks at hand.

M&T: Earnings, Valuation, Dividend Forecasts

BofA Global Research

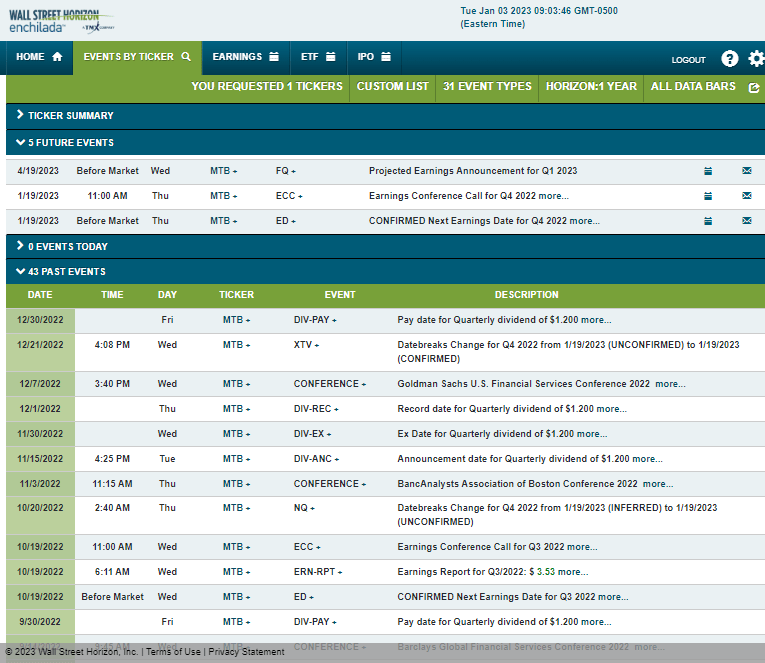

According to corporate event data provided by Wall Street Horizon, MTB has a confirmed Q4 2022 earnings date of Thursday, January 19 before market open with a conference call later that morning. You can listen live here. The following projected reporting date is Wednesday, April 19.

Corporate Event Calendar

Wall Street Horizon

The Options Angle

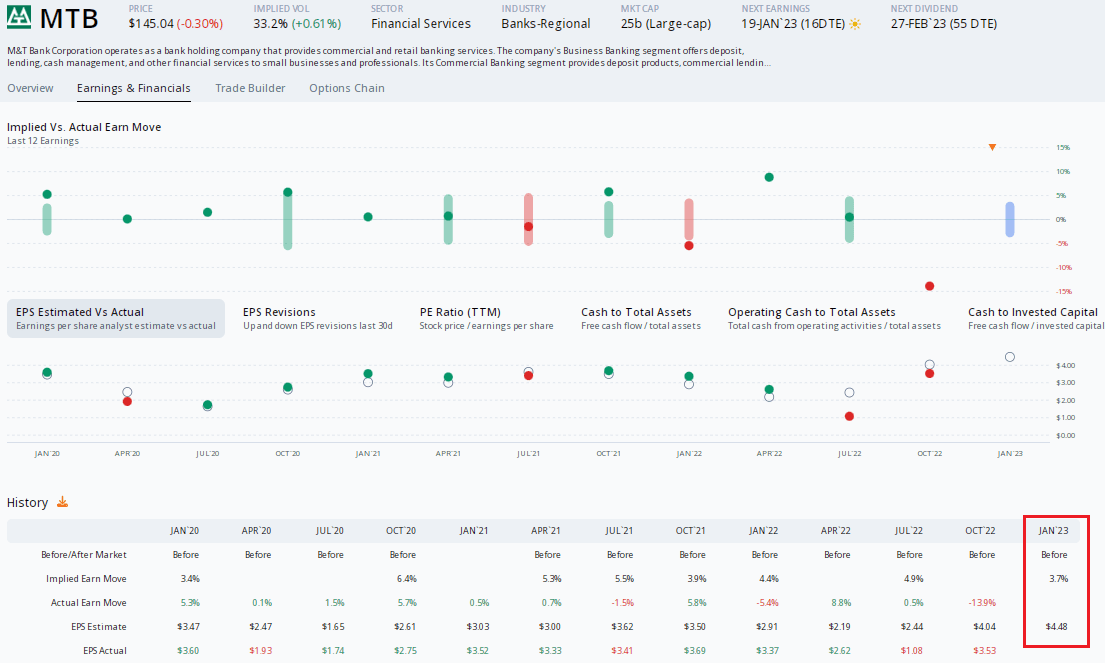

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS forecast of $4.48 which would be a strong 33% rise from $3.37 of per-share profits earned in the same period a year ago. Since reporting in October, there has been one analyst EPS upward revision for MTB.

Options traders, meanwhile, have priced in a modest 3.7% earnings-related stock price swing using the at-the-money straddle that expires closest to the earnings report. With implied volatility at 33.2%, it is not an overly volatile stock despite a steep 13.9% decline after the Q3 report in October. The firm has a mixed beat rate history. Overall, the options appear cheap with that level of premium. But what direction should you take? Let’s analyze the chart.

MTB: Low Implied Volatility Ahead Of Earnings, EPS Growth Expected

ORATS

The Technical Take

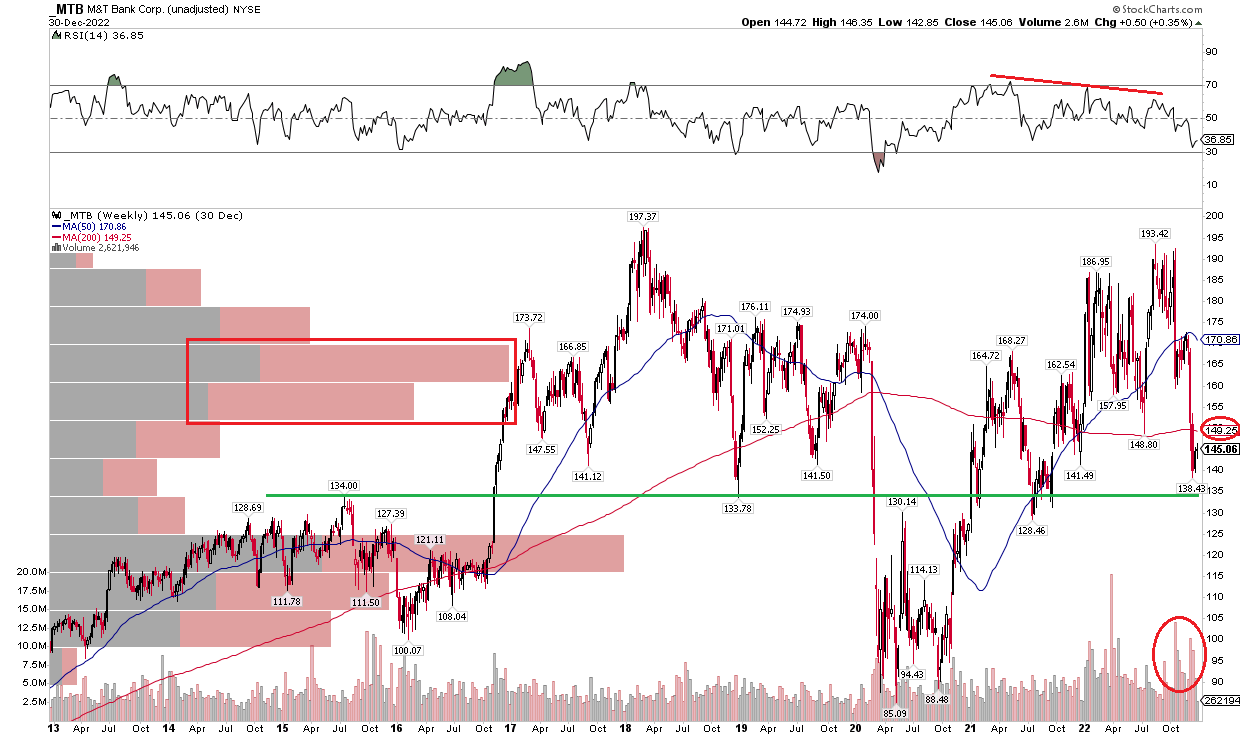

I went long-term on the chart of MTB. Notice in the 10-year weekly view below that shares are near important support around the $133 to $142 range. The stock ended last year at $145, bouncing off $138. Notice, though, that RSI on the weekly chart showed a series of lower highs as the stock rose – that was bearish divergence, and the shares resolved back down to support. The 200-week moving average, meanwhile, is simply sideways, indicative of a messy and trendless trend. Finally, there has been high volume on recent weekly declines which I don’t like. Overall, the technical picture is mixed but a long bias is perhaps warranted given the pullback to support.

MTB: Shares Bounce Off Key Support, But Overhead Supply Remains

Stockcharts.com

The Bottom Line

MTB is not a picture-perfect play, but the valuation is low, and its yield is decent. Technicals are mixed, but the stock appears to be bouncing off support. Long here with a stop under $130 seems to make sense ahead of earnings later this month.

Be the first to comment